SPY - Long Leading Forecast Through H1 2024: Continued Downward Pressure

2023-08-02 12:05:54 ET

Summary

- Long leading indicators provide insights into the likely state of the economy one year or more from now.

- Two indicators - interest rates and housing market indicators - are at horrible levels, but have bounced off even worse levels from last autumn, so are neutral.

- Corporate bond yields, housing, corporate profits, real money supply, the yield curve, credit conditions, and real retail sales per capita are all negative indicators.

- Altogether they indicate that negative pressure on the economy from background financial and monetary conditions will continue through H1 2024.

Introduction

With the report on Q2 GDP and the Senior Loan Officer Survey of bank lending by the Federal Reserve, almost all the information we need to take a long-range peer into the likely state of the economy one year from now is available, via the long leading indicators.

What Are The Long Leading Indicators?

I have several systems for forecasting the economy. One is the high-frequency "Weekly Indicators," which, as the name implies, is updated weekly and is thus very timely. For the short term, up to about 6 months out, a second, K.I.S.S. method, relies on the Index of Leading Indicators, and is a perfectly adequate tool with the inconvenient habit of being right more often than most highly paid Wall Street forecasters.

To forecast the period over 6 months out, I turn to "long leading" indicators, relying for that on monthly and quarterly data which has been extensively vetted in for decades already, and as during that time going back 50 years has a sustained record of turning one year or more before the onset of a recession.

Most of what you read which seeks to forecast the economy falls into two categories of leading you astray:

1. Most observers simply project existing trends into the future, overlooking that there are some datapoints that reliably turn before others, and thus completely miss turning points until they are already in the rearview mirror.

2. A great deal - perhaps most - of what you read about the economy starts off with an ideology and a conclusion based on that ideology already baked into the cake. The writer then marshals a series of datapoints that confirm that already-determined conclusion. The very same utterly decisive economic metric from last year that was moving in one direction is completely ignored this year when it is moving in the opposite direction, and vice versa.

By contrast, my method is to look repetitively at a bank of indicators that have decades - in a few cases, over a century - of history, and a demonstrable record of being reliable harbingers of the continuation or reversal of an existing trend.

Now let's return to my main topic at hand. Geoffrey Moore, who for decades published the Index of Leading Indicators, and in 1993 wrote " Leading Economic Indicators: New Approaches and Forecasting Records ." He identified 4:

- Housing permits

- Corporate bond yields

- Real money supply

- Corporate profits adjusted by unit labor costs.

A variation of the above is Paul Kasriel's "foolproof recession indicator," which combines real money supply with the yield curve, i.e., the difference in the interest rate between short- and long-term treasury bonds. This turns negative a year or more before the next recession about half of the time.

Another long leading indicator has been described by UCLA Prof. Edward E. Leamer, who wrote " Housing IS the Business Cycle ." In that article, he identified real residential investments as a share of GDP as an indicator that typically turns at least 5 quarters before the onset of a recession.

Several other series appear to have merit as long leading indicators as well. Real retail sales in several forms also have value as a long leading indicator and, in particular, real retail sales per capita. Additionally, the tightening of credit conditions also appears to have merit as a long leading indicator.

That gives us a total of 7 categories of long leading indicators. All of these economic series have a long-term history of turning a year or more before a recession.

Important Previous Forecasts

In February, in my forecast through the end of this year, I wrote:

“Not only have these indicators have continued to deteriorate in the past 6 months, but not only are none positive, for now none are even neutral! Every single one is negative, if even slightly so.

“Based on these indicators, the ’Recession Watch’ that I issued last spring to begin this Quarter, and amplified into a ’Warning’ in November, remains in effect throughout this year. This does not mean that a recession will last all of this year. Rather, it means that the conditions which were ripe for a recession will continue for the next 12 months, subject to the condition that these indicators typically indicate that a recession is ending more on the order of 6-8 months ahead rather than 1 year ahead. And as indicated above, the first of them, corporate and long Treasury bond rates, may turn neutral by the end of this month.

“As indicated above, when the short leading indicators also turned down, I upgraded this to ‘Recession Warning’ in late November. Several coincident indicators … appear to have already turned down, but several others … have not.”

My current top to bottom review of all my models is to check, and update, that conclusion.

Current Trends In The Long Leading Indicators

Corporate Bond Yields

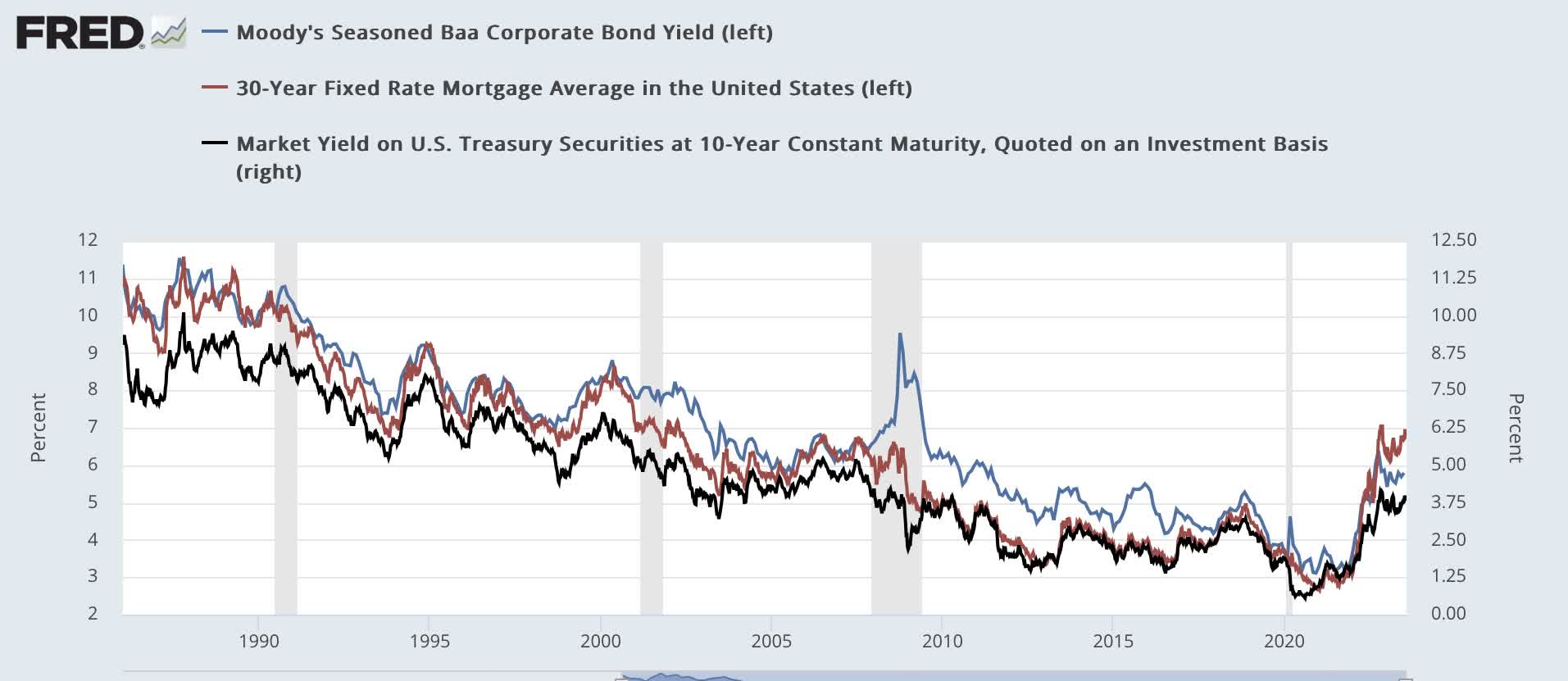

On a monthly basis, corporate bond yields data goes back over 100 years to 1919. With the exception of the 1981 "double-dip," the fiscal contractions underlying the 1938 and 1945 recessions, 1926, and - excusably I think! - 2020's pandemic - corporate bond yields have always made their most recent low over 1 year before the onset of the next recession, as shown in the graph below of the last 40 years (although the correlation goes back much further):

{kind=link}

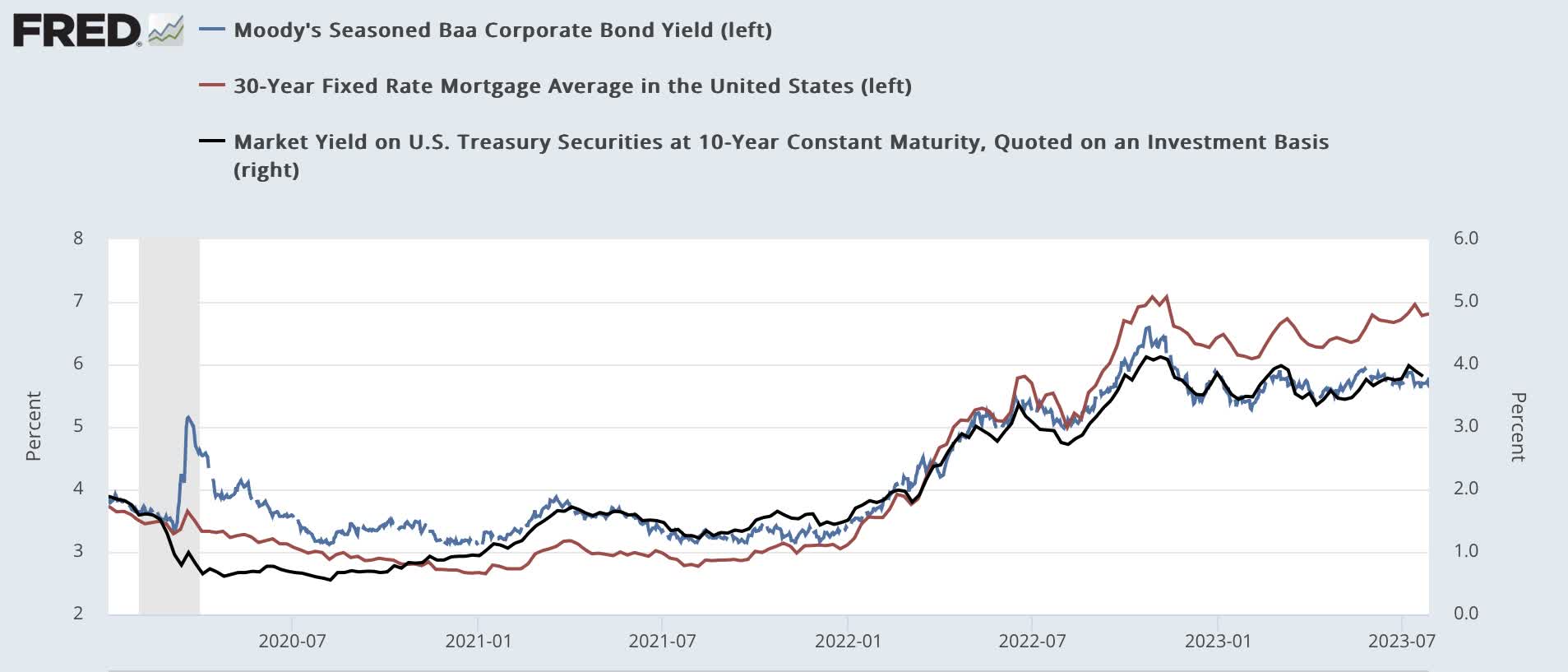

The sharp rise upward in bond yields in 2022 was the most in the past 40 years, even surpassing those before the last 3 recessions. But they have not made a new high since last October and November, as shown in this close-up view of the post-pandemic era:

Interest rates post-pandemic (FRED)

{kind=link}

Historically, most often bond yields have peaked before recessions, and before the Fed is even finished raising rates. As a result, this indicator has turned neutral, but has not improved enough to be an actual positive.

Housing

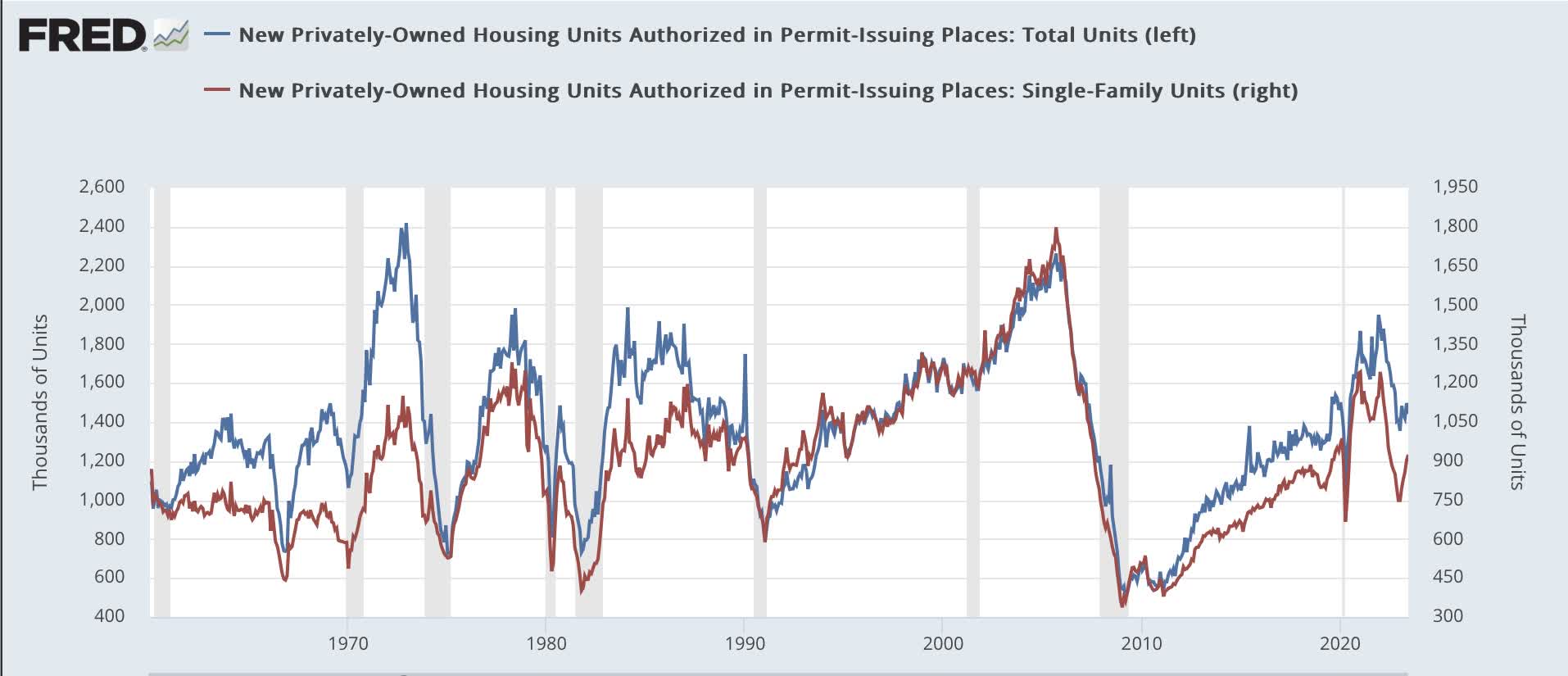

Housing, which typically follows interest rates with a few months' lag, has typically declined by over one year, and by 20% or more before the onset of a recession (the mild recession of 2001 being the exception, with only a 10% decline), as shown in the below graph of total housing permits ((BLUE)) and single family permits (red), which have the most signal vs. noise of any leading housing metric:

{kind=link}

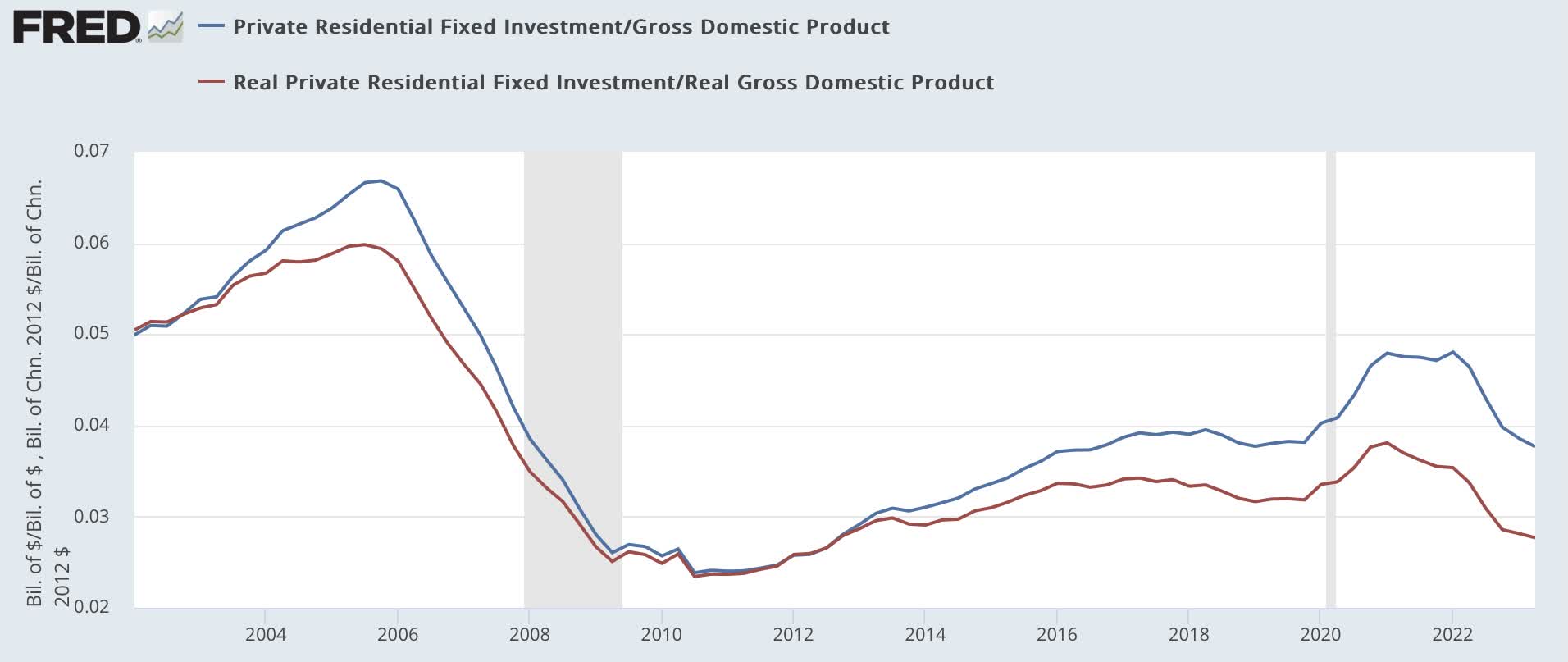

Additionally, housing as a share of GDP, both nominally and in real terms, declined further in Q2, and is now down over 20% from its expansion peak in Q1 2022:

Housing construction as a share of GDP (FRED)

{kind=link}

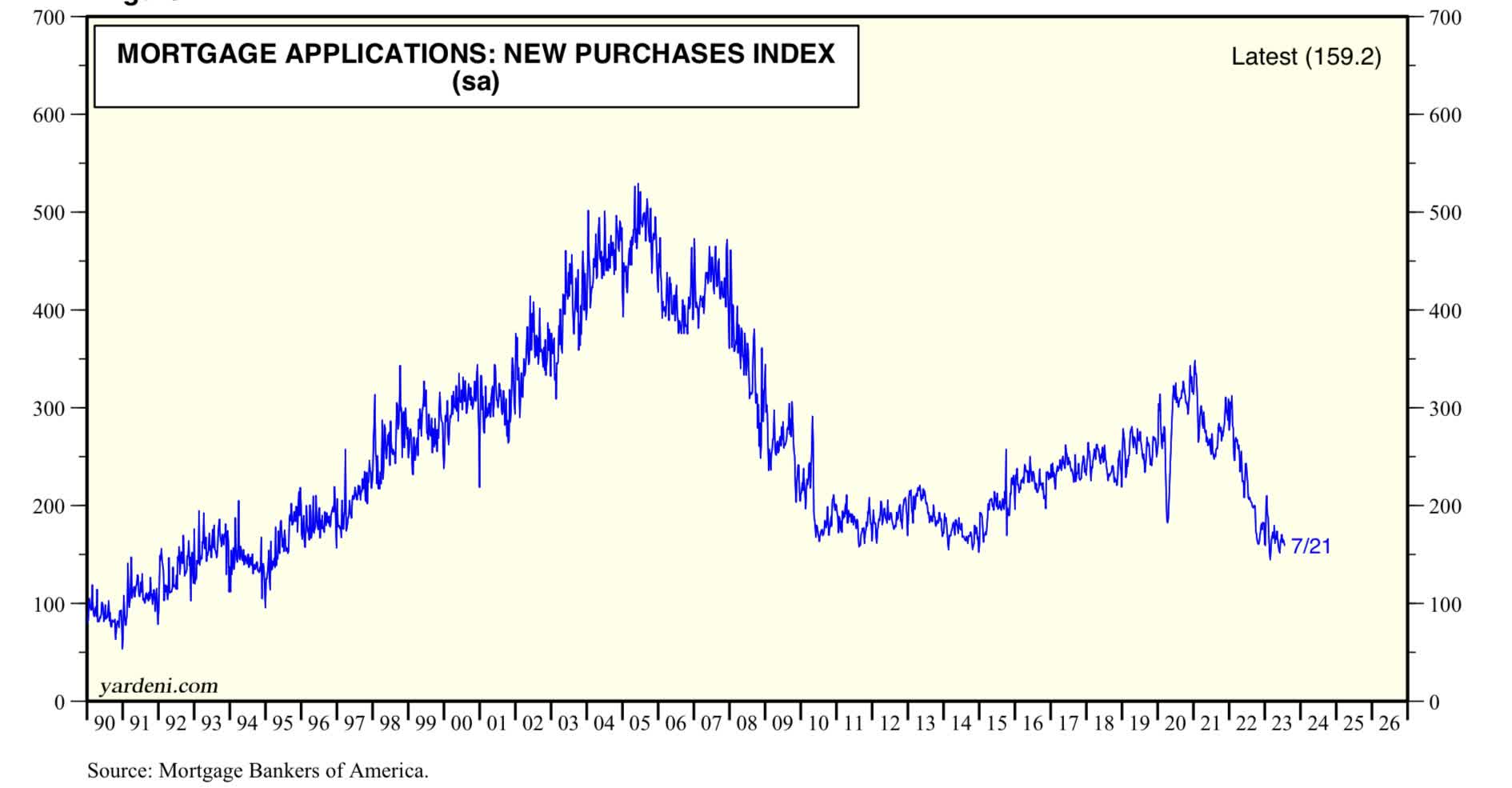

Perhaps most potent is the below graph of purchase mortgage applications. Although they have increased slightly off their worst levels, generally these are at their lowest levels since 2014, and before that the last Millennium:

Purchase mortgage applications (Yardeni.com)

{kind=link}

There is simply enormous downward pressure on the housing market.

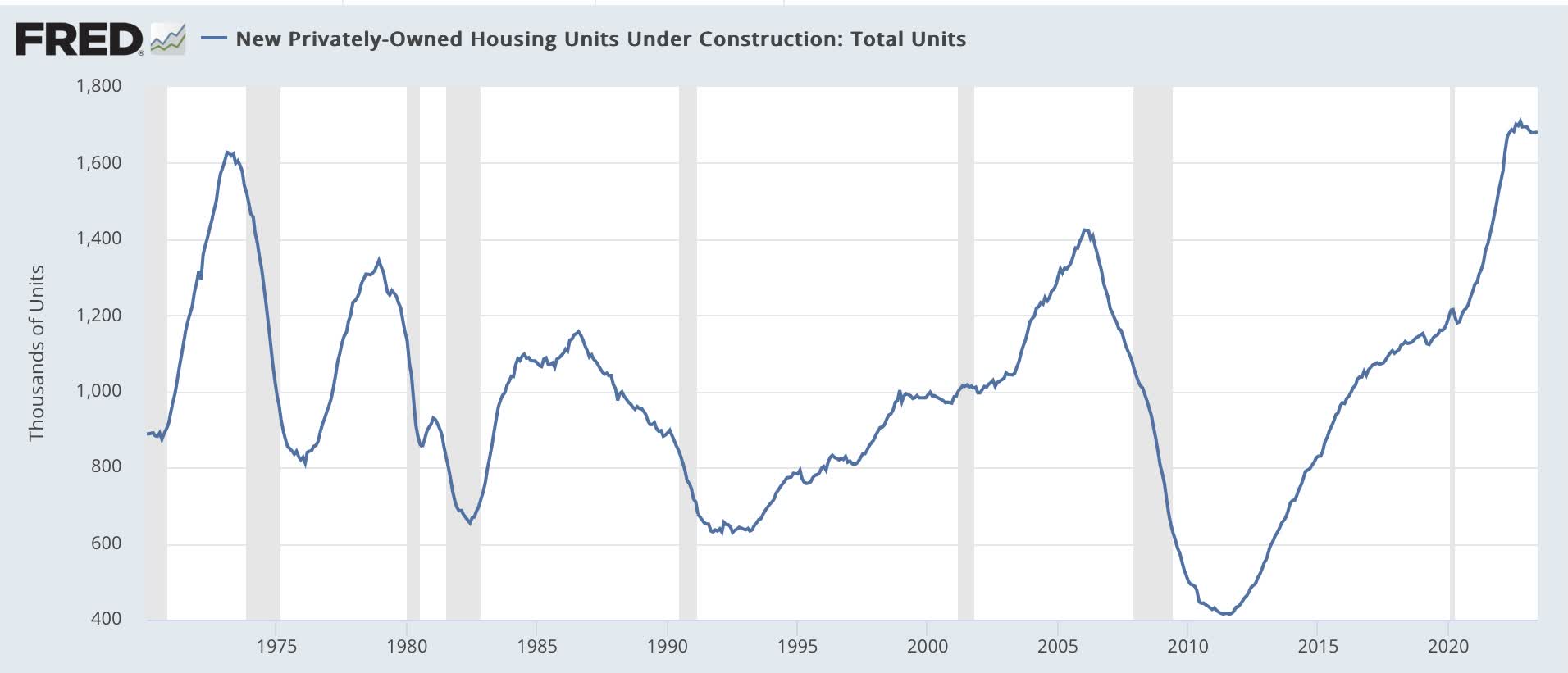

One important difference this time around about housing's effect on the economy is housing units under construction, the ultimate measure of the economic impact of housing. It typically has followed permits down after 3 - 6 months, but with much variability, and continues to be near record highs:

Housing units under construction (FRED)

{kind=link}

Housing thus presents a mixed picture: higher permits and new home sales, lower investment as a share of GDP, and units under construction which are slightly down from peak. Thus, housing, too, qualifies as a neutral.

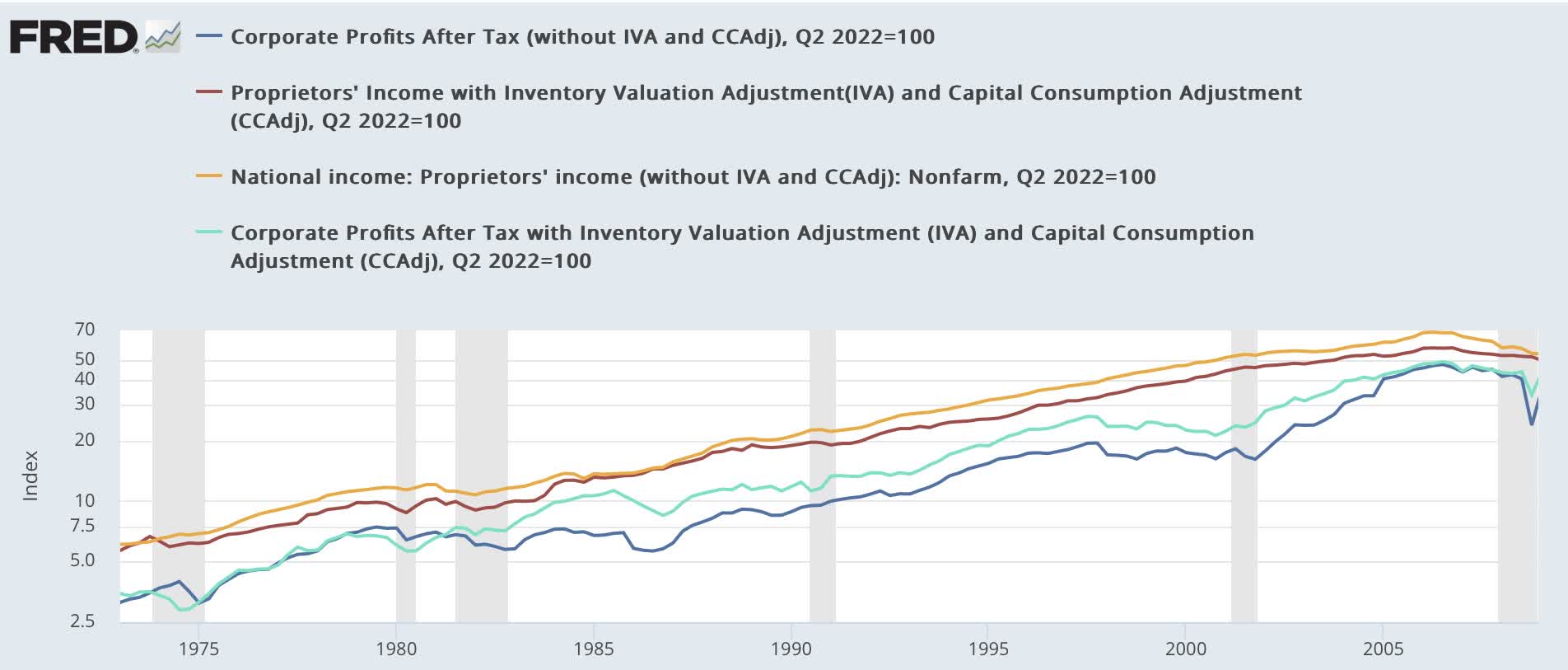

Corporate Profits

Corporate profits deflated by unit labor costs have an excellent track record going back over half a century as well. Below I show them both with and without inventory adjustments, as well as the placeholder of proprietors' income, for the past 50+ years, in log scale:

Corporate profits and proprietors income (FRED)

{kind=link}

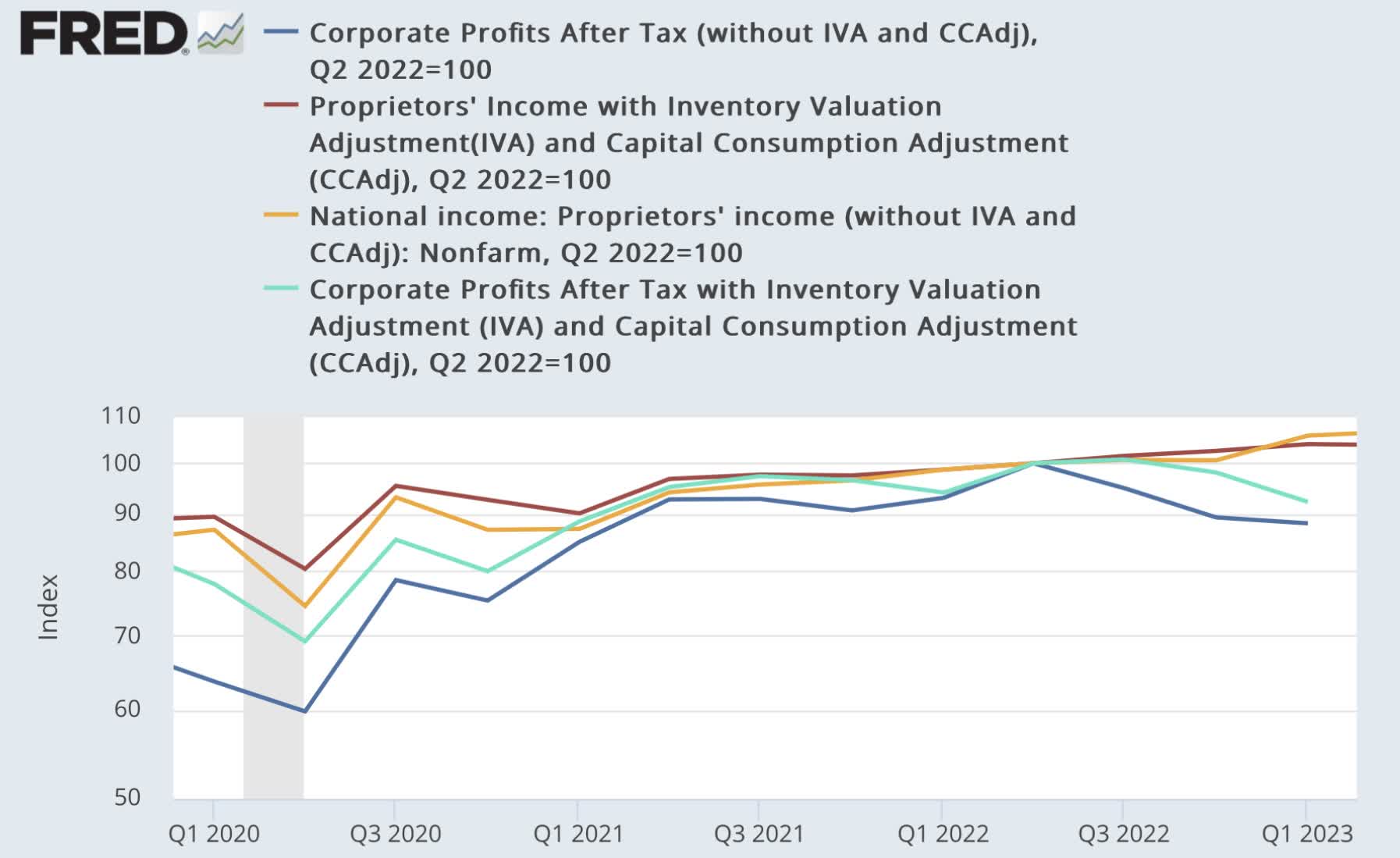

These are not reported until the second estimate of GDP, so Q1 is the latest data we have. But proprietors' income normally behaves similarly to corporate profits, often with a one quarter or so lag, and was reported in the initial Q2 estimates, as follows:

Corporate profits and proprietors income post-pandemic (FRED)

{kind=link}

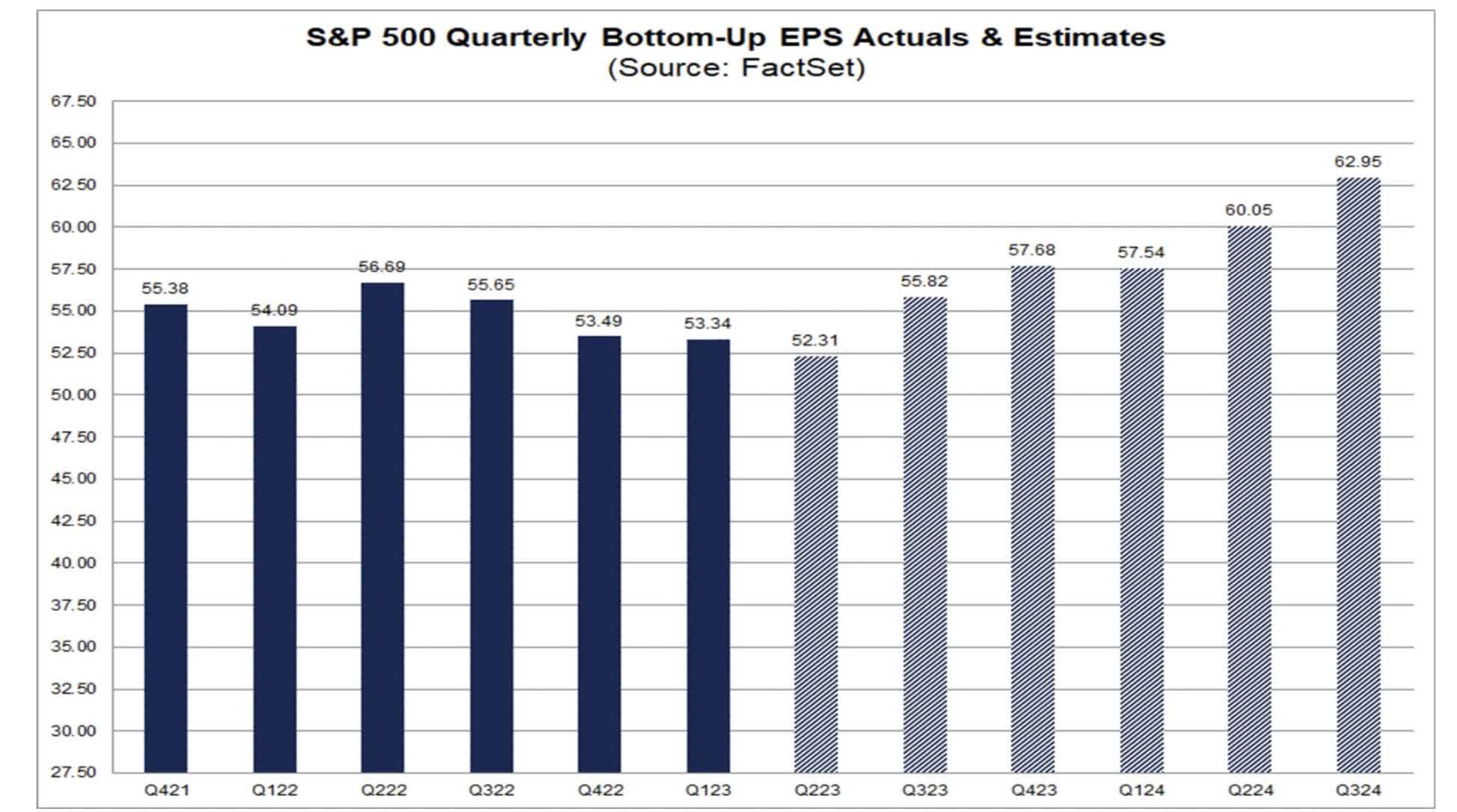

Additionally, here is the chart of nominal corporate profits for the S&P 500 (SP500) through last week by FactSet:

S&P 500 earnings (FactSet.com)

{kind=link}

This also shows corporate profits down over 5% from their nominal peak in Q2 of last year.

As a result, this indicator is negative.

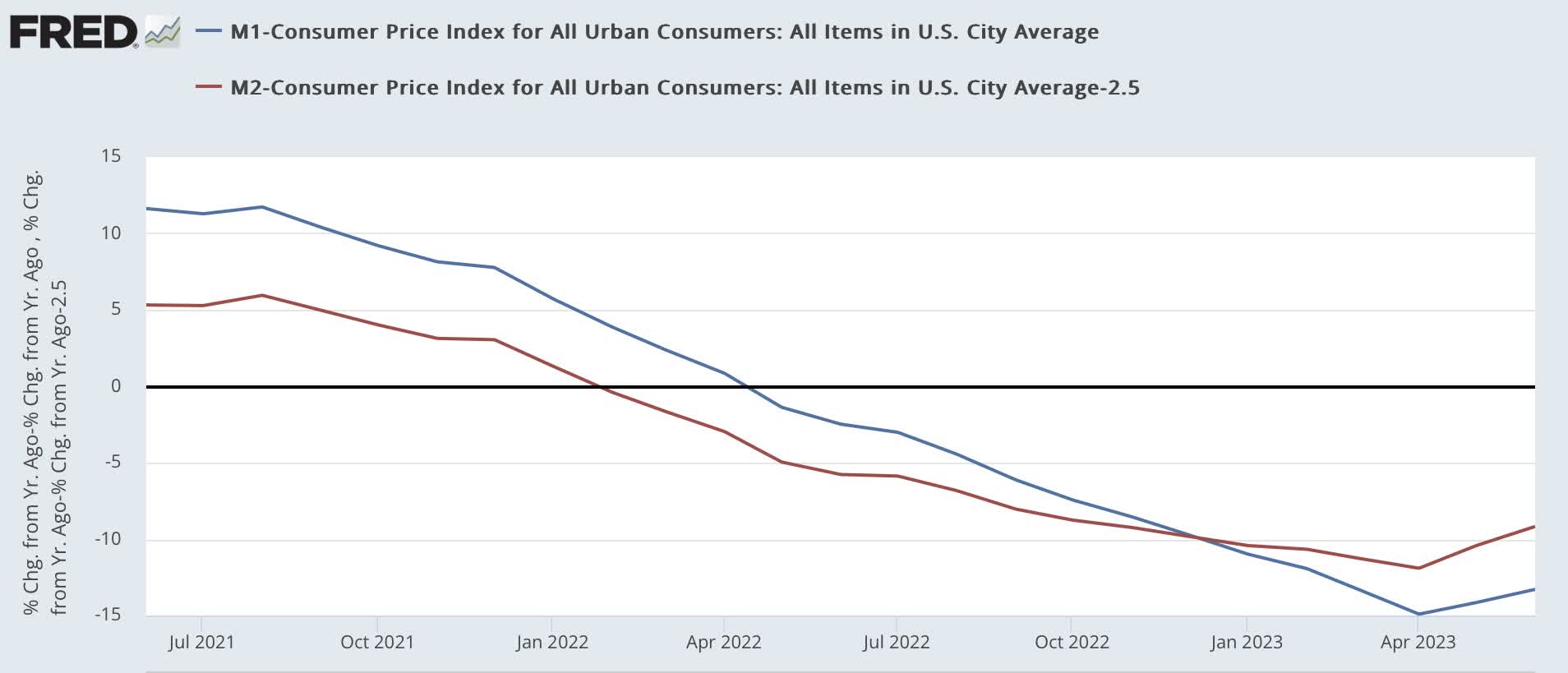

Real Money Supply

No recession has ever started without at least real M1 turning negative or real M2 declining to under +2.5%. Here is this relationship going back over 60 years until the end of 2019 on a YoY% basis:

{kind=link}

In March 2022, Real M2 turned negative YoY. It was joined by real M1 in May. Currently both were recently down more than -10%, the worst level since 1980.

Real money supply is thus also a negative.

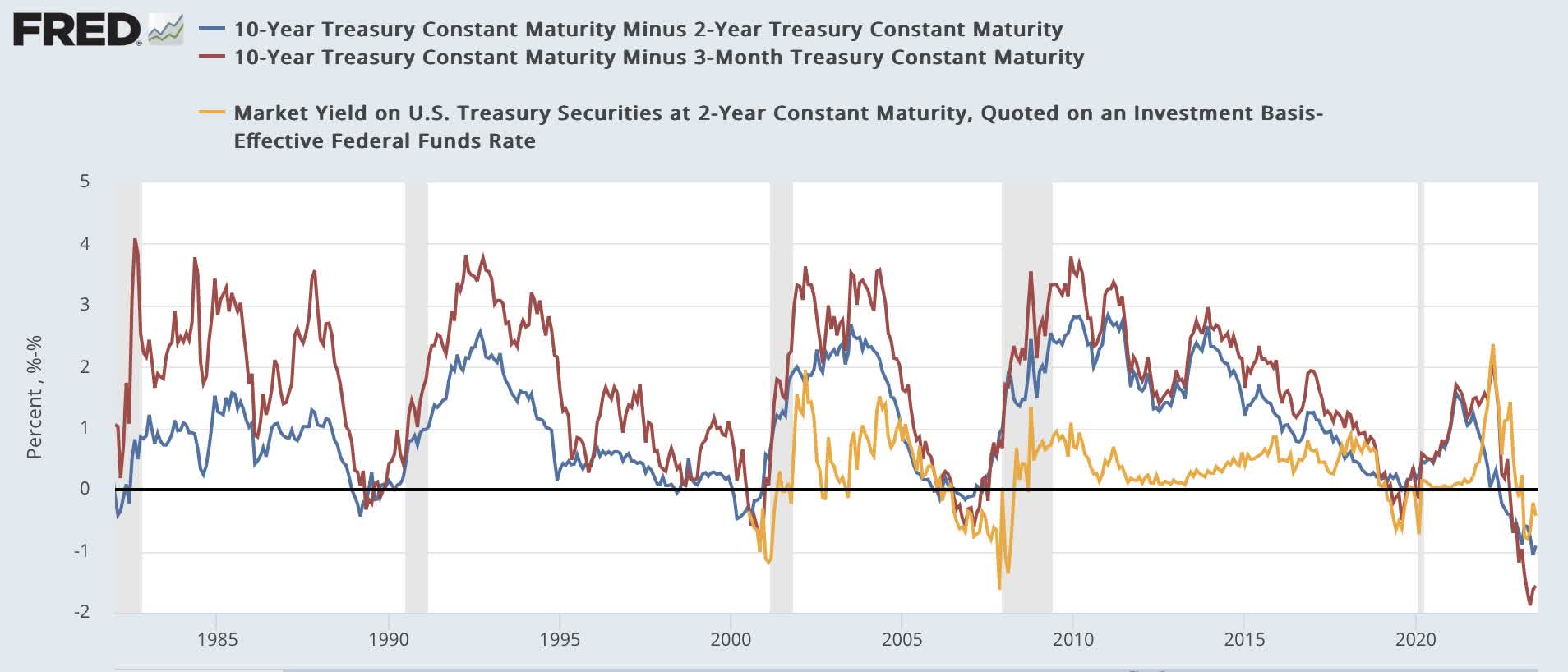

The Yield Curve

This has been an excellent long-range forecasting tool in times of inflation (although I do not think a positive yield curve is definitive in low interest rate deflationary environments). In the last 60 years, typically, a recession has begun after the Fed raises rates to combat inflation, and sufficiently so that the yield curve inverts.

Here is what 3 popular measures of the yield curve, the 10 year minus 2 year Treasury, 10 year minus 3 month Treasury, and 2 year Treasury minus Fed funds rate, look like for the past 25 years:

{kind=link}

All three have inverted, although the 2 year minus Fed funds is much less inverted than the other two. Thus, the yield curve is very negative.

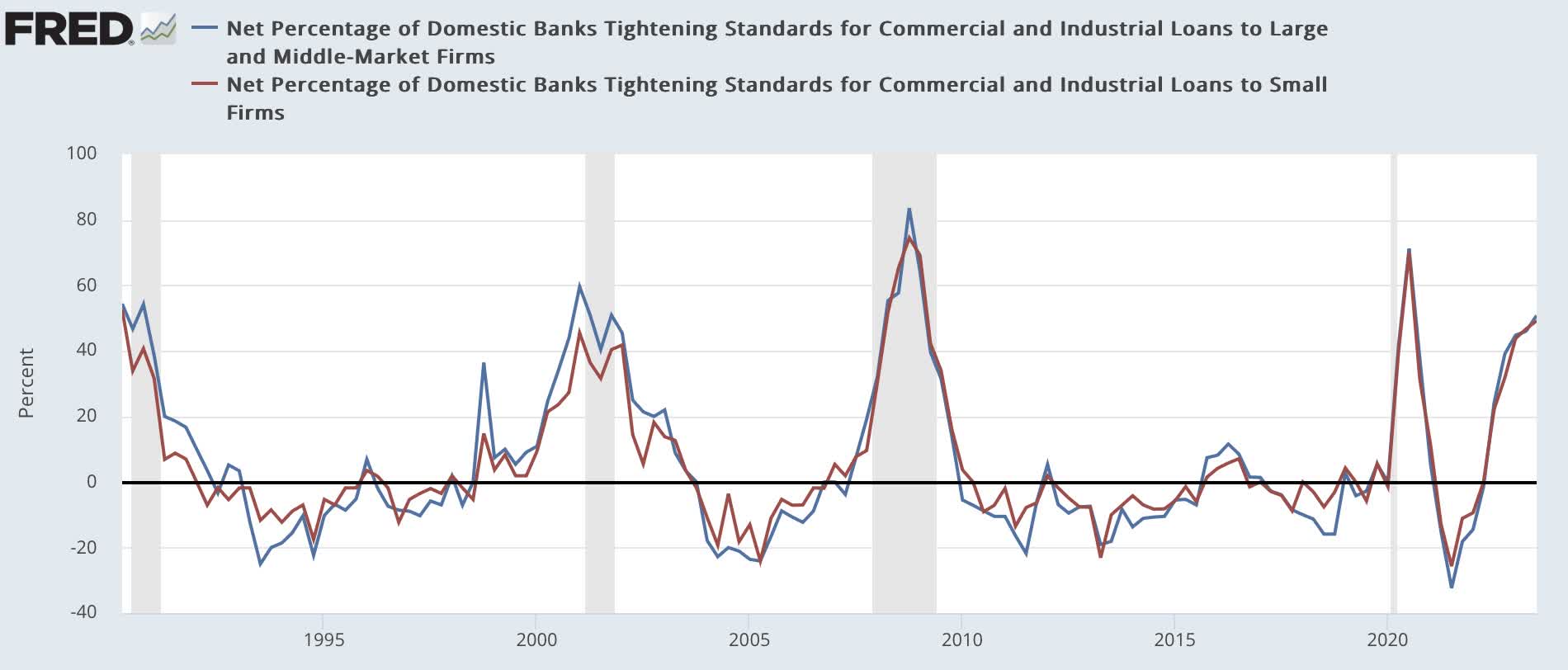

Credit Conditions

The loosening or tightening of credit also appears to be an important component of changes in the economy over one year out. Although it only has a 30-year track record, two components of the Senior Loan Officer Survey have had a good track record.

The first component, the percentage of banks tightening vs. loosening standards for commercial loans to large ((BLUE)) and small (red) firms, has turned much higher, to levels only seen during the worst depts of past recessions. Note that a "positive" number actually means tightening. Don't blame me!:

{kind=link}

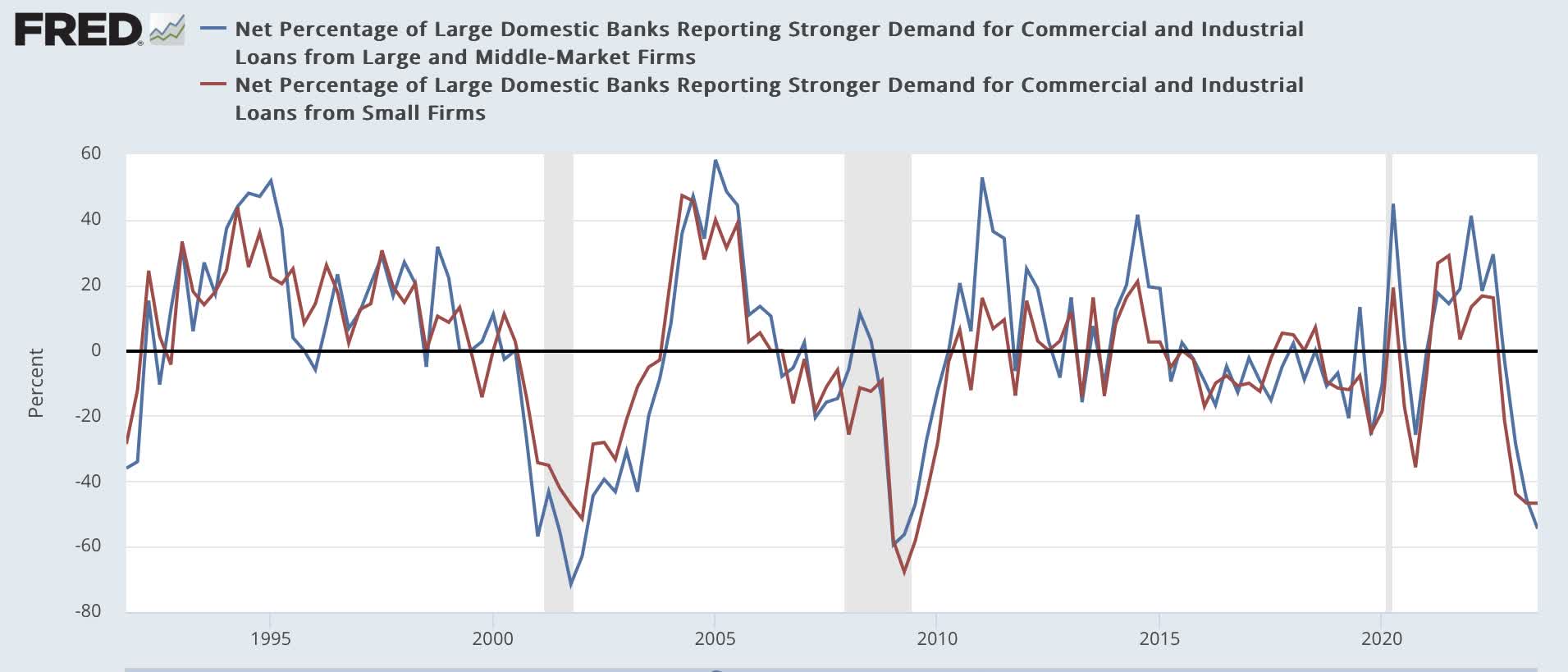

The second component, demand for loans by large ((BLUE)) and small (red) firms, also is now at levels on par with its past worst readings during the prior two recessions:

Demand for commercial loans (FRED)

{kind=link}

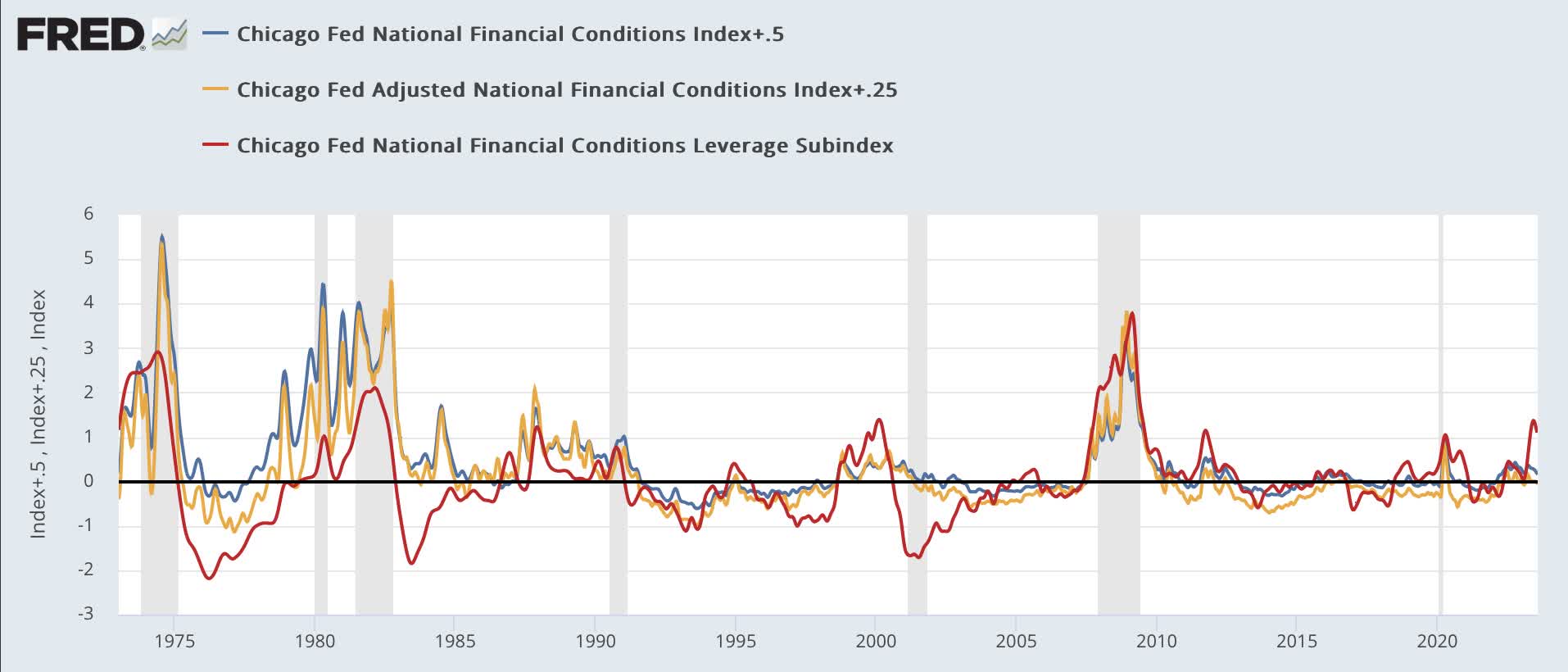

On a weekly basis, the Chicago Fed Financial Service Index ((BLUE)), Adjusted Financial Conditions (gold) index, and Leverage subindex (red), which have had a good record in the past anticipating the Senior Loan Officer Survey's result re tightening credit, are mixed, with the most leading Leverage subindex being very negative, while the Adjusted index is slightly negative and the unadjusted index slightly positive in comparison with their historical inflection points (again, like the credit tightening index above, a “positive” reading is actually negative for the economy):

Chicago Fed financial indexes (FRED)

{kind=link}

Because the most leading aspects of these indicators are very negative, so is this sector.

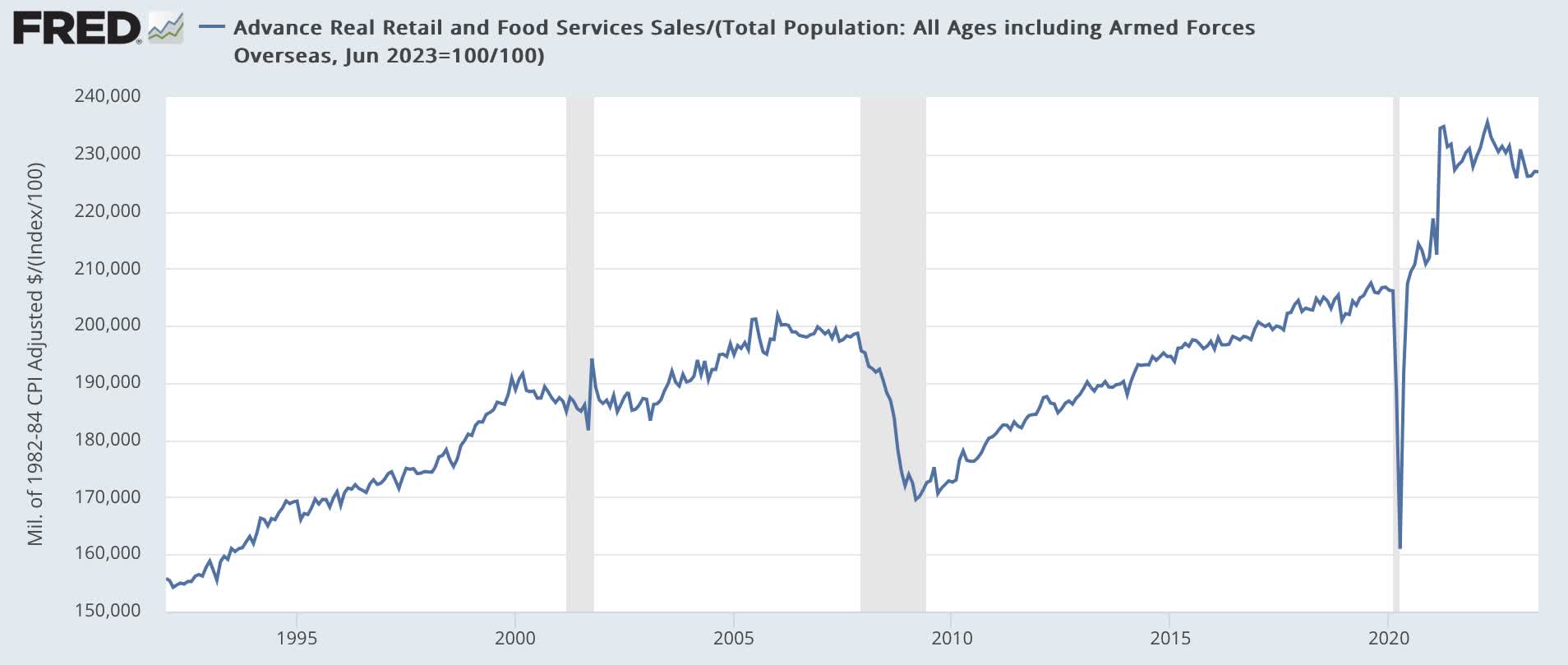

Real Retail Sales Per Capita

These peaked more than a year before the onset of the last two recessions, but made troughs within six months of each recession bottom.

These made record highs in March and April 2021, during the stimulus spending spree, but since April 2022 have consistently trended negative:

Real retail sales per capita (FRED)

{kind=link}

Thus, this indicator is negative as well.

Summary And Conclusion

Let me point out, first of all, that this is a more comprehensive set of indicators, and in some cases, indicators with longer and better track records, than are found in my more timely "Weekly Indicators" columns.

Of the 7 indicators, two - interest rates and housing - are neutral. The remaining 5 - corporate profits, real money supply, the yield curve, credit conditions, and real retail sales per capita - are all negative.

This tells me that the underlying longer-term conditions in the economy remain negative. Although no recession has occurred, the background conditions to give rise to one, depending on the status of the short leading indicators, remain. Thus, the “Recession Watch” remains into H1 of 2024.

I will update my short term forecast for the next 6 months separately, and also my “consumer fundamentals nowcast,” and with that, comment further on whether the “Watch” should at this time be a “Warning.”

For further details see:

Long Leading Forecast Through H1 2024: Continued Downward Pressure