LMT - Lockheed Martin's Shares Should Be Resilient In 2023

Summary

- Lockheed Martin had one of its best years in a long time during 2022. Shares bucked the overall downward trend in the markets.

- Defense equities have become a safe haven in this uncertain global economy, given Russia's invasion of Ukraine as well as concerns over US-China relations.

- We think many defense contractors, including Lockheed Martin, are well-positioned to do well in 2023. Its ~2.5% dividend yield should offer support to shares, too.

- Our fair value estimate of Lockheed Martin is currently at ~$412 per share with the high end of the fair value estimate range just north of $505.

- Though we’re not expecting a huge 2023 as it relates to Lockheed's share price performance, we are expecting resilience given its strong fundamentals and dividend growth profile.

By Valuentum Analysts

Lockheed Martin (LMT) put up one of the best years in history during 2022 - not only did it beat the market, but its shares advanced more than 35%, while broader economic markets were down double-digits. With ongoing geopolitical uncertainty from the Ukraine invasion to Sino-American relations, investors have been flocking to defense equities as a safe haven amid global economic uncertainty and contractionary monetary policy. During 2022, defense equities turned into "defensive" equities, and we think many, including Lockheed Martin, are well-positioned to do well in 2023, too.

Lockheed Martin is quite shareholder friendly. At the time Lockheed Martin issued third-quarter results in October , the defense contracting giant revealed how much it cares about its shareholder base by rewarding them with a high-single-digit increase in its quarterly dividend, to $12 per share on an annual basis, and upping its share repurchase program to the tune of $14 billion. During the firm's third quarter of 2022, Lockheed Martin's free cash flow generation was strong and reached $2.7 billion, which compares to $1.6 billion in the same period last year.

We like to use the discounted cash-flow model in our work. Our discounted cash-flow-derived valuation of Lockheed Martin is currently at ~$412 per share with the high end of the margin of safety range just north of $505. We'll talk more about how we derive our fair value estimate and fair value estimate range for Lockheed Martin in this note. With the company's equity trading at ~$475 at the time of this writing and management spending billions in share repurchases during the latter months of 2022 alone, we don't think 2023 will be as strong of a year for the firm as it's reasonable to believe that some technical consolidation may be required given a slower pace of buybacks.

With that noted, however, we think shares of Lockheed will remain resilient, given its moaty characteristics, cash-flow generating prowess and payout yield, which stands at approximately 2.5% at the time of this writing. During the past 12-18 months, defense stocks, in general, have held up quite well, particularly in light of the weakness across the broader equity markets over the same time period. Dividend paying stocks have also held up nicely. We think one might still expect conservative investors to continue to park cash in defense equities as global economic uncertainty and contractionary policy continues.

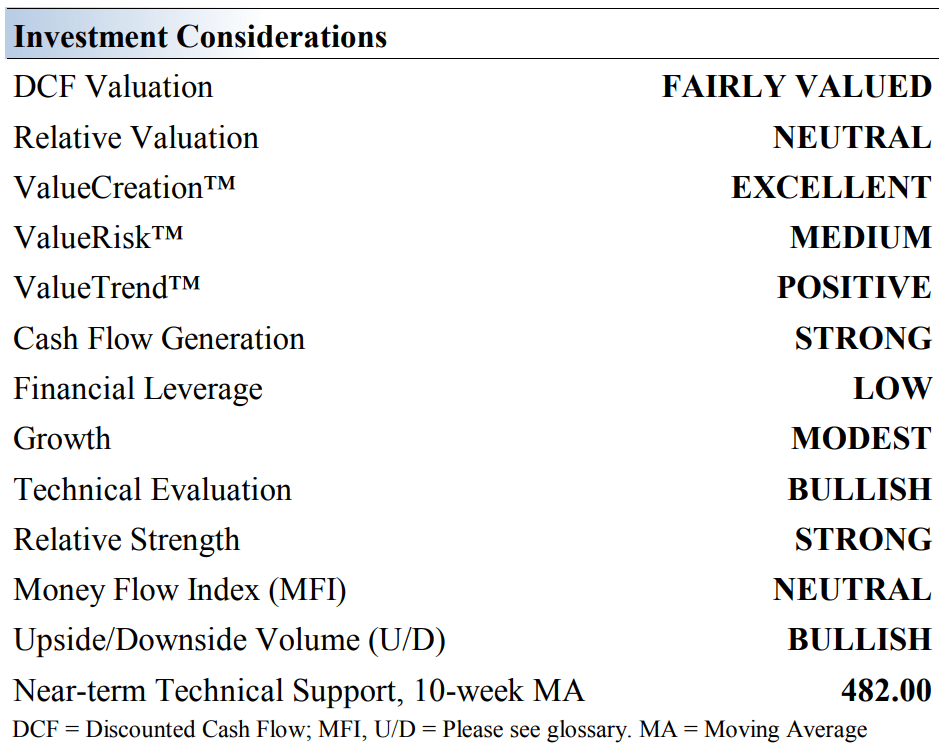

Key Investment Considerations

Key Investment Considerations (Image Source: Valuentum)

{kind=link}

Lockheed Martin is an aerospace and defense powerhouse that researches and makes advanced technology systems, products and services. The current fast-changing and tense geopolitical environment is driving the need for more defense spending, in our view, playing into the company's wheelhouse.

Several geopolitical conflicts in particular could stimulate more defense spending including growing US-China tensions, perennial threats from North Korea, and Russia's invasion of Ukraine, among others. Given the tense geopolitical backdrop, we think the outlook for defense spending from the US and its Western allies is solid. This should offer more and more opportunities for Lockheed in the years ahead.

Such a dynamic security landscape around the world requires state-of-the art weapons systems and advanced, sometimes clandestine technologies. We think the firm is well-positioned to meet the needs of governments around the world that continue to demand more and more from Lockheed. As evidence of that, Lockheed ended the third quarter with backlog of $139.7 billion, up from $135.4 billion at the end of 2021.

Lockheed Martin's order rates continue to be lumpy but healthy, and its backlog offers insight into the company's future expected earnings and cash flow performance. With our expectations for defense spending to be solid in coming years, Lockheed Martin's potential to continue growing at a nice clip is strong, in our view, particularly as it works to keep the warfighter in top condition.

When Lockheed reports fourth-quarter 2022 results, likely at the end of January, the firm expects cash flow from operations greater than $7.9 billion and capital spending of $1.9 billion to result in free cash flow generation greater or equal to $6 billion. The defense giant's free cash flow came in at $4.9 billion through the first nine months of 2022, a level that was up from $4.0 billion during the same time period in the year-ago period.

Lockheed Martin also has exposure to the space economy, which helps round out the potential of its business outlook. It has a number of offerings in this area that meet commercial, governmental, and national defense needs. We think the defense contractor's potential for considerable growth in this area is encouraging, though we note that such an area may be more discretionary than other necessary defense requirements.

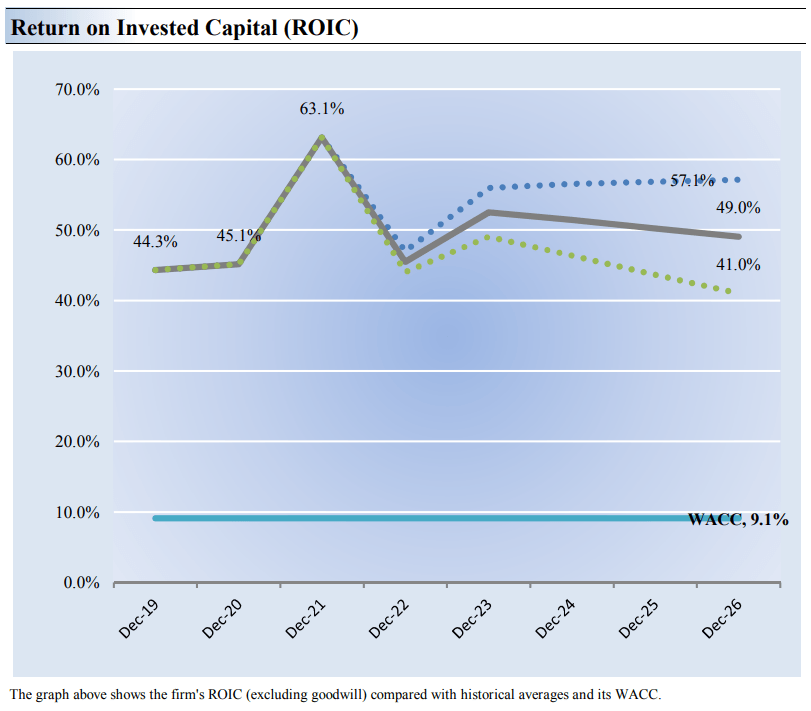

Lockheed Martin's Economic Profit Assessment

Return on Invested Capital (Image Source: Valuentum)

{kind=link}

We like to say that return on invested capital [ROIC] is the holy grail, as we believe the best measure of a company's ability to generate value for shareholders is expressed by comparing its return on invested capital with its weighted average cost of capital [WACC].

The difference between ROIC and WACC is called a company's economic profit spread. Economic profit is much different than accounting profit. Some companies could be generating accounting profits, but destroying shareholder capital along the way. What this means is that their respective cost of capital is greater than their return on invested capital.

Lockheed Martin's 3-year historical return on invested capital (without goodwill) is 50.9%, by our estimates, which is above the estimate of its cost of capital of 9.1%. Lockheed Martin is a strong economic-profit generator, in this sense. It is generating a positive economic value spread.

As such, we assign Lockheed Martin a ValueCreation rating of EXCELLENT. In the image immediately above, we show our forecasts for the company's ROIC in the years ahead. The solid grey line reflects the most likely outcome, in our opinion, and the scenario that results in our fair value estimate.

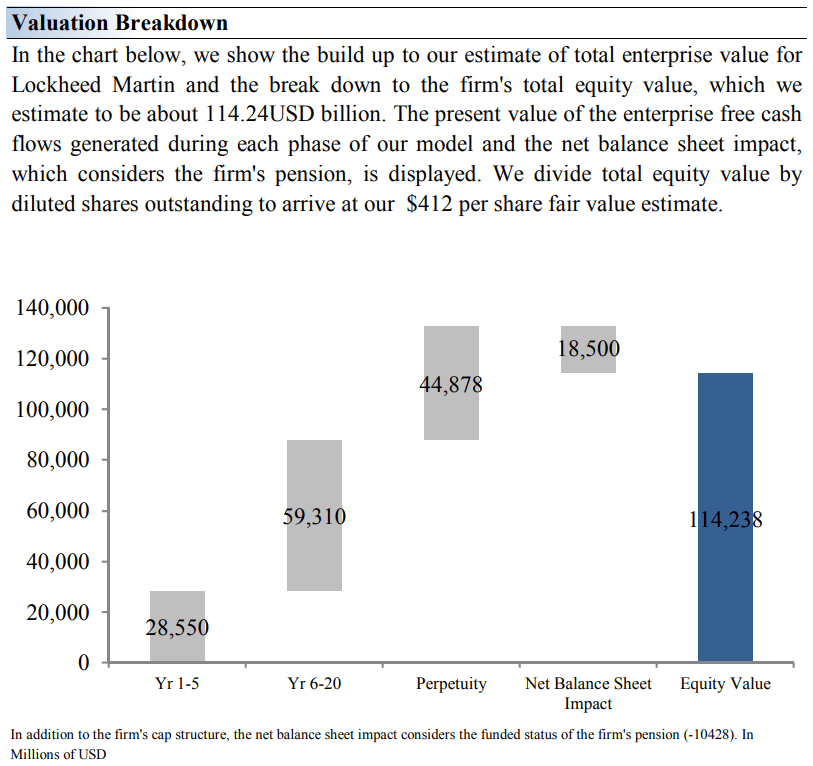

Lockheed Martin's Cash Flow Valuation Analysis

Valuation Breakdown (Image Source: Valuentum)

{kind=link}

The discounted cash flow model is a powerful process. It helps to put together all of the qualitative (and quantitative) aspects of a firm. If something qualitative cannot be quantified into the DCF, one might question whether or not that thing is truly a source of value. Qualitative items such as the strength of management, the strength of a brand name, or some other intangible quality such as culture must all be quantified within this process. The DCF hits straight to the core, and that's what we like most about it.

On the basis of our DCF process, we think shares of Lockheed Martin are worth $412 each with a fair value range of $319-$505. Note, this updated fair value estimate is slightly higher than the one in our previous update on Seeking Alpha in August 2022. The margin of safety that we ascribe to our fair value estimate is driven by the firm's MEDIUM ValueRisk rating, which is derived from an evaluation of the historical sensitivity of important valuation considerations and a future assessment of them.

We find that we add the most value with our DCF process as it relates to thinking about long-term operating assumptions. As a result, our near-term operating forecasts, including key items such as revenue and earnings, generally will not vary too much from consensus estimates or management guidance. Near-term forecasts don't move the needle much in the DCF. Our valuation model reflects a compound annual revenue growth rate of 2.3% during the next five years, a pace that bucks any cyclical downturn caused by global economic weakness.

Our valuation model reflects a 5-year projected average operating margin of 14%, which is above Lockheed Martin's trailing 3-year average. Beyond year 5, we assume free cash flow will grow at an annual rate of 3.7% for the next 15 years and 3% in perpetuity. We think these operating assumptions are reasonable (and perhaps conservative) for Lockheed Martin, and we apply a 9.1% weighted average cost of capital to discount the resulting future free cash flows.

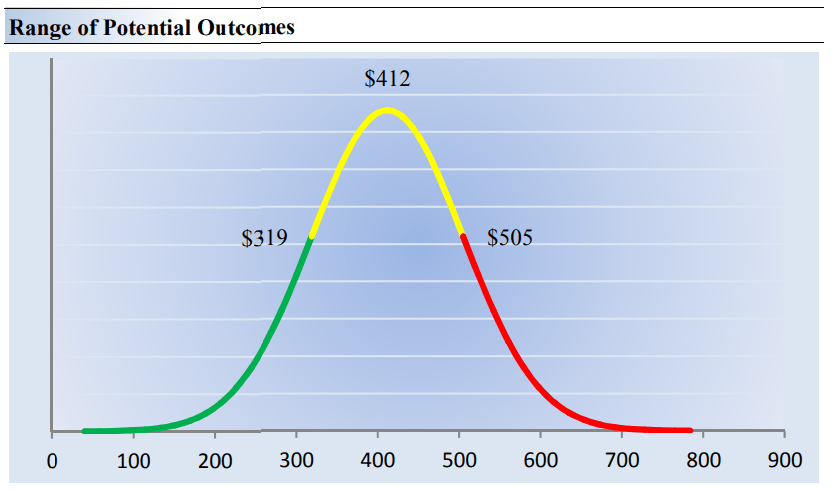

Range of Fair Value Outcomes (Image Source: Valuentum)

{kind=link}

Valuation is never supposed to be precise. In fact, it is folly to believe in precision when it comes to the DCF. That doesn't mean the process is not without significant value, however. When the price of a company falls way outside what one might consider to be a fair value range, as derived by the DCF, then a true opportunity may await the investor. These are the companies that Warren Buffett calls "fat pitches."

Our discounted cash flow process values each company on the basis of the present value of all future free cash flows from year 1 through perpetuity. Though we estimate Lockheed Martin's fair value at about $412 per share, we emphasize that each company has a unique range of probable fair values that's created by the uncertainty of future revenue or earnings expectations, especially those forecasts made long into the future -- the ones that nobody can truly be sure about.

After all, if the market knew the future with certainty, there wouldn't be much volatility in the markets as stocks would trade exactly at their known fair values. This is an important thought as the market is a pure reflection of future uncertainty.

Said another way, it is the market that is trading shares on the basis of future fundamental expectations that sets the price, and it is the analyst's (market's) assumptions of future fundamental expectations that sets the value. This link is inextricable and forms the basis for how we view changes in stock prices -- to a large extent, as changes in future expectations.

As we embrace the uncertainty of future expectations, our ValueRisk rating sets the margin of safety or the fair value range we assign to each stock. In the graph above, we show this probable range of fair values for Lockheed Martin. We think the firm is attractive below $319 per share (the green line), but quite expensive above $505 per share (the red line). The prices that fall along the yellow line, which includes our fair value estimate, represent a reasonable valuation for the company, in our view.

Though this fair value range for Lockheed Martin is quite large, future expectations can change quickly, and we only have to look at 2022 to see how fast just one key driver behind the DCF changed. For example, to start the year, the 10-year Treasury rate was resting at a benign 1.5%, but it surged to north of 4% in October of last year. Though a 250 basis point change in the discount rate doesn't seem like much, it has widespread implications on long duration equities, which don't generate material free cash flows until long into the future.

Dividend Considerations

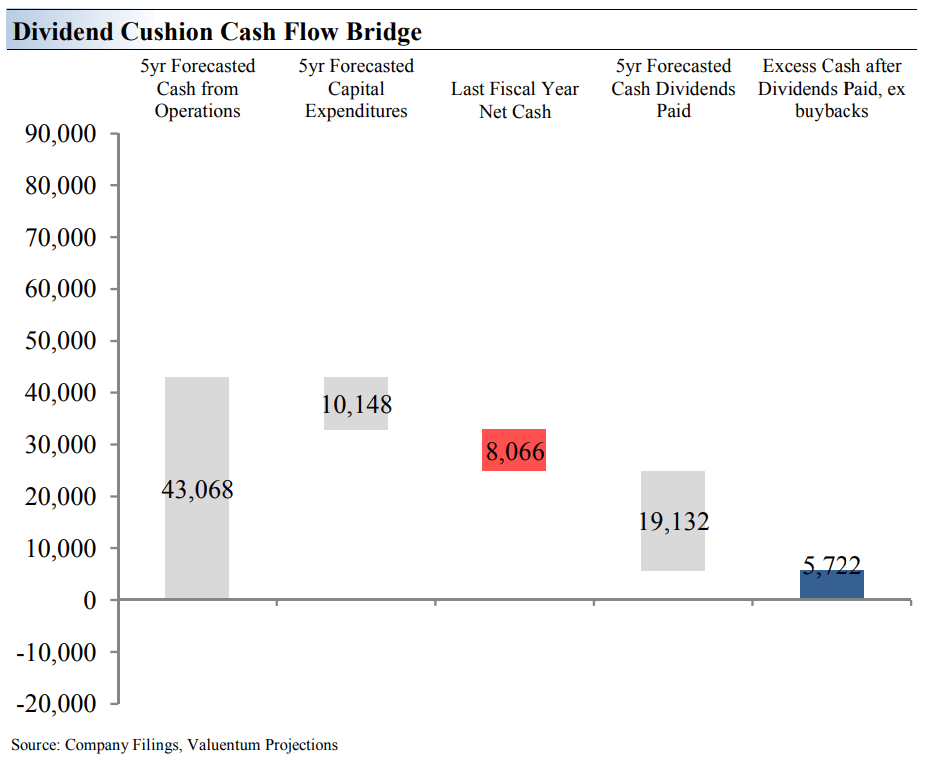

Dividend Cushion Cash Flow Bridge (Image Source: Valuentum)

{kind=link}

The discounted cash flow model has other applications, too, and it could be used to assess dividend health. For example, in forecasting future assumptions within the DCF, one invariably derives future expectations for operating cash flows, capital expenditures, as well as future expectations for cash dividends paid. These forecasts are very valuable for income and dividend growth investors.

By applying the DCF in the income or dividend growth context, one can look at whether the firm will generate sufficient free cash flows over a certain period (let's say, five years, as in the case of the Dividend Cushion ratio, above), and compare that sum to expectations of a company's future expected cash dividends paid over the same time period.

If the company can generate more free cash flows than pay as cash dividends over the same time period, its dividend health can be viewed as rather strong. Further, if the company has a large net cash position on the balance sheet, it has further ammunition to support the payout if future expectations of free cash flow come up short.

We tend to like companies with strong free cash flow generation in excess of their cash dividends paid and a net cash position to boot. Lockheed Martin has tremendous free cash flow generation in excess of expected cash dividends to be paid over the next five years, but a net debt position. Still, its Dividend Cushion remains strong given the excess cash we expect it to generate after paying dividends and dealing with debt-service costs over the distinct five-year forecast period.

The Dividend Cushion ratio should always be viewed as a ranking mechanism given that we wouldn't expect all companies to have to repay debt over the immediate five year period. Much like a credit rating ranks probability of default, we think the Dividend Cushion ratio helps rank probability of a dividend cut.

For companies that have a large positive blue bar at the right of the image above, their Dividend Cushion ratios are above 1. The larger the ratio is above 1, the stronger the dividend growth potential, in our view. The smaller the ratio below 1, or the higher the negative a ratio, the higher the probability of a dividend cut. These companies won't have a positive blue bar.

Concluding Thoughts

A lot of things played into Lockheed Martin's hands during 2022, not the least of which is a robust buyback program that catapulted shares during the year. Though we don't expect a huge year in terms of share-price performance for the company in 2023, we expect the company's equity to be resilient, and we like Lockheed Martin in the context of our dividend growth process.

The defense contracting giant's free cash flow generation remains solid (as evidenced by its most recently reported quarter), its backlog has strengthened since the end of 2021 (despite global economic uncertainty), and growing geopolitical tensions continue to drive the need for more and more defense spending. Europe remains on high alert as the war in Ukraine rages on.

Though we prefer Lockheed Martin to have a net cash position on the books as it relates to an evaluation of its dividend health, shares yield an attractive ~2.5% at the time of this writing, and we think they could make a lot of sense in a well-diversified equity portfolio targeting long-term dividend growth potential. At the very least, Lockheed Martin should be on your radar. We hope you enjoyed this work.

This article or report and any links within are for information purposes only and should not be considered a solicitation to buy or sell any security. Valuentum is not responsible for any errors or omissions or for results obtained from the use of this article and accepts no liability for how readers may choose to utilize the content. Assumptions, opinions, and estimates are based on our judgment as of the date of the article and are subject to change without notice.

For further details see:

Lockheed Martin's Shares Should Be Resilient In 2023