LMT - Lockheed Martin: Western Fiscal Realities May Sink Hopes Of Higher Defense Spending

Summary

- With the Ukraine conflict still in full force and growing noise about a war over Taiwan, arms manufacturers like Lockheed Martin are seeing a great deal of bullish investor interest.

- There is another side to the equation of geopolitical frictions, namely the resulting decline in Western World living standards, with countries like Germany seeing real household incomes plunge by 4.1%.

- With worsening living standards, as well as other issues, such as excessive government debt, and other spending demands, defense spending is likely to be slashed rather than increased.

- Lockheed Martin is enjoying a significant influx of orders from around the Western World at the moment, but some of them may end up canceled, even if there are fees involved.

- Western military acquisitions planning may switch to more efficient spending, as inevitable questions will be asked about NATO running low on certain supplies a year into supplying Ukraine's war effort, despite over $1 Trillion/year in spending.

Investment thesis: With the ongoing Ukraine conflict and rising tensions with China arms manufacturers such as Lockheed Martin ( LMT ) are seen as obvious beneficiaries from what is seen as a period of rising defense spending as a response to the challenges before us. These expectations are bolstered by governments themselves making plans, finalizing contracts, and making public statements about the need to bolster the military. On the other side of the equation, however, there is growing public discontent with declining living standards, even as governments are starting to feel fiscally squeezed by rising interest rates.

There are competing calls to spend more on climate change, infrastructure, and R&D in order to maintain economic competitiveness, and counter China's growing economic dominance in the developing world, and so on. My thesis is that once global geopolitical tensions will cool, Western governments will mostly reverse defense spending plans, in some cases even going as far as canceling existing contracts. In the face of all other competing needs, defense spending will lose out in the absence of an immediate geopolitical stimulant meant to convince the public of the dire need to increase military budgets.

Lockheed saw a decline in revenues and earnings in 2022 compared with the previous year

There is arguably a lag effect before arms manufacturers will start to see improved revenues and earnings from higher demand for military hardware. It takes years for the increased demand to translate from government assessments and resulting plans that translate into contracts, and then final deliveries and full reimbursement for the equipment and services provided. It may explain why Lockheed did not see an increase in revenues & profits, even as NATO members poured tens of billions of dollars worth of equipment into Ukraine, while also announcing plans to beef up their own militaries.

Lockheed's full-year results actually showed a 9% decline in net earnings, from $6.3 billion in 2021 to $5.7 billion in 2022. Revenues declined from $67 billion in 2021, to just under $66 billion in 2022, meaning that profit margins also declined, given that revenues declined by only 1.5%. Interestingly, Lockheed does not see an improvement in revenues for this year compared with last year, with its estimate being between $65 billion and $66 billion.

An item of interest in Lockheed's 2023 outlook is an estimate of $840 million in interest expenses, which comes out to 1.3% of expected revenues. For a company that often has to spend significantly upfront on R&D and other capital costs before seeing revenue inflows from sales, it is not a bad debt-servicing situation by any means. I tend to get worried about most companies that spend up to or above 5% of revenues. it usually means that debt servicing costs are starting to suffocate the company.

The one detail that should be a reason for investors to be bullish for the long term is the growing backlog of orders.

{kind=link}

It is in large part the reason why Lockheed Martin trades at a pretty high P/E level compared with most industrial sector stocks and investors have been pushing the stock price up as of late.

{kind=link}

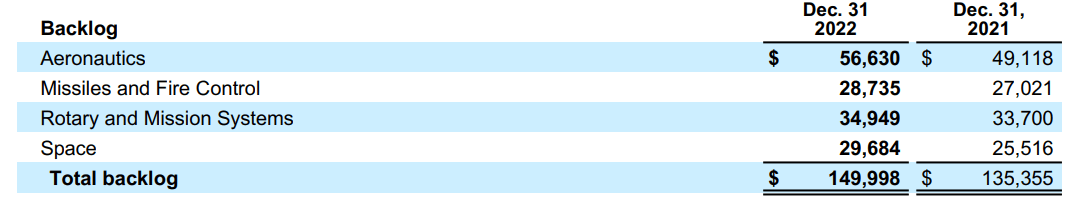

With a forward P/E of almost 18, it is trading as a stock that investors evidently feel that it has some significant improvement in earnings on the way, which seems to be a justified assumption based on the growing backlog of orders to fill. While waiting for the expected improvement in earnings, investors can enjoy a dividend of over 2.5%, which makes the waiting a little bit more pleasant.

Growing social angst across the Western World, related to declining living standards, makes it unlikely that NATO governments will keep resolute on military spending growth

The Ukraine conflict is coming close to reaching a full year, which left many Western armories short on certain supplies. The world is once more convinced that major military conflicts will involve large, well-armed armies on both sides. This, and growing talk of a possible US action to militarily defend Taiwan in an open confrontation with China in a conventional war is leading to a paradigm that is getting to be close to being gospel in regard to military spending outlooks and expectations for this decade. In other words, geopolitical tensions are making it more and more likely that more military spending becomes a necessity.

The less publicized fallout of the Ukraine conflict as well as other geopolitical frictions such as between the US and China is the resulting deterioration in the economic performance across much of the world, but especially in places like Europe, where a painful divorce from Russian energy left the continent in a state of permanent potential economic crisis. Some of this is starting to spill into the streets, with large protests and strikes in France and the UK where the magnitude of the protests is starting to reach the one million marchers mark.

The French & British protests are by no means directly associated with society or governments having to choose between improving living conditions, expectations for pensions, and so on, and military spending. Governments do have to be mindful however that they may not be able to do both, especially as borrowing costs are also increasing. A recent protest in Denmark however did directly pit the government's desire to raise military spending at the expense of workers losing a public holiday in order to pay for it. Clearly, some segments of the public are not entirely willing to sacrifice in the name of higher military expenditures.

Europe has not been a prime market for high military spending proposals for many decades now, which might explain why there is emerging pushback from the public against plans to increase defense budgets, even as there is a major war happening on the continent. With major economies like Germany seeing real wages decline by more than 4% last year, odds are that public opposition to higher defense spending will probably grow, as everyday worries, such as ordinary households trying to just make ends meet, will quickly overwhelm the idea that Russia will just try to march into all of Europe and try to take over. This will probably become the case even more so once the Ukraine war ends.

The issue of defense spending in the United States tends to have far more public appeal. Cutting spending is often seen as unpatriotic while increasing spending is associated with being tough on the international stage. Here too, as is the case in Europe, competing for social welfare spending, climate change, as well as other spending needs or desires, will crowd out defense spending.

Another aspect of defense thinking needs to take into account the fact that recent surveys have shown that 77% of young adults are unfit for military service , due to health or intelligence level. I would add to that that the demographic that makes up the bulk of the young people who would be fit, is not necessarily the demographic that may be attracted to military careers. The rate of obesity among children in the highest income and highest educated demographics tends to be only half compared with lower income demographics. Investing in raising healthier, smarter children may become just as much of a priority or even more so for long-term national security thinking than the kind of hardware that Lockheed Martin can provide.

{kind=link}

One final factor to keep in mind is that the current proxy war in Ukraine, with NATO arming Ukraine to fight against Russia, is revealing some potential flaws in military procurement strategies. It seems that many NATO militaries would not be prepared to sustain a high-intensity war against a well-armed opponent, despite NATO's collective spending of over $1 trillion per year. It raises inevitable questions in regard to spending efficiency. Western militaries will probably come to conclusions that can lead to arms manufacturers having their profit margins squeezed in a quest to show improvements in spending efficiency.

Investment implications

For now, things are looking up for Lockheed's future prospects. The closing of the Canadian deal for 88 F-35 fighter jets, valued at over $14 billion is just the latest example of why investor enthusiasm for this stock may be justified. I wonder how long it will take, given what I know about Canadian politics, as a Canadian citizen how long before opposition parties will argue that this deal should be canceled in order to divert the money to the health care system or to other social needs. It has happened before , and it probably will happen again. It might not only be Canada either that will probably seek to cancel deals, and prefer to pay penalties rather than have to sit on military spending policies that the public will not approve of.

Given Lockheed's stagnant performance last year, and a similar outlook this year, those improved future prospects, on the back of a growing orders backlog are crucial to its positive outlook that justifies a P/E of almost 18. In the absence of positive geopolitical developments, in other words, continuing frictions going forward, it is hard to make the case for an outlook that envisions continued growth in NATO military spending, therefore it is hard to make a good investment case for Lockheed Martin. There are simply too many competing priorities for Western governments, while resources are becoming more scarce.

As far as continued geopolitical tensions go, I foresee a turning point, where de-escalation will take place. It has to be because we are starting to get too close for comfort in terms of posturing our way into a situation of potential global calamity. My guess is that the turning point will arrive this year, and if that is the case, we will see a flurry of cancelations of existing contracts, as well as reductions in plans to sign future contracts for most arms manufacturers, including Lockheed Martin products. If I am right and news of such a turn in policy priorities will start to trickle in, Lockheed's stock price could have some significant downside from current levels.

For further details see:

Lockheed Martin: Western Fiscal Realities May Sink Hopes Of Higher Defense Spending