LMT - Lockheed Martin Stock: New All-Time Highs Are Fully Warranted

2023-04-18 15:41:08 ET

Summary

- In this article, I start with a discussion of fading supply chain challenges and the 2024 defense budget request.

- Lockheed Martin Corporation, which just reported Q1 earnings, is in a great spot to benefit from accelerated defense spending in targeted areas like space, aeronautics, and missile defense.

- Lockheed Martin beat earnings estimates, issued strong guidance, and sees both lingering supply chain issues and rebounding orders down the road.

- Even though LMT stock has broken out, I believe that shares have more room to run, thanks to improving macroeconomic conditions and an attractive valuation.

Introduction

Lockheed Martin Corporation ( LMT ) is my single-largest investment. It has a weighting of more than 8% in my dividend growth portfolio, as I used every major opportunity since 2020 to buy shares. The only reason why I was able to buy LMT shares at attractive prices in 2020/2021 is that the company (and its peers) struggled with severe post-pandemic supply chain issues and budget uncertainties. It kept most major defense stocks from breaking out. That changed in 2022, when the war in Ukraine unleashed the realization that the defense capabilities of NATO nations are, in fact, not where they should be.

Now, Lockheed Martin Corporation is back to normal. Supply chain issues have eased, defense demand remains high, and valuations are still attractive.

In this article, we'll discuss all of this, using the bigger picture and the company's just-released earnings.

So, let's get to it!

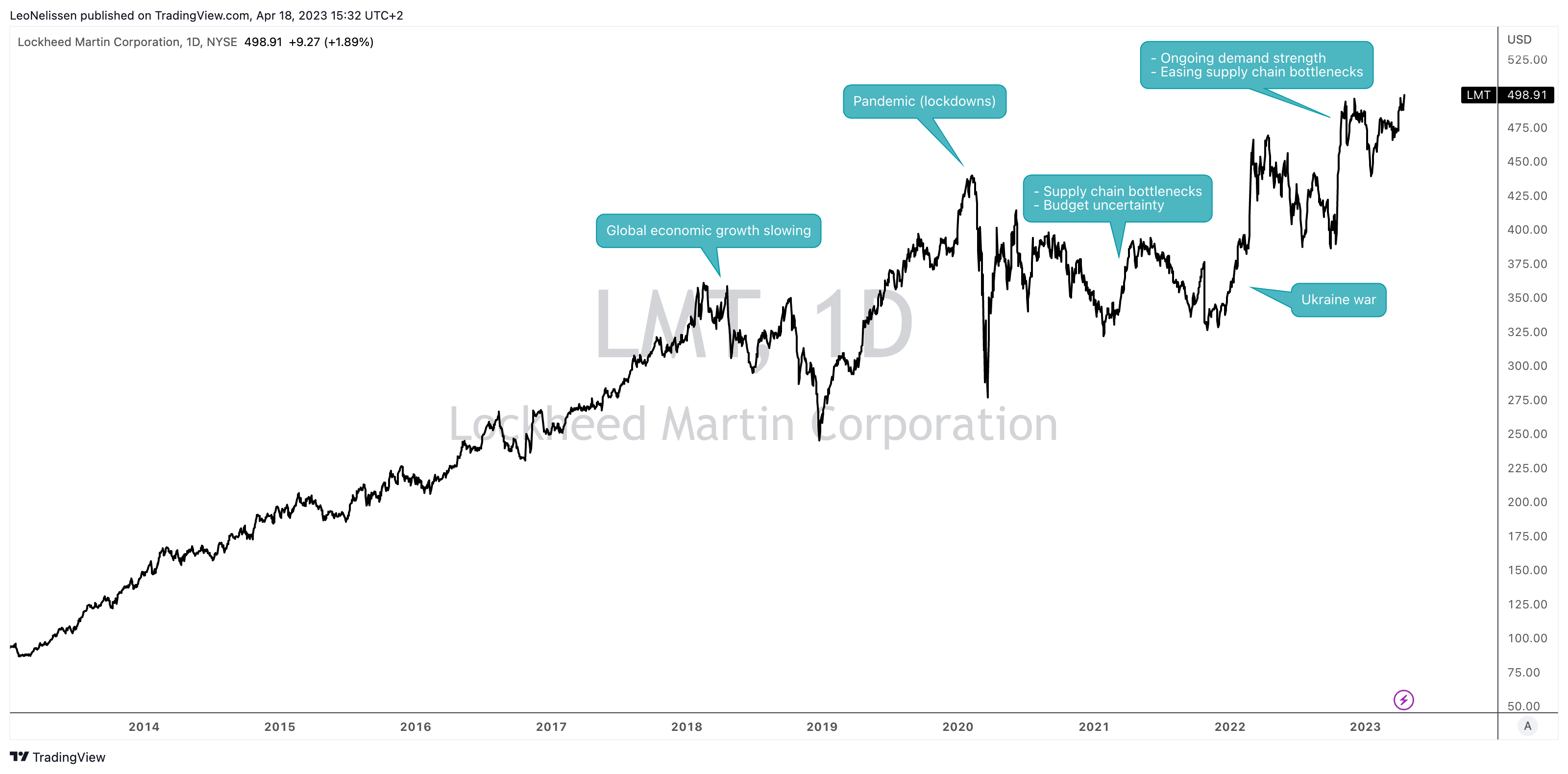

A Few Volatile Years

Lockheed Martin investors have been through a number of rallies and sell-offs in the past few years.

The smooth uptrend after the Great Financial Crisis ended in 2018 when global growth started to weaken. Back then, it was amplified by the trade war with China, which caused some stock market volatility. Once stocks had a nice rally going again, the world was shaken by global pandemic-related lockdowns. It caused a steep stock market selloff. While the S&P 500 (SP500) quickly recovered from that slump, Lockheed Martin did not. In fact, it had two major downtrends before finally recovering in 2022. These selloffs were caused by significant supply chain issues that made it impossible for labor and material-intensive defense giants to protect margins. They were not able to turn their backlog into finished sales, at least not at the pace they were used to.

TradingView (LMT)

{kind=link}

Unfortunately, what ended this volatile sideways trend was the horrible war in Ukraine, which confronted NATO nations with the bitter truth that years of under-spending resulted in an abysmal state of defense capabilities.

Back then, the uptrend was amplified by China pressuring Taiwan and increasing defense spending in the APAC region.

Now, LTM is benefiting from both higher demand and easing supply chain issues.

Budget & Supply Benefits

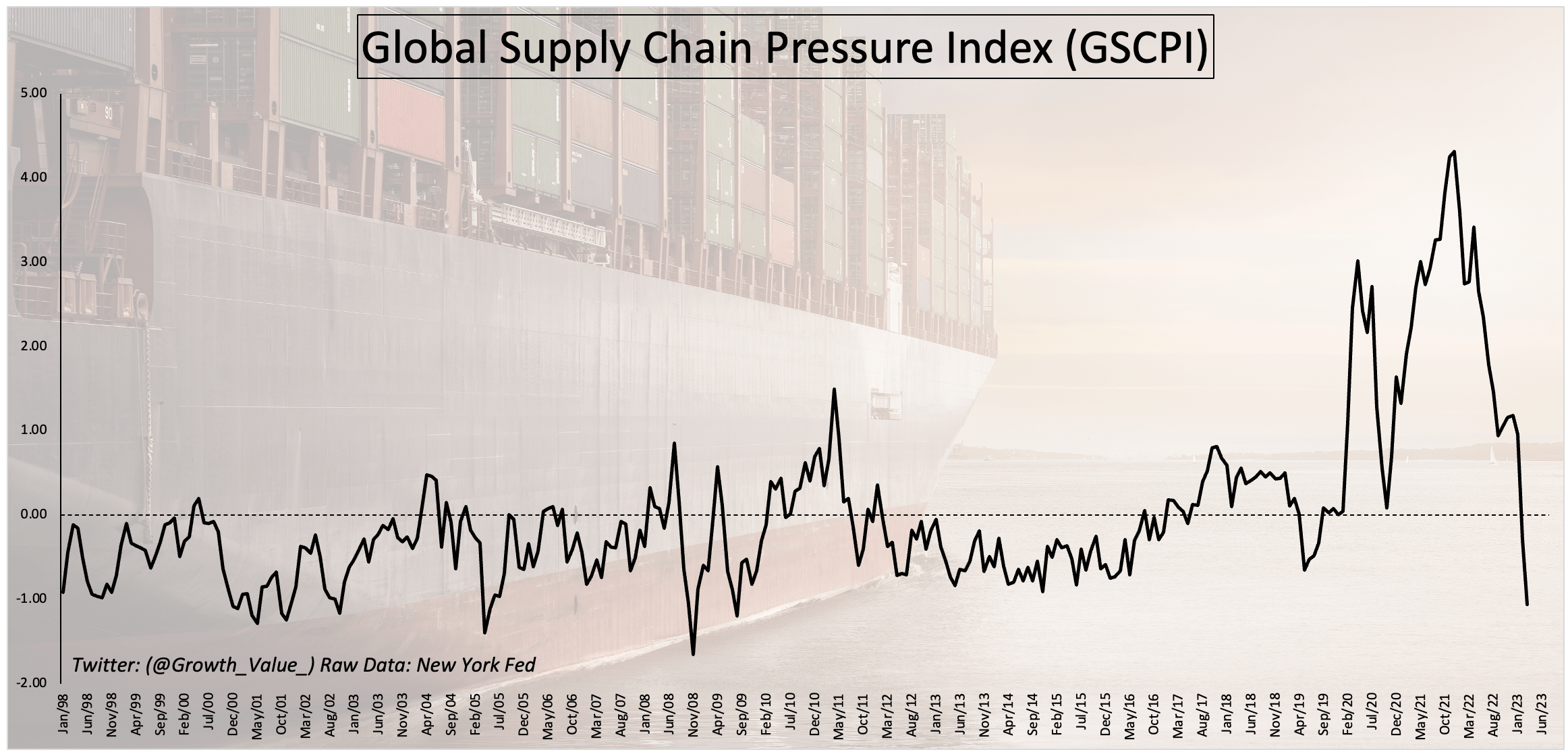

Before we dive into Lockheed's earnings, let me give you some background info, starting with the supply chain situation.

The Global Supply Chain Pressure Index below incorporates a wide range of data, including transportation costs (water, air, and land) and results from various purchasing manager surveys.

After an unprecedented surge in 2020 and 2021, indicating severe pressure on supply chains, the index is now at a multi-year low, as I expect that a large part of this decline is caused by demand destruction.

{kind=link}

In other words, not only have producers adjusted their production, but they also experience fewer orders as a result of the ongoing decline in global growth expectations.

While this is bad for the global economy, it's very good for defense companies for two major reasons (most people forget reason 2):

- It's easy to obtain much-needed (often high-tech) materials to turn backlog into revenue.

- Slowing economic growth is hurting cyclical companies, which lowers competition for certain supplies. After all, companies like Lockheed Martin have close to zero commercial exposure.

Furthermore, the defense budget is now a tailwind.

As reported by Defense One , the Biden administration has submitted a defense budget request ("PBR") to Congress that defense officials are calling the "largest, nominal-dollar peacetime budget ever" for the Pentagon.

The request includes $842 billion for the Pentagon. The total is $886 billion, including the Energy Department's nuclear weapons work and other federal projects.

Furthermore, it includes record-breaking funding for some key areas related to Lockheed Martin's capabilities, like weapons procurement, research and development spending, and space-related activities.

Here are some takeaways from the budget:

() The request is $25 billion more—roughly 3 percent higher, not counting inflation—than the $816 billion Congress appropriated for 2023.

() The Pentagon is seeking lawmakers’ approval to sign multiyear procurement deals for five types of missiles: Naval Strike Missile, SM-6, AMRAAM, JASSM-ER, and LRASM.

() The request includes $145 billion for research-and-development projects, the most ever.

() The budget request includes $29.8 billion for missile defense; $11 billion for hypersonic weapons and other long-range missiles; $13.5 billion for cyber activities; $1.8 billion for artificial intelligence-related efforts; and $1.4 billion joint all-domain command-and-control projects.

Lockheed Martin Confirms The Bull Case

With all of this in mind, let's dive into the company's results and comments.

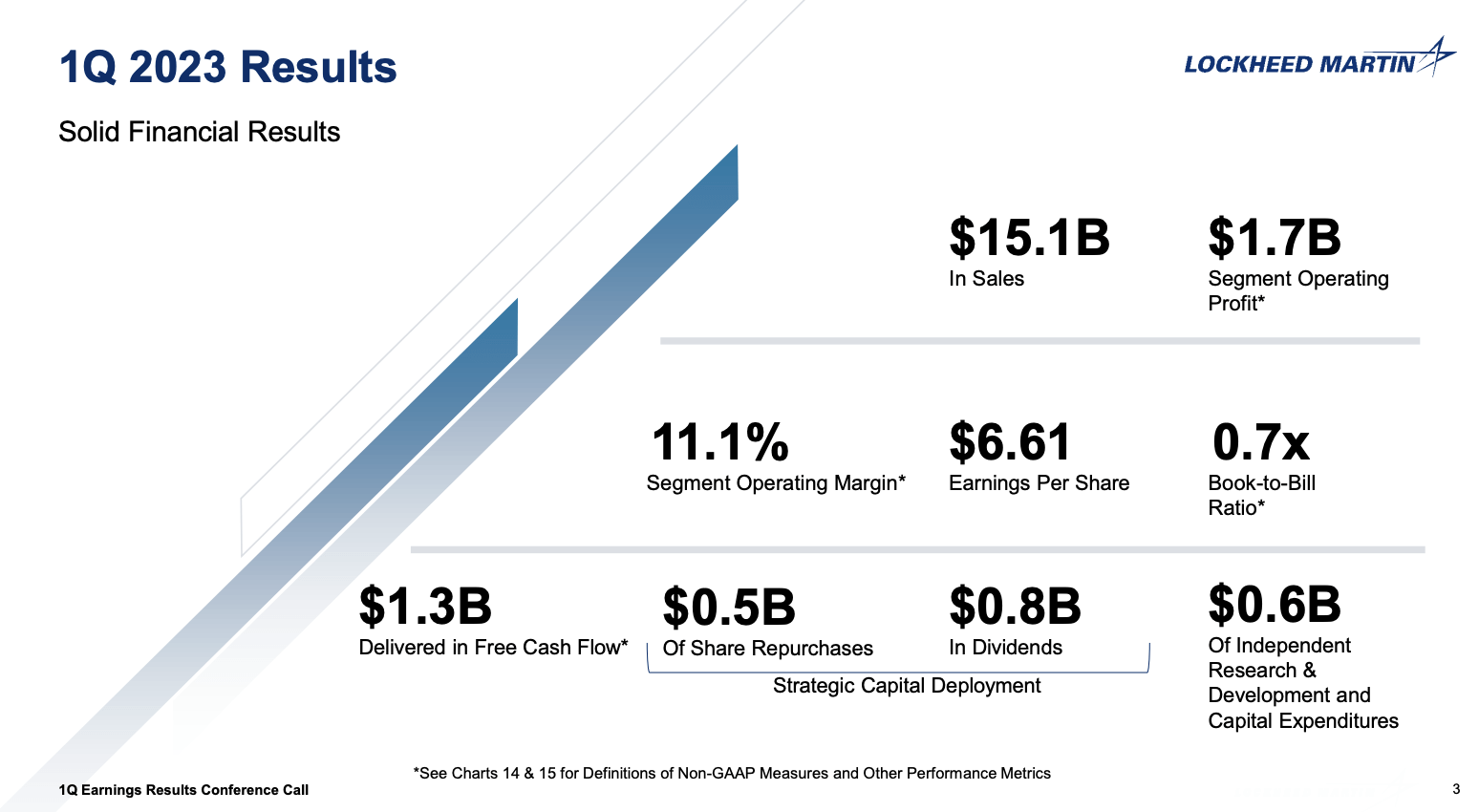

In its first quarter, Lockheed Martin generated $15.1 billion in revenue, an increase of 0.9% versus the prior-year quarter. The company reported $6.43 in adjusted EPS (adjusted for, i.e., pension items). This number beat estimates by $0.37. It's unchanged versus its 1Q22 result, as shown by the handy chart below.

Seeking Alpha

While it doesn't matter too much, the company has beaten earnings in three consecutive quarters.

Seeking Alpha

Here's a sales breakdown per segment:

- Aeronautics (-2%) saw lower F-35 production numbers, higher F-16 sales, and higher sales of classified products.

- Missiles and Fire Control (-3%) benefited air and missile defense sales, which was offset by weakness in sensors, global sustainment, and actively strike missiles.

- Rotary and Mission Systems (-1%) benefited from a higher volume of integrated warfare systems and sensors. Lower Black Hawk volumes and C6ISR weakness offset these benefits.

- Space (+16%) benefitted from higher volumes across the board, including classified programs, Orion, communication, and ballistic missile programs.

In the quarter, the company generated $1.3 billion in free cash flow. All of this was distributed through dividends and share buybacks.

{kind=link}

With all of this in mind, Lockheed Martin's CEO, James D. Taiclet, started the 1Q 2023 earnings call with highlights from the quarter and an overview of the PBR, which I just discussed using Defense One comments and numbers.

The threats posed by China and the Russian invasion of Ukraine have increased demand for Lockheed Martin's advanced solutions. Key highlights from the PBR included the procurement of 83 F-35 aircraft, continued expansion in classified programs, and higher funding for munitions.

Furthermore, the PBR also included investments in key technology development efforts, such as conventional prompt strikes, long-range hypersonic weapons, next-generation interceptors, hypersonic defense, and other space programs. Lockheed Martin's investment priorities, including microelectronics, 5G technologies, and joint all-domain operations, also received increased funding.

Regarding the F-35, Lockheed's largest program, there are tailwinds and headwinds. Tailwinds include strong orders, including 88 units for the Canadian armed forces. However, Lockheed expects a potential impact on deliveries later in the year due to software maturation related to technology refresh-3 and hardware delivery timing. However, this is not expected to have an impact on revenues.

Taiclet also mentioned achievements in other programs, such as the first Greenville-built F-16 Block 70 delivered to Bahrain and additional orders from Jordan and Bulgaria for F-16 jets. As I briefly discussed, strong F-16 sales offset some headwinds in the F-35 program.

Moreover, you may have noticed in the PowerPoint slide above that the company has a book-to-bill ratio below 1.0, which indicates that production is faster than the flow of new orders.

When asked about the book-to-bill ratio needed for the company to resume growth in 2024, Lockheed Martin's CFO, Jesus Malave, stated that the target is around 1. Last year, the backlog was at $150 billion, and this year the company is planning for it to be similar, possibly down or up by $1 billion. A book-to-bill ratio of 1 sets the company up for growth resumption in 2024. While there is potential for the backlog to grow, the current plan is for it to be relatively flat, aligning with the company's strategy for driving growth in 2024.

Based on everything said so far, the company's guidance was strong.

- In 2023, it sees net sales between $65 and $66 billion. Analysts expected $65.7 billion. Diluted EPS is expected to come in between $26.60 and $26.90. Analysts were looking for $26.71.

- Free cash flow is expected to come in at $6.2 billion, which implies a free cash flow yield of 4.8%.

These numbers allowed the company common stock to hit a new all-time high.

FINVIZ

With that in mind, Lockheed also commented on supply chains. Going into the earnings call, I expected the company to say some positive things, as it was able to report strong guidance. In both 2021 and 2022, weak guidance was often caused by worse-than-expected supply headwinds.

CFO Jay Malave acknowledged that there had been some challenges in the supply chain, particularly at MFC and RMS, which have had lingering issues impacting on-time delivery performance. These challenges were expected as the company had reset expectations in the second quarter of 2022, and they do not anticipate significant improvement until the end of 2023 or going into 2024. In other words, while supply chain issues are fading, there seem to be some issues in high-tech defense. The good news is that this was expected.

To mitigate some of these issues, the company is implementing best practices in supply chain management by aggregating demand across all business units and programs, synchronizing requirements, and making bulk buys from raw materials to mid-stage components.

LMT Stock Valuation

With everything said so far, one might make the case that LMT shares aren't cheap. That is true. We're not dealing with deep value. However, the breakout is fully justified. The company is trading at 14x NTM EBITDA and an implied free cash flow yield of slightly less than 5%. Even better is that new orders are expected to accelerate.

Furthermore, after 2023, the company is in a good spot to benefit from a complete supply chain normalization, which will further fuel EBITDA. So, unless budget talks fail completely or the company runs into issues that would prevent it from turning its backlog into sales, I believe that the company has room to run to $550 without being anywhere close to overvalued.

This brings me to my takeaway.

Takeaway

The past two years weren't easy. However, I feel validated that I bet on the right horse. Lockheed Martin Corporation is back. Orders are accelerating, the new defense budget is perfectly aimed at supporting the products and services it offers, and supply chain issues are expected to be completely gone going into 2024.

After breaking out, I believe that LMT shares have more room to run. The valuation remains attractive, and free cash flow generation should pick up quite significantly in the years ahead.

Unless the company encounters new structural issues that could endanger its guidance, I'm convinced that Lockheed Martin Corporation is now in a much better environment, allowing its stock to start a meaningful new uptrend with much lower volatility.

For further details see:

Lockheed Martin Stock: New All-Time Highs Are Fully Warranted