LMT - Lockheed Martin: Q3 Is More Of The Same No Market-Beating Returns Here

2023-10-18 12:28:40 ET

Summary

- Lockheed Martin announced Q3-23 results that exceeded subdued expectations, reporting 1.8% revenue growth and $6.75 EPS.

- With geopolitical tensions increasing worldwide, demand for Lockheed products is as strong as ever.

- However, the company is unable to capture the value of these demand spikes, amid supply chain constraints and government limitations.

- Accordingly, growth is expected to remain low, and a margin expansion isn't expected before 2025.

- I see no path for market-beating returns at the current valuation and reiterate a Hold with a price target of $504 a share.

Lockheed Martin ( LMT ) just announced its Q3-23 results, reporting 1.8% revenue growth and $6.75 EPS, both exceeding expectations. As the stock recovers from a disappointing second quarter primarily due to increasing geopolitical tensions worldwide, investors are once again met with the reality that is the defense industry.

It takes a very long time for higher demand to materialize, especially as the entire industry is still struggling from supply chain constraints. Furthermore, even when demand is high, defense contractors like Lockheed can't raise prices and take more margin.

I see no path for LMT to provide market-beating returns in the foreseeable future, and reiterate a Hold with a price target of $504.

Background

Back in July, I downgraded Lockheed Martin to a Hold, following an earnings call which provided a lot of clarity regarding the company's ability to improve margins in the mid-term.

As I wrote in the article, margin expansion played a crucial part in my initial buying thesis, and following management's remarks about their intention to pass any price increase and operational efficiency benefit to the customer, I understood a margin expansion is unlikely.

Heading into this quarter, I estimated it's going to be pretty much more of the same. Simply put, there was nothing about the third-quarter print that was expected to change market sentiment.

Let's see if this estimate turned out to be true.

Q3-23 Highlights

{kind=link}

Lockheed Martin Q3-23 Presentation

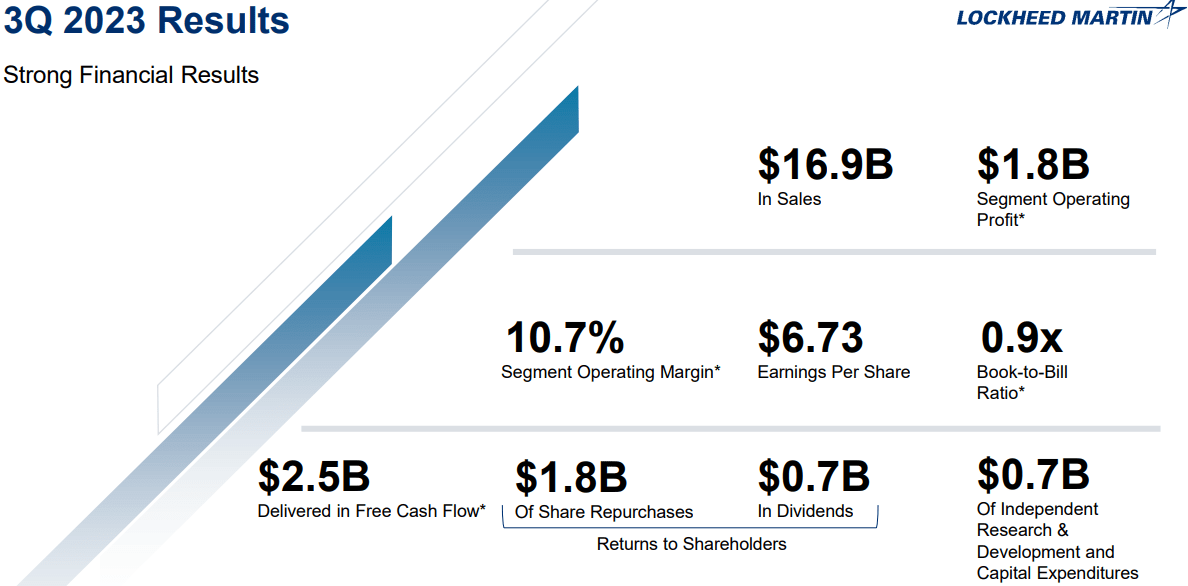

Lockheed Martin reported consolidated revenues of $16.7B, a 1.8% increase from the prior year. Based on its historical seasonality, the company is on pace to deliver relatively flat revenues for the full year. In terms of segment operating profit, the company reported $1.8B, reflecting a 10.7% margin, a 40 bps decrease Q/Q and a 50 bps decrease Y/Y.

Created by the author based on data from Lockheed Martin financial reports; MFC = Missiles & Fire Control; RMS = Rotary & Mission Systems.

Aeronautics sales decreased by 5% Y/Y, due to lower F-35 volume resulting from tough comparisons in lot funding. The decrease was slightly offset by higher volume in Skunk Works. MFC sales increased 4% Y/Y due to higher volumes in several programs. RMS sales grew by 9% Y/Y, due to higher volumes as well. Lastly, higher volumes in Space drove an 8% increase Y/Y.

Created by the author based on data from Lockheed Martin financial reports; MFC = Missiles & Fire Control; RMS = Rotary & Mission Systems.

Looking at EBIT per segment, Aeronautics declined by 12%, due to the revenue decrease combined with 72 bps margin contraction driven by lower profit adjustments. MFC operating profit increased by 4%, in line with revenues. RMS increased by 2%, as revenue growth was materially offset by a margin decrease of 78 bps, driven by lower profit adjustments. Lastly, space operating profit declined 15%, as margins decreased 220 bps due to lower net profit adjustments and lower equity earnings.

Other Notable Numbers & Guidance

F-35 deliveries grew to 30 in the quarter, up three jets Y/Y. According to management, they are now producing at a rate of 156 F-35s per year, in line with their 2025 goal.

Other Aeronautics deliveries all declined compared to the prior year period. The company's backlog decreased to $156B, reflecting a $1B (1.3%) decrease quarter-over-quarter.

{kind=link}

Lockheed Martin Q3-23 Presentation

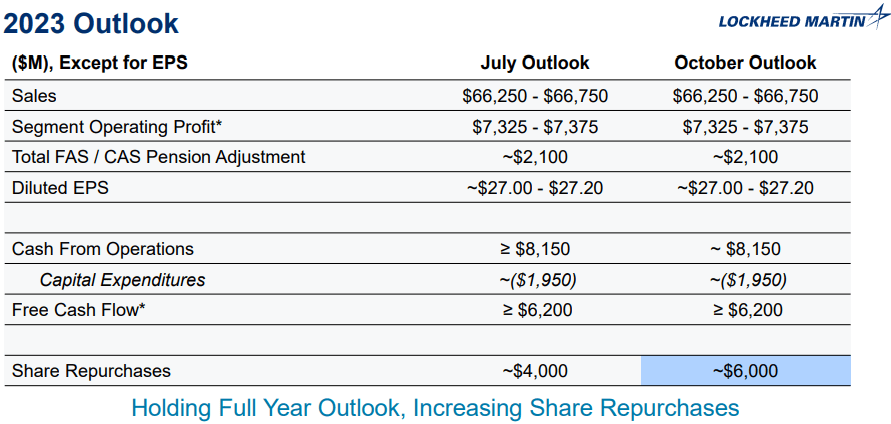

Overall, Lockheed's results are more of the same. They are still struggling with the supply chain, growth is still low, and margins are continuing to decline. In short, there's nothing to suggest we should see a significant improvement in the near term. As evidenced by the reaffirmed guidance, investors shouldn't hold their breath for a major surprise in Q4.

Important Notes And The Inability To Capture Value From The Demand Spike

On the U.S. budget, though the specific trajectory of the future U.S. defense budget is still in process between the administration and Congress, the global threat landscape is increasingly elevated. Our robust backlog reflects the relevance and importance of the Lockheed Martin portfolio and elevating deterrence to great power conflict involving the United States and its allies and the solid positioning of our business to serve our domestic and international customers.

--- Jim Taiclet - Chairman, President and CEO, Q3-23 Earnings Call

It seems pretty much clear at this point, and as we discussed in previous articles, demand is not the problem for Lockheed here. If they had unlimited capacity capabilities, we'd probably see revenues spike in Nvidia-like numbers in light of the ongoing geopolitical situation in the world. However, they do have a major capacity constraint.

A few comments on 2024... We still anticipate low single-digit sales growth as we convert our strong backlog position. As I previously mentioned, the backlog supports a higher growth rate, but the value chain remains constrained by extended lead times that have yet to compress.

On segment margins, we expect the underlying business to be relatively flat year-over-year, but anticipate variability caused by the timing of impacts from the MFC classified program. And at free cash flow, we're following the budget process to determine whether it will have an impact on the timing of our program schedules and milestones but are continuing to set internal targets that deliver mid-single-digit growth and free cash flow per share.

--- Jay Malave - CFO, Q3-23 Earnings Call

Continuing from the previous comment, we can see that management is still citing supply chain problems. Entering 2024, this will mark the fourth calendar year since COVID-19 hit, and the defense value chain is yet to fully recover.

When asked if they're thinking about increasing the capacity above the 156 aircraft target in light of the immense demand, management gave the following answer:

We've all settled on the 156 per year rate as the joint investment that we're all willing to make, given the demand that's out there.

There is the annual sort of slotting priorities discussion that happens within the Joint Program Office and the international partners, and that will keep the line full for many, many years. If we were to get significantly more international orders that might motivate us jointly, and I mean us meaning the government and industry, including our suppliers, by the way to make an incremental investment. But I think that, that would have to be a significant increase in the order book above what we see today.

--- Jim Taiclet - Chairman, President and CEO, Q3-23 Earnings Call

So, reiterating what we discussed in the previous article, Lockheed can't capitalize on the major demand spike in the short term, nor is it enough to justify changing long-term capacity plans. Combine that with the fact that Lockheed's operating margins are limited by their agreements with the government, and you realize that Lockheed isn't capable of capturing the value of the demand spike.

Valuation

Since the results came in line with expectations, there are no changes in my DCF model from the July article, and I reaffirm my price target of $504 a share. As such, I thought I'd tackle valuation from a different perspective this time.

Lockheed Martin is trading at a 16x P/E multiple, with no major difference between GAAP, Non-GAAP, Forward, or TTM, they're all in the 15.8x-16.2x range. Maybe unsurprisingly, this is pretty much in line with the median P/E the stock's been trading at for the past decade, as well as the past five years.

Lockheed operates in a recession-proof industry, and within the industry, LMT proved its ability to outperform through extraordinary products like the F-35, and incomparable shareholder returns through dividends and buybacks. Just recently, it announced its prototype of a new weapon system for protecting the United States from intercontinental ballistic missile attacks passed a key test.

As I wrote in previous articles, I find Lockheed as a very decent investment for long-term dividend investors. However, I see no path for this to become a market-beating investment at the current valuation.

I believe there are two categories of investments that are able to surpass the market's returns at a high probability. It's either investing in a business that consistently outgrows the market in terms of revenues and EPS, or, a high-quality business that's selling for a very attractive valuation.

To my assessment, Lockheed does not fall under either of those categories, trading at its historical valuation.

Conclusion

Lockheed Martin is an amazing business. It's one of the most important companies in the world, and demand for its products is as strong as any other company in the world. However, as a defense contractor, Lockheed's growth is materially constrained by its supply chain and capacity, which are not elastic and aren't capable of responding to demand spikes. Furthermore, its margins are fixed and limited under its agreements with the U.S. government.

I believe it is a great investment for those who are looking for steady dividends, low volatility, and decent returns. That being said, I see no path for market-beating returns at the current valuation.

Because we're in the business of trying to beat the market with our individual holdings, I rate Lockheed as a Hold.

For further details see:

Lockheed Martin: Q3 Is More Of The Same, No Market-Beating Returns Here