LMT - Lockheed Martin's Inflection Point Makes It A Must-Own Dividend Stock

Summary

- In this article, I start by highlighting why I believe that high-quality investing is so important. This includes focusing on quality dividend growth and low volatility. Lockheed offers both.

- Lockheed Martin has not been known for high growth, which could end in the 3-4 years ahead as the company is nearing an inflection point of higher deliveries and stronger margins.

- The company has a very decent dividend yield, satisfying dividend growth, and a focus on buybacks. I expect total shareholder distributions to accelerate in the years ahead.

Introduction

It has been a while since I wrote my most recent Lockheed Martin ( LMT ) article in May of this year. In this article, I want to do more than update the strong case for a dividend investment in this defense giant. Lockheed, which has become my largest investment, is what I consider one of the single best places to put one's hard-earned money. In this article, I go over the company's qualities as a dividend growth stock as well as new developments that push the company to what CEO Jim Taiclet calls an "inflection point". What we're dealing with here is a company that can outperform the market with a low-volatility profile, good news regarding the US and allied defense spending, and the company's ability to boost free cash flow, which it aims to distribute entirely to investors.

In other words, I will explain why I have invested close to 8% of my net worth in this defense giant.

As we have a lot to discuss, let's get to it!

Buy Quality

The other day, a friend of mine sent me a YouTube video from a guy who recommended dividend stocks with an average yield of 25%. I'm not referring to the source here as there are many similar videos out there if you look for it and I'm not looking to start a fight with anyone.

I'm bringing this up because there are a lot of examples on the world wide web of people buying ultra-high-yield stocks for the sake of income and safety. Eventually, they end up getting neither as these yields aren't sustainable.

In my world, a yield close to 3% is very decent. Everything between 3-4% is what I consider a high yield. That's not based on my opinion, but on the fact that the Vanguard High Dividend Yield Index Fund ( VYM ) is yielding 3.0%.

Hence, this article is also aimed at retail investors looking for a high yield. I want to make the case that LMT's 2.6% is a fantastic deal on a long-term basis.

With all of this said, let's look at some numbers.

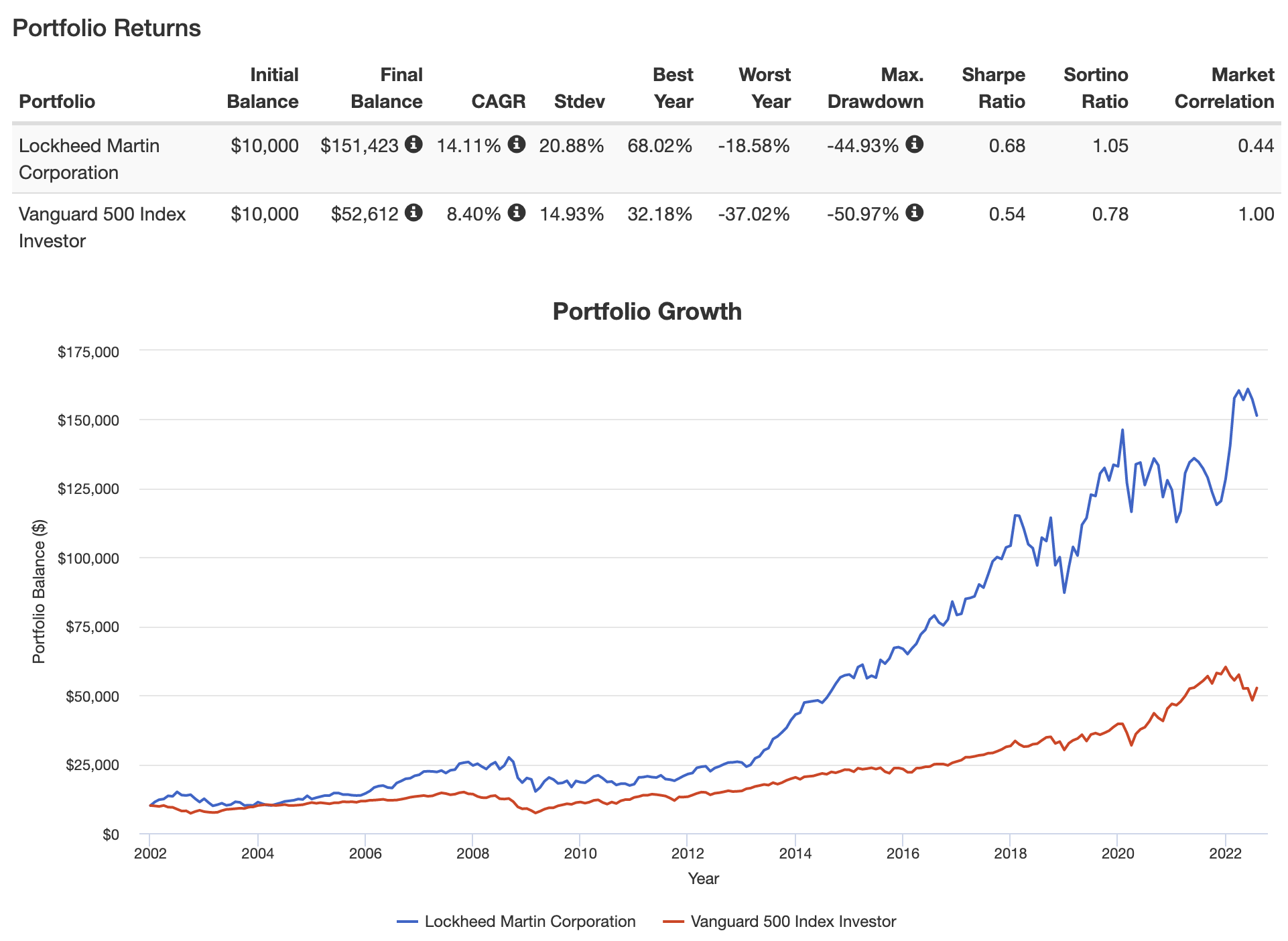

Going back 20 years, Lockheed has returned 14.1% including dividends. The S&P 500 has returned 8.4% with a standard deviation of 14.9%. Lockheed's standard deviation is a bit higher at 20.9%, which still allows the company to beat the S&P 500 on a volatility-adjusted basis as well (Sharpe/Sortino ratios). Moreover, LMT has a market correlation of just 44% during this period. The company does rise in bull markets, but it doesn't necessarily sell off every time the market encounters weakness.

{kind=link}

After all, Lockheed, like all of its peers, is not mainly impacted by demand risk - compared to "non-defense industrials". As the years after 2019 show, defense companies are mainly struggling with supply risks as demand remains high. After all, Lockheed generates close to 100% of its sales through government contracts.

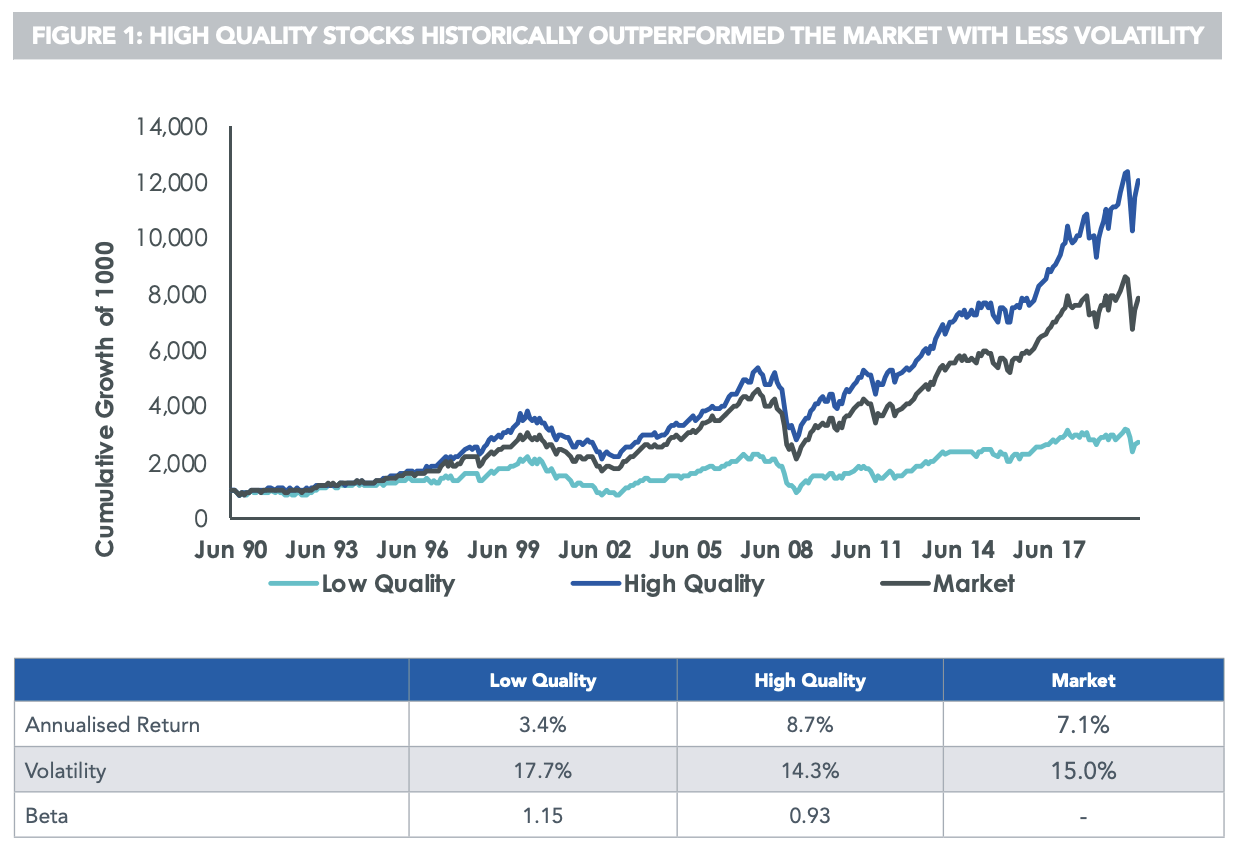

I'm bringing this up because I recently looked into why investors should buy quality stocks, which includes discussing the definition of quality - after all, I doubt anyone reading this has ever bought a stock they believed was a non-quality stock.

In an article called "Nasdaq: When Quality Means Outperformance", I looked into what makes a company a quality company.

In July 2020, WisdomTree published a report making the case for quality stocks. A part of its takeaway was:

Out of all the equity factors, Quality is one of the most consistent. It has a proven track record of outperformance and it typically delivers steady returns across most market regimes. It is ideal for prolonged periods of uncertainty when a bear market rally or a deep drawdown are as likely and it is, therefore, an ideal candidate to consider for a strategic, core investment in equities

At this point, you're probably wondering how WisdomTree defines quality. Well, this is the answer:

Quality Investing is defined as investing in companies that have some or all of the following characteristics: good management, strong balance sheet, economic moat, sound dividend policy, stable earnings, and profitable and efficient operations.

While I believe that "good management" is a combination of all the other characteristics, a quality company is a company with a big moat, able to achieve dividend growth thanks to stable earnings and profitable operations. In other words, all characteristics above are related. For example, if I were to run a business with positive free cash flow but a horrible balance sheet, I would probably have to prioritize debt reduction over dividend growth.

A company with all characteristics offers the ultimate stamp of approval, which benefits investors in bull markets and bear markets when investors prioritize quality over high-risk growth stocks.

What this means is that quality stocks outperform the market on a longer-term basis with a lower volatility profile. The chart below displays this quite handily - the same goes for the Lockheed Martin chart I showed in this article.

{kind=link}

While I do own some high-volatility stocks, buying high-quality is very important to me and I cannot stop communicating this on here as well as it allows investors to better stomach steep drawdowns. After all, not panicking during recessions and sell-offs, is a big part of generating long-term wealth. Lockheed is a cornerstone of my low-volatility strategy. This includes its dividend.

Lockheed Martin's Dividend

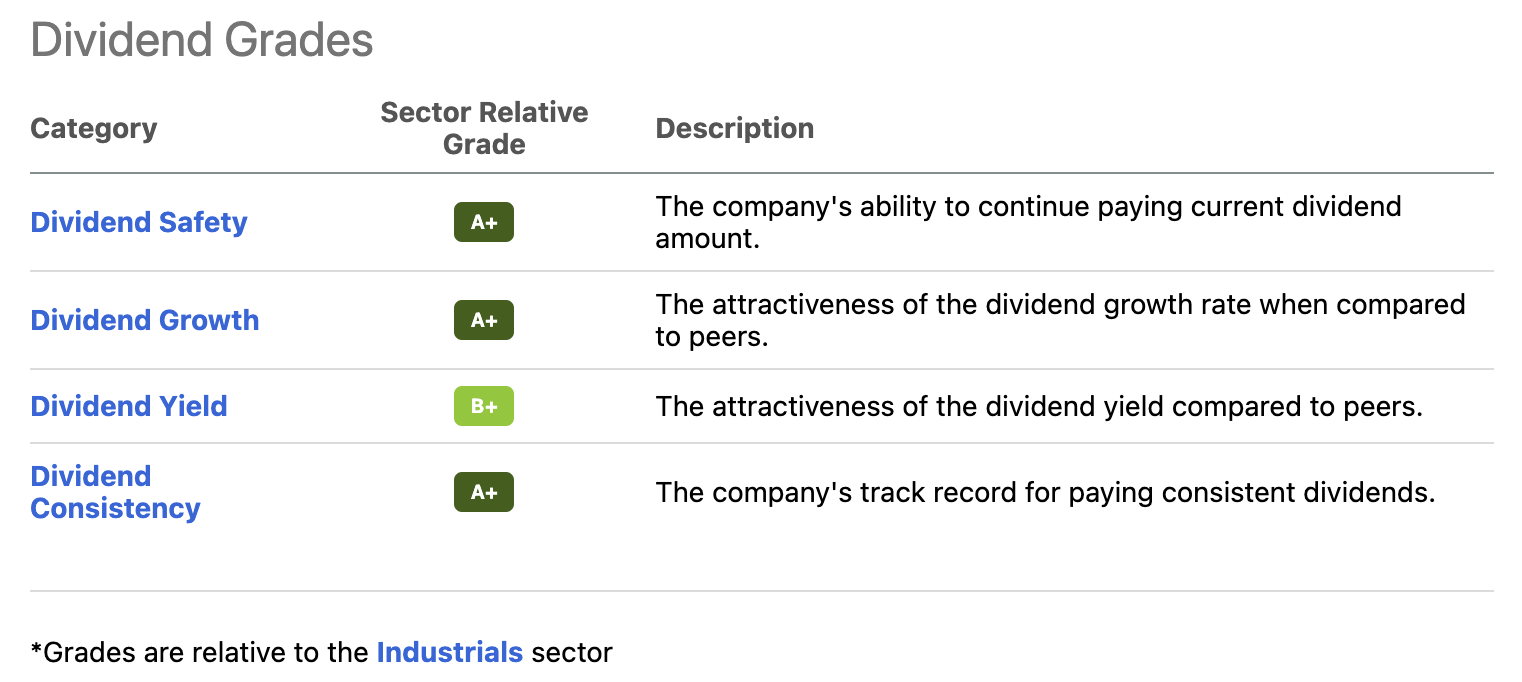

The Lockheed dividend is fantastic. Looking at the Seeking Alpha dividend scorecard, we see that the company scores very high relative to the industrials sector. LMT scores A+ on safety, growth, and consistency. Its yield scores a B+.

{kind=link}

Currently, Lockheed pays a $2.80 dividend per share per quarter. That's $11.20 per year and 2.6% of its current stock price.

2.6% isn't *that* much, and it doesn't qualify as a high yield. Yet, I think it's one of the best yields to own. Because dividend growth is rather high and extremely consistent.

Over the past 10 years, the average annual dividend growth was 11.4%. This number has declined to 8.6% on a three-year basis, which is still a great deal given that we're dealing with a yield close to 3%.

These are the most "recent" hikes:

- September 2021: 7.7%

- September 2020: 8.3%

- September 2019: 9.1%

If we assume that the company maintains 8% long-term dividend growth, a 2.6% yield turns into a 3.8% yield on cost in just five years.

On a side note, I believe that dividend growth will accelerate as I will explain in this article. I'm using 8% as a base case here to show what we're dealing with here in terms of potential yield growth in the near-term future.

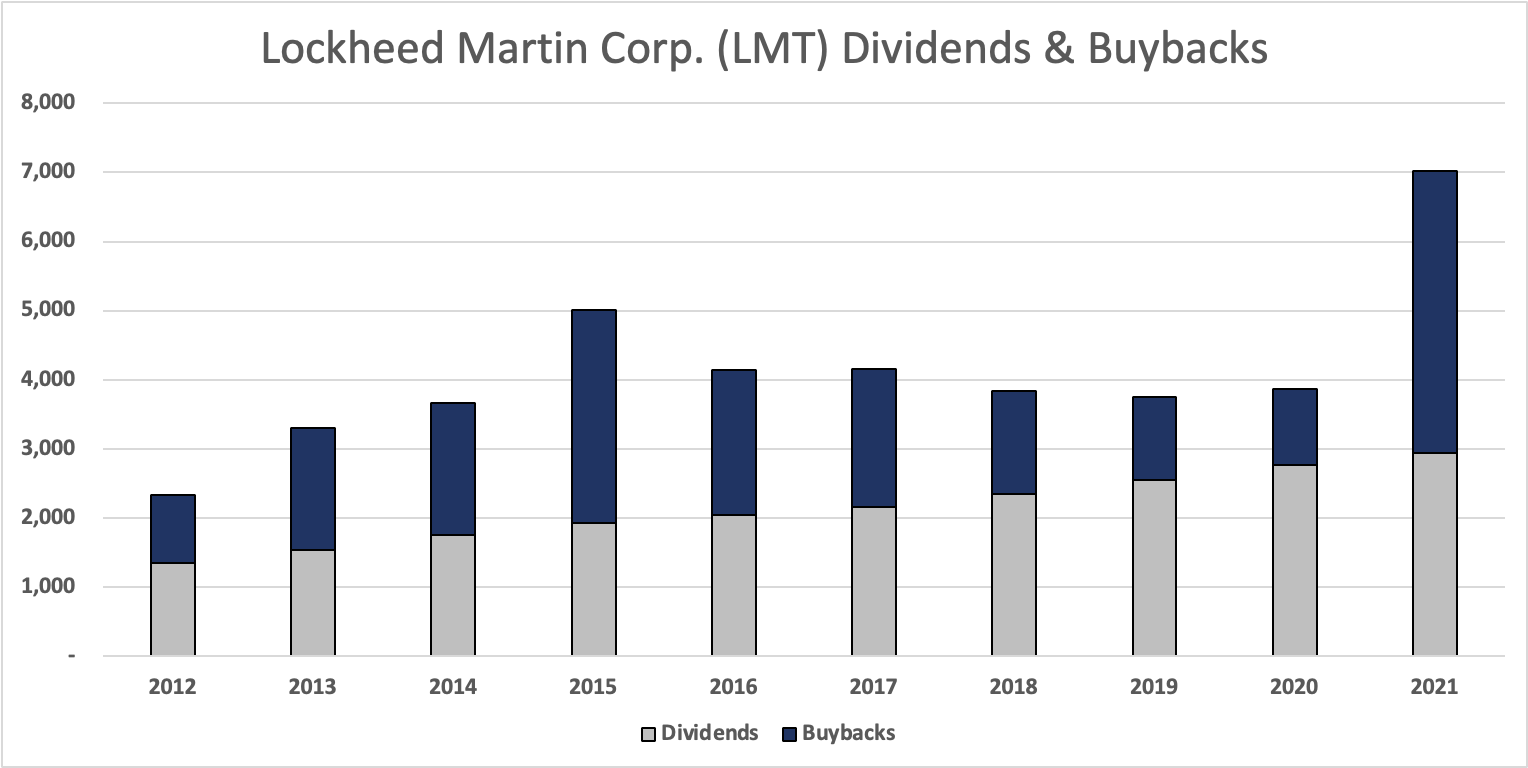

It also needs to be said that LMT is keen on buybacks. The company was especially engaged in large buybacks during the stronger pre-COVID years (and 2021).

{kind=link}

Going back to 2012, the company's dividend has been raised by 180% while the company bought back 19% of its diluted shares outstanding.

Now, with this in mind, let me address why I believe that LMT becomes an even bigger buy than it is already.

LMT's Inflection Point - A Strong Bull Case

It feels a bit like the world is falling apart, at least from a geopolitical point of view. The war in Ukraine is not just causing human suffering in the region, but the economic war tied to it is impacting all of Europe. In Asia, it looks like China is becoming increasingly aggressive towards Taiwan.

In the Middle East, Afghanistan is rapidly going back in time after the US exit almost exactly one year ago.

Add to this that Iraq is now accelerating into a lawless mess as the government is losing control of parts of Baghdad.

{kind=link}

As I mention in almost all of my articles, the goal of owning LMT is not to benefit from war. The point of owning high-tech defense is that investing in next-generation capabilities prevents war - at least between major nations, not terrorists.

With all of this in mind, global defense spending is ramping up.

Here are some headlines that pop up on Google when searching for "defense spending":

- Japan plans big defence spending boost to counter rising China threat

- Taiwan unveils record defence budget amid tensions with China

- Taiwan Plans 14% Boost in Defense Spending to Counter China

- Seoul proposes 4.6% hike in defense spending for 2023

- Global military spending hits record high

- Spain approves over $1B boost in military spending

- Germany commits €100 billion to defense spending

In the US, the situation isn't different as the House and Senate Armed Services Committees approved their versions of the FY 2023 National Defense Authorization Act. The SASC recommended a $45 billion increase to the President's request and the full House chamber passed the completed authorization bill with a $37 billion increase.

{kind=link}

According to Lockheed Martin :

While the budget process remains in its early stages, we are encouraged by the support our programs have seen with the Senate recommending additional F-35 and Black Hawk helicopters, increases over the lower-than-expected volumes that were in the initial presence request.

What we're dealing with here is the recognition that high inflation calls for more funding while global security threats (i.e., the ones I listed in this article) provide bipartisan support for higher spending.

Moreover:

[...] the demand in the situation that our customer base is facing has dramatically changed over the last three, four months.

Based on these developments, the company is changing its outlook when it comes to the "inflection point" for the company. Initially, Lockheed expected the US defense budget to be relatively flat in the next few years. That was the likely path prior to the war. Now, that has changed.

According to CEO Jim Taiclet :

[...] we're aiming for the company and for the share count to be ready for an inflection point now again, in 2024 and beyond, the middle of the decade. This unfortunate situation in global security having deteriorated can only bolster our inflection point from where it would have been.

Lockheed Martin has been through a prolonged period of very slow revenue growth as it cannot impact the timing of major programs like the F-35, the Black Hawk, and supply chain issues causing inflation to fly. Hence, share buybacks were not only a way to generate value in a low-growth period but also to prepare the company for "turbocharged" growth. After all, when growth accelerated while the share count is lower, earnings per share growth is even stronger.

This brings me to the inflection point again, as the company sees accelerating revenue growth mid-decade.

[...] we think shareholder value inflection point comes mid-decade because the revenue growth we expect to ramp in, we're doing a lot on the efficiency side, something we can control over the next two, three years with our digital transformation and other cost control efforts that we've actually redoubled recently. And so we're going to continue to invest in the business, and so we can make that -- during this period so we can make that inflection point as attractive as possible for you as we expect it to come.

While Lockheed is unable/unwilling to discuss how high operating cash flow could rise in the years ahead, it remains committed to returning 100% of free cash flow to its shareholders.

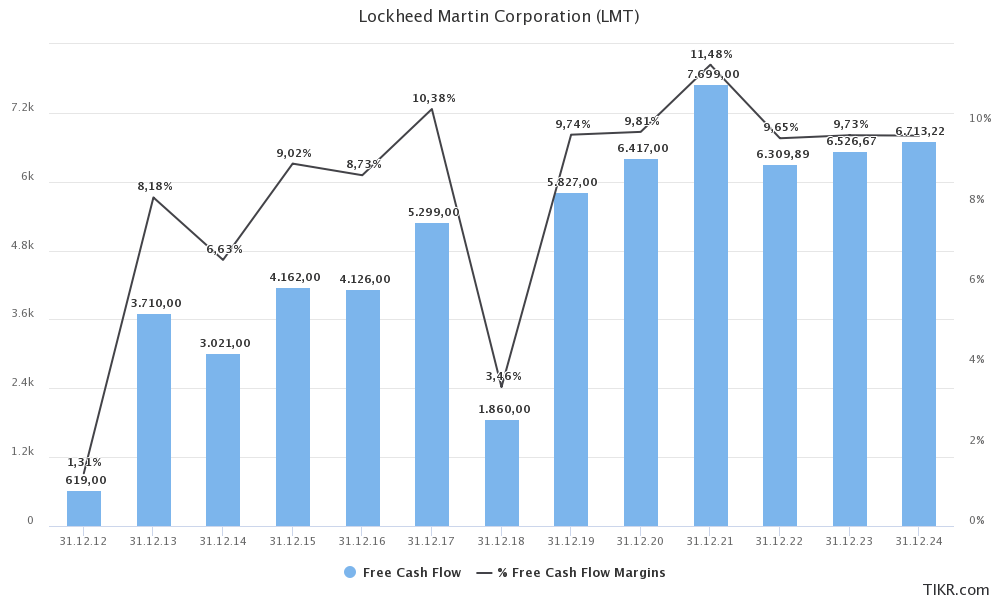

With that said, it's good news that LMT expects to be close to an inflection point as free cash flow isn't expected to grow that much in the two years ahead. Prior to what LMT believes will be an uptick in growth, we're likely looking at $6.5-$6.7 billion in annual free cash flow based on an FCF margin close to 9.7% of total revenues.

{kind=link}

The good news is that even $6.7 billion in expected free cash flow is a good deal. It translates to a 5.9% FCF yield using the company's $112.7 billion market cap. If the company maintains high shareholder distributions, we are looking at strong dividend growth and buybacks ahead of the inflection point.

Valuation

Lockheed Martin is valued at roughly 12.3x EBITDA. This is based on its $127.4 billion enterprise value consisting of $112.7 billion in equity market value, $8.9 billion in expected net debt (just 0.9x EBITDA), and $5.81 billion in pension-related liabilities. I used $10.4 billion in expected EBITDA until the end of 2024 (pre-inflection point).

Hence, I can recycle the comment used in my last article (updating the numbers):

It's not deep value, but it's not high enough to keep me from buying. The same goes for the implied free cash flow yield of 5.9% that I calculated in this article. It's close to the upper bound of the historic range. In other words, investors are not overpaying to get access to free cash flow, and that is very important.

YCharts

Takeaway

Markets are nervous. Inflation is high, supply chains are damaged, and the Fed is eager to aggressively hike to combat inflation. Meanwhile, economic growth is slowing and global tensions are rising.

Yet, I sleep well knowing I have high defense exposure, which includes having made Lockheed Martin my largest position.

The company is one of the highest-quality stocks thanks to a stellar business model with a huge moat, steady financials, and the ability and willingness to let shareholders benefit through steadily growing and (what I believe to be) juicy dividend yield.

While financials have been steady, the company is nearing an inflection point. Order books are expected to rise due to rising defense budgets in the US and abroad, with higher deliveries and higher margins expected to happen after 2024.

For now, the company will mainly focus on buybacks to lower the share count. This will help to fuel strong earnings per share growth after 2024 when revenue is expected to accelerate.

The valuation is fair, and I recommend LMT to income-oriented investors, as well as dividend growth investors and everyone looking for high-quality exposure with the chance to outperform the market on a long-term basis.

(Dis)agree? Let me know in the comments!

For further details see:

Lockheed Martin's Inflection Point Makes It A Must-Own Dividend Stock