LMT - Lockheed Martin: Q2 2023 Tells A Bad Margin Story (Rating Downgrade)

2023-07-18 21:43:34 ET

Summary

- Lockheed Martin just published its Q2-23 results, beating even my above-consensus expectations. Revenue grew by 8.1%, and EPS totaled $6.65.

- Lockheed has raised its full-year guidance to reflect better-than-expected recovery, and now expects sales growth already in 2023.

- Demonstrated by the record $158B backlog, the demand for Lockheed's products and services is as strong as ever.

- However, management has provided a very poor outlook regarding the company's ability to improve margins in the future.

- Margin expansion played a crucial part in my investment thesis, and without it in the near future, I have to downgrade the stock to a Hold, despite the revenue story.

Lockheed Martin ( LMT ) just announced its Q2-23 results, reporting 8.1% revenue growth and $6.65 EPS, both beating expectations. The company is showing continued progress in recovery from its supply chain issues, as revenues return to growth faster than expected. Lockheed's capacity enhancements are progressing across each of its major programs, setting the stage to capitalize on the increasing defense budgets worldwide, demonstrated by a record $158B backlog. However, the margin story is problematic.

I downgrade the stock to a Hold and update my price target to $504 per share.

Background

I began covering Lockheed Martin in a March article , claiming the company's temporary headwinds provide a buying opportunity. I urge you to read that article, in which I explained my investment thesis in detail and why I expected above-consensus profitability and growth in 2023 and beyond, as well as described the company's operating segments, risks, and Lockheed's major tailwinds and headwinds. Then, I last covered it in April.

In short, my investment thesis regarding the company is based on Lockheed's timely capacity enhancements (specifically in its F-35 program) as defense budgets all over the world are on the rise. Unlike many other defense contractors, Lockheed has a history of fulfilling its immense backlog, and it's expected to recognize 98% of its $158B contracts by the end of 2024. Thus, I find Lockheed as one of the best positions to capitalize on the growing worldwide defense spending.

Now, let's focus on the company's results, see how my projections fared compared to the consensus, and provide an updated model.

Q2-23 Highlights

Lockheed Martin Q2-23 Presentation

{kind=link}

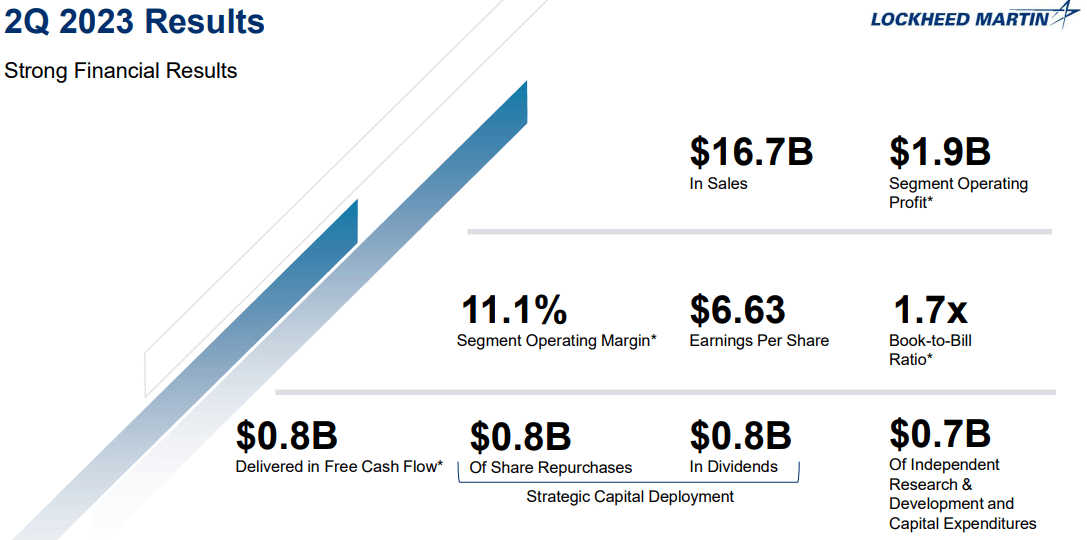

Lockheed Martin reported consolidated revenues of $16.7B, an 8.1% increase from the prior year. Based on its historical seasonality, the company is on pace to deliver 1.3% growth for the entire year. For the quarter, the company reported segment operating profit of $1.9B, reflecting an 11.1% margin.

Created by the author based on data from Lockheed Martin financial reports; MFC = Missles & Fire Control; RMS = Rotary & Mission Systems.

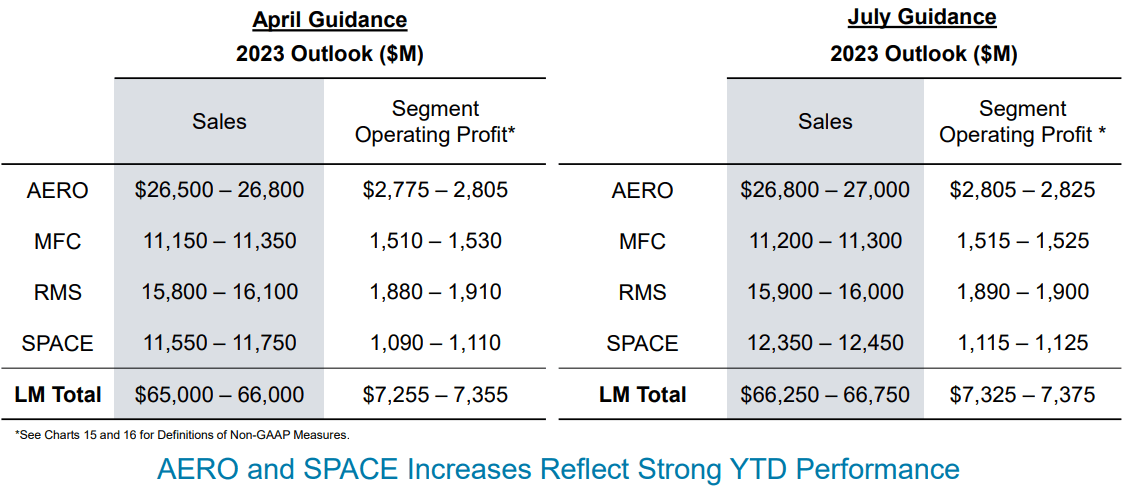

Growth was fueled by a 17.3% increase in Aeronautics, primarily due to higher volumes on production contracts in the F-35 program, and a 12.0% rise in Space sales, due to higher volumes as well. Growth was slightly offset by a flat MFC and a 2.9% decline in RMS, which was dragged by lower production volume in the Sikorsky helicopter programs.

Created by the author based on data from Lockheed Martin financial reports; MFC = Missles & Fire Control; RMS = Rotary & Mission Systems.

Looking at EBIT per segment, Aeronautics increased by 17.2%, due to revenue growth and steady margins. Missiles & Fire Control decreased by 11.2%, due to lower net favorable profit adjustments which resulted in a two percentage point margin contraction. Rotary & Mission Systems decreased by 1.5%, as revenue declines were slightly offset by better margins. Lastly, Space grew by 15.0%, due to revenue growth and a small margin improvement which resulted from favorable adjustments and higher equity earnings.

Other Notable Numbers

F-35 deliveries were up significantly due to timing and reached 45 jets in the quarter. Other Aeronautics deliveries all declined compared to the prior year period. The company's backlog reached $158B, reflecting a $13B (8.9%) increase quarter-over-quarter.

Overall, I find Lockheed Martin's results very impressive, as the company was able to beat analysts' expectations in both revenue and EPS. However, enthusiasm was restrained by lower margins compared to the prior quarter, reflecting the company's supply chain problems still existent. Furthermore, operating cash flows declined YoY, although it was primarily due to the timing of federal tax payments, which should have the opposite impact in the upcoming quarters.

Updated Guidance

Lockheed Martin Q2-23 Presentation

{kind=link}

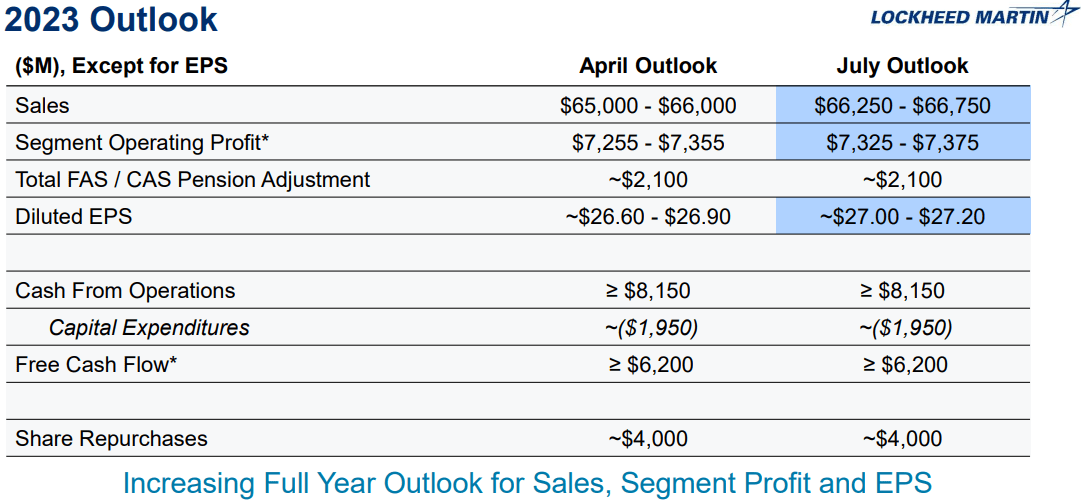

Lockheed's management increased its full-year guidance for sales, segment operating profit, and EPS, supporting my initial projection for faster-than-expected recovery. However, similar to the quarterly results, it's not yet the time to celebrate a perfect victory.

Lockheed Martin Q2-23 Presentation

{kind=link}

As we can see, while the mid-point of the sales guidance was upgraded by 1.5%, the mid-point of the segment operating profit barely changed, reflecting worse-than-expected margins. Consequentially, we understand that the majority of the upgrade is the result of non-operational items and better sales performance, but the margin improvement is not here just yet.

Lockheed Martin Q2-23 Presentation

{kind=link}

Important Notes From The Call

We are confident in our ability to achieve these higher expectations and return to growth sooner than previously anticipated.

--- Jim Taiclet - Chairman, President and CEO, Q2-23 Earnings Call

Clearly, the company did not expect to deliver 8.1% growth in the quarter. While the guidance suggests a relatively flat year, the growth numbers in the second quarter do provide more certainty in the company's ability to return to growth.

Our current view is we expect to deliver 100 to 120 F-35 aircraft in 2023. Importantly, there is no change to our longer-term delivery outlook of 156 aircraft in 2025 in the foreseeable future.

--- Jim Taiclet - Chairman, President and CEO, Q2-23 Earnings Call

No surprise here, management has reiterated its 2025 targets and provided some more clarity on the number of aircraft underneath its Aeronautics guidance for the year. The F-35 backlog amounted to 421 aircraft at the end of the quarter, providing confidence in the need for the company's investments in increased capacity.

So If Everything Is So Great, Why Is The Stock Dropping?

Clearly with the backlog, it's not a question of demand, it'll be a question of supply and we need to go through that analysis over the next few months and determine to what extent our growth outlook will change if anything from this from this baseline.

--- Jim Taiclet - Chairman, President and CEO, Q2-23 Earnings Call

First of all, management was extremely cautious with revising their long-term guidance upwards. They still expect low-single-digit growth from 2024 and beyond.

[ regarding the transition to multi-year contracts ] As we enter into agreements that will cover multi years, we will also get into contracts with suppliers for those same multi years. So any benefits that we get from that probably is going to drop to our customer. So I wouldn't expect there to be any type of margin upside from where we are today.

--- Jim Taiclet - Chairman, President and CEO, Q2-23 Earnings Call

Secondly, as previously discussed, the sudden war in Ukraine has induced a need that the industry hasn't dealt with many times before, which is a sudden surge of demand. This has caught the supply chain, which was already struggling, in a rough spot. This has resulted in a major change for the industry, which is going to transition to multi-year contracts, in order to provide more clarity for suppliers and defense contractors like Lockheed.

The problem is many investors, including me, were expecting Lockheed to benefit (at least a little) in terms of margins. And management is clearly saying no, it's not going to happen.

[ regarding the 1LMX program ] It's intended to make or make us more competitive company. Many of those benefits that we are going to obtain, we will pass those through in pricing rates to our customer. And so we won't necessarily see more our margin benefit from it, but become more competitive to capture more business and stay in front of the industry and maintain our leadership.

--- Jim Taiclet - Chairman, President and CEO, Q2-23 Earnings Call

The 1LMX program is a digital transformation project across all of Lockheed's business units, which aims to make the company more agile and efficient. Yet again, another initiative that I expected to drive at least some margin upside, we find out that management has different plans.

Updated Financial Model

In my April article , I provided my near-term projections for the company:

For Q2-23, I project revenues of $16.2B and a net income of $1.7B, higher than the consensus of $15.9B in sales and a net income of $1.6B.

Based on the Q2 results, I reiterate my FY23 assumptions, which are marginally better than the company's guidance. I now expect revenues of $66.8B, EBIT of $8.6B, and Net Income of $7.0B. For Q3-23, I project revenues of $16.7B and Net Income of $1.7B.

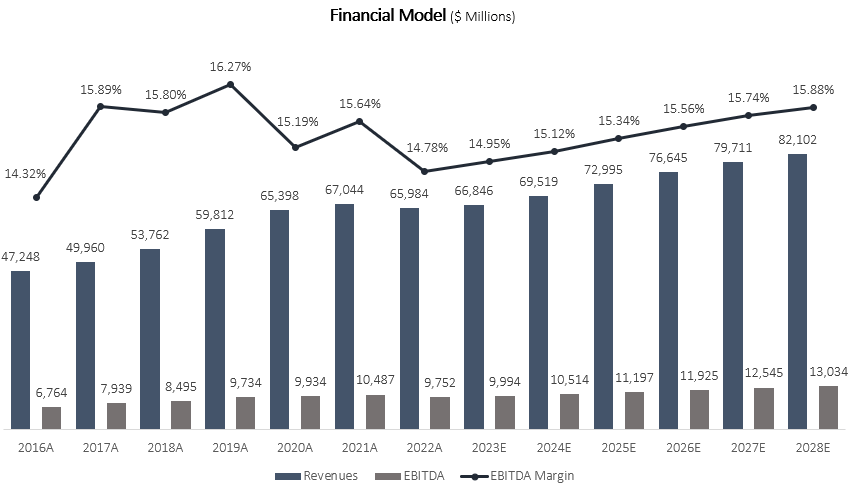

As a consequence of the quarterly adjustment, I need to update my long-term model as well. I now forecast LMT will grow revenues at a 3.7% CAGR between 2022-2028, which is higher than the consensus of approximately 3.0% growth, but below the company's past 7-year CAGR of 5.7%. I estimate revenues will grow at this pace due to backlog fulfillment, capacity enhancements, and the company's ability to capitalize on the increasing defense budgets all over the world.

I project EBITDA margins will increase gradually up to 15.9% in 2028, as the supply chain recovers and losing contracts end. This is not outside of the company's reach, as we already saw similar margins in the past.

Overall, my assumptions result in EBITDA growth in excess of revenues. Which is according to the management's guidance for margin expansions and recovery in the mid-term.

Created and calculated by the author based on data from Lockheed Martin financial reports and the author's projections.

{kind=link}

Taking a WACC of 8.4%, I estimate LMT's fair value at $127.8B or $504 per share.

Conclusion

In my view, Lockheed Martin should be a cornerstone in every long-term dividend investor's portfolio. The company operates in a recession-proof industry, with the richest governments in the world as its customers. Within the industry, LMT proved its ability to outperform its peers through extraordinary products like the F-35, and incomparable shareholder returns through dividends and buybacks. While the company is experiencing short-term headwinds, recovery is progressing better than expected, and the future is bright with the company's production capacity expected to increase significantly in order to meet the growing outsized demand.

However, it's clear that the company's margins are going to stay deflated for a long time, and its ability to return to historical highs is doubtful. With a company like Lockheed, it's important to remember its upside will always be limited by the cost+ contracts it operates under, something that I missed in my previous articles.

I was certain that the company's digital transformation and the industry's transition to a more agile supply chain should translate to a margin expansion. Well, according to the management, this is not the case. While I do appreciate its goals of being "more competitive", I believe Lockheed is already one of the strongest players in the industry, and I expected it to result in a margin expansion, along with better revenue growth.

For those reasons, I downgrade the stock to a Hold.

For further details see:

Lockheed Martin: Q2 2023 Tells A Bad Margin Story (Rating Downgrade)