RTX - Lockheed Martin: Not Worth Your Money At Today's Price

2023-11-27 02:57:26 ET

Summary

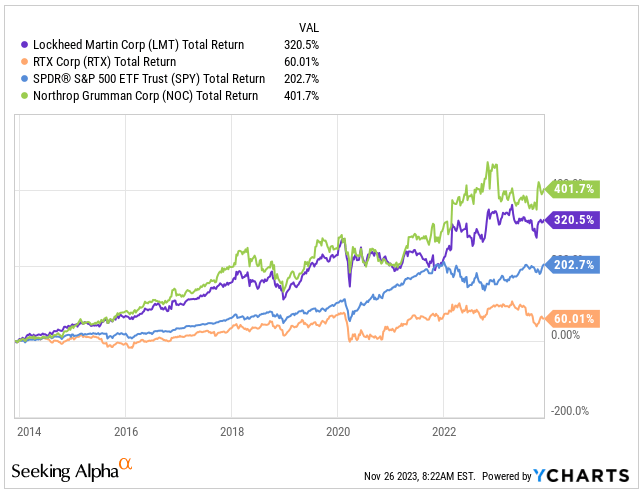

- Over the past decade, Lockheed Martin, a staple in the US defense sector, has crushed it, easily beating the market.

- LMT runs a solid and profitable business model, relying on long-term contracts with governments and boasting a hefty backlog of almost $156 billion.

- Despite the global surge in military conflicts, the Company hasn't quite expanded its top and bottom lines as much as I would have anticipated.

- Although LMT dividends are attractive, the projected growth is slow, and the current valuation poses a risk to overall returns.

- I don't foresee more than a 6% annualized return over the next 4 years. Given the plentiful opportunities in today's market, my recommendation for investors would be to look elsewhere.

Looking for a reliable, stable investment in a high-tech business within a non-cyclical industry? Meet Lockheed Martin Corporation ( LMT ). They're a major player in US defense, worth over $110 billion in market cap, specializing in aerospace and defense, designing aircraft that compete with Boeing ( BA ), innovating top-notch defense systems, and spearheading space exploration, contributing significantly to both national security and space advancement.

You've probably heard about the recent crash of the F-35 aircraft near Charleston, South Carolina. That plane was made by Lockheed Martin, part of what's known as the priciest US defense project ever. It's estimated that this project will end up costing taxpayers about $1.7 trillion over its lifetime, quite the win for Lockheed. The base model of an F-35 jet runs around $100 million, but that's just the starting point. Countries worldwide shell out significant amounts for upgrades. Currently, 17 allied nations are involved in the program, with over 975 planes manufactured since 2006.

Lockheed's scope isn't limited to the F-35, though. In a world where uncertainty and conflicts like the one between Russia and Ukraine or Israel and Palestine seem to be spreading, Lockheed is capitalizing on these unfortunate situations by selling products like the Javelin Missiles - a high-explosive anti-tank weapon - and the HIMARS system, known for its flexibility, affordability, and precision in rocket fires.

The US Department of Defense budget has been steadily growing and hit $817 billion in FY23, towering over China's threefold and dwarfing Russia's more than tenfold. Lockheed, along with peers like RTX Corp. ( RTX ) and Northrop Grumman ( NOC ), have had a successful decade, and considering the uncertain world we're in, it seems likely they'll continue to thrive in the next one.

{kind=link}

Let me walk you through Lockheed Martin's financials and why I'm keen on it. However, given the current valuation, it might be wise to hold off for a better entry point. Otherwise, the total returns might not be as impressive as expected.

The Growth Might Be Slow, But It's Reliably Stable

Given the nature of the aerospace and defense industry, there's a consistent demand for the products and services offered by Lockheed Martin due to ongoing global security concerns and military modernization efforts.

Lockheed Martin's steady performance comes from its extensive long-term contracts with governments, both domestically and internationally. These agreements have built up a substantial backlog, currently standing at nearly $156 billion as of Q3 2023 , shielding the company from market cycles. Even though the company might not boast the swiftest growth, this stability more than makes up for it.

Backlog (LMT IR)

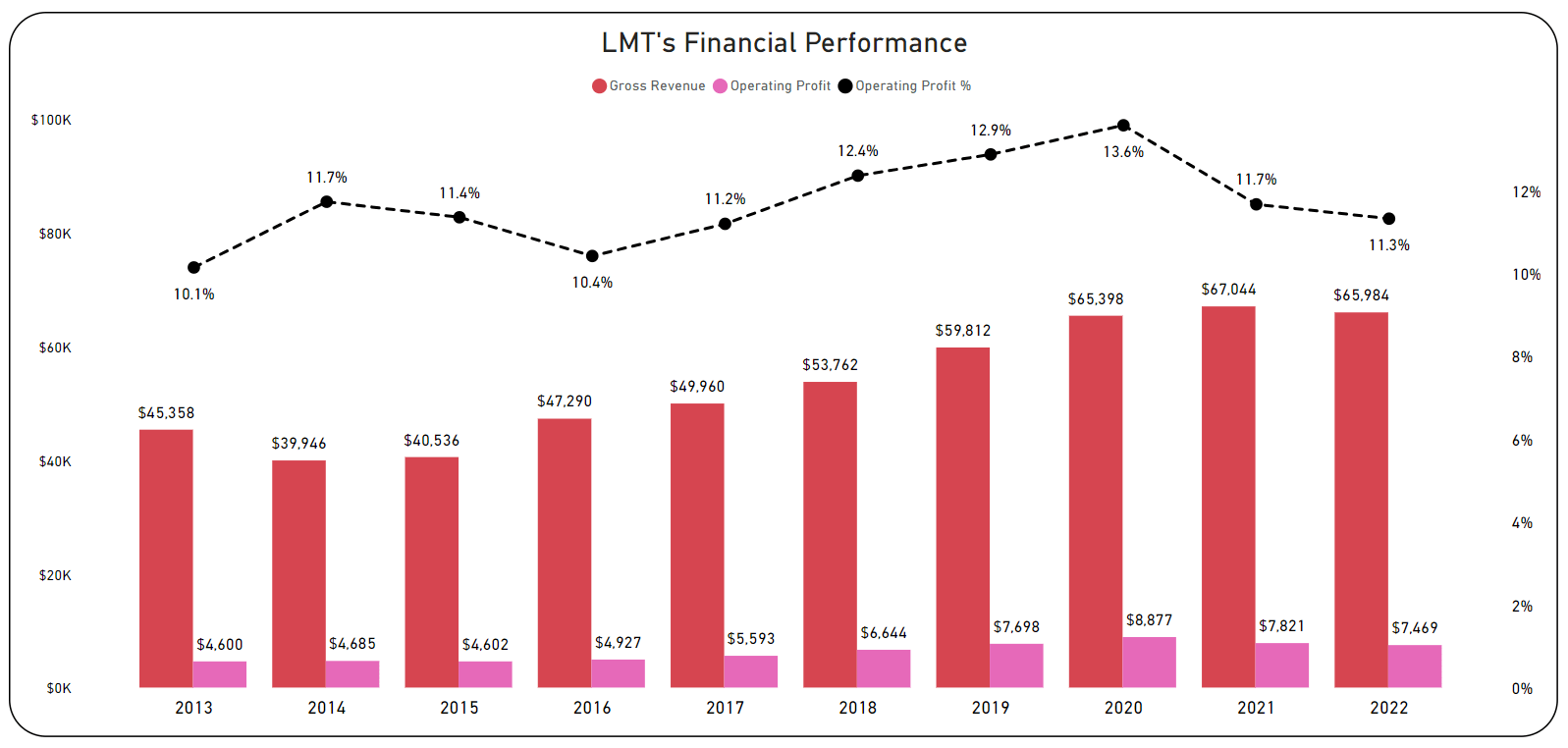

In the past ten years, Lockheed Martin achieved a consistent 3.8% CAGR in its top-line revenue. Being among the world's largest defense contractors, it benefits from economies of scale, leading to improved cost efficiencies in both production and operations. The Operating Profit saw a slightly speedier growth at an annualized rate of 5.0%.

While this might not be the fastest growth out there, the stability of the business is evident in the Operating Margin, averaging at 11.7% without significant fluctuations. This stability makes it an appealing choice for those seeking a defensive addition to their portfolio focused on dividend growth.

Historical Financials (Author's Graph (Data LMT IR))

{kind=link}

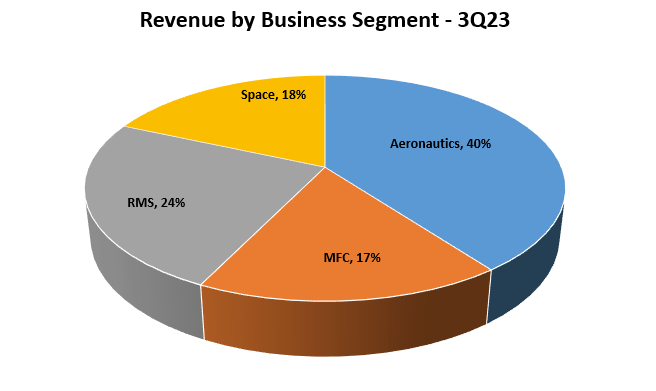

Lockheed Martin's business spans various areas . Although it's mainly renowned for its aircraft division with F-35s, making up 40% of its total revenue, it's also the primary source of operating profit, clocking in around a 10% margin as of Q3 2023.

However, sales have taken a hit compared to last year due to a drop in volume, particularly in lot funding, leading to some tough comparisons. The Skunk Works division, which is responsible for a number of highly classified R&D programs, saw increased volume, softening the blow a bit, but despite being the biggest segment, it's not the one experiencing the growth I would like to see.

The next big chunk for Lockheed Martin is the Rotary and Mission Systems "RMS", making up 24% of its total revenue with an operating margin of 11.7%. It's actually one of the segments experiencing faster growth within Lockheed, clocking a 9% YoY increase thanks to boosted production volume.

Then there are the smaller contributors - Missiles and Fire Control "MFC" and Space - each accounting for less than 20% of the total revenue. Both have margins ranging between 12-14%, but they're not exactly hitting the growth numbers I'd prefer considering their smaller size, both staying below 10% YoY growth.

Revenue by Business Segment (Author's Graph (LMT IR))

{kind=link}

You might be wondering why, amidst ongoing global conflicts like the one in Ukraine, where critical systems like Javelin missiles and HIMARS play pivotal roles, Lockheed Martin isn't experiencing more rapid growth in what seems like an ideal environment for such a company.

Well, the answer lies in supply chain issues that are still impeding efforts for weapons manufacturers to scale up production for Ukraine and replenish stocks for the US and its allies.

Despite significant support from the Pentagon, major US arms manufacturers are taking longer than anticipated to ramp up production. These companies intend to meet contracts by procuring machinery from overseas to increase the output of sought-after artillery shells.

Lockheed Martin highlighted persistent shortages of vital components, such as rocket motors for various missiles, affecting their efforts to boost production, which, in turn, is impacting their results.

Executives from defense companies have cited ongoing challenges with rocket motors, affecting missile production for Lockheed Martin, Raytheon Technologies, and prompting Northrop Grumman's involvement to supplement the previous sole supplier, Aerojet Rocketdyne.

So, what's on the horizon for Lockheed Martin?

Defense firms saw a significant increase in funding during the US government's fiscal 2023. However, the Pentagon's budget request of $842 billion for fiscal 2024, a 3.2% increase from last year's enacted budget, sits below analysts' highest expectations. Considering a sector inflation rate of around 5%, this proposal implies a real-term reduction.

Looking ahead to fiscal 2025 and beyond, the Pentagon is aiming for further growth flattening, underscoring the tough budgetary decisions faced by military leaders and Congress.

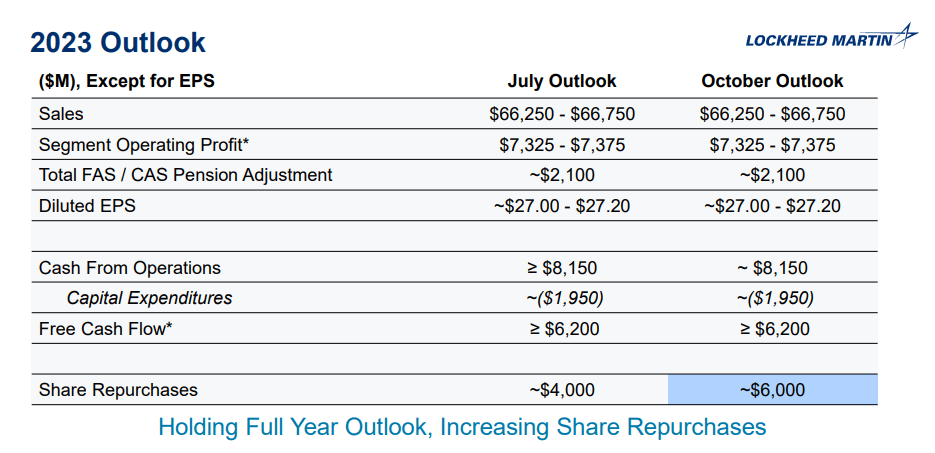

In light of this, Lockheed Martin is maintaining its outlook and anticipates delivering around $66.5 billion in sales in FY23, representing less than a 1% YoY growth, with Operating Profit aligning closely with last year's figures - hardly anything exceptional, to say the least.

{kind=link}

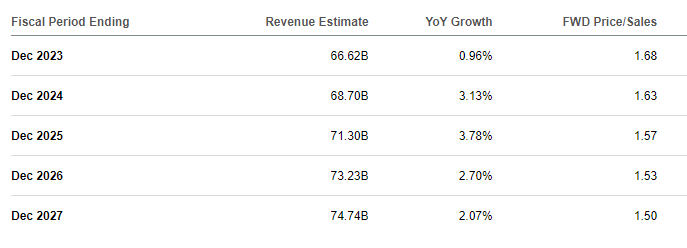

As we look ahead past FY23, analysts aren't anticipating significant growth due to the stagnant defense budget, supply chain hurdles, and ongoing production challenges related to the F-35 platform. Projections hover around a modest 2% to 3% annual uptick in top-line growth, marking a rather lackluster outlook.

Revenue Growth Forecast (Seeking Alpha)

{kind=link}

Dividends & Buybacks

According to Seeking Alpha's Dividend Grades, Lockheed Martin consistently earns high marks, mostly receiving an A+ for Dividend Safety, Dividend Growth, and an A for dividend consistency.

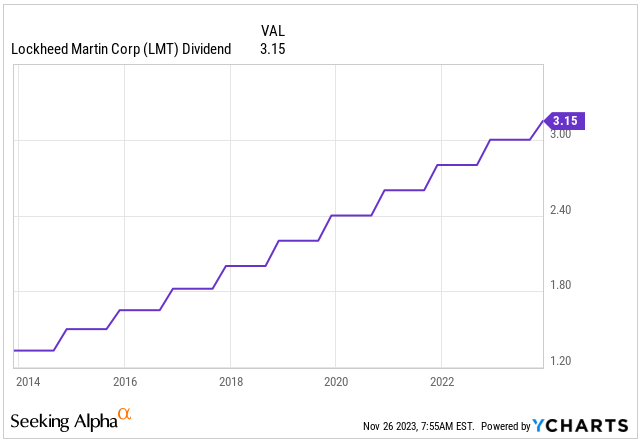

Investors often eye LMT for its dividends, given its current 2.65% dividend yield, amounting to $3.15 per share. Over the last decade, LMT's dividend has surged by an impressive 137%. If you'd invested in the stock a decade ago, your yield on cost would be an impressive 8.89% - quite an achievement.

However, recent growth has tapered, marked by a modest 5% dividend hike . Considering the anticipated lackluster future growth in both top-line and EPS, the days of double-digit dividend hikes might be behind us. This shift could potentially deter dividend growth investors.

Despite this, the dividend remains secure, boasting a payout ratio of less than 45%. Personally, I prefer stocks with a payout ratio closer to 35%, offering more flexibility for future dividend growth or providing a sturdy defense against potential dividend reductions. Nevertheless, Lockheed Martin's current payout ratio remains reasonable.

Dividend Growth (Seeking Alpha)

{kind=link}

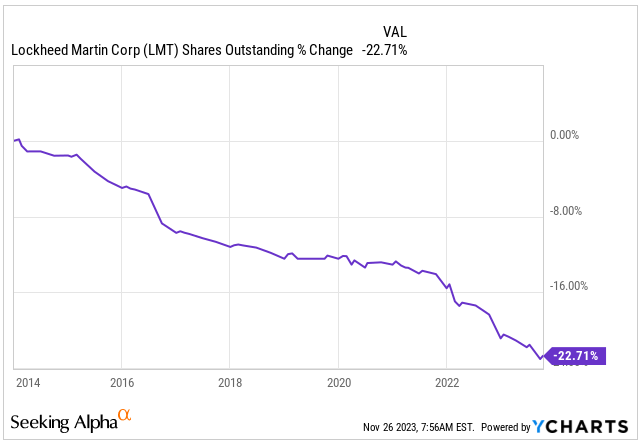

Similarly, over the past decade, Lockheed Martin has decreased its outstanding shares by nearly 30%. Given their substantial free cash flow generation, this trend is anticipated to persist. The company is projected to repurchase approximately $6 billion worth of shares, which accounts for about 5.3% of the current outstanding shares, as per their outlook.

Shares Outstanding (Seeking Alpha)

{kind=link}

Valuation

To put it simply, Lockheed Martin isn't overvalued ; it's trading at what seems to be a fair price. Considering the expected subdued growth ahead, I don't anticipate any significant expansion in valuation or substantial capital appreciation beyond the reliable dividends it offers.

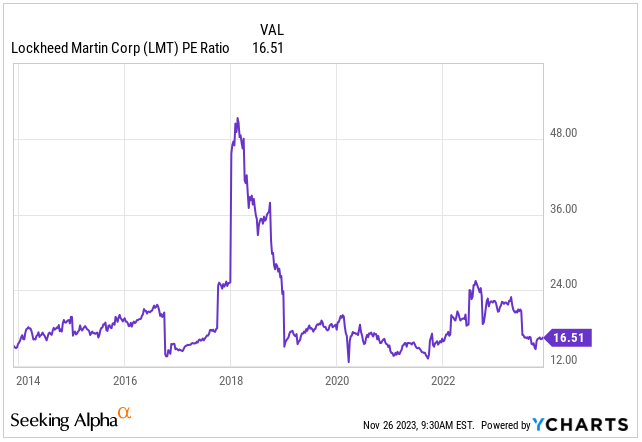

Currently, LMT is trading at 16.51x its FY23 earnings, which isn't high. In fact, it aligns with the average PE ratio over the last five years.

Looking at the Forward EV/EBITDA, the stock stands at 12.69x its FY24 earnings, marking a 6.6% increase from its five-year average.

Comparing it with the sector, one could argue that LMT is slightly undervalued, trading at a 5.4% discount when considering the Forward PE ratio.

{kind=link}

Assuming the full FY23 EPS aligns closely with last year and expecting a modest 2% to 3% top-line growth in the next 4 years, factoring in the ongoing buybacks, I estimate an approximately 3.5% annual EPS growth until 2027.

Based on LMT's five-year average Forward PE ratio of 16.5x, I project the stock could reach around $524 by the end of 2027, suggesting an annual capital appreciation of roughly 3.2%. This falls significantly below what I anticipate the market to yield.

When factoring in the 2.65% dividend yield, the overall annual return would hover around 5.85%. In my view, this is underwhelming compared to both my expectations from the overall market performance over this period and other opportunities available in today's market landscape.

| Fiscal Year |

| 2023 |

| 2024 |

| 2025 |

| 2026 |

| 2027 |

| EPS $ |

| 27.19 |

| 26.82 |

| 28.28 |

| 28.89 |

| 30.80 |

| EPS Growth |

| -0.1% |

| -1.4% |

| 5.4% |

| 2.2% |

| 6.6% |

| Forward PE |

| 16.5 |

| 17.0 |

| 16.0 |

| 17.0 |

| 17.0 |

| Stock Price $ |

| 449 |

| 456 |

| 452 |

| 491 |

| 524 |

Conclusion & Game Plan

Lockheed Martin, a major player in the US defense sector, maintains a stable, non-cyclical business model bolstered by an impressive backlog hitting nearly $156 billion as of Q3 2023.

While I believe the company will likely withstand economic fluctuations, historical growth has been sluggish and is anticipated to continue this trend, especially with the real decrease in the US defense budget.

The company's healthy 2.65% dividend appeals to income and dividend growth investors, but I don't foresee the robust double-digit dividend hikes seen in the past due to the sluggish growth and less aggressive buybacks.

Although I appreciate the overall business, I'm not looking to buy in at the current juncture.

My ideal entry point for Lockheed Martin would be at a valuation around 13x its earnings, suggesting a stock price of $353. However, I'm hesitant to pay more, given the plentiful other market opportunities that promise better returns without compromising on the quality of the business.

For further details see:

Lockheed Martin: Not Worth Your Money At Today's Price