LMT - Lockheed Martin Is Best Of Breed And Worth Considering

2023-05-01 13:13:28 ET

Summary

- Lockheed Martin offers investors a compelling combination of income growth and capital appreciation upside.

- Short-term hurdles are holding down deliveries of its F-35 jet fighters this year, though these headwinds should abate in the medium term.

- Management expects Lockheed Martin will return to growth in 2024.

- Lockheed Martin is a stellar generator of free cash flow in almost any operating environment and is run by an incredibly shareholder friendly management team.

- Its exposure to the space economy underpins Lockheed Martin's bright growth outlook.

Global geopolitical tensions are hot and getting hotter which in turn is driving up national defense budgets in North America, Asia, and Europe. Lockheed Martin Corporation ( LMT ) is well-positioned to capitalize on this dynamic as the defense contractor is the prime contractor on the massive F-35 jet fighter program, is a leading provider of offensive and defensive missile weapon systems, and has exposure to the rapidly growing space economy with offerings that meet the needs of defense, governmental, and commercial customers.

On March 9 , the Biden Administration requested Congress approve a $842 billion US Department of Defense budget for fiscal 2024. If approved, that would represent a $26 billion increase over fiscal 2023 levels and a $100+ billion increase versus fiscal 2022 levels. While final appropriation levels will likely differ, the trajectory of national defense spending in the US and across other Western-aligned nations is favorable for Lockheed Martin.

Earnings Update

Lockheed Martin reported first quarter 2023 earnings on April 18 that beat consensus top- and bottom-line estimates. On a GAAP basis, the company reported $15.1 billion in revenue (up 1% year-over-year) and $6.61 in diluted EPS (up 3% year-over-year). A 16% year-over-year increase in sales at its 'Space' business operating segment offset modest declines elsewhere.

Lockheed Martin's financial and operational performance is facing near-term headwinds as deliveries of its F-35 jet fighters are expected to be subdued due to limited supplies of jet engines from Pratt & Whitney, a division of Raytheon Technologies Corporation ( RTX ), and delays concerning a key software update. However, please note that these headwinds are temporary and should abate in the medium term. Pivoting to its earnings, a combination of cost containment efforts, meaningful pricing power, favorable movements at its unallocated line-items and strength at its Space operating segment enabled Lockheed Martin to grow its GAAP operating income by 5% year-over-year in the first quarter of this year.

As of March 26 (the end of Lockheed Martin's fiscal first quarter), the company's total backlog stood at $145.1 billion. While down from $150.0 billion at the end of calendar year 2022, Lockheed Martin's backlog remains enormous. Robust demand for its offerings should enable the firm to continue churning out mountains of cash flow going forward.

Cash Flow Powerhouse

Analyzing a company's historical free cash flow performance (defining free cash flow as net operating cash flow less capital expenditures) provides a useful benchmark for evaluating its future free cash flow generating potential. From 2020-2022 , Lockheed Martin's annual free cash flow averaged just over $6.7 billion versus $3.0 billion in run-rate dividend obligations in 2022. The company also repurchased $13.1 billion of its common stock in aggregate from 2020-2022, highlighting the incredibly shareholder friendly nature of Lockheed Martin's management team.

Lockheed Martin is a rock-solid free cash flow generator run by a shareholder friendly management team. (Lockheed Martin - 2022 Annual Report)

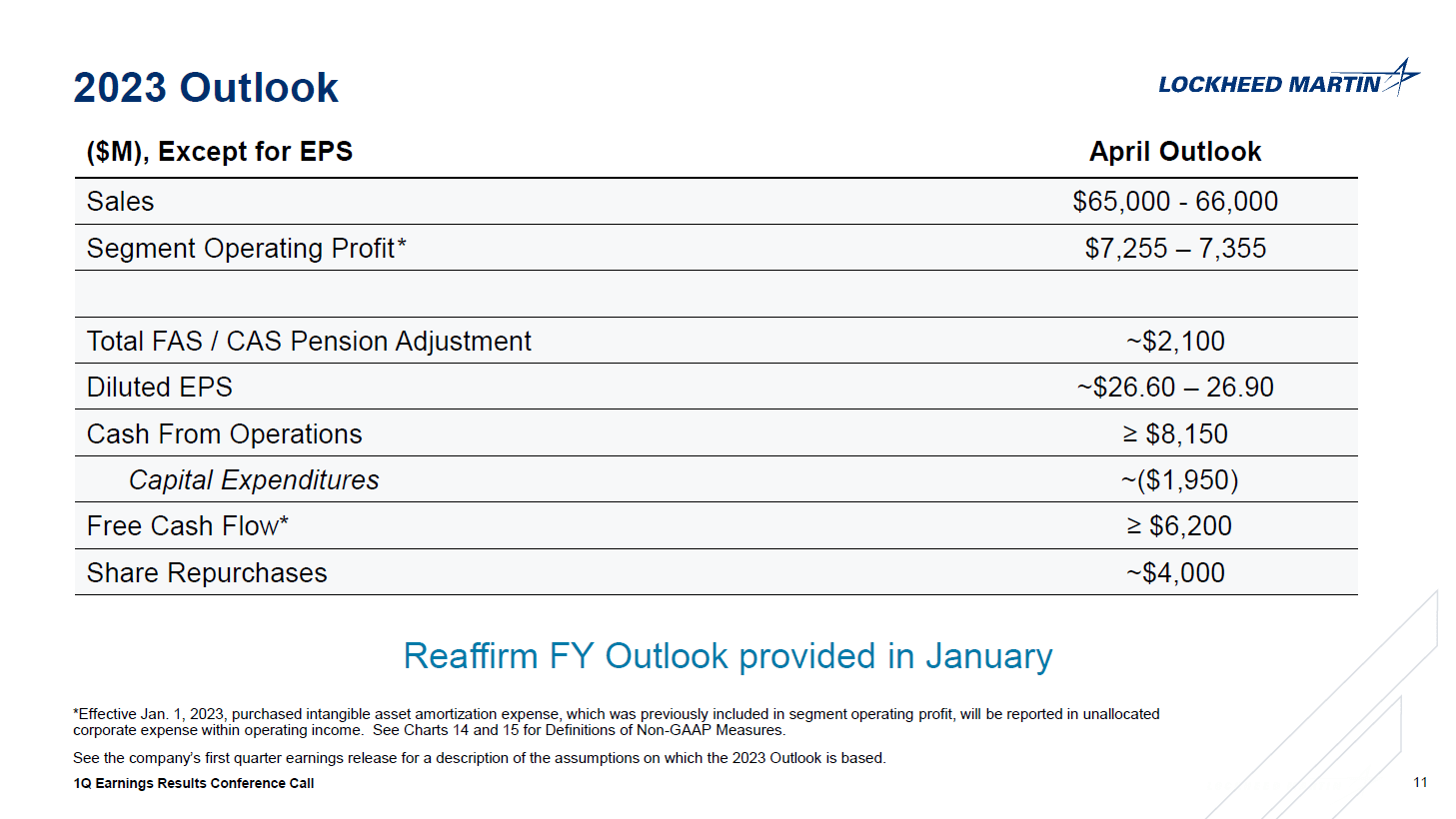

During Lockheed Martin's first quarter earnings update management reaffirmed guidance for 2023 that the firm put out in January. That guidance calls for ~$6.2 billion in free cash flow this year. Though 2023 is expected to be a difficult year for Lockheed Martin, its forecasted free cash flows should be more than enough to cover its expected dividend obligations (around $3.1 billion when annualizing its first quarter payouts, keeping in mind the firm boosted its per share dividend by 7% sequentially during the final quarter of 2022). Shares of LMT yield a nice ~2.6% as of this writing.

Lockheed Martin expects to spend around $4.0 billion buying back its stock this year. While the bulk of those repurchases are expected to be funded by its free cash flows, some of those buybacks will likely require the firm to lean on its balance sheet strength. At the end of its fiscal first quarter, Lockheed Martin had $2.4 billion in cash and cash equivalents on hand versus $0.1 billion in short-term debt and $15.5 billion in long-term debt on the books.

Given that interest rates have increased materially in recent quarters, paring down its net debt load would be a better use of its free cash flow compared to buying back its stock given that shares of LMT have boomed higher of late, in my view. With that in mind, as Lockheed Martin is a solid free cash flow generator in almost any operating environment, the company should be able to stay on top of its various financing obligations.

Management expects the firm's sales will decline by 1% this year versus 2022 levels at the midpoint of guidance while Lockheed Martin's adjusted non-GAAP EPS is expected to decline by 2% during this period. The company forecasts that it will return to growth in 2024 due in large part to deliveries of its F-35 jet fighters returning to normalized levels.

Lockheed Martin expects to generate substantial free cash flows this year, even in the face of sizable headwinds. (Lockheed Martin - First Quarter of 2023 IR Earnings Presentation)

{kind=link}

Favorable Growth Outlook

Recent contract wins highlight why Lockheed Martin should return to steady growth in the medium term. On April 28, Lockheed Martin secured a $7.8 billion deal covering the delivery of additional F-35 jet fighters to the US military and the militaries of US allies. Furthermore, on April 27 , Lockheed Martin put out a press release noting that:

The U.S. Army has awarded Lockheed Martin a Not-to-Exceed $4.79 billion contract to manufacture two full-rate production lots of GMLRS [Guided Multiple Launch Rocket System] rockets and associated equipment. The contract calls for the production of GMLRS Unitary and Alternative Warhead rockets and integrated logistics support for the U.S. Army and international partners… GMLRS is an all-weather rocket designed for fast deployment that delivers precision strike beyond the reach of most conventional weapons. The munition is the primary round for the Lockheed Martin produced HIMARS and MLRS family of launchers and features a Global Positioning System aided inertial guidance package and small maneuvering canards on the rocket nose, which add maneuverability to enhance the accuracy of the system.

Additionally, Lockheed Martin's vibrant space offerings represents another major growth driver for the firm.

Last year, the US National Aeronautics and Space Administration (NASA) selected Lockheed Martin to build the Mars Ascent Vehicle ((MAV)) as part of NASA's plan to send rock samples from Mars back to Earth for scientific purposes, which is expected to happen roughly a decade from now. The company played a key role in developing the Ingenuity helicopter which accompanied the Perseverance rover to Mars as part of NASA's Mars 2020 mission. Lockheed Martin also has exposure to the fast-growing commercial space economy via its offerings covering satellites (such as the LM 400 and its GPS III satellites), spacecraft (such as the innovative Orion spacecraft designed to support deep space human travel), and much more .

Discounted Free Cash Flow Model and Lockheed Martin's Equity Valuation

Lockheed Martin generated $7.7 billion in free cash flow in 2022, though this performance was aided by favorable special items that boosted its net operating cash flows while its capital expenditures were relatively low compared to historical levels and its guidance for 2023.

When assuming that Lockheed Martin generates ~$7.0-$7.5 billion in normalized free cash flow per year, these free cash flows grow by 5% annually into perpetuity (justified by the favorable environment for Western national defense budgets and Lockheed Martin's exposure to the fast-growing space economy), using a weighted-average cost of capital of 10%, taking its $13.2 billion net debt load into account (at the end of its fiscal first quarter), and factoring in its 255.7 million outstanding diluted share count at the end of its fiscal first quarter, the intrinsic value of its equity comes out to ~$496-$535 per share when using the discounted free cash flow analysis process.

Here is how I calculated that:

$7.0-$7.5 billion in normalized free cash flow divided by 0.05 (10% discount rate less 5% perpetual growth rate) = $140.0-$150.0 billion.

$140.0-$150.0 billion less Lockheed Martin's $13.2 billion net debt load = $126.8-$136.8 billion.

$126.8-$136.8 billion divided by 255.7 million outstanding diluted shares = ~$496-$535 per share.

This process is far from perfect and small changes in one's assumptions can result in large swings in the intrinsic value of a company's equity. With that in mind, the strength seen in shares of Lockheed Martin this year appears justified given its strong free cash flow generating abilities and exposure to secular growth tailwinds. Shares of LMT are changing hands at ~$468 as of this writing.

Downside Risks

Investing in Lockheed Martin comes with downside risks that readers should be aware of. For instance, its net debt load in a rising interest rate environment will create a drag on its future financial performance as higher net interest expenses eat into its cash flows and earnings. Additionally, Lockheed Martin is expecting its financial performance to face substantial headwinds this year before recovering next year. Should supplies of jet engines from Pratt & Whitney remain subdued or if anything else gets in the way of the pace of its F-35 deliveries over the coming quarters, Lockheed Martin's financial performance will likely remain subdued.

Most importantly, Lockheed Martin's performance is heavily influenced by the trajectory of the US defense budget and to a lesser extent the national defense budgets of key Western allies, factors that are outside of the company's control. In my view, these downside risks are manageable when considering that the global geopolitical environment is conducive to rising national defense budgets and given that Lockheed Martin is a rock-solid free cash flow generator in almost any operating environment.

Concluding Thoughts

Shares of Lockheed Martin offer investors a nice combination of income growth and capital appreciation upside. In the face of simmering geopolitical tensions, investors would be wise to consider exposure to defense contractors. Lockheed Martin is best of breed in this space. While the company is facing a difficult 2023, its longer-term growth outlook is incredibly bright. As shares of LMT have been on a powerful upward climb of late it appears that investors are warming up to Lockheed Martin's coming financial rebound.

For further details see:

Lockheed Martin Is Best Of Breed And Worth Considering