LMT - Lockheed Martin: Here Is Why I Am Lowering My Price Target After Q3 Earnings

2023-10-23 16:39:58 ET

Summary

- Lockheed Martin Corporation's Q3 2023 revenues grew by 1.8% to $16.7 billion, driven by stronger sales in Space and Rotary and Mission Systems.

- The demand environment for defense equipment and services is strong, but Lockheed Martin sales may not increase immediately due to long evaluation and procurement processes.

- The company maintained its 2023 financial outlook and plans to repurchase $6 billion worth of shares for the full year.

Lockheed Martin Corporation ( LMT ) posted its third quarter results on the 17th of July before the opening bell. Year-to-date, shares have lost around 7% of their value. Indeed, there are some challenges ahead, but the current environment for defense equipment and services provides an appreciable backdrop.

Lockheed Martin Q3 2023 Results: Revenues Grew, Earnings Declined

{kind=link}

A major item to wrap your head around is the fact that the demand environment for defense equipment and services is strong, but that's not going to result in increased sales from one day to the other. The evaluation and procurement processes are long, with many milestones to be cleared before a sale is recovered, or even a purchase agreement is drafted. So, the positive demand environment we see today is not something that translates into sales anytime soon. 2024 is, in fact, the earliest point where defense contractors see this happening more prominently. On top of that, driven by some program-specific pressures and global supply chain issues, sales might not be directly reflective of demand, but of supply chain constraints on which a layer of program transitions can be added. So, while the outlook is strong, there are definitely some pressuring elements.

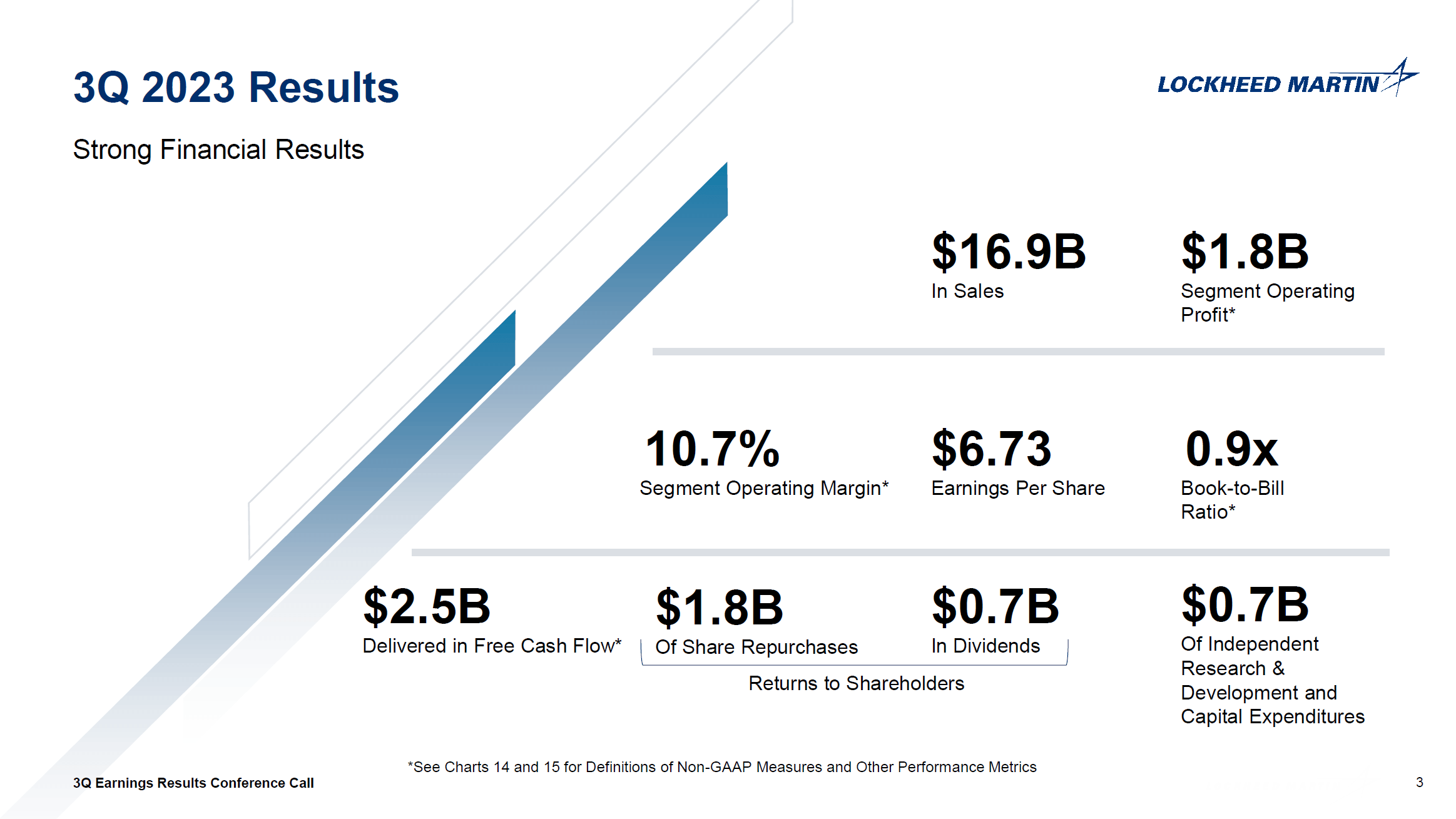

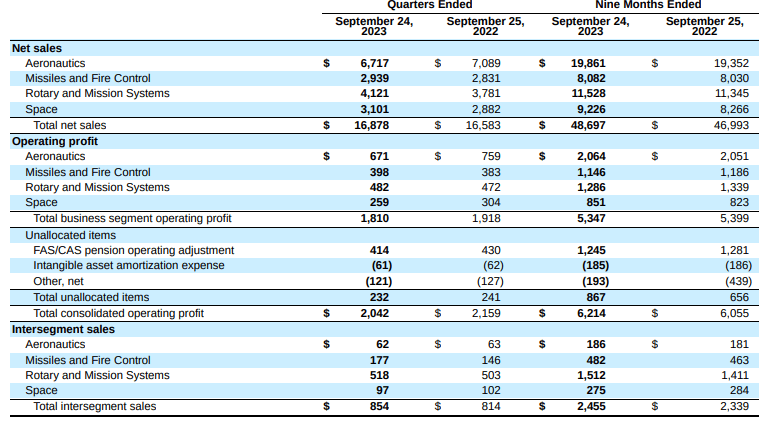

Total sales were up 1.8% to $16.7 billion, driven by stronger sales in Space and Rotary and Mission Systems offset by lower Aeronautics sales. The book-to-bill ratio was below one, but still stood strong at 0.9x. As mentioned, there's a timeline for contracts to be added to the backlog, so that materialization is not immediate or near term.

{kind=link}

The aeronautics department saw revenues decrease by 5.25% or $372 million driven by lower F-35 deliveries presenting a $525 million revenue pressure, partially offset by $125 million sales growth for classified programs. Profits declined 12% or $88 million driven by $115 million in lower F-35 profits partially offset by $50 million higher classified program profits while net profit rate booking adjustments were $80 million lower year-over-year. So, in some way you can look at the F-35 and classified programs to explain the profit decline, but one could as well consider the lower catch—up adjustments this year to explain it. Overall, margins within the segment dropped 70 bps to 10%.

The Missile and Fire Control segment experienced 4% or $108 million sales growth bringing the revenues to $2.94 billion driven by higher sales in the tactical strike for GMLRS and HIMARS offset by lower PAC-3 sales. Profits increased in the same range, pointing at stable margins of 13.5%. Interesting to note is that the increase in profits primarily came from increase profits on sensor and global sustainment programs, while integrated air and missile defense programs posted comparable profits.

Rotary and Mission Systems revenues increased by $340 million or 9% driven by higher integrated warfare systems and sensors sales and C6IRSR sales. RMS saw margins decline year-over-year due to higher volumes being partially offset by lower profit at Sikorsky and lower net profit booking rate adjustments.

Space saw revenues grow by $219 million or 8% increase in sales. This was driven by $135 million by the Next Generation Interceptor and Fleet Ballistic Missiles programs, and $45 million in national security space programs, while Orion sales set commercial civil space programs $40 million higher. Profit growth was absent, and the segment even posted a 15% decrease to its earnings due to lower equity earnings from United Launch Alliance and lower favorable profit adjustments.

Overall, results are not bad, but we see some variability in the performance between segments, and while revenues did grow, earnings declined somewhat, which admittedly also is caused by the timing of the Lot 15 award last year for the F-35.

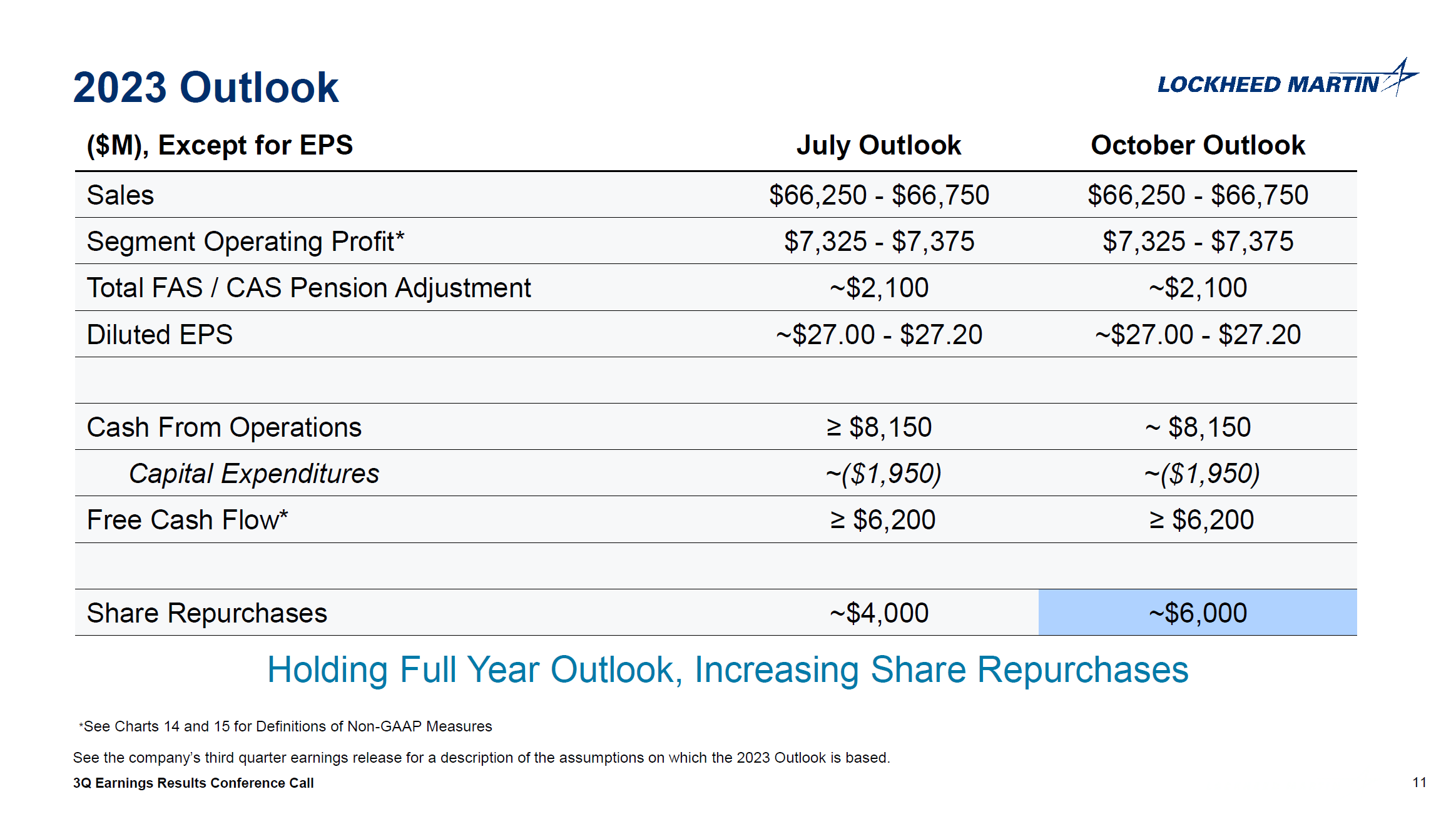

Lockheed Martin Maintains 2023 Financial Outlook

{kind=link}

During the second quarter earnings presentation, Lockheed Martin increased its revenue guide by $1.25 billion on the low end and $750 million on the high end while it increased its profit outlook by $20 million to $70 million, and the third quarter results did not provide any support to increase that guidance. What has been reflected is the increased share repurchase authorization, and the company now expects $6 billion in shares to be repurchased for the full year.

Is LMT Stock A Buy? Yes, But With A Lower Target

Lockheed Martin beat earnings consensus by $0.15 per share and revenue estimates by $160 million, but it was far from a spectacular earnings announcement. In fact, EBITDA estimates for 2023-2925 is down 2% while free cash flow expectations are now 1% lower. As a result, I am maintaining my buy rating supported by share repurchases but increasing debt with a revised stock price target for Lockheed Martin, which I discussed in a Stock Price Targets Alert for Lockheed Martin available to subscribers.

Conclusion: Still A Buy

As noted previously, the current results are actually not extremely important to Lockheed Martin in the sense that absent of surprises in either direction, 2023 is going to be a transition year. In that regard, even the outlook for 2023, which includes a previous increase to the guided ranges, is not the most interesting. The growth should have been in 2024 and beyond, driven by significant demand for defense equipment. However, the analyst expectations have become negative for 2024 and 2025. We can, of course, see that changing in the future, but it does seem that some F-35 risk is being integrated in the estimates.

I believe that while Lockheed Martin might be a hold in the books of some analysts and shareholders, that rating does not quite capture the growth prospects ahead yet. They are difficult to assess given the long-term nature of the industry and the complexity of the industry.

For further details see:

Lockheed Martin: Here Is Why I Am Lowering My Price Target After Q3 Earnings