RTX - Lockheed Martin: Paying The Price For Defense

Summary

- Lockheed Martin is a dominant force in the defense industry.

- The company's locked-in F-35 contracts should yield strong, predictable returns for decades.

- The stock isn't a value today, I prefer Raytheon. LMT is a hold.

After covering Raytheon ( RTX ) earlier this week, it seemed like a good idea to do a dive into Lockheed Martin ( LMT ), the largest defense contractor in the market based on government allocation.

{kind=link}

The company has compounded greater than market returns over the long-run. LMT is firmly rooted in the oligopoly of major defense contractors, and has been a pioneer in aerospace throughout its history, including notably the legendary Skunk Works. The company has historically been well-managed, competitive in winning contracts, and shareholder-friendly. This has shown through in returns, with a 12% annualized total return over the past 2 decades, compared to the ~8-9% return of the SPY.

Lockheed's Place in the Defense Industry

Bloomberg

I talked quite a bit about the benefits of investing in the defense industry in my last article. The significant up-front research and development, intense competition for contracts, and deeply rooted relationships between the contractors and the government make the industry nearly impermeable to new entrants. The government awards contracts with the expectation of a long service life for the products, and it requires these companies to be able to flex manufacturing prowess in delivering orders, stability to ensure operational security, and the ability to maintain and service the equipment over the long-term. The trust that comes from programs like the Hellfire missile, Black Hawk helicopter, F-16, and others is earned over a long period of time.

Macro Trends

Adding to that, the government's defense budget has pretty steadily moved up over time. I've shown a graph of post-cold war spending, and outside of some scalebacks from 2011 to 2018, the budget has been up and to the right along with GDP. Most recently, the spending bill approved a 10% increase to $858B for 2023. LMT derives around 70% of its revenues from DOD contracts, making it closer to a pure-play defense contractor than RTX, which has significant commercial aerospace operations.

There's always risks of reductions in defense budgets, but the war in Ukraine has provided both American and other NATO country interest in LMT's products, and global tensions have been scaling up in recent years with Russia and China. Although it's not what anyone would hope for, the reality is its unlikely defense budget cuts are coming in the near-to-medium term, considering the risks.

Recent Results

{kind=link}

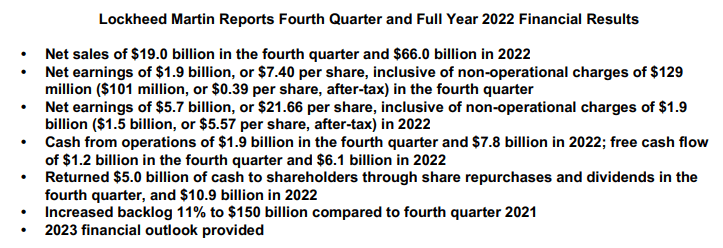

LMT's recent results were mostly flat, overall. The company delivered 7 fewer F-35's than projected due to an operational pause on engine deliveries, and sales declined in rotary, missiles and support systems, and space.

However, the backlog is strong, and grew at a book-to-bill ratio of 1.2 to $150B. The company's products look to drive much higher growth into next year.

{kind=link}

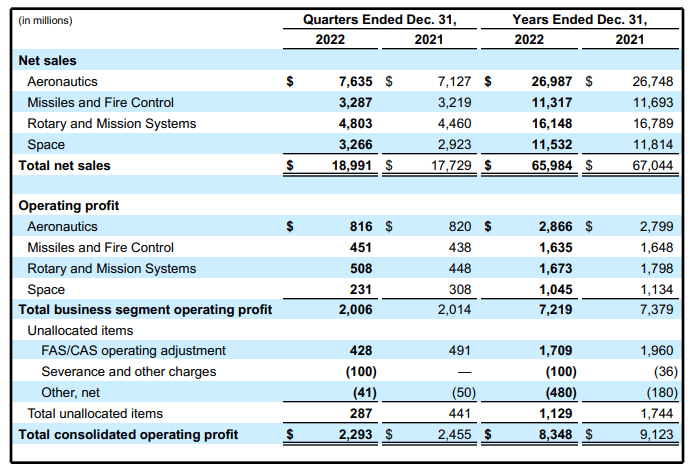

Breaking down the company's segments a little, the largest portion of sales and operating profits comes from aerospace. The F-35 program was recently projected by the Government Accountability Office to cost $1.7T overall, from R&D to production, servicing, and sustainment. It was a joint effort between the US, UK, Italy, Netherlands, Australia, Norway, Denmark, and Canada. Since the project's launch, Germany has signed on, and as the Ukraine war stretches on, demand looks to continue for the fighter jet across NATO. A contract like this one will provide steady demand to LMT for decades. Through multiple tech upgrade cycles, servicing contracts, and additional orders to maintain numbers, LMT is looking at a long-term cash cow with strong demand and mission-critical applications.

The F-35 does have its detractors in government, however, and LMT is under the microscope to reduce costs and improve reliability. It will be important for investors to stay plugged in to the program somewhat, considering its importance to the company. LMT will have some push-ups to do from here to lower costs and provide maximum value considering the size of the program. However, that being said, with the sunk costs of the F-35, the likelihood of material negative impact in the form of a contract shift or overall failure of the program are incredibly unlikely.

Sikorsky Helicopter, acquired from the United Technologies breakup, will not be a huge growth driver for the company, but it does represent the second-largest segment. The company produces the iconic Black Hawk helicopter, and upcoming orders for the CH-53K King Stallion heavy-lift helicopter and others should maintain a strong backlog for the business going forward.

Hypersonic missiles and missile defense systems are the major growth driver for the Missiles and Fire control segment, and the company's United Launch Alliance engaged in satellite launches and Orion Exploration class spacecraft mounted on NASA's Artemis I has 7 missions under contract in the space segment.

The interesting wrinkle in the company's space segment is the competition with SpaceX and Blue Origin. 55% of revenues come from satellite services and products, and innovation in reusable rocket launch capabilities could pose a risk to LMT from here. However, the portion of overall revenues at risk from competition with those companies is not significant, and is not an existential threat to the overall business. Overall, the space segment is surprisingly not all that enticing to me as an investor. It's the lowest-margin portion of the business, and it appears less predictable than the other segments overall.

{kind=link}

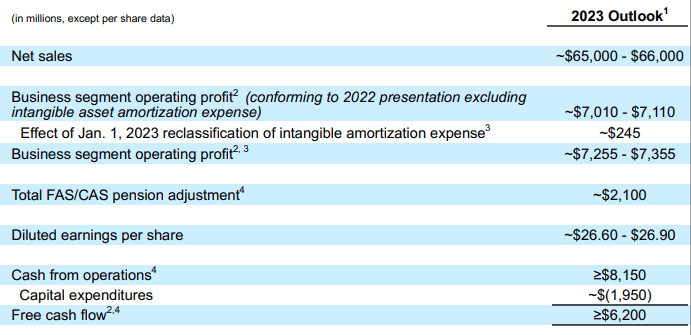

Looking forward, the company is projecting improved growth in 2024. Considering the long lead times for the company's products, they are able to forecast sales well into the future with the backlog, so it's not empty words. However, 2023 will be a year of mostly treading water for LMT, with a small decrease in revenue overall.

Capital Allocation

The company's balance sheet is in a good spot. Free cash flow is strong, with $6.1B against a market cap of $121B. The long-term debt load is relatively stable and easily serviceable with the company's cash position, and the dividend is well covered.

The dividend has been hiked by the company for 20 consecutive years, and I have no reason to believe LMT won't be joining the ranks of the Dividend Aristocrats 5 years from now. Dividend growth most recently was 7.7%, with a 10-year average of 10.85%

The company is focused on cannibalizing the share count, as well. Most recently, the company repurchased $7.9B of shares in 2022, and upped the authorization by another $4B into next year. The share price has bounced around quite a bit in recent years, but is now reaching new highs so it's likely the shares were repurchased at lower prices.

Valuation

{kind=link}

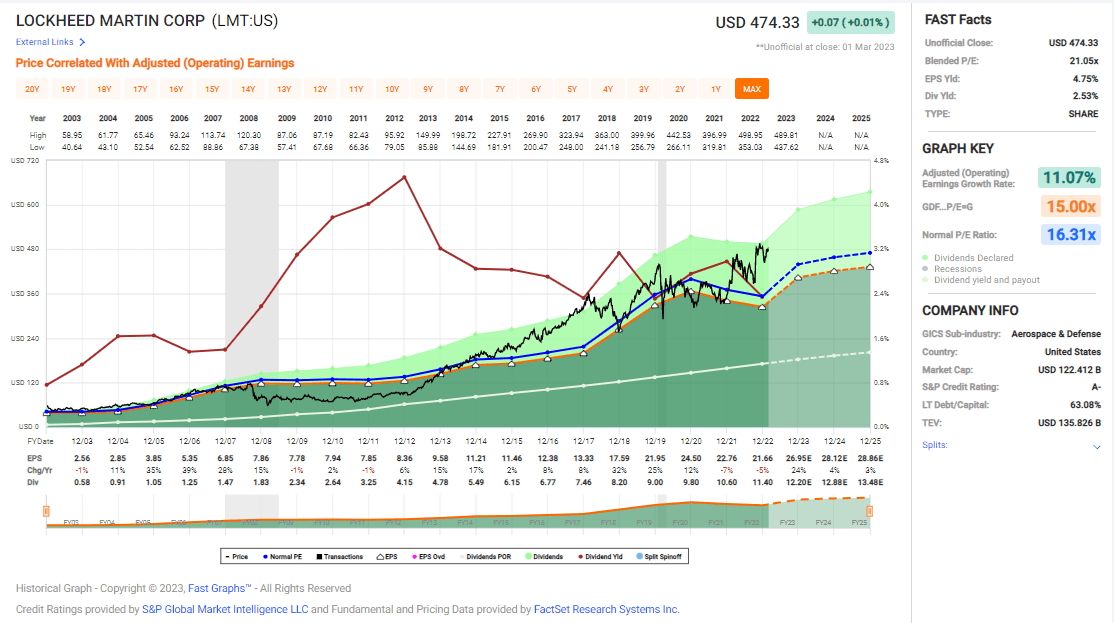

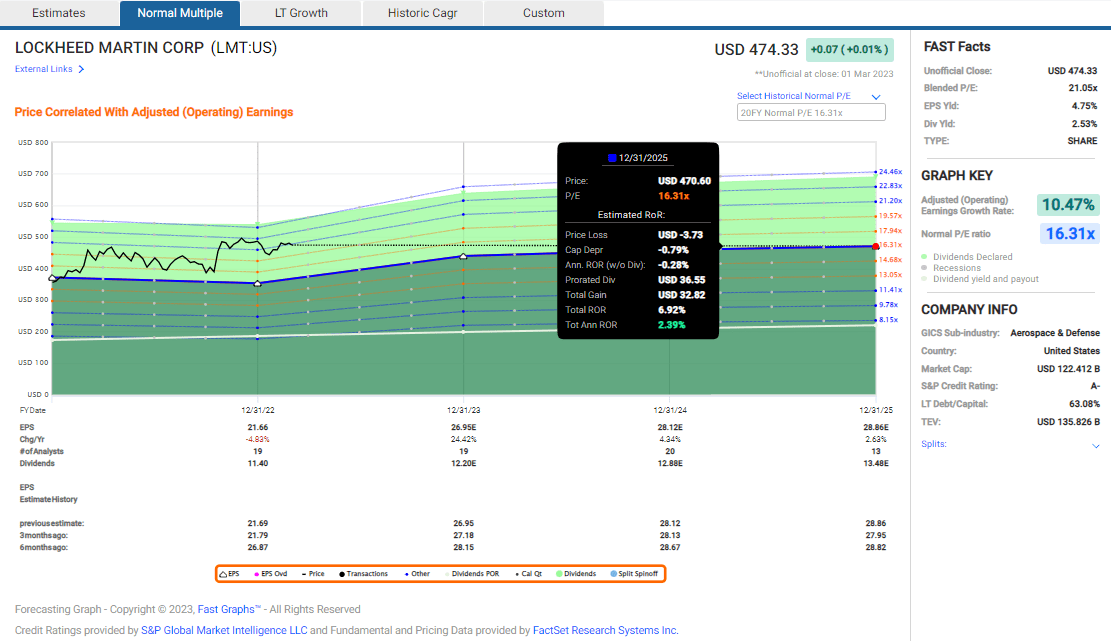

Looking at the company's long-term earnings, it's a mostly steady grower and has compounded earnings growth at 11% over the long-run. That's a value that puts LMT in good company as a compounder. However, the company appears expensive today. As I mentioned above, the company is treading water in 2023, and anticipates a re-acceleration of earnings growth in 2024 on the back of F-35 sustainment growth and additional orders throughout the business lines.

{kind=link}

Based on analyst estimates for earnings growth and a return to the company's long-term average valuation, the multiple compression and lackluster earnings growth would yield an annualized total return of 2% or so from here.

{kind=link}

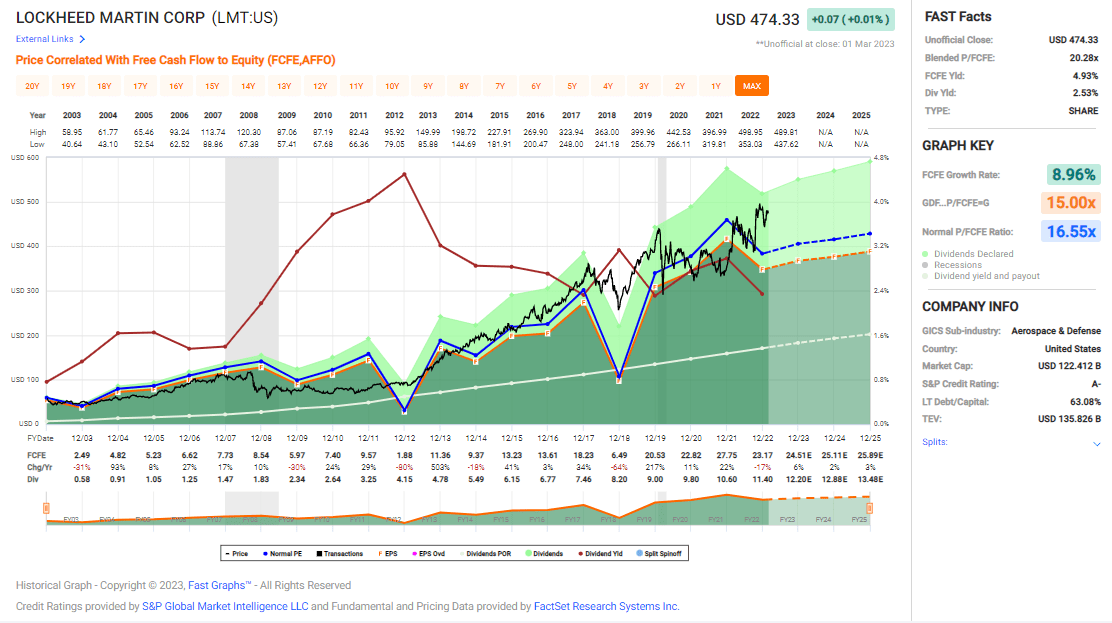

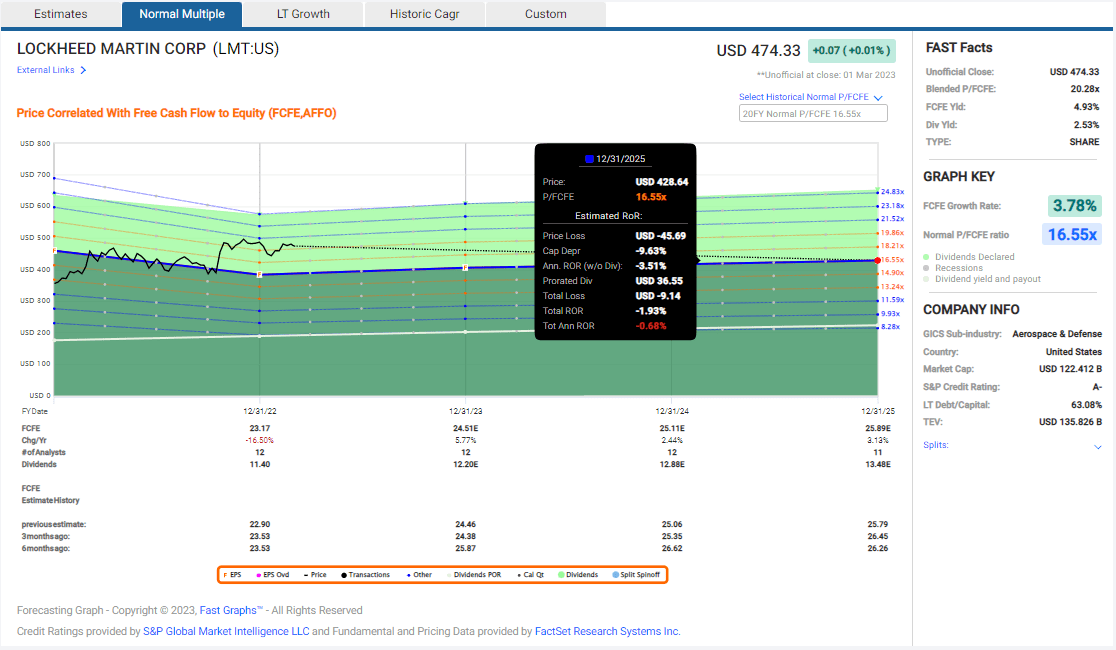

Free cash flow has grown at around 9% a year over the long-term. Outside of major capex events and one-offs, it looks to have been relatively steady and is projected for low-to-mid single digit growth over the next few years.

{kind=link}

Based on the company's typical FCF multiple, and analyst estimates for FCF growth, an investment today would lose money off multiple compression over the next 3 years or so.

Conclusion

LMT is a strong operator with some incredible products. The F-35 should provide the company stability and a huge runway for cash generation in coming years. However, the stock is overly expensive today, especially considering the article I just wrote on Raytheon trading at a more attractive valuation with similarly enticing growth prospects although slightly more risk. I'm a buyer of LMT on a sell-off, which the stock has historically delivered from time to time for observant investors. It's a hold today, watching for a price closer to $400-420, which it was trading below as recently as October.

For further details see:

Lockheed Martin: Paying The Price For Defense