LMT - Lockheed Martin Stock Surges After Earnings

Summary

- Lockheed Martin beat expectations on earnings per share, but missed on revenues.

- 2023 will be flat, return to growth to 2024.

- Share repurchase authorization boosted stock performance.

- Authorization of spending another $4 billion by year-end is not prudent.

- Additional share repurchases are a pacifier for shareholders as they will see little to no growth in 2023.

Shares of Lockheed Martin (LMT) posted their biggest gain in 2.5 years following the release of Q3 earnings. In this report, I will analyze the results to see what there was to like about the earnings and guidance, but I will also address what there was to dislike about earnings.

Lockheed Martin Beats Expectations

{kind=link}

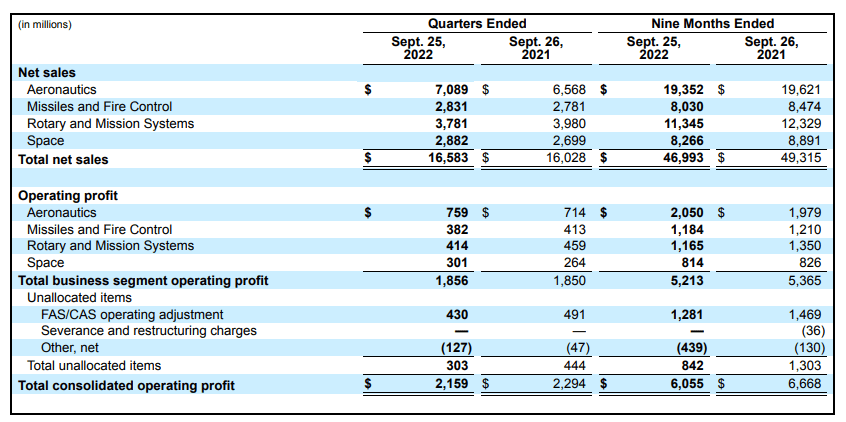

So first and foremost, Lockheed Martin posted earnings per share of $6.87, beating the analyst estimates by $0.15, but its revenue of $16.58 billion missed estimates by $100.26 million. With the exception of Rotary and Mission Systems, revenues were up in all segments resulting in a 3.5% year-over-year increase in revenues, but revenues are still 4.7% lower when looking at the nine-months ended numbers. So, Lockheed Martin closed the gap a bit but is still trailing last year’s numbers.

Aeronautics was the best performing segment for Lockheed Martin, booking an 8% increase in revenues. This was driven by revenue recognition timing as $425 million in F-35 slipped from Q2 2022 into Q3 2022. Profit margins contracted slightly from 10.9% to 10.7% as negative adjustments of $25 million and $40 million lower operating profits on classified programs outpaced $70 million in higher operating profit for the F-35 program and $15 million favorable net adjustments for the F-22 program. Overall, we do see the positive impact the Lot 15 agreement has on Lockheed Martin’s revenues and profits.

Mission and Fire Control saw revenues increase by $50 million or 2% driven by a sales increase of $95 million for integrated air and missile defense programs due to higher PAC-3 missile volumes. This was partially offset by $55 million in lower sales for sensors and sustainment driven by the elimination of the Warrior sustainment program. While sales were up, profits actually decreased with margins dropping from ~15% to 13.5% driven by lower net favorable adjustments for PAC-3, unfavorable adjustments for the Advanced Radar Threat System and $10 million for higher sensor and sustainment profits, partially offset by absence of unfavorable adjustments on an energy program. So, what we are seeing is that specific programs are leading to increased sales, but overall program specific profit adjustments are decreasing the profits either way.

Rotary and Mission Systems was the only segment that saw its revenue decline, in total by $199 million or 5%, driven by lower Black Hawk volume accounting for 80% of the drop. Profits decreased by $45 million or 10% due to lower favorable adjustments and Black Hawk volume, offset by absence of unfavorable items on a ground-based radar program in the current quarter.

On Space, revenue increased by 7% or $183 million which is not completely unexpected as Space is considered a growth area for Lockheed Martin, with Next Generation Interceptor revenues pulling the cart for revenue growth, accounting for $155 million in increase sales. The margins expanded from 9.8% to 10.4% based on higher equity earnings from United Launch Alliance, which was already signaled last quarter.

{kind=link}

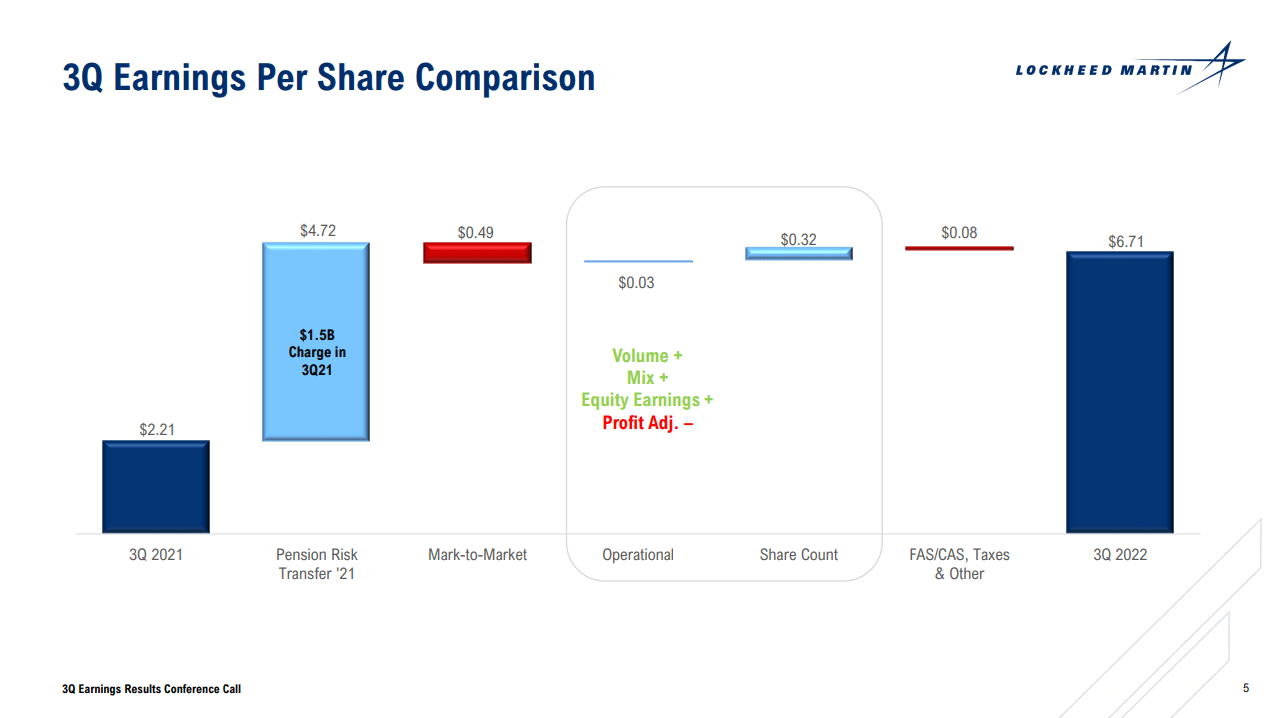

What I found interesting is that bridge from the Q3 2021 adjusted EPS of $6.44 to $6.71 in Q3 2022. 10% of that growth is driven by operational performance and 90% of it is driven by share count reductions. That is not necessarily bad, but EPS growth is apparently driven by the company buying back its shares and not so much by operational volumes, mix and efficiency improving.

Lockheed Martin Guidance Shows Tough Transition Point

{kind=link}

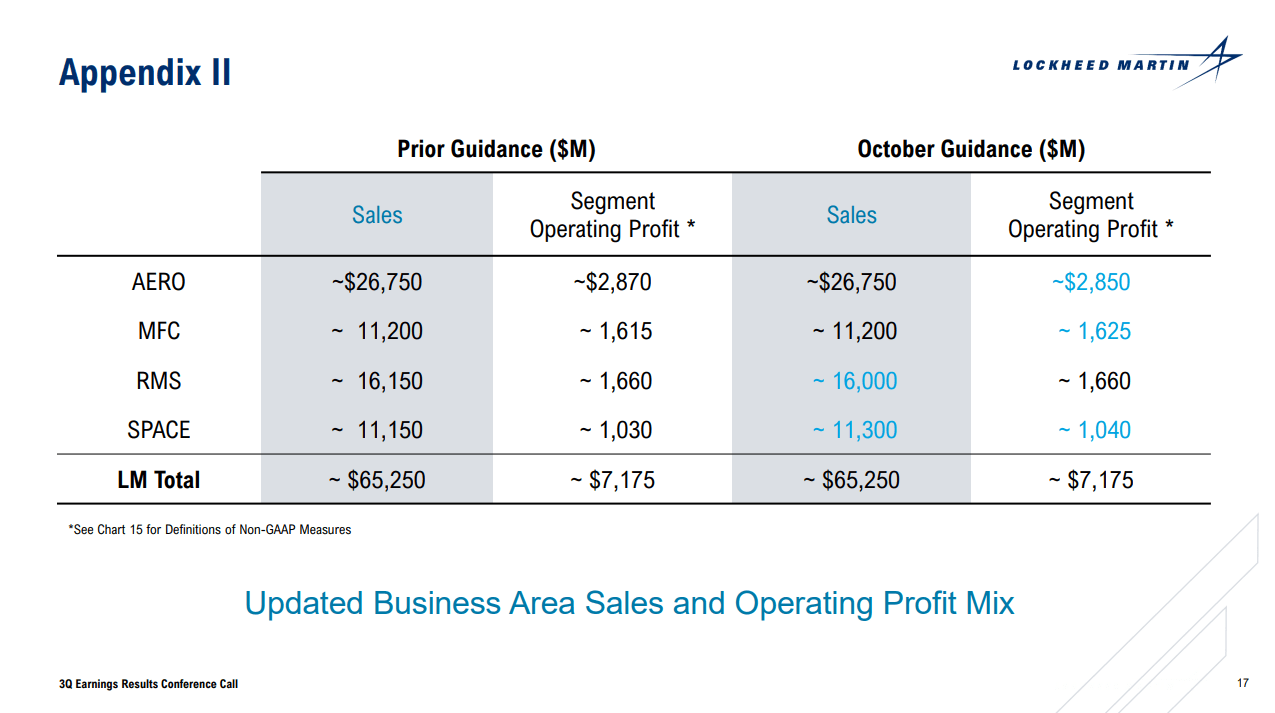

While results were certainly not bad, it is not so much the results or the operational guidance that gave a boost to the share prices today. Lockheed Martin is keeping its operational guidance constant for the year - up $150 million on Space but down by the same amount for Rotary and Mission Systems, and similar on profits we see Aeronautics going down by $20 million, Mission and Fire Control and Space go up by $10 million each. So, small moving items, but the complete picture remains the same.

{kind=link}

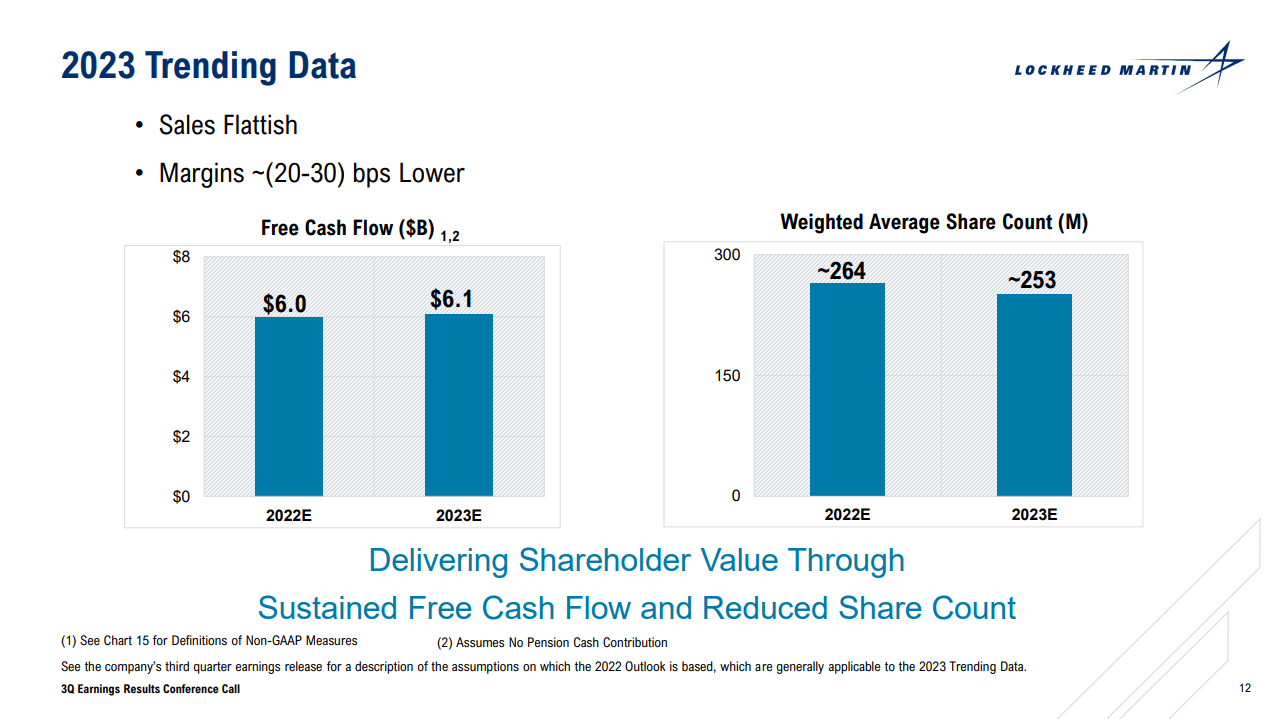

Data for 2023 hardly looks impressive either, sales will be flattish with free cash flow up slightly. I think what we are seeing here is why Lockheed Martin said it would assess its 5-year plan last year. What hurt Lockheed Martin is the fact that F-35 will stick to 156 deliveries annually for the foreseeable future and next year its volumes will be down which really takes away some of the revenue and profit potential that would normally be offsetting reductions on programs that are winding down such as Space-Based Infrared System and Next Gen OPIR both of which are some space wind-downs. Then the F-35 will be burning off some of the F-35 sales that were previously recognized on higher volume expectations that as part of long-lead items had already found their way into sales in 2021 and 2022. In 2023, classified program ramp-up and Next Generation Interceptor ramp-up as well as F-35 sustainment are not going to be offsetting those wind-downs and lower volume and catch up for the F-35.

However, 2024 should be better and that is as the ramp for classified program sales continues, Next Generation Interceptor and the CH-53K helicopter entering the production rate phase while there are hopes for F-35 production to increase again. So, 2023 basically is flat because of the F-35 fallout that results in program wind downs no longer being “more than offset”, but in 2024, the ramps are stronger and 2024 is also where the increased air missile defense product sales due to the situation in Ukraine and Taiwan come into the picture. Northrop Grumman (NOC) previously also saw 2024 as a year where the changed geopolitical and budget environment could start translating into sales. So, putting it all together, a year ago Lockheed Martin already saw where this was heading and opted for a review on its five-year plan, but it is now enjoying some positive tailwinds from the situations in Ukraine and Taiwan that will help the company from 2024 onward, just not in 2023 it is too early for that.

Lockheed Martin Stock Jumps On Repurchase Authorization

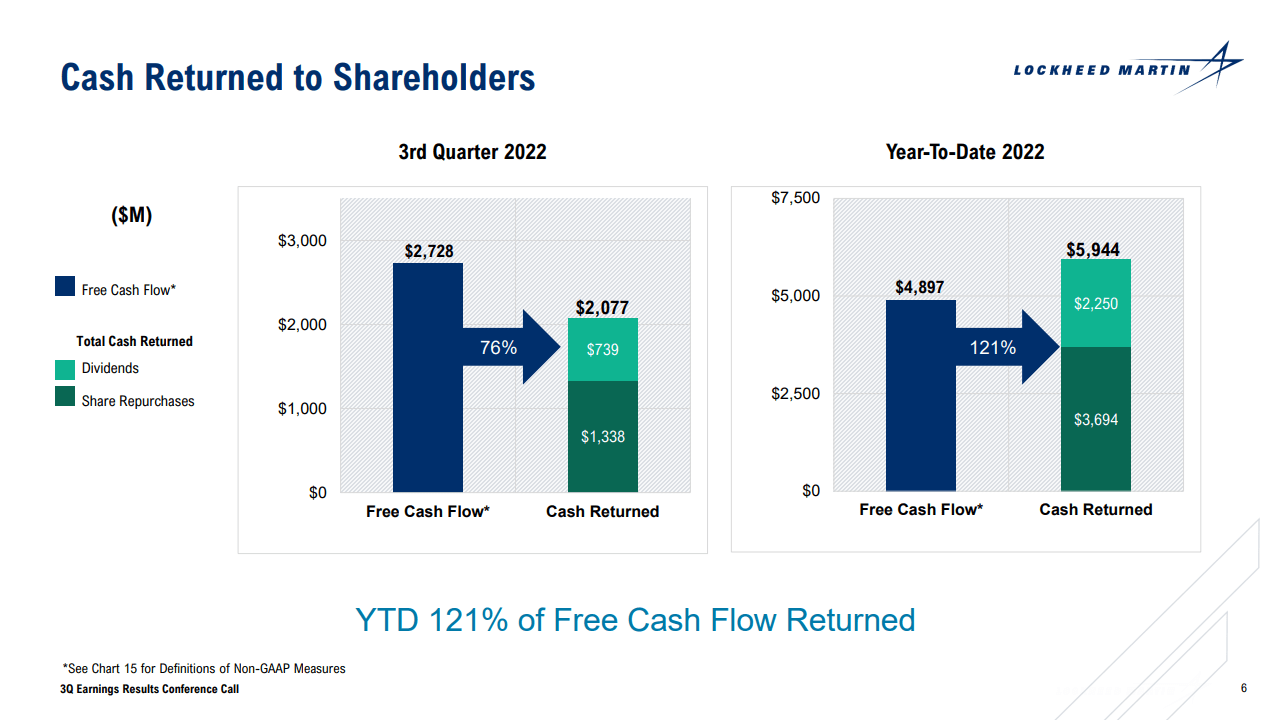

What really put a booster on share prices for Lockheed Martin is the expansion of the share repurchase plans for this year by $4 billion to $8 billion. Prior to the earnings release, shares of Lockheed Martin were trading at $397.31. With the $4 billion hike plus the $306 million that was initially to be spent on share repurchases, 4% of the outstanding shares could be rebought. In total, $14 billion in share repurchases were authorized of which $4 billion were to happen this year, $4 billion in 2023, $4 billion in 2024 and $2 billion in 2025. What the current share price increase of 8.7% mostly reflects is the planned repurchases for this year and next year that would provide opportunity for Lockheed Martin to buy back 7.9% of its stock. The remaining 0.8% gain comes from the EPS beat I would say, and this shouldn’t really come as a surprise as we previously saw that EPS growth was 90% driven by share repurchases and for just 10% by the results. Today’s share price action reflects exactly that. Obviously, with prices jumping, it means that less stock can be repurchased, but the market has decided to pull forward the effect of the repurchase program.

Lockheed Martin Should Not Have Hiked The Share Repurchase Authorization

{kind=link}

Now the big question is. Should Lockheed Martin have done this, and to be frank, I don’t think they should have done it. I am not a shareholder of Lockheed Martin due to local restrictions of my broker, but if I were a shareholder, I would be happy, as an analyst… not so much. Lockheed Martin currently has cash and cash equivalents of $2.4 billion. Its free cash flow in Q4 should come in at $1.1 billion and around $800 million will be paid in dividends. So, the $4 billion that Lockheed Martin will spend the remainder of the year on repurchases means that it will pay out more than it will generate. In fact, the $4.3 billion that exceeds accounts for 70% of the 2023 free cash flow, and right now Lockheed Martin does not have the cash, so the company will borrow the money to pay it to shareholders. I think that is hardly stellar decision-making and I believe the reason they do it is because 2023 will be somewhat flattish and this is the way to keep shareholders happy and be able to hike dividends next year again, but I hardly find it a wise decision. The way it looks, Lockheed Martin will be returning over 180% of its free cash flow to shareholders and that reminds me of a certain company (Boeing (BA)) that spent all of its cash flow on shareholder returns, eventually getting crushed by tens of billions of dollars in debts as things fell apart for the company. Now, I am not saying that things are falling apart for Lockheed Martin, but spending all your cash flow on shareholders, especially in the form of share repurchases, does not seem the most prudent thing to do to me especially since this is the same company that sees 2023 being flattish and a year ago was on the verge of evaluating its 5-year plan.

Conclusion: Buy Rating On Lockheed Martin Performs For Shareholders

Shares of Lockheed Martin have advanced by 7% since the last time I wrote a report covering the company’s dividend hike. The Buy rating I had on the stock is so far working well and it seems that Lockheed Martin will continue returning value to shareholders. However, while I do believe results were good, I think Lockheed Martin is getting ahead of itself with the increased repurchase authorization while we see flattish free cash flow in 2023 and might see continued supply chain challenges as well as potentially budgetary constraints.

I do believe that missile defense and international F-35 sales will be significant for Lockheed Martin in the years to come and provide a nice base for investment in the Defense giant. However, I don’t feel the repurchase authorization of $4 billion in the fourth quarter is a prudent action. It does seem like a pacifier for shareholders for a flattish 2023 outlook.

For further details see:

Lockheed Martin Stock Surges After Earnings