LMT - Lockheed Martin: Set For Long-Term Growth

Summary

- Lockheed Martin is a hugely profitable defense contractor which boasts impressive shareholder returns.

- Market-leading product portfolio complemented by long-term, fixed-price contracts guaranteeing future revenues.

- Flatline FY22 shouldn't hurt long-term growth.

- The growing prevalence of global geopolitical tensions should boost the US Defense budget and thus Lockheed's revenues.

- A high share price means building a position from a value perspective is difficult.

Investment Thesis

Lockheed Martin Corporation ( LMT ) is a market leader in the defense and arms sector. Their market reach and vertical integration is unparalleled which provides the firm with significant value generation possibilities.

Historically, the company has provided significant shareholder returns while maintain strong rates of revenue growth.

Their current portfolio of products and solutions combined with long-term fixed price contracts have allowed the firm to lock-in future profitability for the foreseeable future.

However, a high share price means determining the right time to build a position is incredibly difficult.

Company Background

Lockheed Martin Homepage

Lockheed Martin is an American aerospace , arms and defense company headquartered in North Bethesda, Maryland. Lockheed is the clear leader of the defense industry which is reflected by a significant portion of revenues coming from military focused sales.

A majority of Lockheed's resources are currently focused on their F-35 multirole combat stealth fighter jet along with their hypersonic missile and missile defense equipment programs. Most of the contracts associated with these programs are multi-year agreements which guarantee Lockheed significant stability in revenue prediction.

Thanks to the immense vertical and horizontal integration achieved by the company, the firm is able to profit from multiple different aspects of their arms and defense programs. This helps to diversify cashflows and create a company which continuously achieves significant profits.

Economic Moat - In Depth Analysis

Lockheed Martin has an almost unrivalled level of industry knowledge in the arms and defense sector. Their simply massive scale and historical expertise has allowed the firm to develop a tangible economic moat.

This wide economic moat is primarily built upon two key factors: their technological advantage and generous exposure to public and classified government contracts.

From a technological perspective, the development of arms, defense equipment, fighter jets and missiles is incredibly complicated and costly. The significant levels of investment required by a firm to even begin developing a product which exceeds the capabilities of the competitions offerings is truly astronomical.

A firm embarking on such a mission to develop a new product would also need to source costly and rare capital (both in terms of facilities and crucially employees) to ensure the program's success.

Luckily for Lockheed, through their history of mergers and acquisitions the company has acquired the extensive portfolio of facilities, employees and financial resources required to ensure they are the market leaders in almost every segment in which they compete.

Lockheed Martin operates in four primary business segments: Aeronautics, Missile and Fire Control (or MFC)), Rotary and Mission Systems (RMS) and Space.

Lockheed Martin - Aeronautics

In the Aeronautics segment, the company has received the Collier Trophy (awarded each year for the greatest achievement in aviation) six times. Their most recent win was in 2018 thanks to their innovative Automatic Ground Collision Avoidance System ( Auto-GCAS ) which is employed on some of their F-35 Lightning II fighters.

The F-35 alone is the most advanced multirole stealth fighter available. Despite its manufacturing and development troubles, the F-35 is a perfect representation of the company's ability to gauge customer demands and deliver a product which exceeds these requirements.

{kind=link}

Annually, Lockheed generates approximately 25% of their revenues from the F-35 program both from aircraft sales and on-going maintenance services. The jet continues to be a cornerstone in their revenue structure and serves as a flagship for the companies' technological abilities.

Program lifespans for such advanced combat fighters can vary, but the F-35 is now expected to remain in active use until at least 2070 . This provides Lockheed with a half-century worth of revenue generation opportunities with the jet.

Despite the F-35 having experienced multiple development timeline and budget overruns (and having cost Lockheed over $350B to develop), the expected service life for the jet will undoubtedly allow the firm to generate huge profits from the program.

While competing multirole fighter jets exist in the market from the likes of industry competitors Dassault and Saab, there is simply no aircraft which can directly match the breadth of abilities harbored by the F-35 platform.

Furthermore, due to the incredibly long development cycle associated with the development of a bespoke aircraft, it would be incredibly unlikely that a new firm could even replicate let alone exceed the F-35's abilities in the coming 30-40 years.

Finally, it must be considered that Lockheed continues to bag significant US Department of Defense ((DoD) contracts to produce more of their F-35 fighters. Just earlier this year in August, Lockheed was awarded a $7.6B contract to produce 129 stealth fighters for the US military and allied forces. The firm also continues to receive smaller contracts for the development of new F-35 variants designed for allied nations uses.

The established relations held by Lockheed Martin and the US DoD allows the company to extract unparalleled levels of value from their products. From a shareholder's perspective, this should in theory allow for increased operational and net margins thanks to the ratio between development costs and revenues generated becoming significantly more fiscally favorable.

Lockheed Martin - MFC

When analyzing the MFC business segment, a similar story of technological prowess combined with contractual superiority can be observed.

Lockheed's primary products in the MFC segment include Air and Missile Defense products, Strike weapons and Tactical Missiles. Missile solutions such as the Hellfire and Javelin programs have been around for over 20 years with continued innovation keeping the products relevant to current global conflicts.

These MFC products are also incredibly complicated pieces of technology with significant sunk costs (both financial and time) being associated with their development. The sale of these solutions usually consists of contracts similar to those seen with Lockheed's F-35 program. A majority of the MFC segment caters once more to the US military and its allied nations.

Given that a good portion of Lockheed's MFC portfolio of products can be classified as "consumables", Lockheed benefits from repeat sales of missiles and strike weapons to its customers. A majority of Lockheed's missile programs do not have a set lifespan as continued product developments and launches provide to maintain future relevance.

Lockheed Martin - Sikorsky Webpage

The Rotary and Mission Systems segment is primarily built upon the Sikorsky Helicopter Company. The significant portfolio of attack and transport helicopters manufactured by Sikorsky ensure that customers have a large product range to choose from.

This allows Lockheed to embed their helicopters into various military operations thus enabling customers to benefit from type commonality efficiencies (much in the same way airlines benefit from operating one type of aircraft).

By ensuring current customers are enjoying the advantages of operating Sikorsky-based helicopter fleets, Lockheed is able to increase the costs associated with switching to another brand of aircraft.

This significantly increases the odds of current operators choosing to replace and expand fleets with more Sikorskys rather than changing to another manufacturer. Once more, this increases the revenue generation opportunities for Lockheed from this business segment moving into the future.

The Sikorsky range of helicopters are relatively differentiated from their competitors and offer a great range of abilities. However, it can be argued that they struggle to meet the same level of industry domination when compared to that achieved by the F-35.

Lockheed Martin - Marine Group

Another significant element of the business segment is the shipbuilding venture being pursued alongside American shipbuilder Fincantieri Marine Group. Lockheed has chosen to create a strategic business partnership with the shipbuilding firm to ensure capital requirements are used efficient and effectively to reduce product manufacturing and development costs.

Together with Fincantieri, Lockheed manufactures a variety of ships across the combat, frigate and countermeasure categories.

Once more, Lockheed is able to vertically integrate the supply of missiles and armaments to their ships through their extensive naval warfare technologies. The ability Lockheed has in offering customers with a holistic defense package across their business segments is an absolutely crucial element that earns Lockheed the wide-moat rating from The Value Corner.

Finally, Lockheed is currently engaged with the US in the militarization of space , primarily through the development of military satellites and intercontinental ballistic missile programs. Their advanced experience in the field has allowed the firm to become primary suppliers for the US and a number of allied nations such as the UK when it comes to long-range missile systems.

Overall, the incredible diversity, reach and specificity of each of Lockheed's business segments combined with their absolute advantage over the competition in contract negotiations earns Lockheed one of the widest-moats of any firm.

The ability for Lockheed to extract value and generate revenue from their business segments is unparalleled thanks to their devotion to offering customers a holistic and integrated range of military products.

Financial Situation

{kind=link}

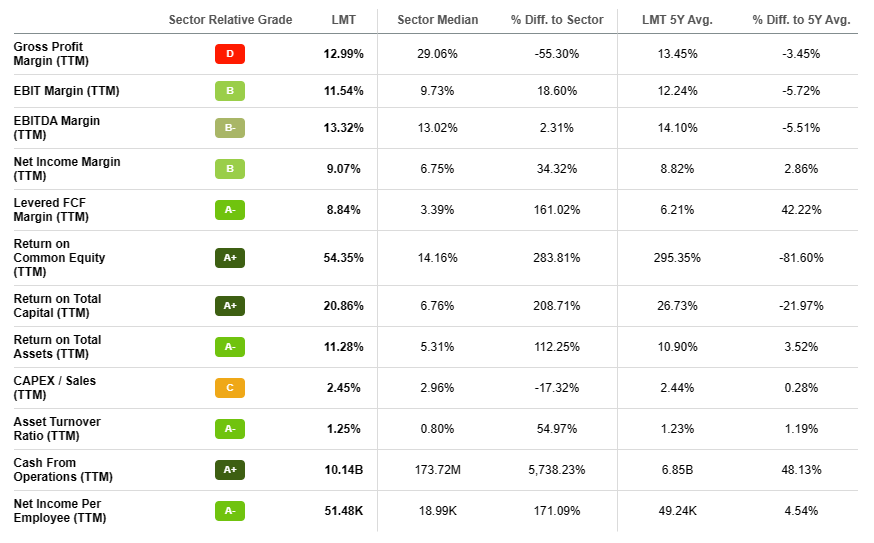

Lockheed Martin has both historically and continues to be a hugely profitable firm. Their consistent EBIT Margins of around 12% combined with a 10Y average ROIC of 38% are just the first indicators of the profit generating prowess the company holds.

Lockheed Martin FY22 Proxy Statement

For FY21, Lockheed Martin saw $67B in net sales with 71% being generated from US Government contracts and 28% from international customers. Only 1% of sales were derived from commercial sources.

Their hugely profitable Aeronautics department continue to lead the charge in revenue generation with Rotary and Mission Systems coming in second place, followed by MFC and Space.

{kind=link}

Net sales in Q3 FY22 were up 4% compared to FY21 figures combing in at $16.6B. Net earnings grew a whopping 200% in the same period. This hugely successful quarter was primarily achieved thanks to a 10% increase in net sales in the Aeronautics department, spurred by the aforementioned contracts for more F-35s.

FY22 MFC sales also increased 2% compared to the same period in FY21, which was primarily due to higher volume demand for their Patriot Advanced Capability-3 ((PAC-3)) missile defense products.

Unfortunately, net sales and profits for the Rotary and Mission Systems segment decreased by 5% and 10% respectively. This was primarily due to lower than anticipated production volumes on their Sikorsky helicopter programs.

Lockheed's Space segment saw net sales increase 7% compared to Q3 FY21 with operating profits also growing 14%. This was primarily attributable to the increased equity earnings from the company's investment in the United Launch Alliance program thanks to higher launch volumes.

These individual segment statistics culminate in consolidated operating profit falling -0.58% compared to the previous year. Essentially, earnings have flatlined since FY21. However, management assures shareholders that this was largely due to the unfavorable timing of various on-going costs and incoming cashflows.

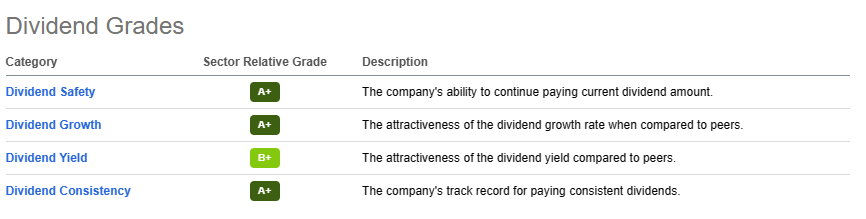

EPS for Q3 beat consensus estimates handily totaling $6.87 per share. This is welcomed news for investors. Furthermore, Lockheed returned $2.1B in cash to shareholders through increased share repurchases in the form of 3.4 million shares and through the payment of a quarterly dividend rate of 7% ($3 per share) totaling $739M.

{kind=link}

Their dividend payments are rated by Seeking Alpha's Quant as A+ which is accurate considering a payout ratio of 41.68% combined with a 5Y growth rate of 8.85%.

{kind=link}

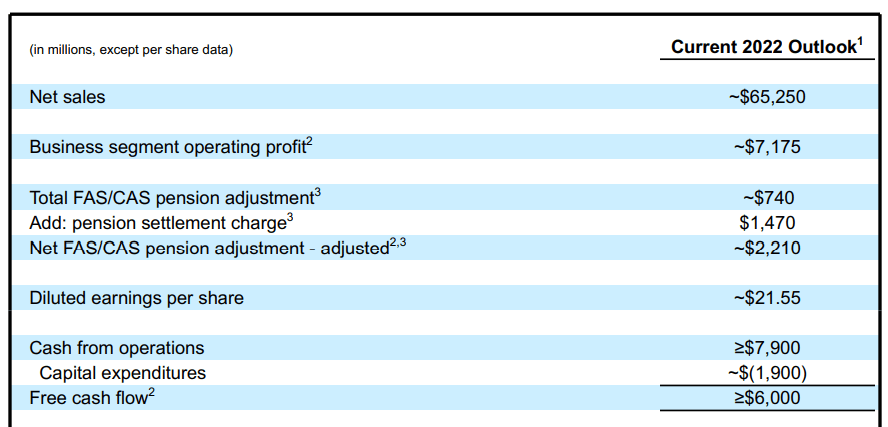

This industry-leading dividend and share buy-back scheme illustrates the overall profitability and health of the company. The firm did no update their current 2022 outlook with sales still estimated to total $65.2B with an EPS of $21.55 and FCF expected at greater than or equal to $6B.

Overall, from a profitability perspective, Lockheed has not managed to generate the same growth in FY22 as they have seen in FY21 or the previous 10 years as a whole. However, their strong backlog of $140B combined with a proven ability to generate huge returns of invested capital and common equity illustrate to me the firm should have a very profitable FY23.

Seeking Alpha - LMT

These stellar fiscal metrics have earned Lockheed with an A+ Profitability rating by Seeking Alpha's Quant in comparison to the industry as a whole. I believe this perfectly sums up their overall profit generation abilities.

It is also pleasantly refreshing to see management rewarding shareholders with healthy dividends and continued share buy-back schemes. Nonetheless, we await the FY22 results to consolidate this year's performance for the firm and to gauge what FY23 holds for the company from a management perspective.

Lockheed's balance sheet looks to be in healthy shape much akin to their income statement. Their total current assets for the TTM are $20.9B while current liabilities only amount to $16.4B.

The firm exhibits a good quick ratio of 1.06 (current assets minus inventory divided by current liabilities). Their current ratio is even more attractive at 1.28 (current assets divided by current liabilities). Furthermore, the firm's debt/equity ratio is 0.96 which illustrates their fiscal stability.

{kind=link}

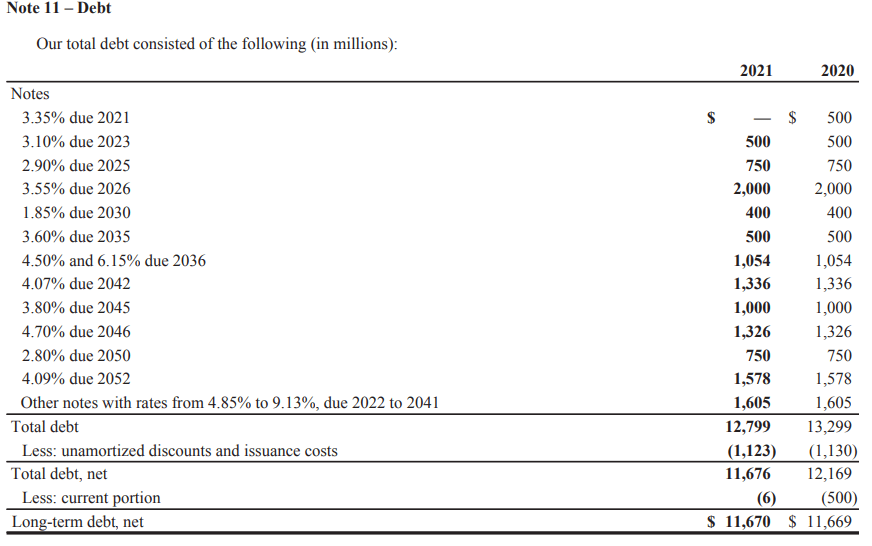

Lockheed has also been very effective at managing their long-term debt keeping their total at around $12B. Management has shown significant levels of fiscal responsibility by ensuring fixed-rates on a majority of their debts. This leave the firm largely immune to the current hike in interest rates which is good news for investors.

In the next 10 years, only around $3.6B in debt will be maturing. This leaves Lockheed in a largely unburdened cash position allowing them to continue investing in crucial next-generation products.

Lockheed exhibits outstanding fiscal stability and is not currently struggling with any major liquidity risks.

Valuation

{kind=link}

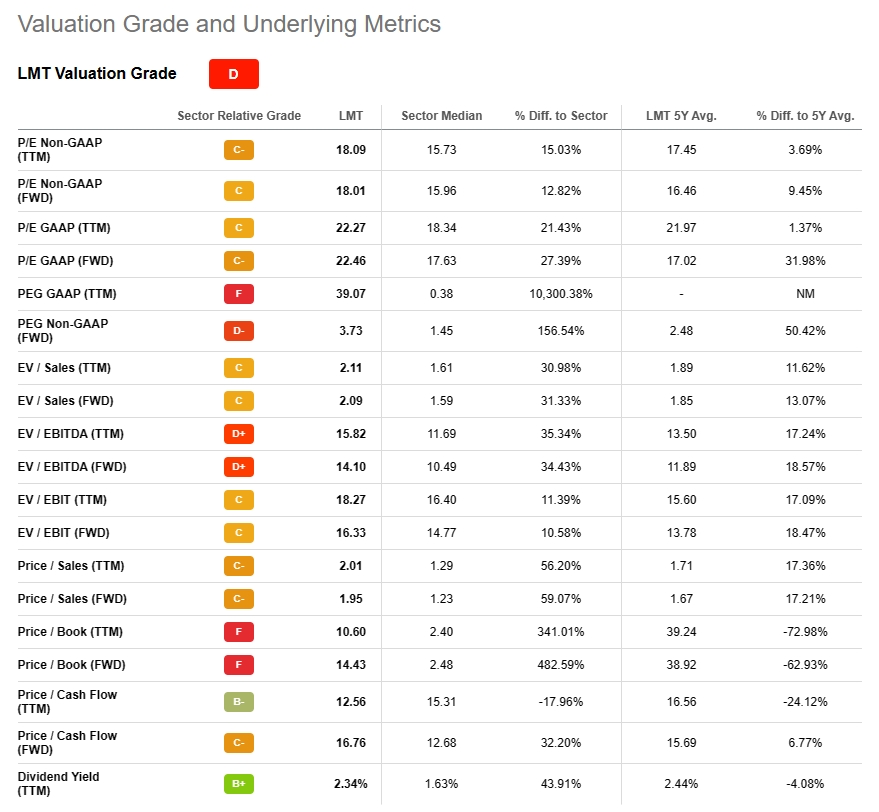

Seeking Alpha's quant system has assigned a D Valuation rating for Lockheed, which I find to be slightly pessimistic. The FWD P/E GAAP of 22.46 is almost 30% greater than that of the sector median. Furthermore, their FWD EV/EBITDA of 14.10 once again exceeds the sector median by over 33%.

These metrics alone suggest the firm is trading at a significant overvaluation compared to their market competitors and their intrinsic value.

However, it must be noted that their Book to Bill ratio is 10.55 indicating significant demand for their products which is supported by the $140B backlog reported by Lockheed's management.

Since a majority of Lockheed's operating performance relies on the budget allowance provided to the US DoD, the expected 10% increase in the US defense budget thanks to the planned Omnibus Package should provide Lockheed with significant future demand for almost all of their products.

Nonetheless, it is important to note that as illustrated by Lockheed's primary valuation metrics and supported by Seeking Alpha's Quant, the firm is currently fairly valued in my opinion.

{kind=link}

In the short term (3-10 months) it is difficult to say exactly what the stock will do. I believe the stock will exhibit some bearish tendencies due to an expected market sell-off after the recent rally the stock has experienced.

In the long-term (2-4 years) I fully expect their position as a leader in the industry to become even stronger. Their unique industry knowledge combined with the potential for significant future growth places little doubt in my mind over the almost undoubtable returns the company should be able to provide to shareholders.

From a pure value perspective, it is essentially impossible to argue for building a position in Lockheed at this moment in time. However, if the expected increased spending on the US military budget occurs, I believe a share price around the $350 could begin to offer investors a margin of safety of approximately 25-30% (considering an intrinsic value of somewhere around the current market price).

Risks Facing Lockheed Martin

The primary risks facing Lockheed Martin arise from the significant reliance on prevailing US political policies regarding defense spending. Considering that around 71% of their revenues rely on the US government, a major decrease in the defense budget would create significant financial concerns for the firm.

However, given the increased prevalence of tensions in Europe due to the Russia-Ukraine conflict combined with rising levels of unrest in Asia, it is widely expected that the prevailing defense spending habits of the US government will lead to increased issuing of contracts for military equipment.

Therefore, I believe that for the foreseeable future (3-6 years) this political threat is relatively inconsequential.

Another potential threat for Lockheed arises from their ESG objectives. Due to Lockheed being a defense contractor, the firm automatically harbors social criticism with activists critiquing the firm and its shareholders as being " war profiteers ".

From an environmental perspective, the firm also contributes significantly towards harmful greenhouse gas emissions with little focus being given towards the sustainability of these operations.

While this ESG risk is quite small, it is important to note the significant portion of younger investors particularly of the Millennial and Gen-Z generations who want their portfolios to maintain a high ESG ranking. In the long-term, this reluctance from investors to invest in companies which illustrate poor sustainability metrics could genuinely begin to harm more controversial companies such as Lockheed.

Finally, as with any firm engaged in the manufacturing of goods or products, there is the possibility of Lockheed failing to execute a bespoke defense program of contract. The struggles faced with the F-35 program which have included almost 10 years total of delays show that not even Lockheed is immune to the occasional stumble.

While such delays and cost overruns are not what shareholders want to see, the possibility of a large-scale program failure, in my opinion, are incredibly remote.

Summary

Lockheed Martin has had an impressive history from an investor standpoint. Their robust business fundamentals, almost monopolistic foothold in the defense market combined with the capital necessary for significant growth has placed the company in an attractive position for potential investors.

While share prices continue to trade at a relative premium to the company's current value, the promise of strong future cashflow generation could mean the stock simply will not drop much below its current levels.

As a short-term investment, I believe there is some volatility in-store for the stock as a market sell-off is expected. However, in the long-term I believe their undeniable position as a market leader places Lockheed in the perfect position for a much-awaited rebound.

I will carefully be watching the stock for the next couple of months and eagerly await to see FY23 forecasts along with the final FY22 results. A weaker FY23 might end-up suiting deep value investors who are looking for a better long-term deal when it comes to Lockheed's shares.

For further details see:

Lockheed Martin: Set For Long-Term Growth