LMT - Lockheed Martin: Still A Buy

Summary

- Lockheed Martin's 2022 sales reflected supply chain and program-specific pressures.

- 2023 will be equally challenging.

- Based on an assessment of TEV/EBITDA, I do see continued upside.

Lockheed Martin ( LMT ) posted its fourth quarter results on the 24th of January before the opening bell. Results exceeded expectations. Nevertheless, I'm considering a downgrade from Buy to Hold for Lockheed Martin stocks. In this report, I explain why.

A Solid Year With Decline

{kind=link}

One major item to wrap your head around is the fact that the demand environment for defense equipment and services is strong, but that's not going to result in increased sales from one day to the other. The evaluation and procurement processes are long with many milestones to be cleared before a sale is recovered or even a purchase agreement is drafted. So, the positive demand environment we see today is not something that translates into sales any time soon. 2024 is in fact the earliest point where defense contractors see this happening. On top of that, driven by some program-specific pressures and global supply chain issues, sales are down year-over-year. So we're seeing down to flat sales while the demand environment is strong.

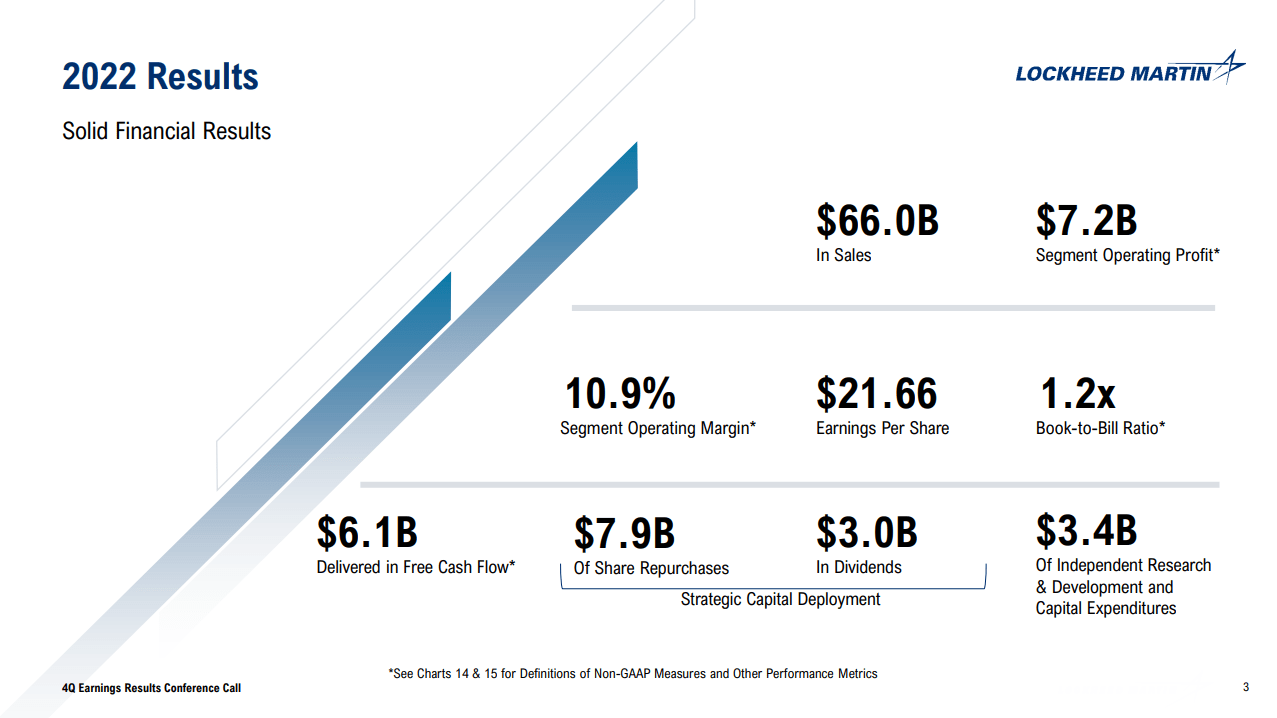

For the full year, Lockheed Martin had guided for $65.25 billion in sales and the company managed to get to $66 billion in sales beating its target and its segment operating profits beat the guidance by $44 million while free cash flow of $6.132 billion met and possibly exceeded expectations of a higher than $6 billion free cash flow.

While overall sales were down year-over-year, Aeronautics sales were up by 1%. This was driven by higher volume on classified programs in the amount of $375 million, higher net favorable adjustments for the F-22 in the amount of $80 million and $55 million for the F-16 program due to higher volume partially offset by volume on sustainment contracts and unfavorable profit adjustments. Aeronautics revenues would have been even stronger if it weren't for the F-35 program to provide a $310 million pressure, primarily driven by lower volume and profit adjustments. Profits for the segment increased by 2% driven by lower unfavorable adjustment on unclassified programs, higher favorable adjustments for the F-22 program but lower results at the F-16 and F-35 programs. All in all, the segment performed quite well given that the F-35 provided a significant pressure on top and bottom line.

For Missile and Fire Control, revenues were down $376 million or 3% for the year, driven by a $280 million in sensor sales decrease and $60 million in lower SNIPER targeting pod volume as well as lower PAC-3 volume. While sales were down 3%, profits were down by only 1% driven by lower favorable adjustments on the PAC-3 program offset.

Rotary and Mission Systems sales declined by 4% driven by timing of training system deliveries, lower production volumes at Sikorsky and lower C6ISR volume. The segment saw profits decline steeper than the revenue decline due to lower Sikorsky sales and lower net favorable adjustments for its helicopters and lower net favorable adjustments on C6ISR programs.

The Space segment saw sales decrease by 2% or $282 million driven by a discontinued program, lower Orion space program sales offset by higher Next Generation Interceptor sales and higher classified sales. Just like with Rotary and Mission Systems, the Space segment saw results decline steeper than sales due to lower net favorable items on national security programs.

Lockheed Martin did not have a bad year, but what was evident was how volumes impact revenues and profits of the programs, rendering the company unable to increase sales due to supply chain issues.

2023: A Flat Year

{kind=link}

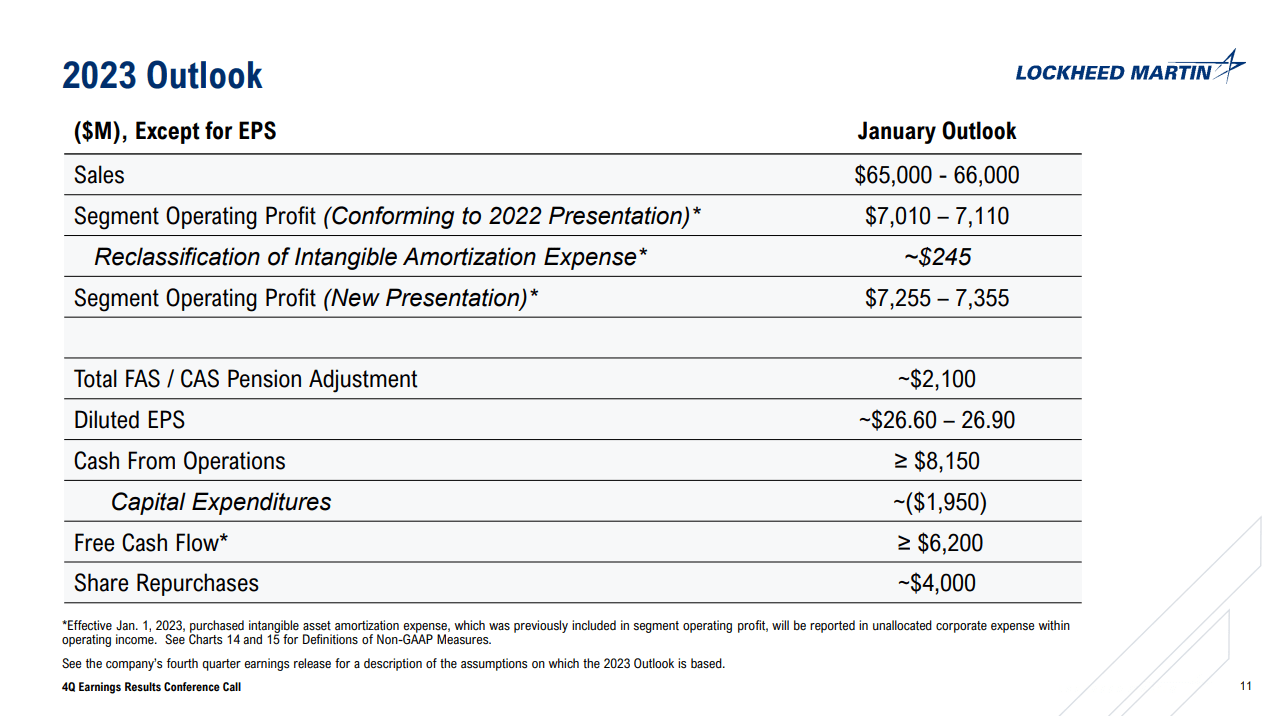

The guidance that Lockheed Martin provided for the year does not come as a surprise. 2023 was seen as a flattish year as the company aims to transition to growth in 2023. The sales outlook of $65 billion to $66 billion shows exactly that. The range of $7,010 million to $7,110 million in segment profits indicates lower profits in 2023. On the positive side, the guidance of >$6.2 billion indicates free cash flow growth.

Roughly $4 billion worth of stock will be repurchased, which should bring down the share count by approximately 9 million shares or 3%. With the current dividend that would indicate that roughly $7.1 billion will be returned to shareholders, exceeding the free cash flow. Returning more to shareholders than generated free cash flow is not something I'm particularly impressed with. The EPS will be in the $26.60 to $26.90 range, which will be down from $27.23 in 2022. So, what we are seeing is that the decline in segment earnings cannot be offset by the current share repurchase plans. The dividend and repurchase yield is around 6.1% which I think is quite nice for shareholders. Consolidated earnings are expected to be roughly flat or around $100 million up year-over-year.

Is Lockheed Martin Stock A Buy?

| Valuation Lockheed Martin |

| Market Capitalization ($ bn) |

| $117.3 |

| Total debt ($ bn) |

| $15.4 |

| Cash and equivalents ($ bn) |

| $2.5 |

| Total Enterprise Value ($ bn) |

| $130.2 |

| EBITDA 2023 ($ bn) |

| $9.8 |

| TEV/EBITDA (2023) |

| 13.3x |

| Current share price |

| $447.53 |

| Undiscounted price target |

| $508.75 |

| Upside |

| 14% |

When I started analyzing the results and writing this report, I expected that I would be downgrading Lockheed Martin from Buy to Hold, driven by flattish results in 2023. However, after considering the total enterprise value coupled with the EBITDA of $9.8 billion that I expect at the midpoint for 2023, a 13.3x TEV/EBITDA is obtained. Using a 15.1x multiple as was the case for Q4 2022 I get to a price target of $508.75 indicating 14% upside excluding share repurchase and $526 including share repurchases. If we were to discount the price excluding share repurchases, I get to a share price of $466.75 which is the price that I believe that shares should be trading at now.

Conclusion: A Tough Environment With Opportunities

Looking at all parts of the picture, Lockheed Martin is in an interesting position. Much of its EPS growth last year was realized by means of share repurchases as supply chain issues and program-specific pressures had an impact on results. At the same time, demand for defense equipment is high but will not quite materialize until 2024 and beyond. So, we do see the opportunity despite a tough year in 2022 and likely an equally tough year for 2023. Either way, we see continued shareholder returns and free cash flow growth, and based on an assessment of the EV/EBITDA multiple, I continue to see an upside that does not yet include higher defense equipment demand translating into sales.

For further details see:

Lockheed Martin: Still A Buy