LMT - Lockheed Martin: A Huge Moat 10% Annual Return Potential And Protection Against Mayhem

2023-12-28 04:58:58 ET

Summary

- Lockheed Martin is a top value stock with a strong total return outlook, making it a good investment choice.

- The global geopolitical situation is becoming more volatile, increasing the importance of defense and inflation-protection investments.

- Lockheed Martin's focus on advanced military aircraft, missile defense systems, and space programs positions it for growth and makes it an attractive long-term investment.

Introduction

53%. That's how much industrial exposure I have in my dividend (growth) portfolio, which holds almost my entire net worth.

The S&P 500 has just 9% industrial exposure.

Although industrial exposure is very cyclical, I have limited the cyclical risks of my portfolio, as more than half of my industrial exposure consists of defense companies.

Roughly 26% of my portfolio consists of four aerospace and defense companies, led by Lockheed Martin ( LMT ), which accounts for 8.2% of my total portfolio value, making it my largest investment.

My most recent coverage of the stock was on September 18, when I wrote an article titled Fortress Of Dividends: Lockheed Martin's 3% Yield Is Among The Best Money Can Buy .

Essentially, my thesis has always been based on the ability of defense companies to generate anti-cyclical revenues, with growth being provided by their ability to innovate.

After all, I'm buying defense to get anti-cyclical technology exposure, not to hope for wars to make me money.

However, in light of current developments, I believe it is important to focus on high-quality value stocks like Lockheed Martin. As I wrote in my 2024 outlook , I believe that market valuations are a reason to opt for value stocks.

On top of that, we're witnessing that the global geopolitical situation is turning into a volatile and dangerous mess.

This year, for example, we discussed the ongoing war in Ukraine in numerous articles. In September, we also had to include the horrendous attacks on Israel and the war that followed.

Although I refrain from predicting geopolitics, we're clearly seeing that a focus on defense companies may not be the worst bet.

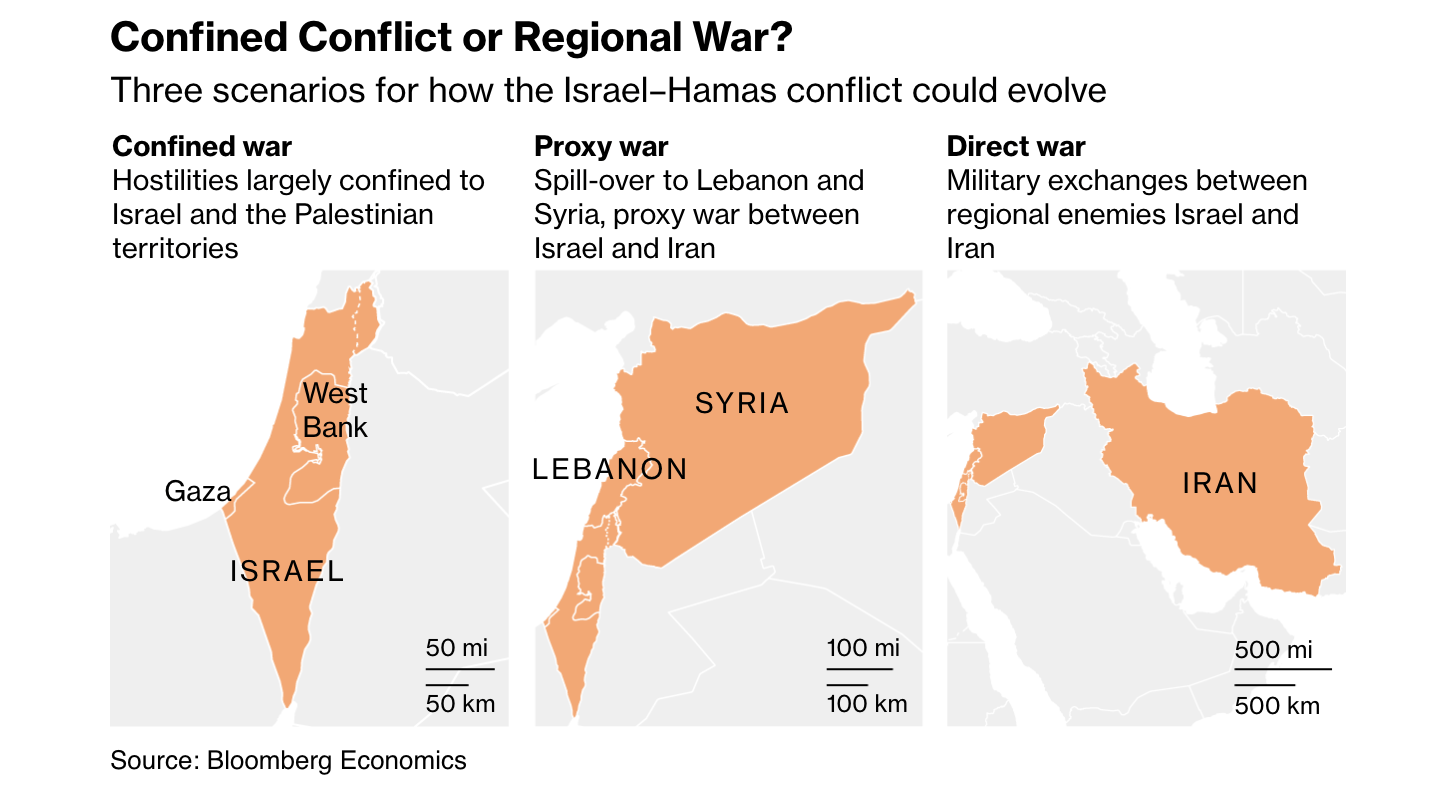

For example, on December 26, Bloomberg reported that the situation in the Middle East is slowly but steadily escalating.

{kind=link}

Bloomberg

According to the article, the recent events in the Middle East signal a potential expansion of conflict beyond Gaza, raising concerns about regional stability.

Experts warn that the longer the Israeli-Hamas conflict persists, the higher the risk of escalation.

Essentially, they make the case that the Biden administration faces challenges in supporting Israel against Hamas while urging restraint in Gaza.

Meanwhile, Israel perceives the conflict as a "multi-front war," having faced attacks from multiple arenas, including Gaza, Lebanon, Syria, the West Bank, Iraq, Yemen, and Iran.

As a result, the Biden administration deploys aircraft carrier strike groups to deter Iran-backed forces and supports Israel in its battle against Hamas.

{kind=link}

Bloomberg

Again, while I'm not trying to make concrete predictions, I believe we are seeing the start of a prolonged period of instability that requires a bigger focus on defense and inflation-protection investments.

Not only is the situation in the Middle East a tinderbox, but we are also seeing that OPEC (led by Saudi Arabia) is using its regained pricing power to keep oil prices high. China is threatening Taiwan, Russia is benefitting from lower Western support for Ukraine, and Europe is still figuring out how to reorganize its defense.

That's where Lockheed comes in, which is one of my favorite value plays with a good total return outlook.

A Well-Diversified Aerospace Player

When it comes to defense investing, I like a number of stocks and have a hard time picking a favorite, especially when it involves a lengthy holding period.

To me, however, one thing is clear: Lockheed is one of the best in the business.

For example, its F-16 plane is still one of the best jets in the world after more than five decades in service.

On top of that, it has a massive portfolio of advanced hardware and services.

The best example may be the company's Aeronautics segment, which stands out as a leader in the research, design, and development of advanced military aircraft.

Notably, the F-35 Lightning II program, which accounts for roughly a quarter of the company's total sales, stands out as an advanced program that combines thousands of suppliers and serves as the backbone of America's and its allied defense capabilities.

{kind=link}

Lockheed Martin

Meanwhile, the Missiles and Fire Control segment solidifies Lockheed Martin's position in air and missile defense systems.

Key programs like Patriot Advanced Capability-3 (PAC-3) and Terminal High Altitude Area Defense ("THAAD") demonstrate the company's expertise in developing advanced defensive missile systems that are currently a lot in the news due to their use in the Ukraine war and/or because they are on the buy list of many allies.

{kind=link}

Breaking Defense

This segment also includes hypersonic solutions, like the one mentioned in the headline above.

Speaking of advanced defense solutions, Lockheed Martin is one of the biggest players in the space industry. On top of owning half of the United Launch Alliance, it is also working on programs like the Space Based Infrared System ("SBIRS") and the Trident II D5 Gleet Ballistic Missile ("FBM").

The only segment I haven't mentioned yet is its Rotary and Mission Systems segment, which includes products like the Black Hawk, Seahawk, and CH-53 helicopters.

Lockheed Martin Is Poised For Growth

The past few years have been challenging for Lockheed and its peers. Defense contractors struggled with post-pandemic supply chain issues, labor shortages, inflation, and budget uncertainties.

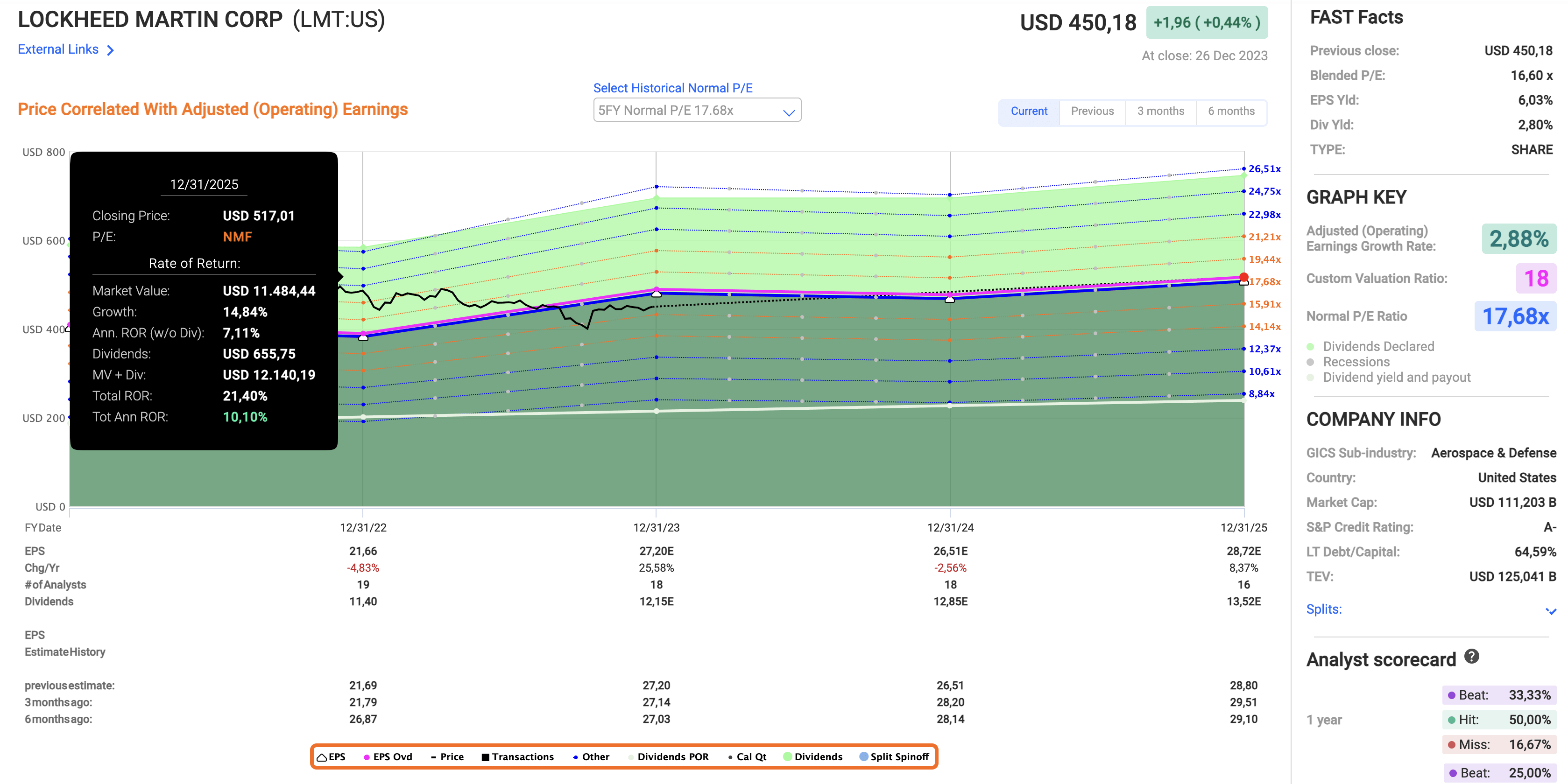

For example, last year, the company saw a 5% EPS contraction. This year is expected to see 26% growth. Next year, EPS is expected to decline by 3% again before potentially rebounding by 8% in 2025. All of these numbers can be seen in the overview below.

{kind=link}

FAST Graphs

However, even based on these volatile numbers, the company could return north of 10% per year, which is based on an 18x EPS multiple (its five-year normalized multiple is 17.7x).

For example, during its third-quarter earnings call, the company noted strong demand for its F-35 program, with the delivery of 30 aircraft in Q3 and a total of 80 for the year.

Continued international interest, as seen in contracts with Denmark, the Czech Republic, South Korea, and Israel, underscores the program's global growth potential, which should continue to benefit from a bigger emphasis on defense spending in the years ahead.

Meanwhile, Lockheed Martin's focus on 21st Century Security initiatives, such as the AIR6500 program in Australia, the Defense of Guam award, and a $1 billion contract for integrated combat systems, positions the company at the forefront of advanced technologies and international collaborations, creating avenues for future growth.

For example, the RMS business, exemplified by the Sikorsky CH-53K helicopter program, secured a $2.7 billion contract for 35 additional helicopters, indicating substantial growth opportunities.

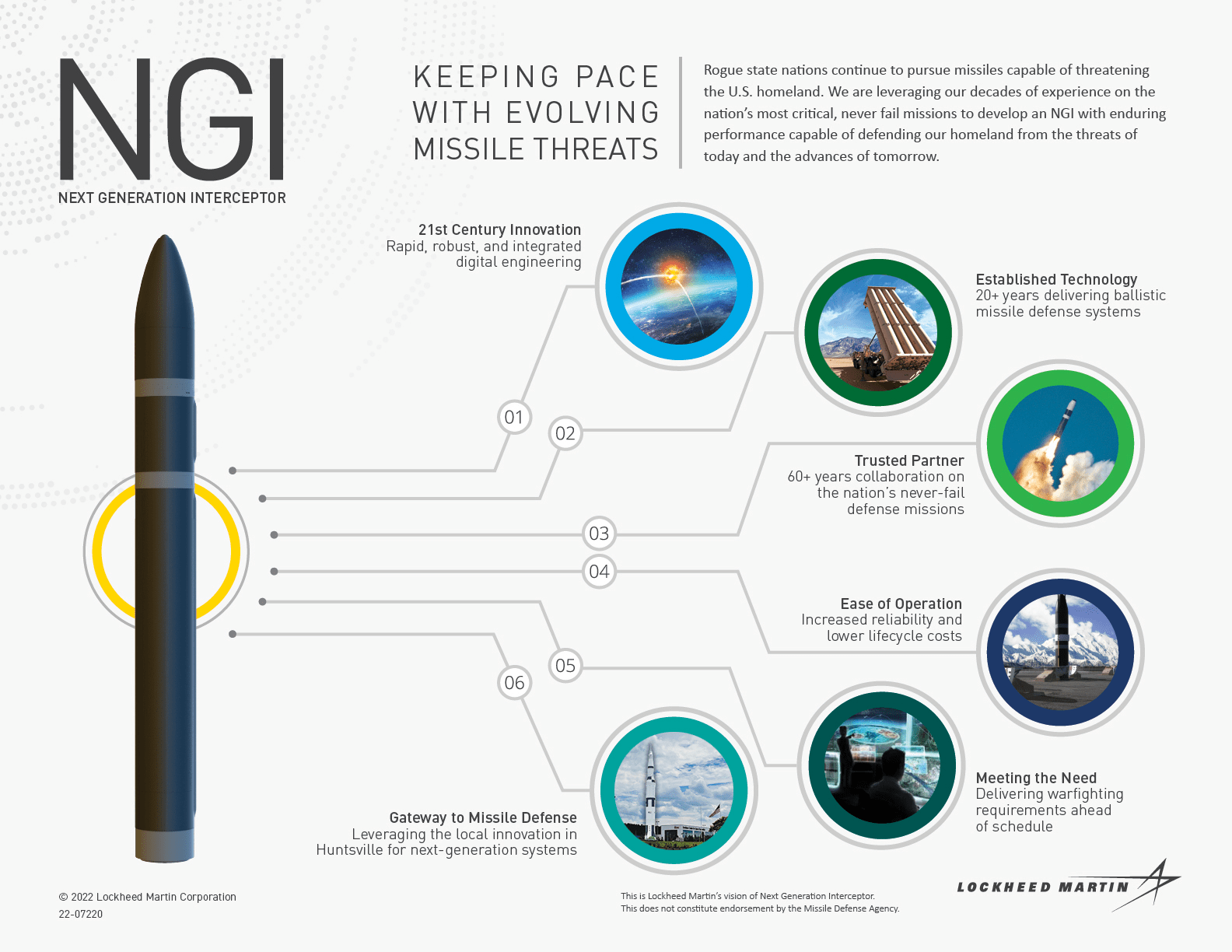

Furthermore, Lockheed Martin's success in the space sector, particularly the Fleet Ballistic Missile Program and the NGI program, highlights sustained growth potential.

{kind=link}

Lockheed Martin

For its NGI program, the company is spending millions on new capabilities in its Northern Alabama facility.

Adding to that, the $1.2 billion contract for the Navy's Trident II D5 life extension and the successful digital preliminary design review of the NGI program reinforce Lockheed Martin's strong position in the space sector, which was one of the best sectors in its third quarter.

In the third quarter, space revenue grew by 8%, while the space backlog grew to over $30 billion, supported by the Transport Layer Tranche 2 award for 36 beta satellites.

With that said, during its third quarter, the company did not give official 2024 guidance.

However, it anticipates low single-digit sales growth, highlighting its strong backlog position as a supporting factor.

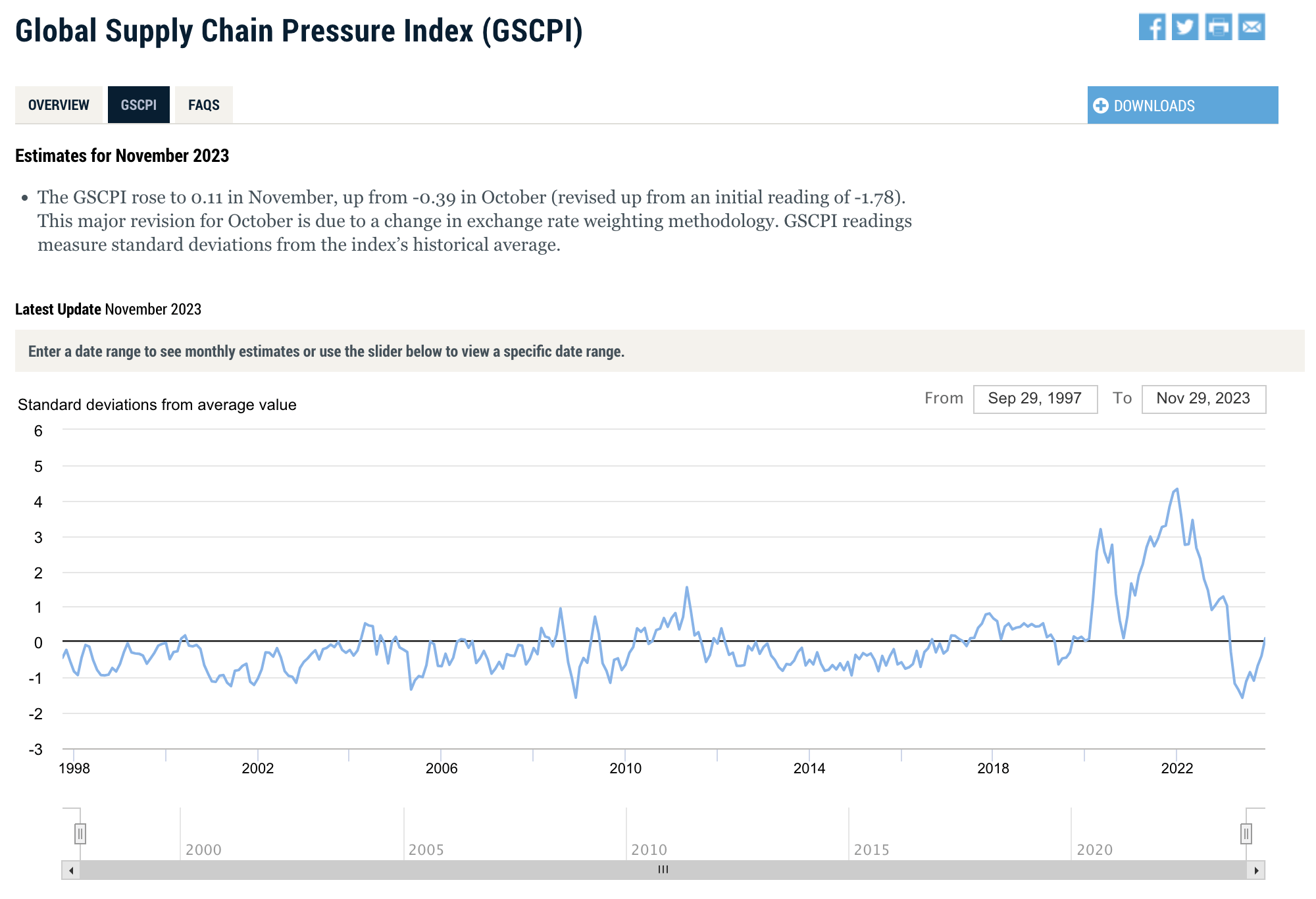

Unfortunately, but not unexpected, challenges were noted, including extended lead times that have yet to compress, impacting the value chain.

The good news is that the Global Supply Chain Pressure Index has normalized, which should help the company bring its supply chains back to "normal" in 2024.

{kind=link}

Federal Reserve Bank of New York

I also expect that general economic weakness will result in less competition for advanced supplies, making it easier for Lockheed and its peers to procure valuable input goods at attractive prices.

After 2024, Lockheed will likely see a favorable mix of strong demand and easing supply chain issues, which is highly favorable for investors as well.

Lockheed's Shareholder Distributions

The third quarter was a perfect example of LMT's ability to reward investors.

Free cash flow was strong at over $2.5 billion, representing 150% of net income.

The company returned 99% of free cash flow through dividends and share repurchases.

Year-to-date, almost $5.3 billion has been returned.

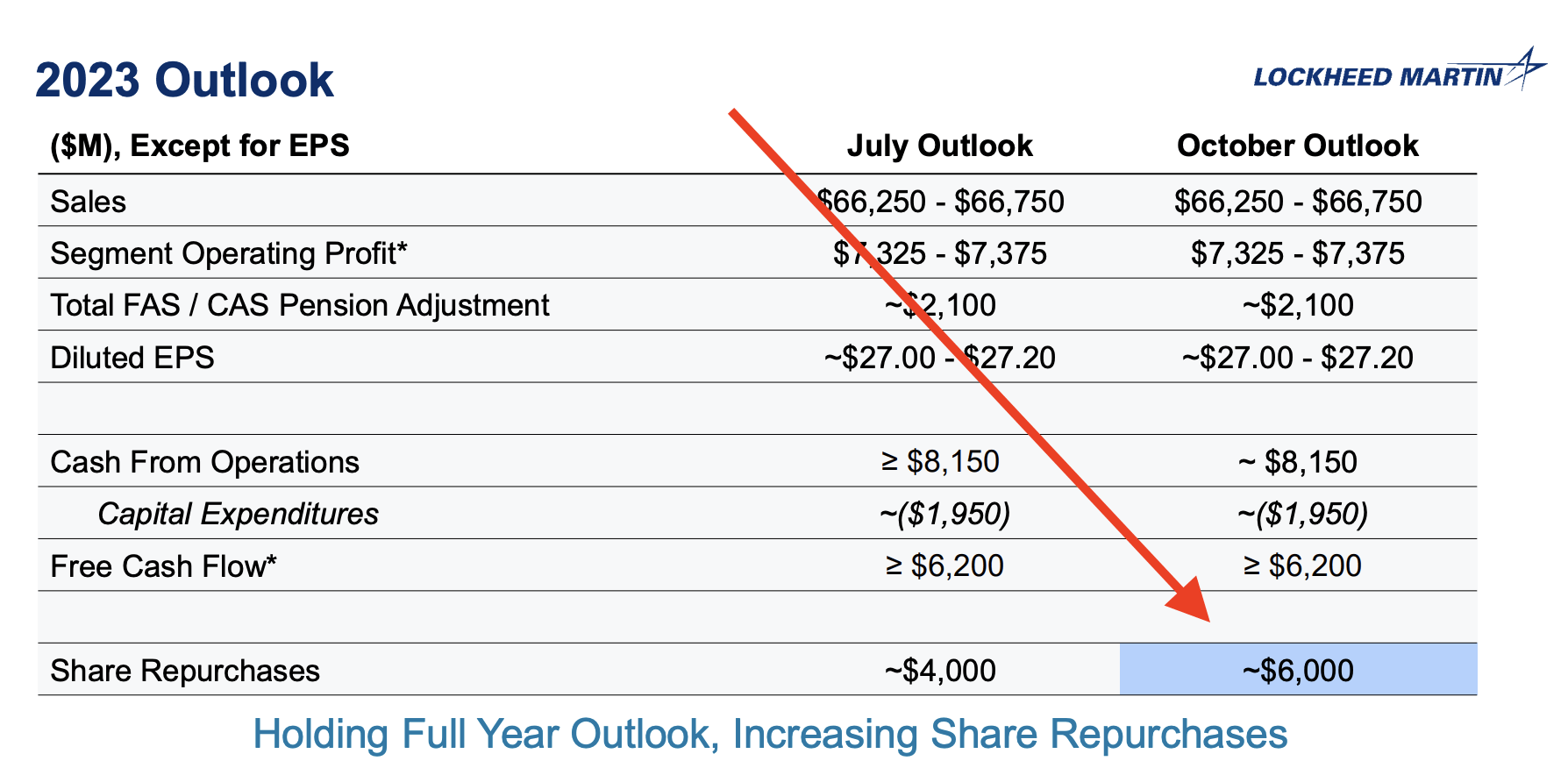

On top of that, the Board approved a 5% increase in the quarterly dividend and an additional $6 billion in share repurchase authorization!

{kind=link}

Lockheed Martin

The company's 2023 buyback program translates to roughly 5.4% of its market cap.

Because the company has a credit rating of A-, which is extremely healthy and backed by a 1.6x net leverage ratio, it does not need to prioritize debtholders over shareholders, meaning it can (and plans to) distribute almost every penny of free cash flow to shareholders.

As the company aims to generate roughly $6.3 billion in free cash flow, it can distribute between 5% and 6% of its current market cap in dividends and buybacks over the next few years.

Over the past ten years, LMT has bought back a fifth of its shares. During this period, it has hiked its dividend by roughly 140%.

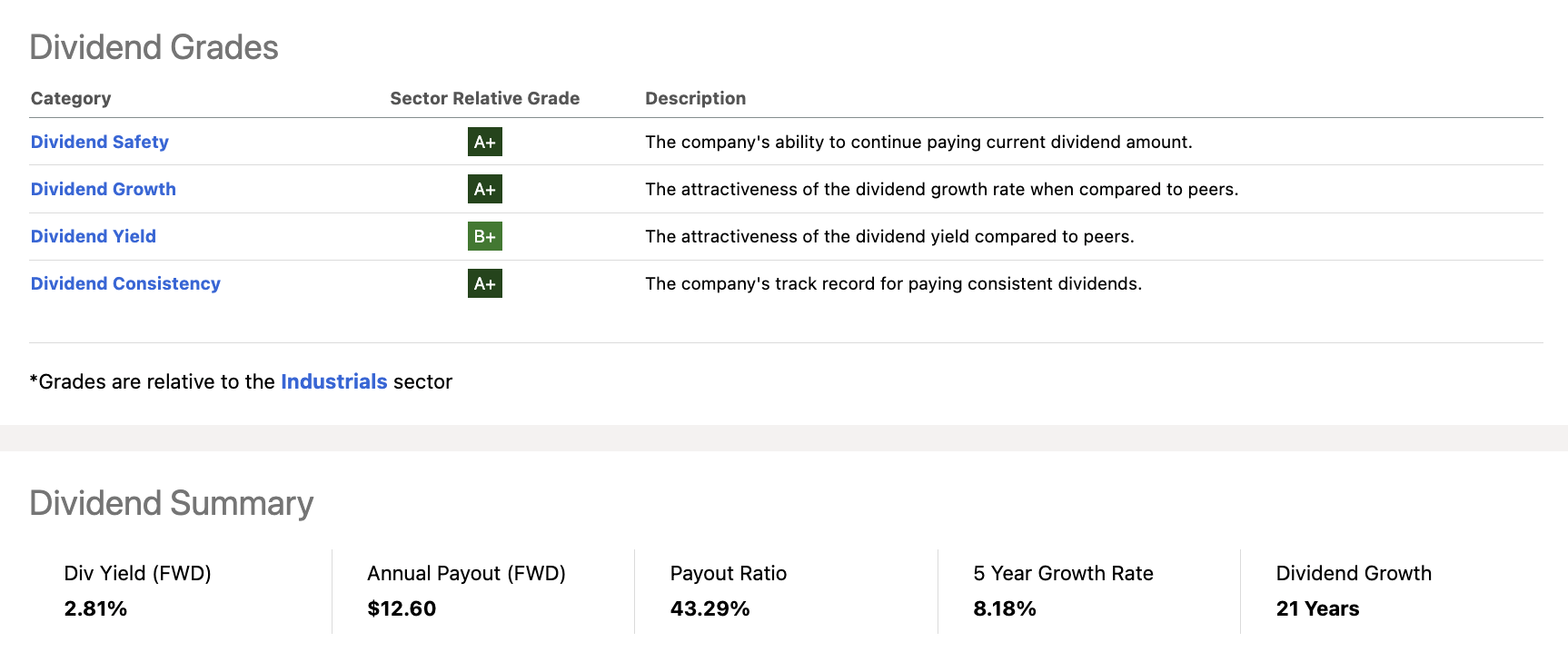

The dividend, which currently yields 2.8%, has a low-40% payout ratio and a five-year CAGR of 8.2%.

Lockheed has hiked its dividend for more than 20 consecutive years, which underscores its stability and safety during recessions.

In general, it has one of the best dividend scorecards in its sector, as evident by not one but three A+ scores for safety, growth, and consistency!

{kind=link}

Seeking Alpha

This dividend is a big part of the >10% annual return projection.

Also, note that LMT has returned 12% since 2013, which makes the aforementioned >10% annual return projection very realistic - especially in light of its $156 billion backlog, strong demand, and fading cost headwinds.

Furthermore, despite headwinds, LMT shares have returned close to 300% over the past ten years, which is significantly more than the already stellar 210% return of the S&P 500.

All things considered, I'm glad I made the decision to make LMT a huge part of my portfolio.

If I get the chance, I will gladly add more shares during corrections in 2024.

Takeaway

I believe Lockheed Martin is a standout long-term investment due to its strategic focus on anti-cyclical products and services.

The company's leadership in advanced military aircraft, missile defense systems, and space programs positions it at the forefront of global security and technology.

Despite challenges, Lockheed's strong financial performance, consistent dividend growth, and shareholder-friendly practices make it an attractive choice.

Meanwhile, the company's resilience in navigating uncertainties and its commitment to cutting-edge initiatives underscore its potential for sustained growth, making it a cornerstone in my long-term investment portfolio and one of the reasons why I expect to sleep well in 2024.

For further details see:

Lockheed Martin: A Huge Moat, >10% Annual Return Potential, And Protection Against Mayhem