RTX - Lockheed Martin Q3 Earnings Preview: A Tricky Situation

2023-10-11 11:21:09 ET

Summary

- In this article, I will weigh in on whether the recent sell-off in Lockheed Martin stock and its recent rebound were justified.

- I examine whether the outlook for LMT stock has changed in the current environment, focusing on growing geopolitical tensions, high government debt, and the persistent high interest rate environment.

- I share my thoughts on the recent - rather paltry - dividend increase, my expectations for the future, and why I avoid watching Lockheed's performance on a per-share basis.

- I explain why LMT stock could fall in response to the upcoming earnings report - even though the company is expected to report solid numbers.

Introduction

Lockheed Martin Corp. ( LMT ) stock has drawn increasing attention from investors recently for two reasons - first, the fairly rapid sell-off from over $450 to under $400 in a little over a month, and more recently, the Hamas attack on Israel that began over the weekend in reaction to which LMT stock rebounded to $435. As a major defense contractor, a rise in the stock price seems a logical consequence of an escalated conflict. Recall Russia's invasion of Ukraine in February 2022, which saw a similar pattern. However, as a long-term investor, it is important to take a closer look at whether Lockheed's prospects have actually changed for the better as a result of this latest tragic - but hopefully short-lived - event.

I first covered the company in a detailed report in October 2021 and in comparative analyses with RTX Corp. ( RTX ) in October 2022 and Huntington Ingalls Industries, Inc. ( HII ) in January 2023 . With the company set to report its third-quarter results next Tuesday, October 17, it's a good time to reassess. In this update, I will:

- discuss whether the recent sell-off and subsequent rise in the share price were justified,

- explain whether the outlook for LMT stock has changed in the current environment,

- share my thoughts on the recent - admittedly quite meager - dividend increase,

- and take a look at Lockheed's earnings performance to date and the potential for an earnings beat on Tuesday.

So, let's dive right in…

Why LMT Stock Has Been Rather Volatile Lately

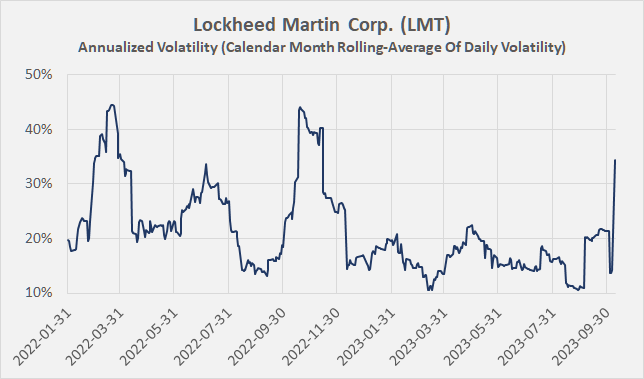

Figure 1 shows the volatility of LMT stock since the beginning of 2022 - Russia's invasion of Ukraine and peak pessimism during the 2022 bear market are clearly visible. The recent spike on October 9 due to the Hamas attack on Israel is also clear, but also look at the increase since early September. There are several reasons for the recent rise in volatility.

Figure 1: Lockheed Martin Corp. (LMT): Annualized volatility, based on calendar month rolling-average of the daily volatility (own work, based on the daily close of LMT stock price)

{kind=link}

The U.S. Defense Budget, Debt, And The Risk Of A Shutdown

As I explained in my first article on the company, I own this defense pure play as a non-cyclical, or even counter-cyclical investment that gives me exposure to the industrial sector. However, it should be kept in mind that the performance of defense contractors correlates with current government defense spending and its expected growth. With a national debt well over $33 trillion , austerity measures should not be ruled out in theory, but of course, with the ongoing conflict in Ukraine, recent events in Israel, and political tensions between China and Taiwan, it is unrealistic to expect defense spending to remain flat or even decline in the future. The fiscal 2024 budget request of $842 billion for the Department of Defense is 3.2% and 13.5% higher than the fiscal 2023 and fiscal 2022 requests, respectively. However, I do not expect defense spending to grow in the high single digits or even low double digits in the future. Instead, given the mid-single digit growth in defense spending between 2017 and 2021 (5.5% average annual growth rate), I believe continued moderate growth is the most likely outcome in this environment.

In addition to the (in my view unfounded) fears of a cap on defense spending amid all-time high national debt, it was the news of a possible U.S. government shutdown that made investors nervous. After all, payments to defense contractors could be delayed and new contracts could be postponed or not awarded at all. While this is a risk to consider before investing in the defense sector, I maintain that a government shutdown will eventually resolve itself. Therefore, I consider these occasional events to be more or less irrelevant to defense stock valuations, but of course such news does lead to increased stock volatility.

The "Hot War" Tailwind

Given the war in Ukraine and the recent attacks on Israel, it seems only logical that Lockheed would be one of the immediate beneficiaries - so it's understandable that LMT stock jumped in response to the headlines, at least in theory.

Granted, Lockheed is very well positioned with its F-35 fighter jet franchise (reliable cash flows for decades) and the close combat, precision fires and strike systems it offers through its Missiles and Fire Control segment. However, given the company's significant reliance on long-term procured projects, an immediate jump in sales and profits is an unrealistic expectation. In this context, the positive reaction to RTX stock is much more understandable given the ten Iron Dome batteries installed in Israel.

That said, I believe LMT will benefit in the long run. The 2022 invasion of Ukraine exposed the inadequate defense capabilities of several European countries, and the company subsequently saw significant orders for F-35s (e.g., 35 for Germany , 36 for Switzerland ). In my view, the reality, revealed once again, of how quickly hot wars can emerge is a stark reminder to governments around the world to maintain an adequate defense infrastructure - despite the need for austerity measures in the face of record levels of national debt.

The Potential Impacts Of A "Higher For Longer" Interest Rate Environment

However, I think there is more to consider than government debt and a possible shutdown. In my view, it was the flattening of the yield curve that contributed to the sell-off. Long-term government bond yields have been gradually rising rather quickly since early September, and the 20-Year Treasury, for example, even exceeded a yield of 5.1% in early October. With short-term yields similarly high, the market is (finally?) pricing in a "higher for longer" interest rate scenario. As a result, companies with a high level of debt and relatively short weighted-average maturity will increasingly have to refinance their maturing bonds at comparatively unfavorable interest rates, which puts pressure on earnings and cash flows.

Lockheed, historically relied (and to some extent still relies) on conventional benefit plans. The company is known for having a comparatively high proportion of unfunded pension liabilities. However, as I explained in this article , Lockheed has done a good job of reducing its risk by purchasing group annuity contracts from time to time. While this is encouraging, in the process the company has taken on debt that will be more expensive to service if the current environment persists for a number of years.

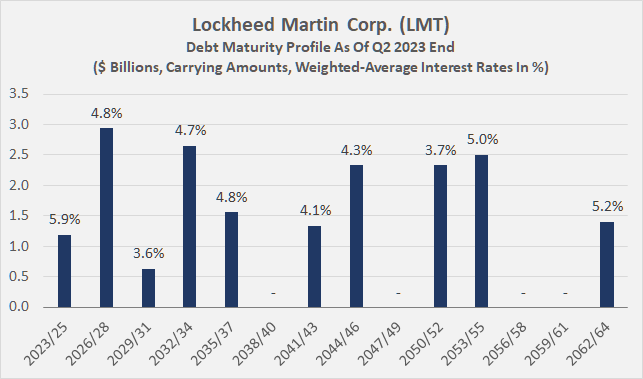

Let's look at Lockheed's current debt maturity profile to get a good understanding of how a long-term high interest rate environment could affect the company (Figure 2). As an aside, the maturity profile is based on information published in the 2022 10-K (p. 86), but includes recently assumed debt (see this May 2023 8-K filing ).

Figure 2: Lockheed Martin Corp. (LMT): Debt maturity profile, including recently assumed debt; in some instances, interest rates had to be estimated (own work, based on company filings)

{kind=link}

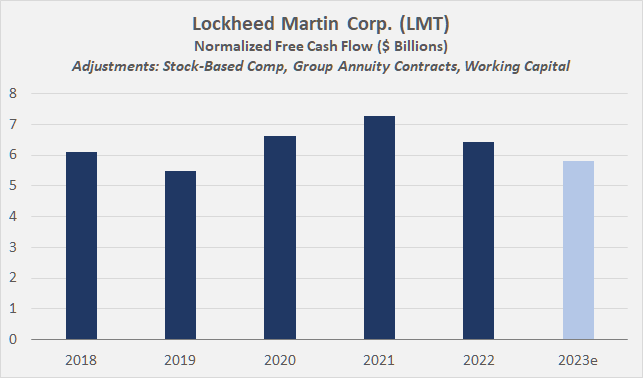

At the end of the second quarter of 2023, Lockheed's net debt was $13.9 billion, largely due to its sizable cash position of nearly $4 billion, but still up 40% year-over-year. However, the maturity profile remains balanced and manageable, given the company's annual free cash flow of about $6 billion to $7 billion (Figure 3).

Figure 3: Lockheed Martin Corp. (LMT): Historical and 2023 estimated free cash flow, with adjustments for stock-based compensation, purchased group annuity contracts and working capital (own work, based on company filings and own estimates)

{kind=link}

The weighted-average interest rate of about 4.4% is quite good and translates to an interest coverage ratio of about 9 times free cash flow before interest. However, investors should keep in mind that Lockheed's weighted-average interest rate was about 50 basis points lower a year ago. High interest rates are taking their toll, and considering that LMT will most likely not repay most of its debt but roll it over it as it matures, debt service costs will likely continue to increase.

Judging by the current yield on its long-term bonds , LMT will likely refinance at a coupon rate of 5.8% to 6.0% if the current interest rate environment continues for a few years. But even if we assume Lockheed refinances all of its bonds maturing through 2026 at 6%, its interest coverage ratio remains well above 8 times free cash flow before interest (even assuming no free cash flow growth). The robustness of Lockheed's balance sheet is also underscored by its weighted-average maturity of about 19 years and its long-term credit rating of A2 , which was recently upgraded from A3.

The company clearly has the financial capacity to continue its current capital allocation program (see subsequent section) and does not need to prioritize debt repayment. However, this arguably positive conclusion raises the question of why Lockheed's recent dividend increase was comparatively meager.

What To Make Of Lockheed's Comparatively Small Dividend Hike?

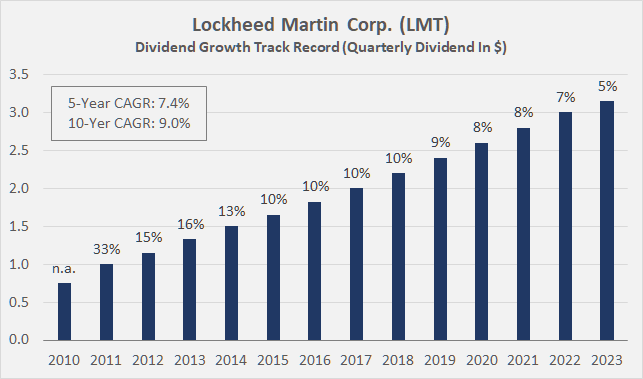

On October 7, Lockheed declared a quarterly dividend of $3.15 per share, a 5% increase. This is significantly less than the five- and 10-year compound annual growth rates of 7.4% and 9.0%, respectively (Figure 4). Considering that LMT's dividend yield is currently 2.9% and assuming that the company continues to increase its dividend by 5% per year, investors would have to wait until 2034 before their yield on cost exceeds the current rate on the 20-Year Treasury. Investing in long-term government bonds once again has become a rather tempting alternative for risk-averse investors who desire well-predictable cash flows - another reason for the recent weakness in dividend stocks.

Figure 4: Lockheed Martin Corp. (LMT): Quarterly dividends since 2010 (own work, based on company filings)

{kind=link}

Conversely, the yield on cost of LMT stock will eventually exceed the risk-free rate, and that is an important aspect of why I invest in dividend-paying companies with good growth potential. I want my income to at least keep pace with inflation, so I aim for a weighted-average dividend growth rate of at least 5% in my portfolio. Those who invest in long-term bonds are accepting that the purchasing power of their cash flows will decline over time due to inflation ( see this article ).

From this point of view, it is of utmost importance to keep an eye on a company's dividend growth potential. If Lockheed continues to grow its dividend at an increasingly slower pace, that would certainly be an issue. The trend (current growth < 5-year CAGR < 10-year CAGR) points in that direction. However, I would not over-interpret this trend and think LMT can return to somewhat higher dividend growth in the future.

For one, LMT typically pays out less than 50% of its normalized free cash flow. Granted, free cash flow growth has been non-existent in recent years, but that is largely due to working capital effects and higher capital expenditures. While capacity expansions are time-consuming and expensive - and thus a drag on short-term free cash flow - they should be recognized positively due to the improved long-term growth outlook. In addition, supply chain issues took their toll, leading to an increase in unfilled orders and thus shifting cash flow to future years. As these issues are gradually resolved, free cash flow growth is expected to return to the long-term average growth in the high single digits.

Another aspect worth noting is Lockheed's recent increased emphasis on share repurchases.

Lockheed repurchased 18.3 million shares in 2022 for nearly $8 billion (p. 95, 2022 10-K). So far in 2023, $1.25 billion worth of shares have been repurchased. However, along with the dividend increase, the company announced a $6 billion increase in its existing repurchase authorization, bringing the total amount of future repurchases to a whopping $13 billion - or nearly 12% of LMT's current market capitalization. Conservatively assuming a net impact of only 10% (consider dilution due to stock-based compensation), the positive impact on Lockheed's dividend payout ratio is still pretty significant and will improve long-term dividend growth potential.

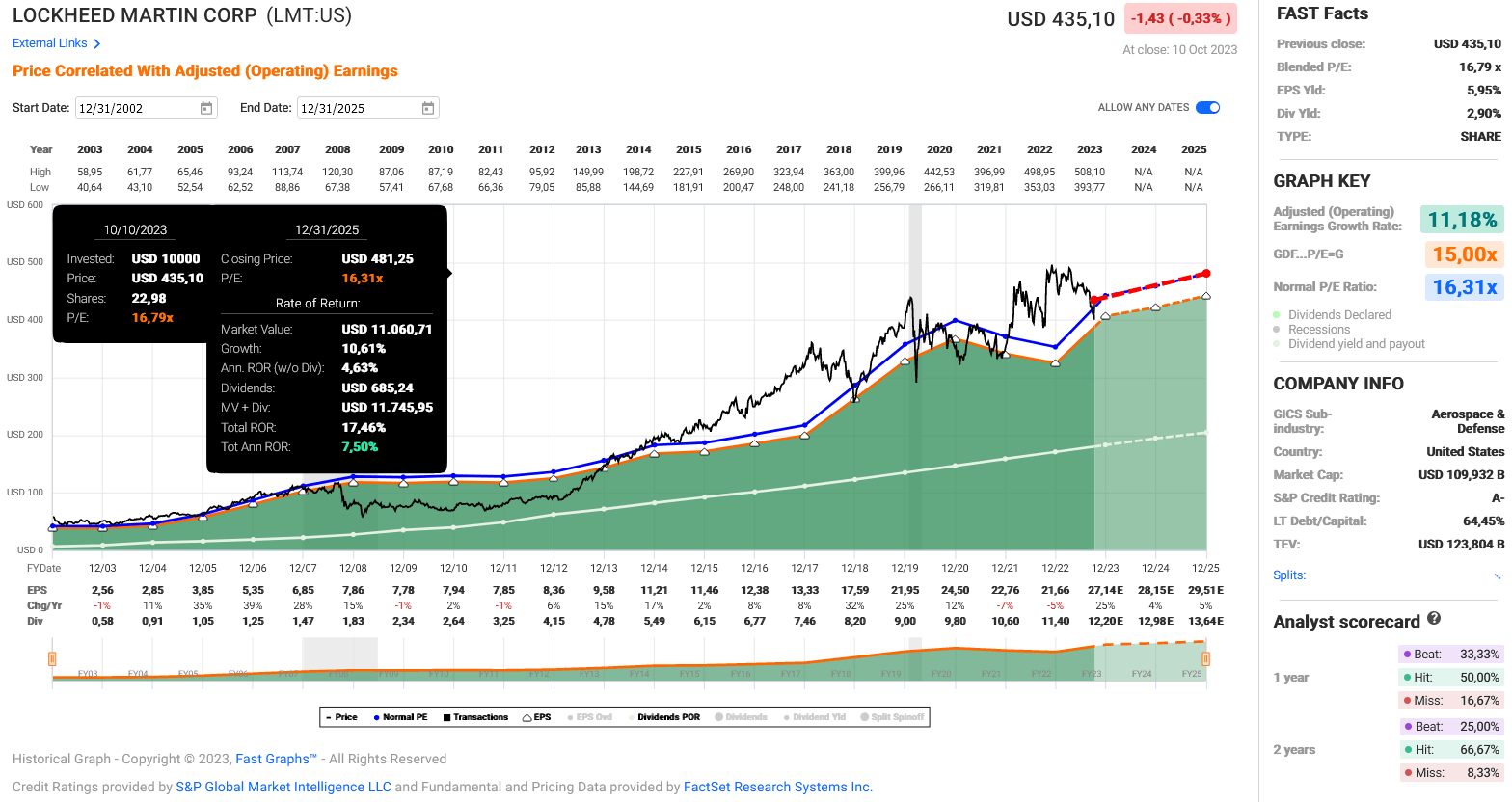

Of course, investors should keep in mind that LMT will finance a significant portion of its buybacks with debt. Given the cost of long-term debt of around 6%, the buybacks arguably come at a significant price. However, given LMT's stock is at least fairly valued, if not slightly undervalued (6% free cash flow yield, PEG ratio of 1.5, blended P/E of 16.8, Figure 5), I think the buybacks represent a good return on investment.

However, investors should keep in mind that buybacks are accretive to earnings per share and, of course, are only sustainable if a company is ultimately able to repay its debt and the underlying business fundamentals are sound. I believe LMT's long-term prospects are solid and the company is well managed, as I explained in my previous post, so I think it is a stretch to conclude that LMT's management feels the need to manage earnings per share through buybacks. However, considering that LMT has retired nearly 20% of share count over the past decade, representing earnings growth averaging 2.4% per year (or 25% of total annual earnings growth over that period), I continue to monitor Lockheed's performance on a company level, not on a per share basis.

Figure 5: Lockheed Martin Corp. (LMT): FAST Graphs chart based on adjusted operating earnings per share (FAST Graphs)

{kind=link}

Did Lockheed Martin Beat Earnings Before And What To Expect From Lockheed Martin's Q3 Earnings?

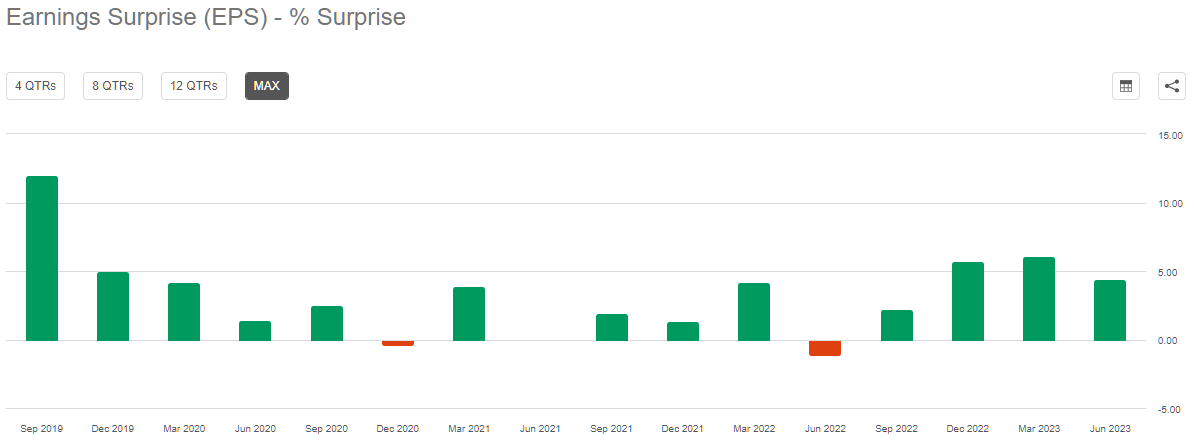

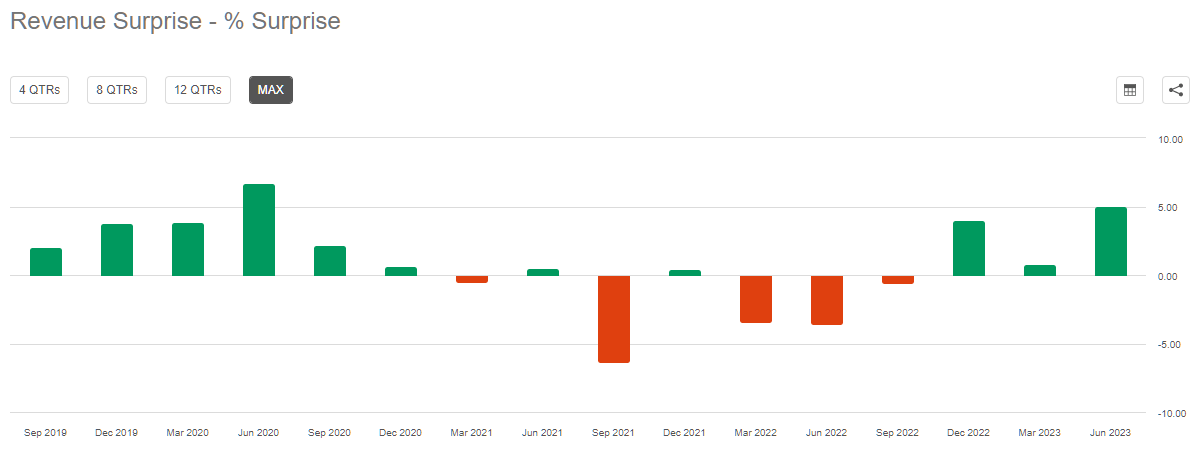

Lockheed Martin beat analysis estimates for earnings per share in 13 of 16 quarters (Figure 6) and for revenue in 11 of 16 quarters (Figure 7). At first glance, this suggests potential earnings management, but given that Lockheed missed revenue estimates in a period that was (and to some extent still is) characterized by supply chain disruptions, I would not over-interpret this discrepancy.

Figure 6: Lockheed Martin Corp. (LMT): Earnings per share surprises on a quarterly basis (Seeking Alpha) Figure 7: Lockheed Martin Corp. (LMT): Revenue surprises on a quarterly basis (Seeking Alpha)

{kind=link}

{kind=link}

Revenues and earnings per share revisions in recent months have been insignificant for both upcoming quarters and longer-term results , suggesting analyst confidence. Based on these data and the recently improved net sales, operating profit and adjusted earnings per share guidance (p. 4, Q2 2023 earnings press release ), an earnings beat on Tuesday seems quite likely. At the same time, the company's tendency to beat earnings estimates is likely baked into investors' expectations.

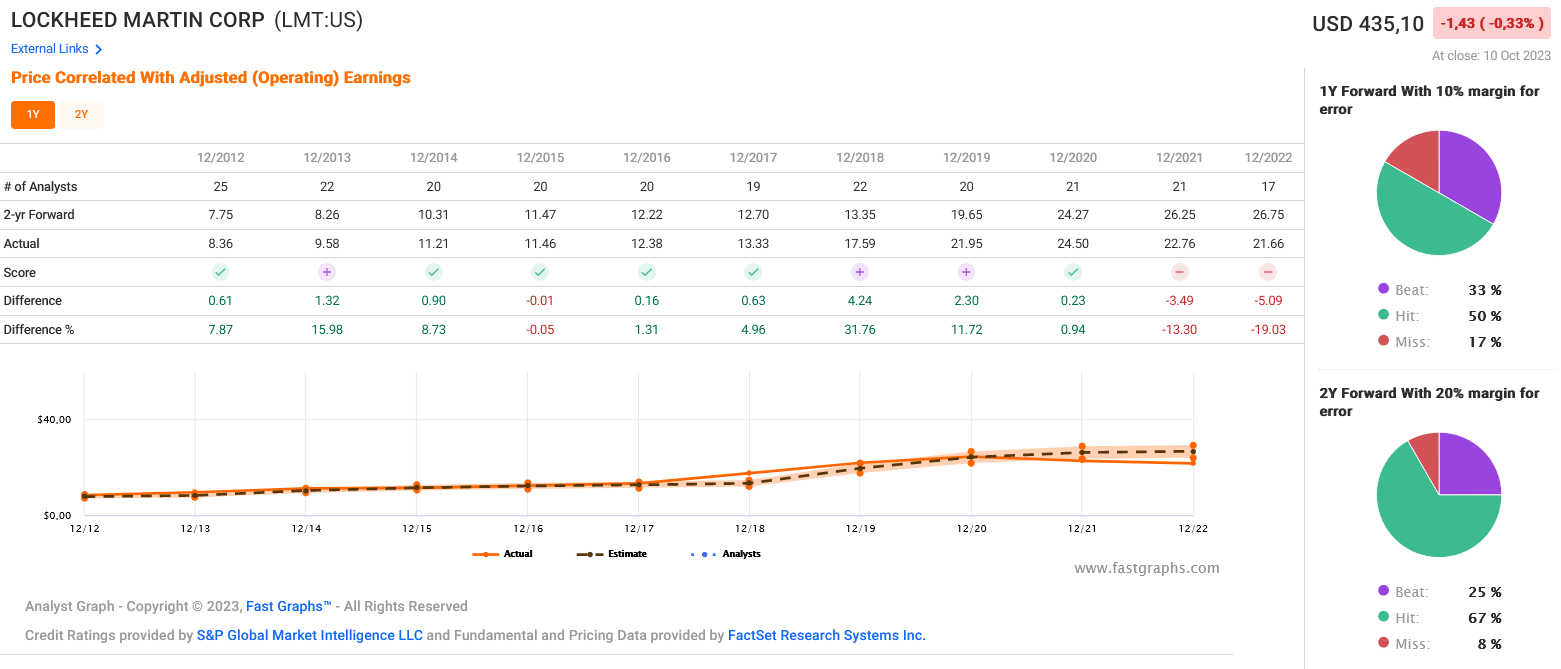

Excluding the negative impact of the pandemic's secondary effects (see analyst scorecard in Figure 8), the longer-term accuracy of analysts' forecasts is also quite solid, underscoring Lockheed's low cyclicality (earnings of conventional industrial companies are, by their nature, very difficult to predict).

Figure 8: Lockheed Martin Corp. (LMT): Analyst scorecard on a one-year forward basis (FAST Graphs)

{kind=link}

As I mentioned earlier, I do not expect recent developments to have an immediate positive impact on Lockheed Martin. However, I do think that the company's long-term outlook has improved, largely due to the change in stance on defense spending in Europe against the backdrop of the war in Ukraine, but also due to recent developments in Israel. Given the immediate and quite significant jump in LMT's stock price following the attacks on Israel over the weekend, I suspect that LMT stock could actually fall in reaction to the earnings report on Tuesday if management does not address potential positives for the company. That doesn't seem unrealistic, considering that there will most likely simply be nothing significant to say. I doubt, for example, that Lockheed's backlog has changed in that short period of time, given how slow defense procurement is.

Conclusion

After a disappointing September - Lockheed Martin stock fell by more than 10% - the overall defense sector regained interest among investors due to Hamas' attack on Israel.

The September decline was due to several factors.

First, stocks of U.S. defense companies tend not to be truly cyclical in the traditional sense, but they are sensitive to news related to government debt and defense spending. However, I think it is important to look beyond these near-term uncertainties (including those related to a government shutdown). I am confident that the U.S. will not cut back on defense spending, especially in light of growing geopolitical tensions. Moreover, the war in Ukraine and the latest developments in Israel are stark reminders of the importance of maintaining an adequate defense infrastructure - despite the need for austerity measures in the face of historically-high national debt. This applies not only to the U.S., of course, but also to Europe in particular.

Secondly, as investors increasingly anticipate a "higher for longer" interest rates scenario, companies with high levels of debt on their balance sheets are coming under increased scrutiny. However, Lockheed's debt is very manageable - despite a 40% year-over-year increase in net debt. With relatively evenly distributed maturities and a weighted-average maturity of 19 years, the maturity profile of Lockheed Martin's debt is very reassuring. The weighted-average interest rate is up about 50 basis points year-over-year, but is still quite low at about 4.4%. I expect the current very solid debt service capacity of about nine times pre-interest free cash flow to remain robust, even as the company rolls over its maturing debt and probably raises even more debt as it is currently conducting significant share repurchases.

The recent dividend increase of only 5% was a bit disappointing given the company's historical track record and the current high risk-free rate. However, I think investors should focus on the long term, and LMT is very well positioned in this regard from an operational perspective. Moreover, the share buybacks - which I think represent a good return on investment - will lower Lockheed's dividend payout ratio and as a result improve its long-term dividend growth prospects. However, considering that about 25% of Lockheed's earnings per share growth over the past decade has been due to share buybacks, I think it is critical to continue to monitor the company's performance on a company basis rather than on a per-share basis.

Lockheed will report its third quarter results on Tuesday, Oct. 17, and given its solid track record, it is likely to beat earnings and probably also revenue estimates. However, this is likely already factored into investor expectations. In my view, investors are looking for signs to confirm the sharp rise in the share price following the recent attacks. Therefore, I can imagine the stock falling in response to the (likely solid) third quarter results if management does not address potential positives for the company. That doesn't seem unrealistic, considering that there will most likely simply be nothing significant to say. I doubt, for example, that Lockheed's backlog has changed in that short period of time, given how slow defense procurement is.

Therefore, I do not intend to add to my LMT position ahead of the results, even though it is still quite small and the stock is fairly valued, if not slightly undervalued. Suffice it to say that I can imagine adding to my position if the stock falls in response to management's comments on Tuesday.

Thank you for taking the time to read my latest article. Whether you agree or disagree with my conclusions, I always welcome your opinion and feedback in the comments below. And if there's anything I should improve or expand on in future articles, drop me a line as well. As always, please consider this article only as a first step in your own due diligence.

For further details see:

Lockheed Martin Q3 Earnings Preview: A Tricky Situation