LMT - Lockheed Martin: Q1 2023 Signals Easing Short-Term Issues Long-Term Upside

2023-04-18 15:39:31 ET

Summary

- Lockheed Martin just published its Q1-23 earnings, beating even my above-consensus expectations. As expected, Lockheed Martin's short-term issues were likely overexaggerated and are starting to ease.

- Aeronautics revenues decreased by 2.0%, Missiles & Fire Control decreased by 2.6%, Rotary & Mission Systems decreased by 1.1%, and Space grew by 15.6%.

- Overall, revenues grew by 1.1% YoY, but more importantly, segment EBIT margins improved in Aeronautics, MFC, and RMS, reflecting margin problems are recovering.

- Lockheed Martin is on pace to beat analyst expectations and its own guidance for 2023, which sets the way for an earlier return to growth than initially thought.

- Due to the stock price increase, I update my Strong Buy rating to a Buy and raise my price target to $553 per share.

Lockheed Martin ( LMT ) just announced its Q1-23 results, reporting 1.1% revenue growth and $6.6 EPS, both beating expectations. The company is showing early signs of recovery from its supply chain issues, as margins are expanding slightly faster than expected. Lockheed continues to progress with its capacity enhancements across each of its major programs, on its way to meeting the increasing unsatisfied demand for its offerings. Mostly as a result of the stock price increase, I update my Strong Buy rating to a Buy, and raise my price target to $553 per share.

Background

A month and a half ago, I published an article about Lockheed Martin and rated the stock a Strong Buy. I urge you to read that article, in which I explained my investment thesis in detail and why I expected above-consensus profitability and growth in 2023, as well as described the company's operating segments, risks, and Lockheed's major tailwinds and headwinds.

In short, my investment thesis regarding the company is based on Lockheed's timely capacity enhancements (specifically in its F-35 program) as defense budgets all over the world are on the rise. Unlike many other defense contractors, Lockheed has a history of fulfilling its immense backlog, and it's expected to recognize 98% of its $150B by the end of 2024. I find Lockheed one of the best positions to capitalize on the growing worldwide defense spending.

Regarding valuation, I showed that Lockheed seems to be trading at a premium compared to its competitors and its own historical average, however, I showed the discrepancy in consensus estimates and explained why short-term issues affect the comparability to past years. Additionally, I listed the FY24 budget as a major catalyst for investors, which turned out to be correct, as the budget increased despite many rumors about a cut. Thus, I estimated LMT's fair value at $551 per share and rated the stock a Strong Buy.

Now, let's focus on the company's results, see how my projections fared compared to the consensus, and provide an updated model. Spoiler alert: Due to the increase in stock price, I updated my Strong Buy rating to a Buy, but also slightly raised my price target to $553 per share.

Q1-23 Highlights

Lockheed Martin reported consolidated revenues of $15.1B, a 1.1% increase from the prior year. Based on its historical seasonality, the company is on pace to deliver flat revenue growth for the entire year. For the quarter, the company reported segment operating profit of $1.7B, reflecting an 11.1% margin.

Created by the author using data from Lockheed Martin's financial report

As we can see, growth was due to an increase in Space sales, which offset small declines in all the other segments. Aeronautics revenues decreased by 2.0%, Missiles & Fire Control ('MFC') decreased by 2.6%, Rotary & Mission Systems ('RMS') decreased by 1.1%, and Space grew by 15.6%.

Created by the author using data from Lockheed Martin's financial report

Looking at EBIT per segment, Aeronautics decreased by 0.6%, Missiles & Fire Control decreased by 2.1%, Rotary & Mission Systems decreased by 13.8%, and Space grew by 12.9%. Besides Space, every segment suffered from lower volumes.

Some other notable numbers - Deliveries were down significantly due to timing. Specifically in F-35, the company delivered only 5 jets in the quarter, compared to 26 in the previous year. The company's backlog is up 8.0% compared to Q1-22.

Overall, I find Lockheed Martin's results very impressive, as the company was able to beat analysts' expectations and saw an earlier-than-expected margin expansion.

Important Notes From The Call

Let's begin with an overview of F-35 deliveries and capacity. Deliveries resumed in February after a halt, which resulted in 19 fewer deliveries compared to the prior year. The company expects a fraction of total year deliveries to be impacted by software improvements and delayed hardware delivery time. It's important to note, there should be no material effect on the company's revenue compared to its guidance. However, it's a testament to the company's ongoing short-term issues, which are yet to be over.

Secondly, regarding labor issues and the company's supply chain, there was no significant change, and recovery is not projected before 2024. Specifically, the company experiences problems in RMS and MFC. However, management stated that the company is close to fully integrating its One Lockheed Martin initiative, which will enable the company to have a full view of demand and distribute components efficiently throughout its production lines. In my view, the fact that the supply chain is still a problem for Lockheed, but also for each of its competitors, supports the notion that this is a 2023 problem, but not much more than that. I don't think this will hurt the company over the long term, as Lockheed's offerings are not replaceable.

Lastly, I want to address some margin matters. MFC margins are expected to continue to be pressured by the unprofitable classified program, despite the higher-than-expected margin in Q1. This is going to weigh down on the segment's margins for the remainder of the year and for the next 4-5 years. Overall, management expects this segment to provide 13.5% margins for the mid-term, and the program's peak effect to occur in 2025. Despite the unprofitable program, the MFC segment is projected to grow profits during this period.

Investment Thesis - Long-Term, Growing, Unsatisfied Demand

Unlike some initial doubts from market participants, Lockheed's most significant customer, the U.S. government, has released its FY24 Department of Defense budget request, which totaled $842B, an increase of 3.0%. Lockheed's management stated the obvious -

Threats posed by China and Russia's invasion of Ukraine is driving the national defense strategy and has created added demand for Lockheed Martin's advanced solutions.

--- Jim Taiclet - Chairman, President and CEO, Q1-23 Earnings Call

Key highlights from the DoD budget include the procurement of 83 F-35 fighter jets, continued expansion of classified programs, and an increase in ammunition funding. Additionally, the request includes a multi-year commitment for Javelin and other product purchases.

Internationally, many ally governments have increased their defense budgets, and Lockheed is experiencing significant growth in that cohort. For example, Canada signed an agreement to buy 88 F-35 fighter jets. Management expects high single-digit growth internationally, which will support overall growth beginning in 2024.

The next 5 years or so, we expect international to be a significant contributor to our growth. When you strip out international, you're talking about high single digits growth there. It's FMS related as well as the F35 program. [For example] the Australian Military satellite communication program. That's a multibillion dollar opportunity and have really expanded the international footprint of our space business, which has historically been predominantly a domestic U.S. based business. So these opportunities continue to present themselves. There's a lot more opportunity in front of us and that is absolutely a growth driver for us over the next five years.

--- Jay Malave, Chief Financial Officer, Q1-23 Earnings Call

And like the domestic demand, international demand is broad-based across all segments, and will support the long-term growth of the company:

On the Aero side, you know the F-35 has been incredibly popular. I think that won every competition meaningful competition over the last few years as far as generation fighter aircraft go. In addition to that, the F-16, we can't build them fast enough, and additional orders are coming in. We're going to compete in India to try to get that order as well and it's a matter of us being able to get to the production rate that the international is demanding. RMS is having a lot of success with the Seahawk helicopter for Example and various versions of the Blackhawk. As we mentioned Australia, we’re there. Also, the radar systems are becoming more exportable as we go forward and both in Europe and Asia, there's demand for those and then at MFC obviously. So, there is a wide and broad range across all of our business areas of significant international demand. It's going to last for many years.

--- Jim Taiclet - Chairman, President and CEO, Q1-23 Earnings Call

As I wrote in my first article, I believe Lockheed Martin should be a cornerstone of every dividend investor's portfolio, and this section is my investment thesis in a nutshell. Lockheed's business has always been viewed as steady, specifically due to the demand side. Under the current geopolitical environment, demand has become more than steady. Disregarding politics, Lockheed's next couple of years should be a great growth period for the company, supported by domestic and international demand, which Lockheed will be ready to fulfill with its increased capacities and production-line improvements.

Updated Financial Model

In the March article, I provided my near-term projections for Lockheed Martin:

My near-term annual projections are very similar to the detailed guidance the company provided. For Q1-23, I expect revenues of $15.2B, and net income of $1.6B, which is slightly above the consensus of $15.0B and $1.5B, respectively. After the April earnings release, we will see who came closer and I will update my model accordingly.

Based on the Q1 results, I reiterate my FY23 assumptions, which are similar to the company's reaffirmed guidance. I now expect revenues of $66B, EBIT of $8.45B, and a net income of $6.9B. For Q2-23, I project revenues of $16.2B and a net income of $1.7B, higher than the consensus of $15.9B in sales and a net income of $1.6B.

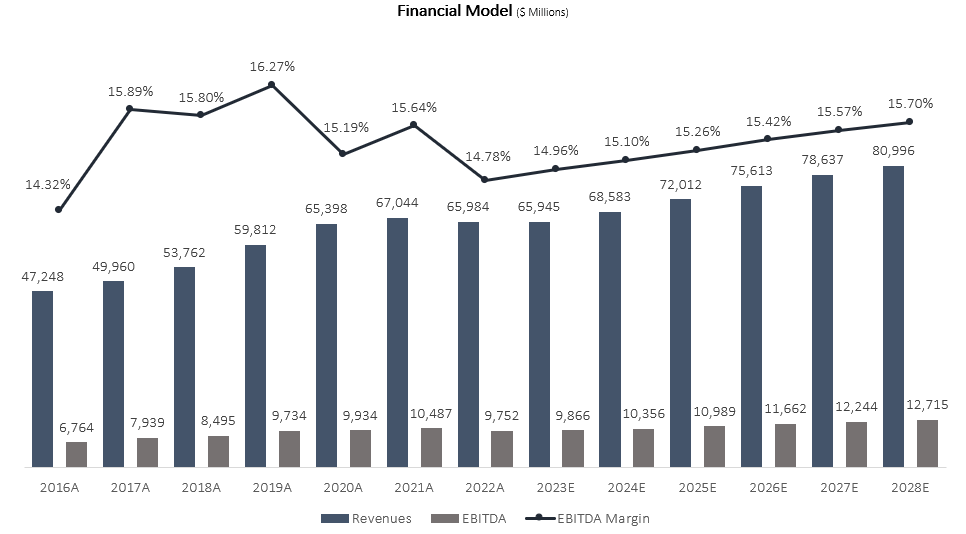

As a consequence of the quarterly adjustment, I need to update my long-term model as well. I now forecast LMT will grow revenues at a 3.5% CAGR between 2022-2028, which is higher than the consensus of approximately 3% growth, but below the company's past 7-year CAGR of 5.7%. I estimate revenues will grow at this pace due to backlog fulfillment, capacity enhancements, and the company's ability to capitalize on the increasing defense budgets all over the world.

I project EBITDA margins will increase incrementally up to 15.7% in 2028, due to higher growth in the higher margin segments, as the supply chain recovers and major programs finish their ramp-up stage. This is not outside of the company's reach, as we already saw higher margins in the past.

Overall, my assumptions result in EBITDA growth in excess of revenues. Which is according to the management's guidance for margin expansions and recovery in the mid-term.

Created and calculated by the author using data from LMT's financial reports and the author's projections

{kind=link}

Taking a WACC of 8.3%, I estimate LMT's fair value at $140.8B or $553 per share, which represents a 9.3% upside compared to its market value at the time of writing this article. My valuation represents a 20.2 P/E multiple on 2023 earnings, which is the company's average P/E multiple in the past 5 years.

Conclusion

In my view, Lockheed Martin should be a cornerstone in every long-term dividend investor's portfolio. The company operates in a recession-proof industry, with the richest governments in the world as its customers. Within the industry, LMT proved its ability to outperform its peers through extraordinary products like the F-35, and incomparable shareholder returns through dividends and buybacks. While the company is experiencing short-term headwinds, margins are recovering faster than expected, and the future is bright with the company's production capacity expected to increase significantly in order to meet the growing outsized demand.

To conclude, I estimate LMT's fair value at $553 per share and rate the stock a Buy.

For further details see:

Lockheed Martin: Q1 2023 Signals Easing Short-Term Issues, Long-Term Upside