LMT - Lockheed Martin: Present Defense Spending Doesn't Indicate Long-Term High Returns

2024-01-18 14:35:38 ET

Summary

- Increased global defense spending presents opportunities for Lockheed Martin, particularly in advanced manufacturing and cybersecurity.

- The company's growth rates have improved, but it may not be as profitable or high-growth as other sectors like technology.

- Valuation suggests that Lockheed Martin may be slightly undervalued, but realistic growth expectations should be considered due to limited defense budget growth and potential risks.

- Due to the moderate growth I believe is likely for the company long term, my analyst rating for the stock is a Hold.

While defense spending may be on the rise, outsized investment returns from Lockheed Martin ( LMT ) stock seem unlikely unless global wars escalate, which would significantly dampen or even depress other sectors in portfolios. As such, betting heavily on defense at this time seems unwise to total portfolio returns in my view. Instead, I am looking at diversifying my portfolio away from concentrated exposures to protect my capital from present geopolitical uncertainty.

Increased Global Defense Spending

The US defense budget has been set to $842 billion for 2024, part of the trend of rising global armaments spending. This is largely due to new challenges defense forces are facing and subtle tactics in hybrid warfare. Investments in AI and automation are at the forefront of industry-leading defense portfolios needed to maintain the global balance of power.

Lockheed Martin will benefit from global defense spending increases, and particular emphasis is on advanced manufacturing like 3D printing. The company is also manufacturing interceptor missiles for systems such as Patriot. This is seeing increased production, directly impacting LMT's operations and financials.

AI, quantum technologies, and microelectronics are going to be intensely leveraged in modern warfare. Heightened cybersecurity is, therefore, at the forefront of priorities in the military supply chain, directly impacting LMT.

Shares for major defense organizations have outperformed the S&P 500 recently, with the trend expected to continue. This is largely due to the demand for munitions and weapons systems driven by conflicts like the Russia-Ukraine war and Israel-Palestine. Increased production volumes for existing systems have led to more profit than developing new systems. As an example, Lockheed Martin's GMLRS (Guided Multiple Launch Rocket Systems) production is set to increase, representing the firm's responsibility to meet demand.

Growth Concerns & Further Financial Considerations

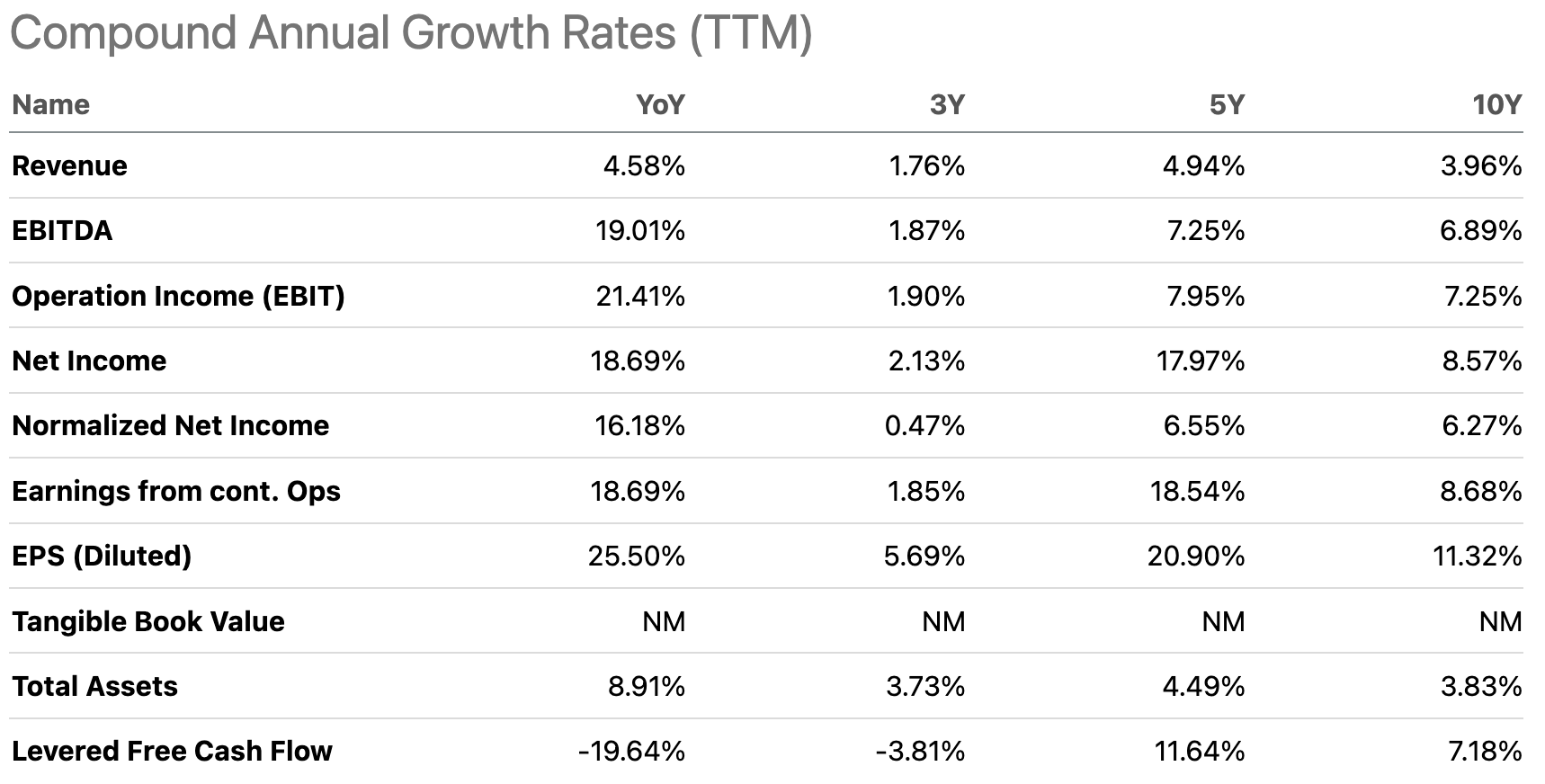

The firm's compound annual growth rates have increased significantly on a YoY basis compared to its three-year averages, particularly for its bottom line. While its revenue has grown from a 1.76% three-year average growth rate to 4.58% YoY growth today, its net income has risen from a 2.13% three-year average growth rate to 18.69% YoY growth today:

{kind=link}

I think Seeking Alpha's Quant Factor Grades for the firm's growth are largely taking in its comparative data from historical averages, not fully equating for the predicted and potential future growth expected from defense budget increases globally in the decade to come. Nonetheless, the firm's profitability is rated A+, with a net margin of 10.29%.

Seeking Alpha

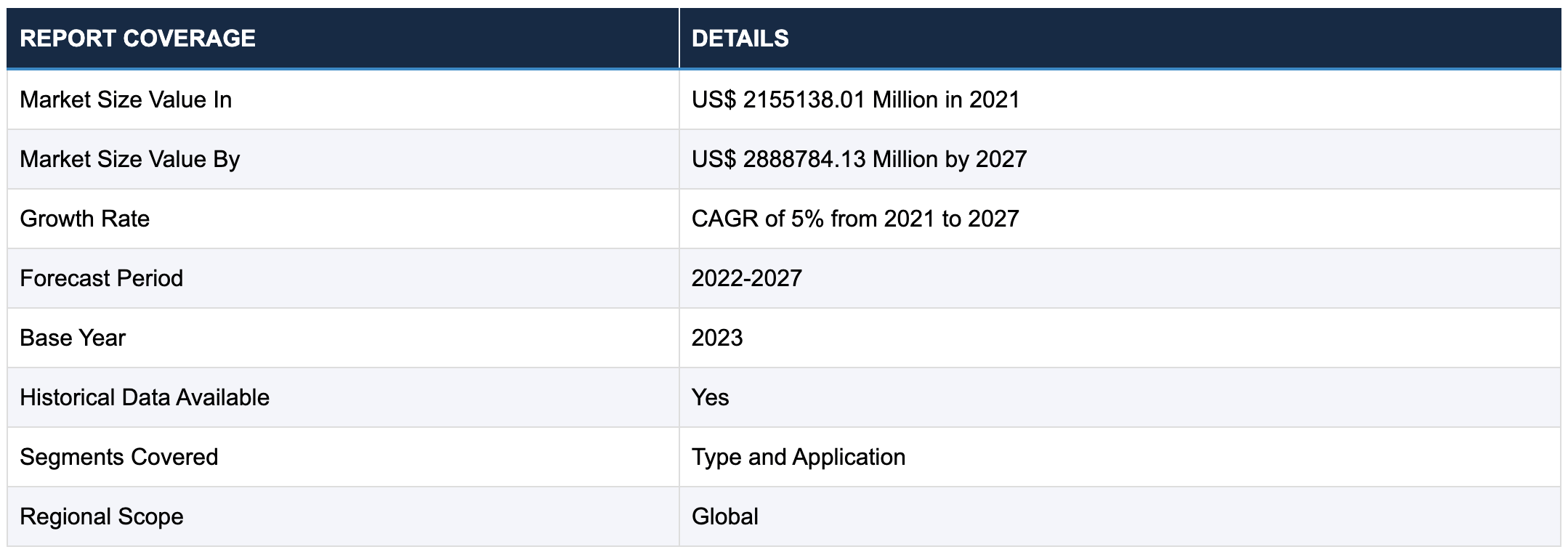

However, unrealistic growth expectations surrounding defense stocks at present are often dependent on speculative global conflicts arising. These are situations the general larger economy would undeniably lose from, while defense contractors and shareholders would win. Business Research Insights outlines a realistic CAGR estimate for the 2021-2027 timeframe that is not based on speculative escalations:

{kind=link}

As such, while the firm's current growth rates have increased recently, I find it unlikely that Lockheed Martin will be as profitable or as high growth as other areas like technology in the coming years when analyzing defense market traction against AI market growth, for example. It, therefore, seems unwise to allocate a significant portion of a portfolio to defense over the long term unless one is actively expecting major wars in the world to escalate. At that point, any balance in a portfolio allocated to other sectors could potentially collapse. Based on those effects, I am consciously allocating away from defense and expecting a larger total return, betting against a global war escalating. I am still protecting myself from any uncertainty by actively looking for non-defense related stocks that are relatively uncorrelated to technology stocks that could be impacted by a geopolitical escalation surrounding Taiwan's TSMC ( TSM ), for example.

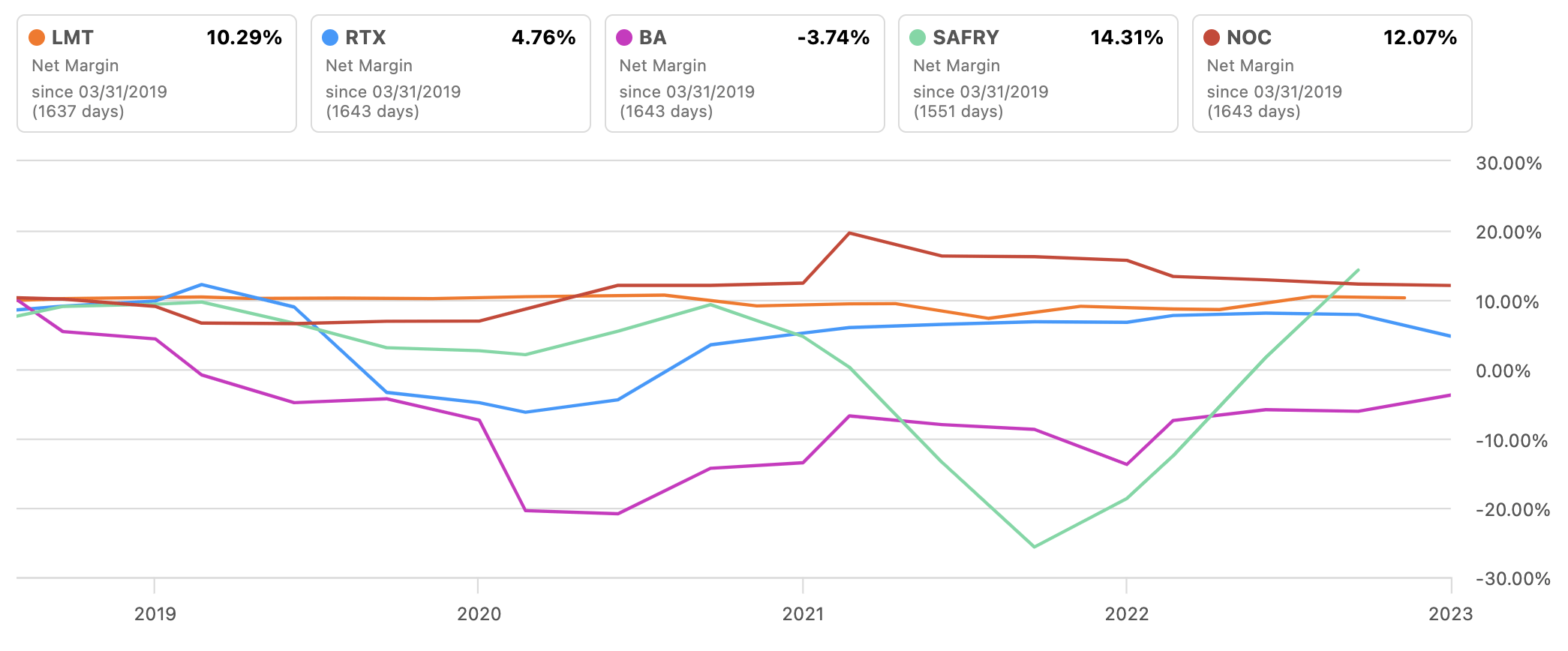

If one were to seek to buy Lockheed Martin stock now, however, one reason to do so could be its margins when compared to competitors. The company is reliably right up there at the top alongside its other defense peers, with little net income margin volatility:

{kind=link}

Valuation

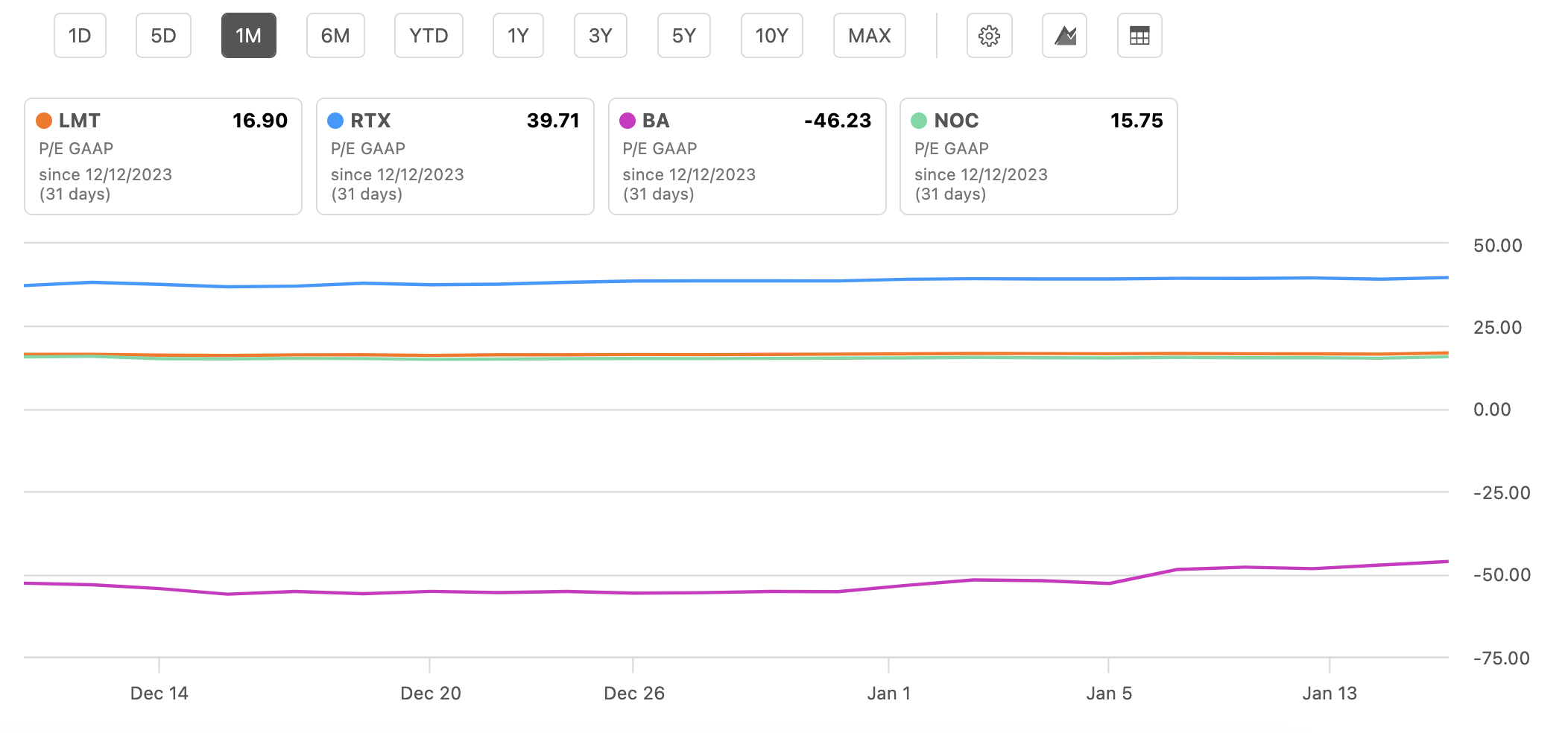

Due to recent and projected growth increases, some people believe Lockheed Martin is fairly valued at the moment. Its P/E GAAP ratio is relatively stable when compared to other defense companies, resting at around 17:

{kind=link}

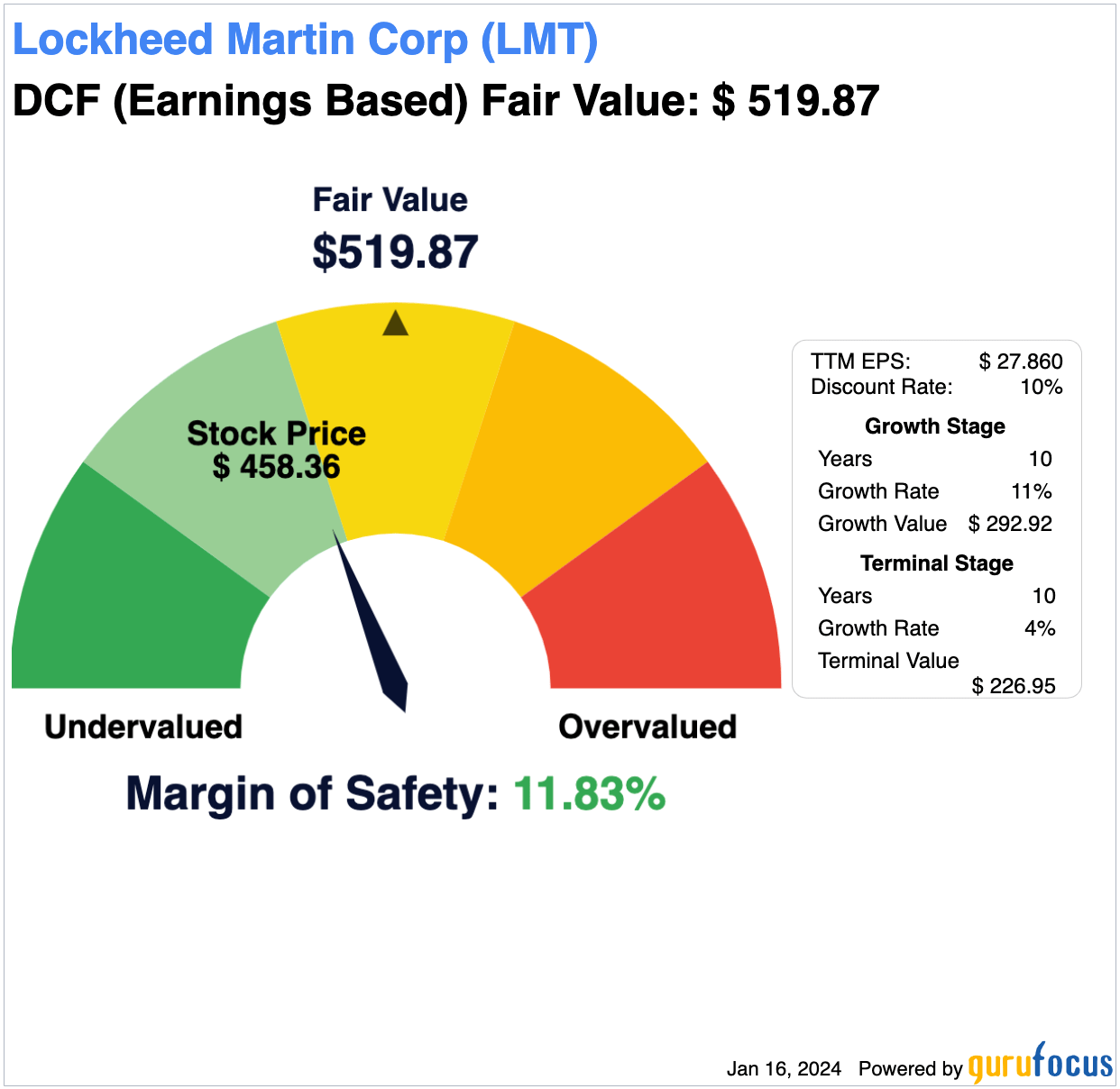

There is some argument to be made on a DCF basis that the company is slightly undervalued. Using a historical diluted EPS growth of around 11% from a 10-year average, I've used this in a DCF analysis, and the stock seems to be around 12% undervalued based on the calculation. I used a 10% discount rate and a standard 4% terminal-stage growth rate. The fair value appears to be around $520.

{kind=link}

This contrasts with Seeking Alpha's Factor Grade C- for the stock, but it's worth recognizing that the firm has a forward P/E GAAP ratio of around 17, Quant Factor Grade B, over 21% below the sector median.

Risks

While the defense budget for 2024 is a record $842 billion, this is only a 3% increase from the previous year. Such limited growth in times of heightened geopolitical tensions could signify that defense spending growth might not reach double digits. This would significantly impact future growth prospects for the firm, and the stock should be treated with realistic, moderate growth expectations, not inflated by geopolitical speculation.

Lockheed Martin's CFO, Jay Malave, indicated profit margin volatility due to impacts from a classified missile program. The program is expected to cause a margin decline of about 25-50 basis points for the year. The company's F-35 airplane deliveries also didn't meet expectations in 2023, and delays have been pushed into 2024. The company is aiming for a delivery rate of 156 units per year by 2025, dependent on the validation of technology refresh (TR-3), which is already behind schedule.

Conclusion

While Lockheed Martin could be an opportunity at the moment based on increased global defense spending, outsized returns depend on escalated global conflict, which would then significantly deplete returns from other industries. As such, betting heavily on Lockheed Martin seems unwise. My analyst rating for the stock is a Hold.

For further details see:

Lockheed Martin: Present Defense Spending Doesn't Indicate Long-Term High Returns