RTX - Lockheed Martin: A Solid Bet On The Future Of Defense And Aerospace (Rating Upgrade)

2024-01-09 11:49:30 ET

Summary

- Lockheed Martin is a leading defense and aerospace company with a competitive range of defense programs.

- The firm has seen mostly flat financial performance in FY23, but increasing global defense spending could drive substantial future growth.

- Shares of Lockheed appear to be modestly undervalued by around 12% in a base-case scenario.

- Buy rating issued.

Investment Thesis – Q3 FY23 Update

Lockheed Martin ( LMT ) is the leading defense and aerospace company in the U.S. The firm has a massive and competitive range of defense programs that have proven hugely popular both in the U.S. and in NATO and allied forces own defense programs.

A mixed FY23 has seen the firm generate around 5% revenue growth with overall margins remaining mostly flat YoY. However, with increasing geopolitical conflicts spurring governments across the globe to increase their defense spending, Lockheed could be well positioned to generate some substantial growth in the coming years.

Nonetheless, shares appear to be at a modest 12% undervaluation considering a base-case scenario with a bear-case valuation model leading to a fair valuation estimate for shares.

Therefore, I upgrade my rating for Lockheed from a Hold to a Buy with a Strong Buy rating only being assignable once a larger margin of safety appears in the valuation of Lockheed shares.

Company Background

Lockheed Martin FY23 Q3 Presentation

Lockheed Martin is an American aerospace, arms and defense company headquartered in North Bethesda, Maryland. Lockheed is the clear leader of the defense industry which is reflected by a significant portion of revenues coming from military focused sales and the firm’s massive reach within the U.S., NATO and allied forces defense agencies.

A majority of Lockheed’s resources are currently focused on their F-35 multirole combat stealth fighter jet along with their hypersonic missile and missile defense equipment programs. Most of the contracts associated with these programs are multi-year agreements which guarantee Lockheed significant stability in revenue prediction.

Thanks to the immense vertical and horizontal integration achieved by the company, the firm is able to profit from multiple different aspects of their arms and defense programs. This helps to diversify cashflows and create a company which continuously generates significant profits.

Recent increases in geopolitical tensions and the rising threat of nations such as Russia, China and Iran becoming increasingly disruptive has led to significant increases in defense spending which ultimately should help further boost demand for almost all of Lockheed’s products and services.

Economic Moat – Q3 FY23 Update

Lockheed Martin has an almost unrivalled level of industry knowledge in the arms and defense sector. Their simply massive scale and historical expertise has allowed the firm to develop a wide and robust economic moat.

For a more in-depth analysis of Lockheed’s economic moat, please refer to my previous article here .

Since my initial in-depth review, Lockheed has only further strengthened their economic moat primarily thanks to perfected product execution and an increasing appetite for defense budget spending by nations.

Fundamentally, Lockheed’s massive economic moat arises from their technological advantage compared to competing defense contractors and from their massive scale providing unparalleled influence within defense departments across allied forces and NATO members as a whole.

It would be essentially impossible for any competing defense contractor to match Lockheed’s scale within the defense industry as the capital, time, labor and government support required to achieve such a feat would essentially be impossible to attain.

Lockheed has arguably spent the last half-century fortifying their position as the leading defense contractor with a huge range of equipment ranging from intelligence gathering tools to fighter jets, hypersonic missiles and all the way to space-related products.

This holistic approach has allowed Lockheed to develop their four distinct operational areas: Aeronautics, Missile and Fire Control ((MFC)), Rotary and Mission Systems (RMS) and Space.

The recent increase in geopolitical tensions has only bolstered Lockheed’s position within the defense industry with a huge number of their products being relied on across the U.S. and NATO member nations.

Many of Lockheed’s products are currently being utilized by Israel and Ukraine in their battles against Hamas and Russia respectively with increased spending on defense equipment by allied forces only further fueling demand for Lockheed’s equipment.

While such a rise in demand is ultimately out of Lockheed’s control, what must be noted is the work Lockheed has put in to fully reap the benefits of this increased appetite for defense equipment.

Lockheed Martin | Aeronautics

Equipment such as the F-35 program, AIR6500 integrated air and missile defense program, GMLRS and HIMARS along with the PAC-3 defense programs have proven to be truly world class defense programs which ultimately have allowed Lockheed to gain an even greater share of the total budget currently being spent on defense across the globe.

{kind=link}

While the Space operational segment continues to generate the least margin for the firm (operating at around 8% OM), I fully believe Lockheed will be able to reap massive returns from this business over time.

Lockheed are experts at profiting from their defense programs. While some incredibly complex programs such as the F-35 fighter jet may be delayed and face significant cost overruns, the long useful lifespans of these programs almost always offset any initial losses made during the development phase of the project.

Furthermore, the U.S. government provides Lockheed with truly massive contracts both in terms of volume and fiscal might which ultimately provides the firm with another massive form of competitive advantage. The tightknit relationship between Washington and Lockheed is almost impossible to replicate even for the other major five U.S. defense contractors.

Overall, the incredible diversity, reach and specificity of each of Lockheed’s business segments combined with their absolute advantage over the competition in contract negotiations earns Lockheed one of the widest moats of any firm in existence in my view.

I still rate Lockheed as having a wide and robust economic moat and believe the firm will enjoy significant growth in the coming 5-10 years as a result of the almost unprecedented spending on defense budgets across the U.S., NATO and allied forces.

Financial Situation - Q3 FY23 Update

Lockheed Martin has 5Y (FY22-FY18) average ROA, ROE and ROIC of 12.34%, 218.26% and 36.31% respectively. These returns are truly remarkable and impressive both from a relative perspective in the defense industry and from an absolute comparison against all other forms of business.

I fundamentally believe that Lockheed is well positioned to further expand these returns as a result of the massive military spending packages currently being proposed across the U.S. and NATO member countries in response to increasing threats from Russia, Hamas and China.

Lockheed’s WACC is currently 5.56% which illustrates just how effectively the firm is able to generate tangible returns on their investment compared to the cost the company endures to raise the capital needed for said investment.

The massive 10% margin between ROIC to WACC helps support my earlier thesis that Lockheed are experts at extracting profits even from massively costly and complex defense programs.

Furthermore, when comparing Lockheed’s returns to those of their primary defense industry competitors Honeywell ( HON ), Raytheon ( RTX ) and Northrop ( NOC ) Grumman, the firm handily outpaces these rivals by around 5-8pp in ROA, ROE and ROICs respectively.

Lockheed has 5Y average (as measured from FY22-FY18) gross, operating and net margins of 13.32%, 13.33% and 9.75% respectively. While these figures are healthy and have remain essentially unchanged for the better part of a decade, Lockheed does fall behind some rivals such as Honeywell and Northrop Grumman who have managed to generate larger margins for their respective defense programs.

This is where I believe the recent cost overruns of multiple projects and significant funding of R&D related to “next-generation” weapons programs has hurt Lockheed’s margin expansion. However, given that Lockheed’s margins are so stable, it can be deduced that the management team at the company believes they have found the perfect balance between immediate profitability and long-term industry outperformance.

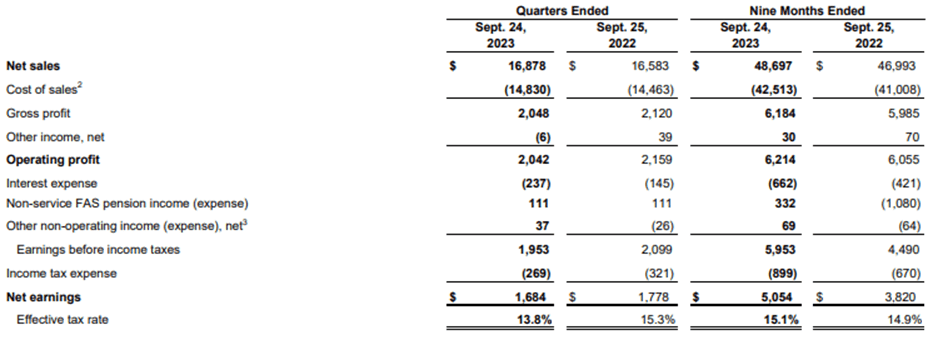

By taking a look at Lockheed’s Q3 FY23, it is clear to see that the firm has had a slightly mixed fiscal year so far from the perspective of earnings releases.

{kind=link}

Q3 FY23 saw Lockheed grow net sales by 2% YoY while COGS grew by 2.7% in the same period. This left gross profits slightly lower YoY at just $2.05B compared to $2.12B the year prior with the total nine months ended September 24, 2023, still seeing Lockheed grow gross profits by 3% YoY.

{kind=link}

Lockheed’s Aeronautics business segment continued to generate the most revenues for the firm despite a 5% decrease in total net sales YoY in Q3 . This slight drop was primarily due to lower net sales for the F-35 program and a $325M sales deferral from Q2 FY22 until additional contractual authorization and funding was found on the Lot 15 contract.

Overall Lockheed’s aeronautics business division has generated essentially flat results YoY considering the first nine months sales data with operating margins remaining essentially constant at around 10.5%.

{kind=link}

The firm’s next largest business segment by revenue was the Rotary and Mission Systems division. Here, Lockheed saw tangible net sales growth of 9% YoY thanks to increased demand for essentially all of their RMS products.

Lockheed’s integrated warfare systems and sensors (IWSS) programs saw increased demand due to new program ramp up (Defense of Guam, Indirect Fire Protection Capability High Energy Laser (IFPC-HEL) and TPY-4 programs) and higher volume (Aegis) along with higher net sales of $60 million on C6ISR (command, control, communications, computers, cyber, combat systems, intelligence, surveillance, and reconnaissance) programs due to higher volume.

Despite the massive demand for such mission critical equipment, Lockheed was unable to expand their operating margin as a result of unfavorable COGS increases for their Sikorsky helicopter programs. The maintenance and support of rotary systems has traditionally provided Lockheed with a high-margin revenue stream which was disrupted slightly in Q3 FY23 as a result of decreased demand.

FY23 YTD, Lockheed’s RMS segment once again operated on what is essentially a constant operating margin of around 11.5%.

{kind=link}

Lockheed’s Space segment saw great 8% growth in net sales as a result of increased demand for their Next Generation Interceptor ((NGI)) and Fleet Ballistic Missile ((FBM)) development programs.

The 15% decrease in operating profit was almost entirely due to lower equity earnings from United Launch Alliance due to lower launch volumes. This left the firm’s Q3 OM at just 8.4% and resulted in the firm’s first nine months OM decreasing from 10.0% in FY22 to just 9.2% in FY23.

{kind=link}

Finally, Lockheed saw their MFC revenues grow just over 4% YoY thanks to solid demand for their GMLRS and HIMARS missile programs particularly thanks to their usage in Ukraine.

MFC’s operating profits also increased 4% in Q3 which allowed Lockheed to maintain a constant OM of 13.5% YoY. The increase in operating profits came as a result of COGS control and higher operating profits from Apache sensor and global sustainment programs.

Cumulatively FY23 has seen Lockheed grow their overall net earnings a substantial 31.6% YoY thanks to solid Q1, Q2 and Q3 results being further buoyed by decreased non-service FAS pension expense and a mostly stable OM.

{kind=link}

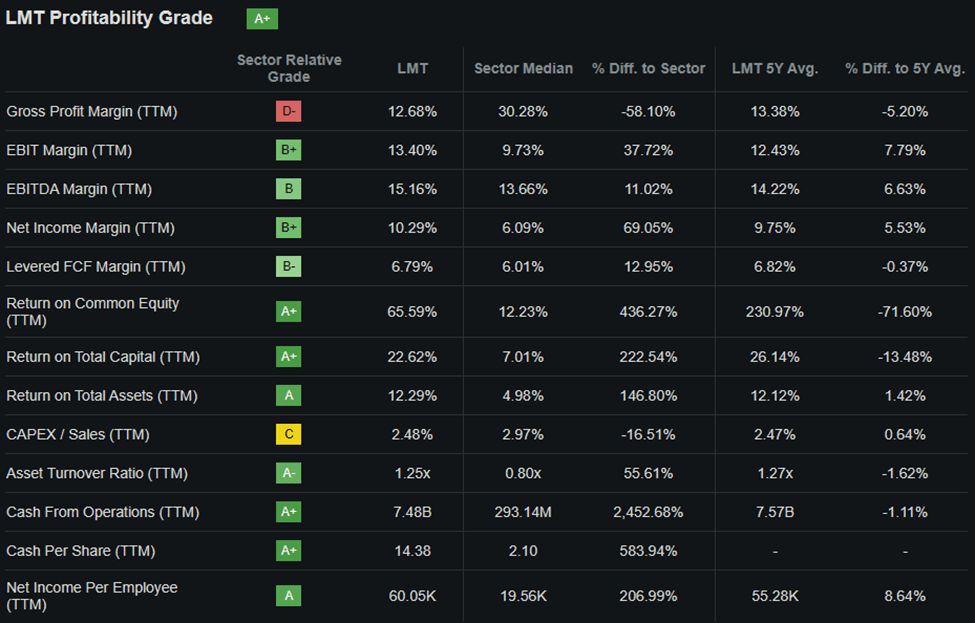

Seeking Alpha’s quant continues to provide Lockheed Martin an “ A+ ” profitability grade which I fundamentally believe is an accurate representation of Lockheed’s continued fiscal prowess.

From a balance sheet perspective, Lockheed continues to be a well-managed company with great capital allocation strategies and fair investor distributions illustrating a conservative yet competitive approach to business form management.

The firm has total current assets of $23.3B while total current liabilities amount to just $17.2B. This leaves Lockheed with an excellent quick ratio of 1.14x and a current ratio of 1.36x. Such great short-term liquidity is further emphasized by the lack thereof at Lockheed’s competitors with Honeywell and Northrop currently operating with quick ratios of 0.92x and 0.98x respectively.

Lockheed’s total assets amount to $56.7B while total liabilities are only $47.4B. The firm also has just $9.3B in total shareholders' equity leaving the firm with a pretty elevated debt/equity ratio of 1.88x.

While this does suggest Lockheed is currently operating with a financial leverage of about 6%, I personally believe this merely illustrates just how well Lockheed is utilizing debt to fund their R&D projects and grow the business even further.

{kind=link}

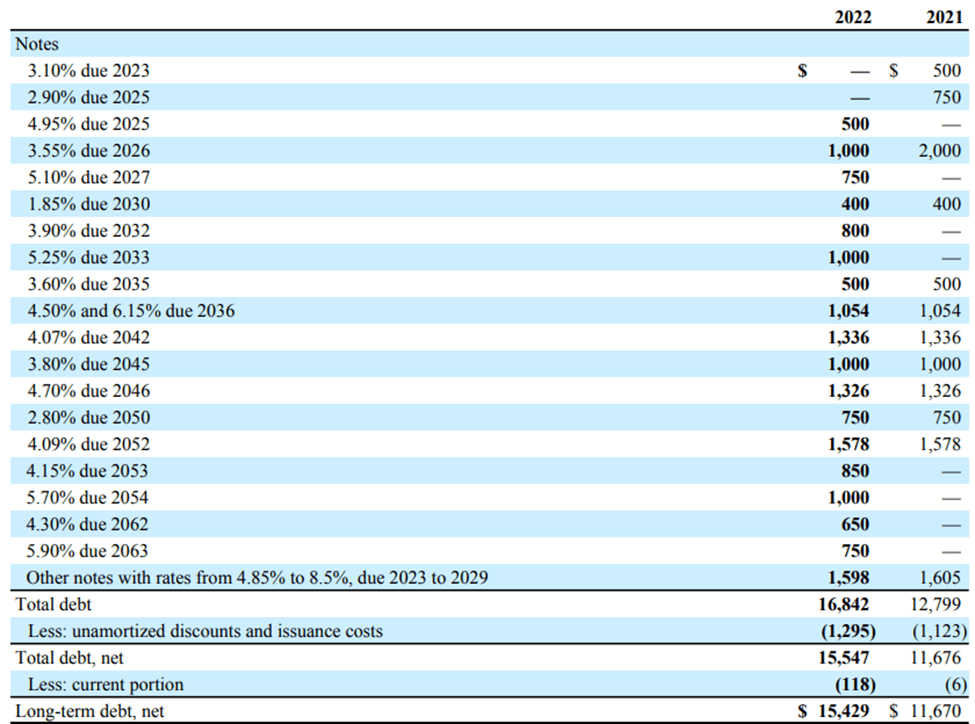

This is further supported by Lockheed’s excellent total debt maturity profile (table as of FY22 ) with a majority of notes being at fixed interest rates with over 80% being due post 2030.

While the latest Q3 FY23 10-Q indicates that Lockheed now has $18.7B in total long-term debt, I see no reason to believe that Lockheed would have taken aboard this debt in any less a conservative manner than they have done in the past 20 years.

Moody’s upgraded Lockheed’s senior unsecured domestic notes to an “A2” rating in August, 2023 while simultaneously upgrading the firm’s commercial paper ratings to a “P-1”. Moody’s classifies “A2” ratings as being of “upper medium” investment grade while short-term debt ratings of “P-1” are considered to be of the highest quality.

{kind=link}

Lockheed’s dividend payments are also rated by Seeking Alpha’s Quant as “A+” which I believe is accurate considering a payout ratio of 43.29% combined with a 5Y growth rate of 8.18%. Lockheed’s annual payout ('FWD') is $12.60 while the firm has a superb 21-year dividend growth streak.

Overall, Lockheed continues to be a profitability powerhouse generating massive returns on their business while simultaneously growing their operations further. The firm has also continued their conservative yet opportunistic approach to capital allocation all the while remembering to reward shareholders handsomely.

Valuation

{kind=link}

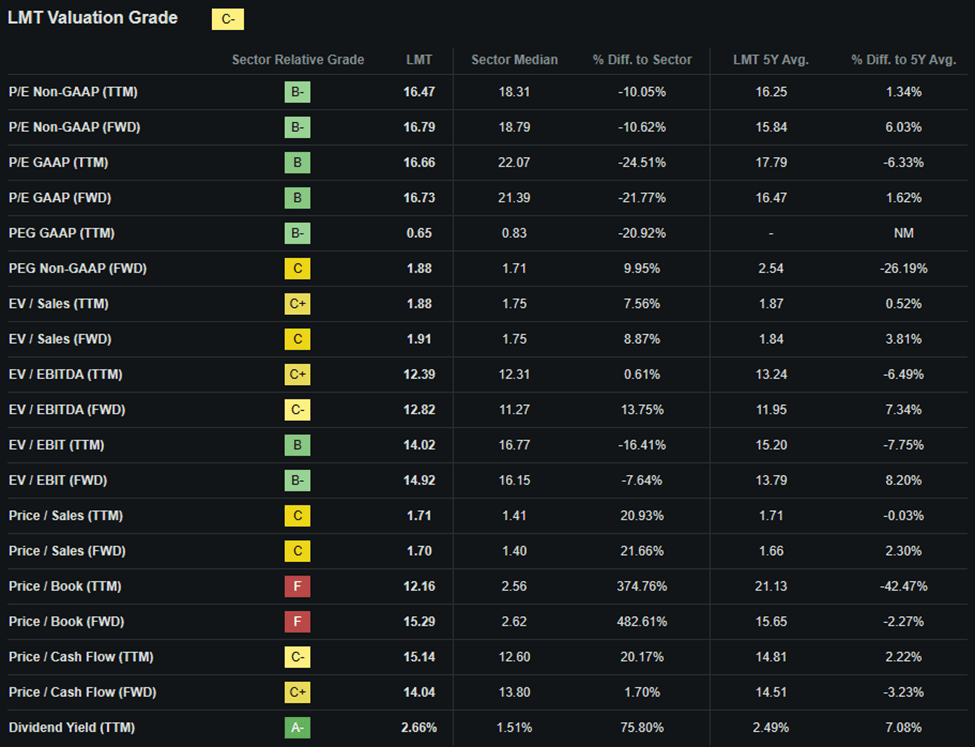

Seeking Alpha’s Quant assigns Lockheed Martin with a “ C- ” Valuation grade which I believe to be a slightly pessimistic representation of the value present within the firm’s stock.

The firm currently trades at a P/E GAAP TTM ratio of 16.66x which represents an 6.33% decrease in the firm’s GAAP P/E ratio compared to their running 5Y average.

Lockheed’s P/CF TTM of just 15.14x is reasonable while their TTM EV/EBITDA of just 12.39x is 6.39% lower than their running 5Y average.

The firm’s Price/Sales TTM of 1.71x is quite high however and represents no real change to Lockheed’s 5Y average. Lockheed also exceeds the sector median in this metric by over 20%.

Considering these basic valuation metrics alone I believe it would be quite difficult to ascertain any reliable picture regarding the possibility for intrinsic value to be present in Lockheed’s shares.

{kind=link}

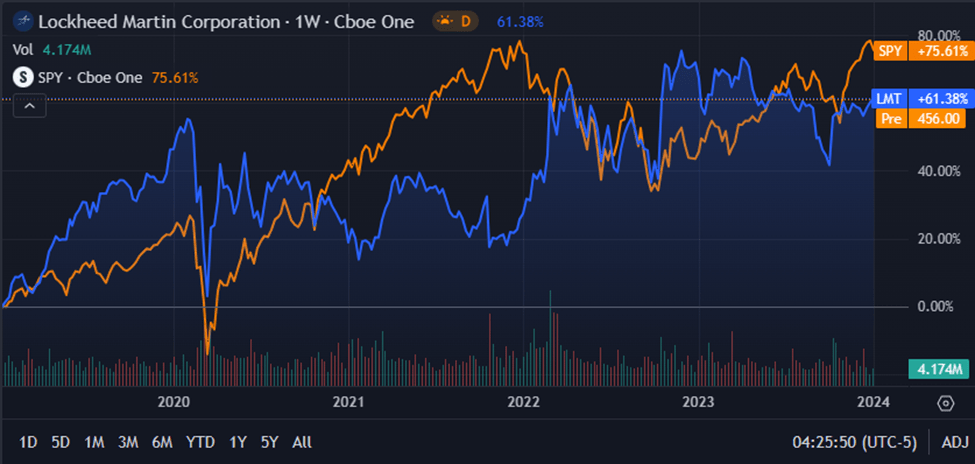

From an absolute perspective, Lockheed shares are trading relatively close to the all-time highs of around $495 witnessed in April, 2023. However, the stock has performed reasonably poorly in 2023 generating basically flat results throughout the year.

Lockheed shares have performed quite well compared to the S&P500 tracking SPY ( SPY ) index which only just outperformed the defense contractor on a 5Y timeframe thanks to the huge December rally seen at the end of 2023.

Considering the relative valuation metrics and absolute comparison, Lockheed Martin does not immediately appear to stand-out as a massive deep-value opportunity. However, an intrinsic value calculation must be completed to obtain a more reliable quantitative valuation picture for the firm’s stock.

The Value Corner

By utilizing The Value Corner’s specially formulated Intrinsic Valuation Calculation, we can better understand what value exists in the company from a more objective perspective.

Using Lockheed’s current share price of $456.50, an estimated 2023 EPS of $27.19, a realistic “r” value of 0.06 (6%) and the current Moody’s Seasoned AAA Corporate Bond Yield ratio of 4.74x , I derive a base-case IV of $517.40.

This represents a 12% undervaluation in shares relative to current prices.

When using a more pessimistic CAGR value for r of 0.045 (4.5%) to reflect a scenario where a globally spanning recession results in decreased defense budget spending by both the U.S. and key allied partners, shares are still valued at around $441.70 currently representing a fair valuation.

Considering the valuation metrics, absolute valuation and intrinsic value calculation, I believe that Lockheed Martin is trading in what can be considered a reasonable price range with a modest 12% undervaluation in shares in a base-case scenario.

In the short term (3-12 months), I find it difficult to say exactly what may happen to the firm’s valuation. While the increasing amount of geopolitical conflicts may further drive defense spending and as a result, demand for Lockheed equipment, a sudden shock to the U.S. economy could see stock prices tumble as investors react to negative catalysts.

Overall, I believe that in the short-term the stock market tends to act as a voting machine rather than a weighing scale. Therefore, I believe it unwise to make any short-term predictions on what may occur to Lockheed’s share prices.

In the long-term (2-10 years), I believe Lockheed Martin will continue to be the absolute dominating force when it comes to the defense industry and sector as a whole.

The firm has a wide and robust economic moat that would be difficult for competitors to replicate while Lockheed’s recent execution successes in multiple defense programs has resulted in a great tailwind for the firm’s future growth.

When combined with the current trend of increased spending on defense equipment, I believe Lockheed is well positioned to benefit from both their own business successes and an overall increase in appetite for defense equipment.

Risks Facing Lockheed – Q3 FY23 Update

Little change has occurred to the threats facing Lockheed Martin. For an in-depth analysis, please read my previous article here .

To summarize Lockheed’s risk profile, the firm still faces tangible risks from their reliance on U.S. government spending and from the possibility of future failures in execution of new projects resulting in margin contraction and stunted growth.

Since around 71% of Lockheed’s revenues arise from U.S. government defense expenditure, the firm is exposed to a cyclical political environment jeopardizing defense spending. Any decreases in the U.S.’ overall defense budget would result in losses at Lockheed Martin which could hinder both short-term profitability and their long-term position.

Lockheed must also continue to develop new defense projects in order to stay ahead of rivals Northrop Grumman and Raytheon. This requires significant R&D expenditure which ultimately will only be reimbursed if the U.S. defense department selects Lockheed’s offerings for mass production.

The F-35 program is a great illustration of Lockheed’s recent successes beating Boeing’s (BA) X-32 JSF demonstrator. The F-22 is another great example of Lockheed (in collaboration with Boeing, and General Dynamics) beating Northrop Grumman’s YF-23 offering.

Such costly programs have recently generated great long-term returns for Lockheed thanks to their offerings winning the supply deals with the U.S. government. However, they also highlight the stakes involved should Lockheed fail to secure final supply contracts in any of their new product development programs.

From an ESG perspective, Lockheed still faces social pressures from being deemed a war-profiteering company with some Millennial and Gen-Z investors appearing to be particularly against the inclusion of any defense contractors in their portfolios.

Summary

Lockheed Martin continues to generate substantial profits from their business operations despite FY23 falling a little short of expectation so far. Reasonably muted revenue growth has been accompanied by essentially flatlined margins and returns.

This appears to have left investors in a slightly clouded state as illustrated by the sideways movement in Lockheed shares.

Nevertheless, Lockheed looks well primed to benefit from increasing geopolitical tensions with their current generation of key defense programs continuing to prove competitive in the overall defense marketplace.

Shares appear to be somewhere between a modest 12% undervaluation and a fair valuation. While the stock has often traded at a slight premium to its intrinsic value, it is difficult to advocate building a substantial position in the defense contractor given the potential for a lack of margin of safety in shares.

Overall, I still believe Lockheed is well positioned to benefit from the current trend of increasing government spending on defense equipment and given the potential for a modest undervaluation in shares, I rate the firm’s stock a Buy.

In order to secure a Strong Buy rating, I would like to see a greater margin of safety with an undervaluation to the tune of around 25% being my minimum. This could occur either by a decline in the firm’s valuation or through an increase in overall operating profits and margins.

For further details see:

Lockheed Martin: A Solid Bet On The Future Of Defense And Aerospace (Rating Upgrade)