RTX - Lockheed Martin: Don't Let Temporary Problems Confuse You It's A Buy

2023-03-06 22:57:14 ET

Summary

- Lockheed Martin is trading at what seems to be a historically high valuation - its current TTM P/E ratio is 22.0, which is 7.0% above its 5-year average of 20.6.

- The company is experiencing supply chain disruptions and pauses in flight operations, which are hurting its growth and profitability. However, those are short-term temporary problems.

- In 2024, Lockheed Martin is projected to return to mid-single-digit growth, and the management is confident it will reach its target to deliver 156 F-35 fighter jets in 2025.

- The global defense budget is expected to increase significantly due to geopolitical tension, as investors await the FY24 budget release from the Department of Defense on March 9th.

- After 20 consecutive years of dividend growth, shareholders are paid to wait for growth to return. I rate the stock a Strong Buy, with a fair-value of $551 per share.

Lockheed Martin ( LMT ) is trading at what seems to be a historically high valuation, as its current trailing twelve months P/E ratio is 22.06, compared to its 5-year average of 20.6. The company's earnings are down due to temporary supply chain disruptions and pauses in flight operations which caused delays in F-35 deliveries, as well as with other products. The market is looking at LMT's long-term prospects and is willing to pay a premium in the near term. The global defense budget is expected to increase significantly, and Lockheed Martin is working on improving its production capacity in order to meet the demand.

I estimate LMT stock's fair value at $551 per share and give it a Strong Buy rating. While it may take time to reach this price target, the company is paying shareholders handsomely to wait via dividends and buybacks.

Company Overview

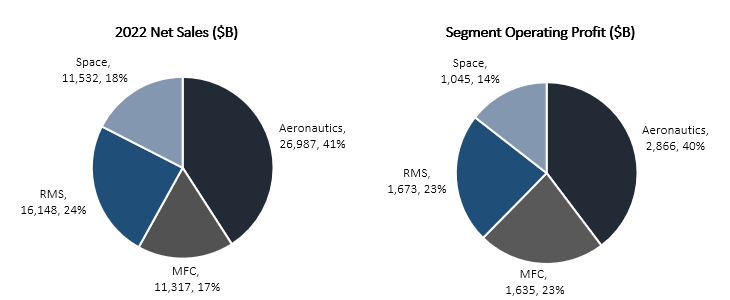

Lockheed Martin, a security and aerospace company, engages in the research, design, development, manufacture, integration, and sustainment of technology systems, products, and services worldwide. It operates through four segments: Aeronautics, Missiles and Fire Control, Rotary and Mission Systems, and Space. The company's main customer is the U.S. Government, which accounted for 73.5% of its net sales in 2022.

Under the Aeronautics segment, the major programs include the F-35 Joint Strike Fighter, the C-130 Hercules, the F-16 Fighting Falcon, and the F-22 Raptor. The F-35 program is the company's largest program, generating 27.0% of its total sales. Under the Missiles and Fire Control ((MFC)) segment, the main programs are PAC-3, THAAD, MLRS, JASSM, Apache, and Javelin. The Rotary and Mission System (RMS) segment's major programs are the Sikorsky helicopters, IWSS, C6ISR, and TLS. Under its Space segment, the major programs are SBIRS, FBM, Orion, NGI, and GPS III.

The segment breakdown for 2022 is as follows:

Created by author using data from LMT's 10-K

{kind=link}

For 2022, the company's sales and segment operating profit decreased by 1.5% and 2.2%, respectively. All four segments saw a small revenue decrease, while the RMS and Space segments accounted for the majority of the segment operating profit decrease.

Headwinds

Like most of its large defense contractor peers, Lockheed Martin experienced major operational disruptions since Covid-19.

During 2022, the COVID-19 pandemic, supply chain challenges, and increased demand caused global semiconductor chip shortages, extended lead times and pricing escalations and these are expected to continue in 2023. These supplier disruptions have resulted in delays and increased costs and have adversely affected our program performance and operating results.

--- Page 6 of LMT's 10-K

Unlike other industries, production chains in the defense industry take a long time to ramp up. Thus, management expects these issues to continue into 2023.

Another major issue was in the F-35 production chain -

At the end of 2022, there was an issue with the Government Furnished Equipment (GFE) engine that resulted in a pause in flight operations and 2022 aircraft deliveries were impacted. The delivery pause continues as flight operations remain on hold and concurrently, GFE engine deliveries have been suspended. We will have greater clarity if changes to our 2023 aircraft delivery expectation are required once the pause in flight operations and the GFE engine delivery suspension have been resolved.

--- Page 33 of LMT's 10-K

We can learn that the company experienced external headwinds that it wasn't able to prevent. Those issues resulted in poorer financial results, and are expected to continue to hurt the company in 2023.

Tailwinds

Although the company is experiencing some headwinds, I find those to be a short-term temporary problem. As a very important company for the United States national security, as well as for its allies, investors can rest assured Lockheed Martin is not going anywhere. In addition, the company's leverage is very low, with a net debt-to-EBITDA ratio of approximately 1.3. So, as we established we can safely rely on the company to weather the storm, let's go over its major tailwinds.

I will not go into detail regarding the geopolitical atmosphere in the world which has changed dramatically due to Russia's invasion of Ukraine. In short, NATO allies have set a target for their defense budget to be at 2 percent of GDP. As of today, many members of NATO are not meeting that target, and some members argue it should even be increased . Specifically relevant for Lockheed Martin, NATO targeted that spending on equipment will amount to 20.0% of the total defense budget. Up until the invasion, that target went somewhat overlooked. Today, this has become a major focus area for NATO members. In conclusion, members of NATO are expected to spend 0.4% of their GDP on military equipment, which is what Lockheed Martin sells.

The conjoined NATO army has already declared it's going to increase its military budget by 25.8%, to €1.96B. Although it's a small amount, it represents the higher level of ambition to enhance the military capabilities of NATO and its members. More importantly, Lockheed's largest customer, the United States Department of Defense, has already increased its 2023 budget by 9.5% to $797.7B.

Another major tailwind is the finalization of the F-35 Low Rate Initial Production Lots 15-17 production contract with the U.S Government for up to 398 aircrafts. This will allow LMT to increase production capacity and reach its goal of 156 F-35 deliveries per year, starting in 2025. Many U.S. allies, including Germany, Canada, and Finland, are expecting to receive a number of F-35 aircrafts in the upcoming years.

Overall, Lockheed Martin is very well set on the demand side for the near future, as we can learn from its 1.2 book-to-bill ratio in 2022, and its constantly increasing backlog:

Created by author using data from LMT's financial reports

The company expects to fulfill 98% of its current backlog in the next 24 months. This means that all the increased demand discussed above is yet to materialize into the company's backlog, because, as can be expected, defense contracts take time to finalize.

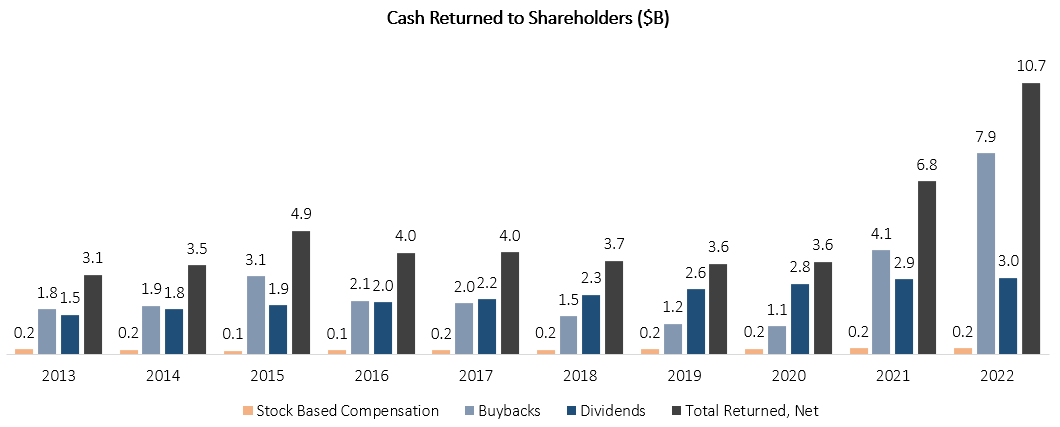

Dividends & Buybacks

Lockheed Martin is a natural constituent in dividend growth portfolios. The company has raised its dividend for 20 consecutive years and has decreased the number of its shares significantly via buybacks.

Created by author using data from LMT''s financial reports

{kind=link}

Between 2013-2022, the company increased its dividend at a 7.7% CAGR, and it returned a cumulative $47.8B to shareholders. At the beginning of 2013, Lockheed Martin's market cap amounted to approximately $30B. In essence, if you bought the stock around January 1st, 2013, you would have gotten 150% of your investment returned to you via cash from the company. There aren't many companies that could say the same.

Competitors & Multiples Analysis

In the defense industry, many "competitors" are actually partners, as they operate through joint ventures and cooperative partnerships. For example, the Javelin missile program is a joint venture between Lockheed Martin and Raytheon Technologies ( RTX ).

Most of LMT's competitors share the same tailwinds and headwinds described above. While each company has its own flagship program, not many companies own a program like LMT's F-35.

Created and calculated by author using data from Seeking Alpha; Data as of March 6th, 2023

Looking at the numbers, LMT is trading slightly below the industry's average FY1 P/E multiple, and slightly above the industry's average at FY3. This reflects a gap between the current consensus expectations and market expectations, as the consensus seems to underestimate LMT's return to growth, while the market seems more positive.

Nevertheless, qualitatively, I find LMT's small premium justified. As I mentioned, LMT's future seems quite bright with the increase in production capacity for the F-35. The company is expected to deliver above-industry growth beginning in 2024 and is expected to improve its margins after the recovery in its supply chain and the completion of its digitalization initiative.

If management is able to deliver on these expectations, Lockheed's actual multiples are lower than it seems.

Valuation & Near-Term Projections

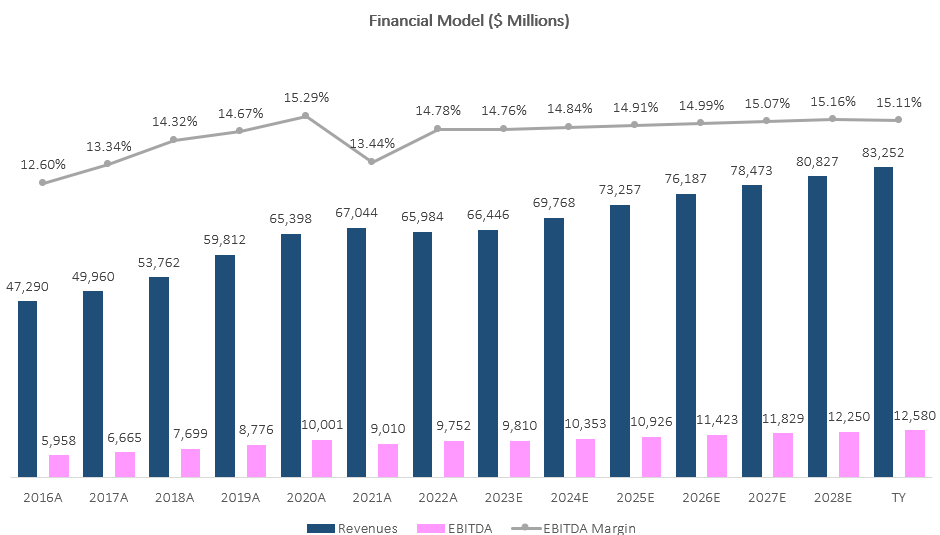

I used a discounted cash flow methodology to evaluate LMT's fair value. I assume LMT will see revenues grow at a CAGR of 3.4% between 2022-2028, which is according to the management's return to growth forecast. I believe revenues will grow at this pace due to backlog fulfillment, the enhanced F-35 production capacity, and the company's ability to meet the increased demand from the larger defense budgets worldwide.

I project EBITDA margins to increase incrementally to 15.1%, as the supply chain recovers and major programs finish their ramp-up stage. This is not outside of the company's reach, as we already saw higher margins in the past.

Overall, my assumptions result in EBITDA growth slightly higher than revenues, reflecting operational leverage and cost-efficiencies.

Created by author based on LMT's financial reports and author's projections

{kind=link}

Taking a WACC of 8.75%, I estimate LMT's fair value at $140.8B or $551 per share, which represents a 15.0% upside compared to its market value at the time of writing this article. While this does represent an arguably high P/E multiple on 2023 earnings (20.6), I believe LMT will see significant growth in 2024, which is why its near-term multiples will look a bit inflated. Plus, this is actually the company's average P/E multiple in the past 5 years.

An important metric to keep in mind when evaluating Lockheed Martin is its share buybacks. As we saw above, when it comes to LMT, buybacks are a significant contributor to total returns. In order to assess if my DCF model is valid and make sure buybacks are reflected, I assigned an exit multiple of 16 ( slightly below the company's 5-year median) to my projected 2026 EPS, which amounts to $34.9. Taking into account a decrease of 2.5% in share count per year, which is according to the company's historical average, I get to a fair value of $558, slightly above my DCF model.

Before you say that my EPS assumption is too optimistic compared to the consensus, let me just say the current long-term consensus does not really make sense. As it stands, analysts expect LMT to grow its revenues by 4.0% annually between 2023-2026, yet they expect EPS to grow by only 1.8%.

In the last ten years, only twice the company grew revenues ahead of EPS, and it was a result of either temporary or non-recurring issues. I don't see any circumstance in the foreseeable future resulting in the company growing revenues ahead of EPS.

Near-term Projections & Catalysts

I find it important to provide additional details regarding my near-term financial projections in order to provide both the readers and me with the ability to measure the accuracy of the investment thesis. This allows me to easily assess whether an earnings report is good or bad, and what adjustments I have to make in my model.

When it comes to LMT, my near-term annual projections are very similar to the detailed guidance the company provided. For Q1-23, I expect revenues of $15.2B, and net income of $1.6B, which is slightly above the consensus of $15.0B and $1.5B, respectively. After the April earnings release, we will see who came closer and I will update my model accordingly.

Regarding catalysts, I'm writing this article 3 days before the United States DoD is supposed to release its FY24 budget. There have been conflicting messages regarding the budget, as Republicans have taken over the House of Representatives and intend to use the national debt ceiling debate to pressure spending cuts from President Joe Biden, and there have been voices calling for a cut in defense spending, or at least a halt in increases. However, this comes after China increased its defense budget by 7.2%, and many members, including Republicans, are calling for non-defense spending cuts.

As I am no political expert, I'll just say I believe even a small decrease in the budget will not hurt the company's growth prospects, as its backlog and demand are already set for the upcoming years. It will however put some pressure on the stock in the near term.

Risks

Some market participants expect the global recession scare and the rising inflation to weigh on governments' legitimacy to increase their defense spend. While this is a valid theory, it has no basis in facts. At the day of writing, all of Lockheed's relevant customers have expressed their plans to increase their defense budgets, and as described above, some have already done so. In addition, LMT's backlog, which is yet to reflect the projected budget increases, has reached an all-time high at the end of 2022.

Another cause for concern is LMT's operational disruptions. The flight pauses and supply chain issues have already affected the company's results, and are yet to recover. If the company's delivery targets for 2025 are not met, the stock will probably suffer. While nobody can predict the future, I put my trust in the management's ability to deliver on their targets, which they are repeatedly affirming at every chance they get.

The last risk I would address is innovation. What really differentiates a long-term compounder like LMT from an ordinary manufacturer is continued innovation and the company's extraordinary products like the F-35. While it is harder to innovate within a huge company like Lockheed Martin, the company's investment arm is constantly looking to acquire the newest technologies. Organically, Lockheed is currently going through a company-wide business transformation to enhance its infrastructure, collaboration, and efficiencies. While this does sound like something every large company talks about, it is extremely important for a company like LMT to be able to deliver products faster and reduce redundancy. Thus, I believe the company, backed by its great financial capabilities, will not miss on future opportunities to innovate.

Conclusion

Lockheed Martin should be a cornerstone in every long-term dividend investor's portfolio. The company operates in a recession-proof industry, with the richest governments in the world as its customers. Within the industry, LMT proved its ability to outperform its peers through extraordinary products like the F-35, and incomparable shareholder returns through dividends and buybacks. While the company's price seems inflated on paper, this is a result of temporary headwinds. The future looks bright with the company's production capacity expected to increase significantly en route to meet the management's 2025 targets. As demand is growing materially due to the geopolitical tension in the world, I estimate LMT's fair value at $551 per share. While it may take time to reach this price target, I believe the company is paying handsomely for shareholders to wait. Thus, I rate LMT as a Strong Buy.

For further details see:

Lockheed Martin: Don't Let Temporary Problems Confuse You, It's A Buy