NOC - Lockheed Martin: Opportunity Knocks

2023-12-31 09:30:00 ET

Summary

- Lockheed Martin is a high-quality, long-term investment choice that's value-priced, especially in a frothy market.

- LMT benefits from long-lived contracts in the defense industry, including the F-35 program, resulting in steady revenue growth and respectable margins.

- It has a strong balance sheet, a low leverage ratio, and a well-covered dividend, making it an attractive option for income and growth investors.

Everyone is a value investor in one form or another. That’s because nobody buys a stock on the mere fact that it’s expensive, but rather because they believe in the future value appreciation potential of the investment.

One of the differentiating factors is the length of time one is willing to hold. For example, short-term day traders prefer volatility and would like to see quick share price appreciation, whereas long-term investors prefer to accumulate at value points and are willing to forsake short-term gains in favor of compounding wealth over the long run.

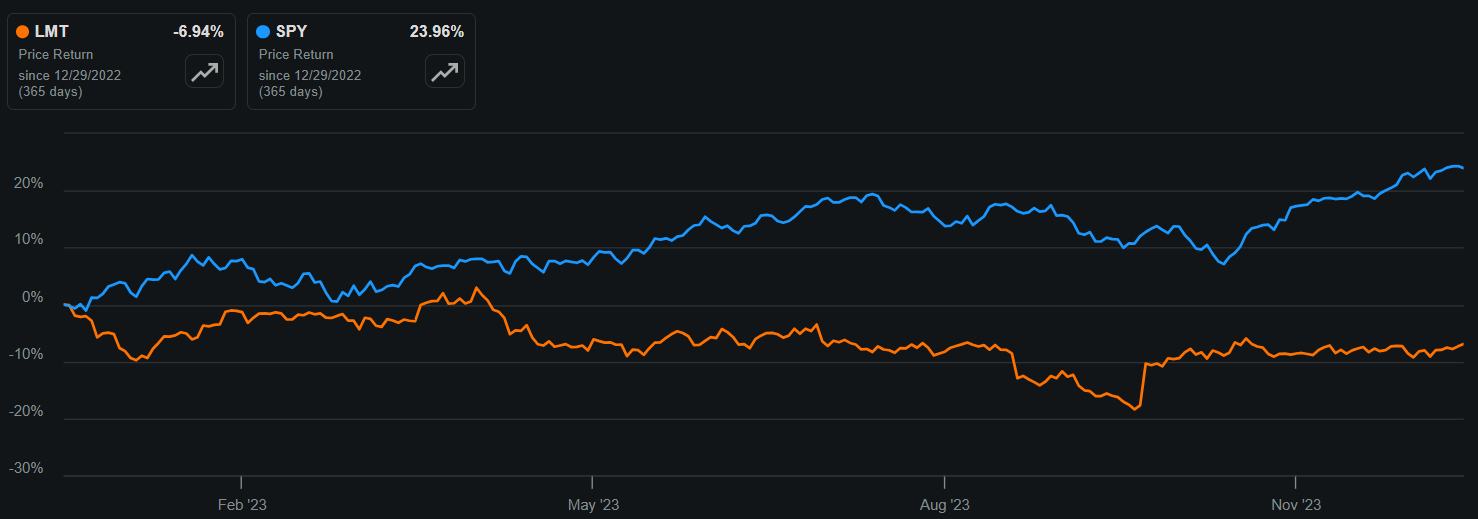

This brings me to Lockheed Martin ( LMT ), which is what I would consider a high quality, moat-worthy company for long-term investors, and which has not engendered the type of quick growth that short-term investors would like to see. As shown below, LMT’s share price has been stagnant over the past 3 months, and is down 7% since the start of the year, far underperforming the S&P 500 ( SPY ).

{kind=link}

I last covered LMT here back in November of last year, with a 'Hold' rating, noting its strong backlog amidst global tensions and its fair valuation. It appears that my rating back then was reasonable, as the stock price has fallen by 5% since my last piece (-2% total return including dividends), and has been outperformed by the 20% rise in the S&P 500 over the same timeframe.

In this article, I provide an update and discuss why investors weary of a frothy market may want to consider LMT at present for potentially strong returns from here, so let's get started!

Why LMT?

Lockheed Martin strikes me as being one of those companies that an investors can hold onto for the long run without having to constantly worry about. That's because unlike a "normal" company that's subject to changing consumer tastes and creative destruction, LMT benefits from having established a reputable technical base in the defense space and long-lived contracts.

This includes LMT's signature F-35 program, which stands as the largest defense procurement program ever awarded by the U.S. Department of Defense and is expected to last through the 2060's. It's worth noting that LMT first started developing the F-35 in 1995. This compares favorably to say, the pharmaceutical industry, which sees "only" 20 years of patent protection on new drugs to market.

LMT's long-lived contracts across segments that stretch beyond the F-35 to include helicopters, missile defense systems, and space systems have resulted in a revenue growth streak that's rather immune to economic cycles. As shown below, LMT's sales have more than doubled over the past 20 years, and it's been rather immune to the recessions in 2008-2009 and in 2020.

{kind=link}

Moreover, unlike other industries that bear the brunt of development costs that hold no promise of market acceptance, defense contractors like LMT are paid to develop their weapons systems after their design and bids are approved by the issuing defense agency. These inherent traits and pricing power due to built-up expertise results in respectable margins for LMT, as reflected by its A+ grade for profitability and an industry-leading return on total capital of 22.6%, comparing favorably to the 7.1% median for the industrial sector.

LMT's track record of steady growth combined with shareholder returns through dividends and share buybacks have resulted in respectable total returns. This is reflected by its 301% total return over the past decade, beating the 212% of the S&P 500, 121% of Boeing ( BA ), and 239% of General Dynamics ( GD ), while being bested by the 385% total return of Northrop Grumman ( NOC ), as shown below.

{kind=link}

Meanwhile, LMT has continued its growth trajectory this year, with top-line revenue growth being ahead of management's expectations. This is reflected by revenue growth of 2% YoY to $16.9 billion during the third quarter, and 3.6% YoY revenue growth for the first nine months of the year to $48.7 billion. LMT also generated an impressive $2.5 billion in free cash flow during the third quarter.

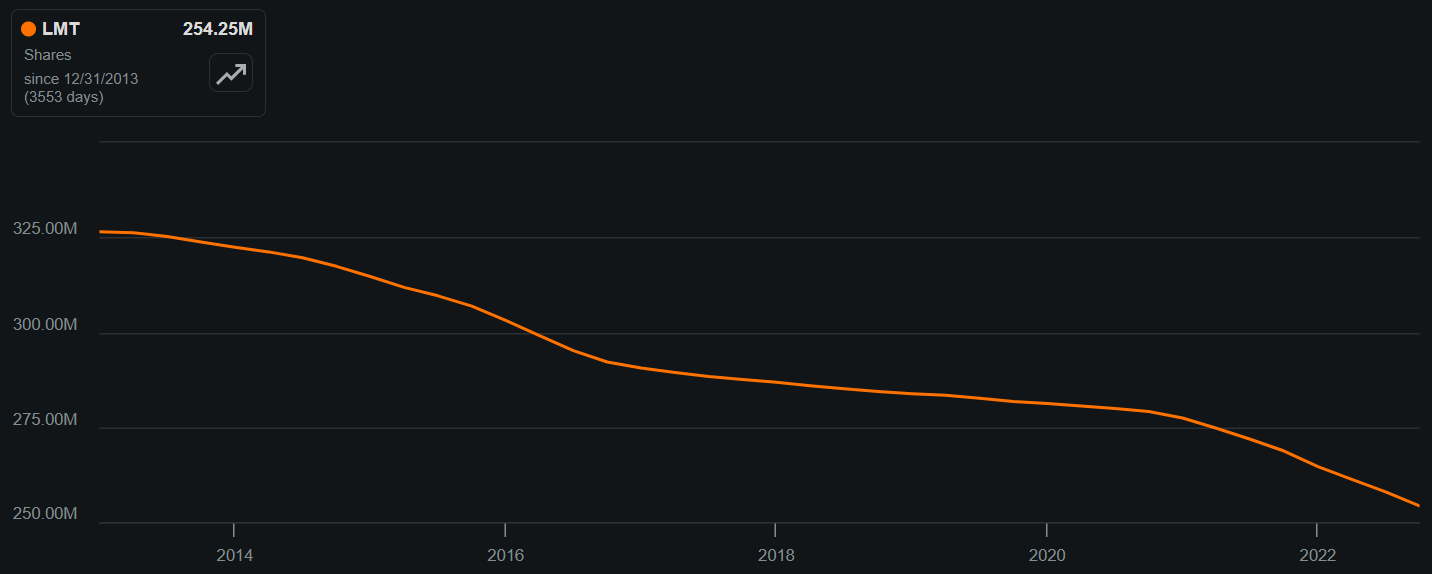

Because it has a long line of sight with respect to future cash flows and expected development costs, LMT as able to return nearly 100% of its FCF to shareholders in the form of dividends and share buybacks. Also encouraging, LMT increased its share repurchase authorization by $6 billion to a total authorization of $13 billion. Based on LMT's current market cap of $112 billion, this equates to a potential 11.6% reduction in the outstanding float at the current market price. As shown below, LMT has reduced 22% of its outstanding shares over the past 10 years.

{kind=link}

Looking ahead, LMT is well-positioned to benefit from demand not only from the U.S., but also globally across Europe, Australia , and Asia for its F-35 and defense systems. This includes a recent major signing announced in late December for the South Korean government to order 20 F-35's from LMT. Morningstar also supports the thesis that LMT should benefit from geopolitical tensions, as noted in its recent analyst report :

Lockheed should benefit from recent and foreseeable increases in U.S. defense spending, driven in the short term by orders to resupply munitions to Ukraine as its forces expend them faster than they can be made. Longer term, the Pentagon has prioritized modernization of the military's ability to counter aggression from multiple so-called great power rivals, namely China and Russia, while also managing threats from terrorism and hot spots like Iran and North Korea.

Risks to the thesis include the fact that LMT's fortunes are tied to defense spending appropriations by the U.S. Congress. While I don't see the potential of defense spending cuts in the near term due to the aforementioned global tensions, this is a risk worth keeping in mind. Other risks include potential for higher interest rates, which would increase borrowing costs.

This risk is mitigated, however, by LMT's strong balance sheet with one of the lowest leverage ratios among its peers. LMT carries a net debt to TTM EBITDA ratio of just 1.35x, sitting below the 3.0x level generally considered to be safe by ratings agencies, and carries an A- credit rating from S&P. Encouragingly, LMT's leverage ratio is down from 1.64x at the end of 2022, as a result of lower net debt and higher EBITDA over the trailing 12 months.

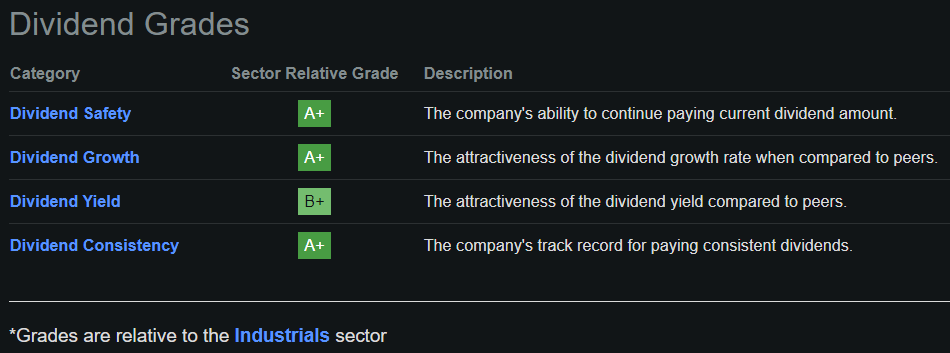

Importantly for income investors, LMT currently yields 2.8% and the dividend is well-covered at a 43% payout ratio. While the yield isn't particularly high, it is double the 1.4% yield of the S&P 500 and comes with an 8.2% 5-year dividend CAGR (comparing favorably to 5.4% for the S&P 500) and 21 years of consecutive growth, making LMT a strong candidate to become a dividend aristocrat in 4 years. As shown below, LMT receives high marks for dividend safety, growth, yield and consistency.

{kind=link}

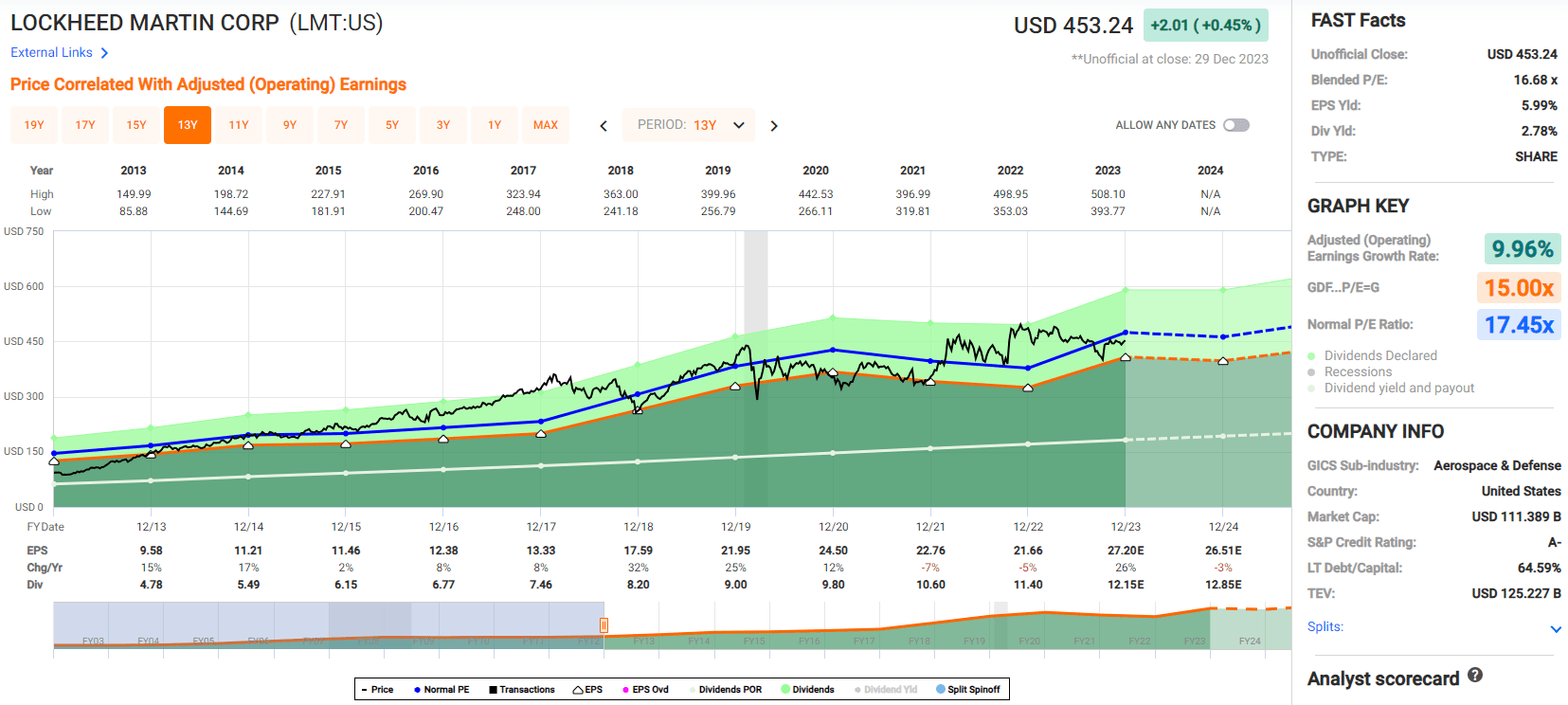

Lastly, I see value in LMT at the current price of $453 with forward PE of 16.7, especially amidst a froth market with elevated valuations in a number of mega- and large-cap names. LMT's valuation also sits a bit lower than its normal PE of 17.5 over the past 10 years. With a 2.8% dividend yield, potential 2% annual share count reduction (based on historical trend), and mid-single digit EPS growth expectation starting in 2025, LMT could produce a long-term total return that could meet or exceed that of the market average.

{kind=link}

LMT also trades at a discount to its peers from a price-to-cash flow perspective. As shown below, its 15.0 price-CF ratio sits below that of NOC, GD, and RTX Corporation ( RTX ).

{kind=link}

Investor Takeaway

All in all, Lockheed Martin offers a combination of steady growth and shareholder returns through dividends and share buybacks. Its strong track record, impressive free cash flow generation, and demand for F-35's globally make it well-positioned for continued success in the defense industry. With a reasonably attractive valuation, especially amidst a frothy market, and a dividend yield that is 2x that of the market average and higher dividend growth, I'm upgrading LMT to a 'Buy' at present.

For further details see:

Lockheed Martin: Opportunity Knocks