LMT - Lockheed Martin: Growth And Income At A Fine Price

2023-04-02 10:18:44 ET

Summary

- Lockheed Martin has rallied over the past two years, though not as much as you might expect given global geopolitical developments.

- Shares are still attractive at today's multiple, especially considering the firm's strong track record and its exposure to the space industry.

- I believe the debt ceiling showdown is scaring traders today, but shares should rally once that problem has been resolved.

Lockheed Martin ( LMT ) is one of the world's largest defense contractors. I've owned shares since 2021. That year was an inflection point for the industry, as sentiment around defense spending hit its trough when the United States pulled its forces out of Afghanistan. Since then, various countries' defense departments have moved to more muscular postures thanks to the invasion of Ukraine among other rises in international tensions and hostility.

Lockheed Martin shares initially jumped sharply as the global geopolitical situation became more challenging. In recent months, however, LMT stock's rally has petered out despite a seemingly strong set of fundamentals and forward outlook:

In short, why hasn't Lockheed Martin powered through the $500 barrier yet, and what is the firm's outlook for 2023 and beyond?

The Bull Case: Reasonable Valuation For A Recession-Resistant Industry

A central attraction to the defense industry is that it is funded primarily by national governments. As such, revenues are guaranteed and backed by taxpayers rather than commercial entities. This is a big perk in recessionary times, such as we may soon be entering, as the government won't cut back spending at the drop of a hat as the private sector would do.

In addition, defense contracts are exceptionally long-term. Lockheed's all-important F-35 program, for example, is expected to run into the 2060s. That's a long-duration revenue stream right there.

The defense industry also has high barriers to entry. The government is unlikely to award important or strategic contracts to start-ups with little evidence they can deliver the goods on time. Entrenched players like Lockheed have the benefits of scale and inertia in maintaining existing programs and winning new contracts.

Given all these attractive traits, you might expect defense stocks to trade at a significant multiple to the S&P 500. Instead, thanks to whatever reason, defense stocks tend to trade at the market multiple or sometimes even a discount. Several of the defense contractors were trading at 12-14x forward earnings in 2021, for example, which was rather surprising given how frothy valuations were in the rest of the market at that time.

Fast forward to today and while LMT stock has jumped significantly, it still stands out as a solid value at the current price. Analysts see the company at around 17.7x forward earnings:

Lockheed earnings outlook (Seeking Alpha)

I believe these estimates are slightly too low, given the wave of increased defense spending budgets we've seen from various countries around the globe, along with the new contracts Lockheed Martin itself has won in recent months. The heavy use of armaments and defense tools in Ukraine, for example, should lead to accelerated reorders and rebuilding of inventory.

In any case, even based off this fairly conservative set of analyst estimates, Lockheed Martin is around 17x earnings -- which represents a 6% earnings yield -- and is set to deliver that regardless of the major economic concerns we are seeing in other parts of the economy. That's enough to serve as a safe harbor.

And, again, I'd note that I think those analyst estimates are too low. Lockheed Martin has rather consistently grown earnings for the past 25 years, regardless of the particular geopolitical conflicts or defense posture that we've seen in the interim:

Again, this is normally the sort of track record what people are willing to pay premium earnings multiple for in comparison to the S&P 500. So, what might be hindering the stock at the moment?

Debt Ceiling Drama Looms

A big risk to the bull case for Lockheed Martin is the upcoming fight over raising the debt ceiling . Investors may be bored of hearing talk about the debt ceiling. After all, it seems markets gyrate on a potential government default scare every few years but there is always a resolution before the deadline.

That's all well and true, as far as the overall market and budget go. However, sometimes, these fights over raising the debt ceiling end up having tangible consequences. In the 2011 fight, for example, the end result, the Budget Control Act, ended up cutting defense spending. As the Wall Street Journal noted, as a result of this law :

"[T]he military was forced to bridge the gap between the GOP's fiscal ambition and its limited congressional power. The Budget Control Act initially cut $487 billion from defense. The law required 50% of additional reductions to come from defense, which accounted for only 20% of federal spending. Over the next decade, the U.S. spent less on defense than originally planned-and less efficiently."

Since things such as entitlement spending are guaranteed and thus very hard to change, defense often ends up being the easiest target for spending cuts at a budgetary impasse. See the 2011 compromise, for example. While a $487 billion budget cut over a decade may not seem like big news in comparison to the overall scope of the Defense Department, it was still a meaningful drag on the outlook for firms like Lockheed Martin.

I doubt that the politicians would actually push through a significant cut to defense spending at a time when there is an active war in Ukraine and rising tensions elsewhere around the globe. But debt ceiling fights have a way of being unpredictable, and until we get a resolution, I believe this will be an overhang for Lockheed Martin and other defense companies' valuations.

LMT Stock Bottom Line

While budgetary worries could keep Lockheed Martin grounded for much of 2023, the longer-term outlook is promising.

Another factor that should help shares blast off is the company's space and satellites program. Lockheed's space operations have already grown to be an $11.5 billion business annually. And that's even as the commercial side of the space industry is in its early days.

Over the next five to ten years, I believe we'll see far more uses for satellite applications such as communications and Earth observation. In addition, there are more speculative possibilities such as space tourism, mining/manufacturing, and potential efforts to colonize other bodies such as Mars.

While I wouldn't put especially high odds on any one of those more speculative ventures paying off big within the next decade, as a whole, they offer a significant right tail upside option for Lockheed and other leading space services vendors. In addition, it's not hard to imagine a speculative mania around space stocks beginning at some point if we start to see traction toward something such as space tourism or zero-gravity manufacturing techniques.

Meanwhile, back here on Earth, Lockheed will be plenty busy ramping up operations to keep people safe amid a world whose geopolitical outlook has gotten a lot cloudier over the past few two years. It seems likely that Lockheed will see both more near-term orders to replenish military supplies given the ongoing Ukraine conflict and also more long-term strategic contracts as governments seek to bolster their deterrence capabilities.

All these factors come wrapped up in Lockheed Martin, which has a tremendous long-term track record while selling at an entirely fair earnings multiple today. I believe shares should sell at a significant multiple to the S&P 500 and yet the stock is on offer for less than 18 times earnings today, even as the firm's outlook has notably inflected upward over the past two years.

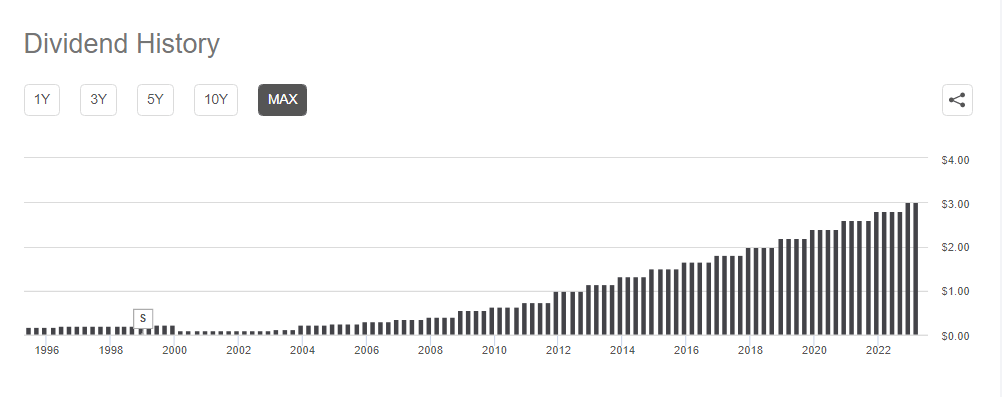

Finally, speaking of income, Lockheed Martin has been a solid dividend growth stock:

LMT dividend history (Seeking Alpha)

{kind=link}

It has grown its dividend 20 years in a row, increasing from 12 cents per quarter in 2003 to $3.00 per quarter today. That's a nice kicker on top of an already attractive business and starting valuation.

The threat of a debt ceiling related budgetary hurdle may linger for 2023, but shares should be set to lift off once that obstacle has been dealt with.

For further details see:

Lockheed Martin: Growth And Income At A Fine Price