VZ - Long Verizon And Holding Until Recession

2023-10-05 15:53:25 ET

Summary

- Verizon's stock has underperformed the broader market by a wide margin this year, pushing its dividend yield to over 8%.

- But cash flows remain intact, underpinned by a normalizing capital deployment strategy and improving wireless economics.

- The combination suggests VZ's recent declines are likely a direct function of rising Treasury yields.

- This creates a compelling opportunity for investors to potentially lock-in an 8% dividend yield at current levels and partake in valuation upside potential when the recession-driven easing cycle kicks in.

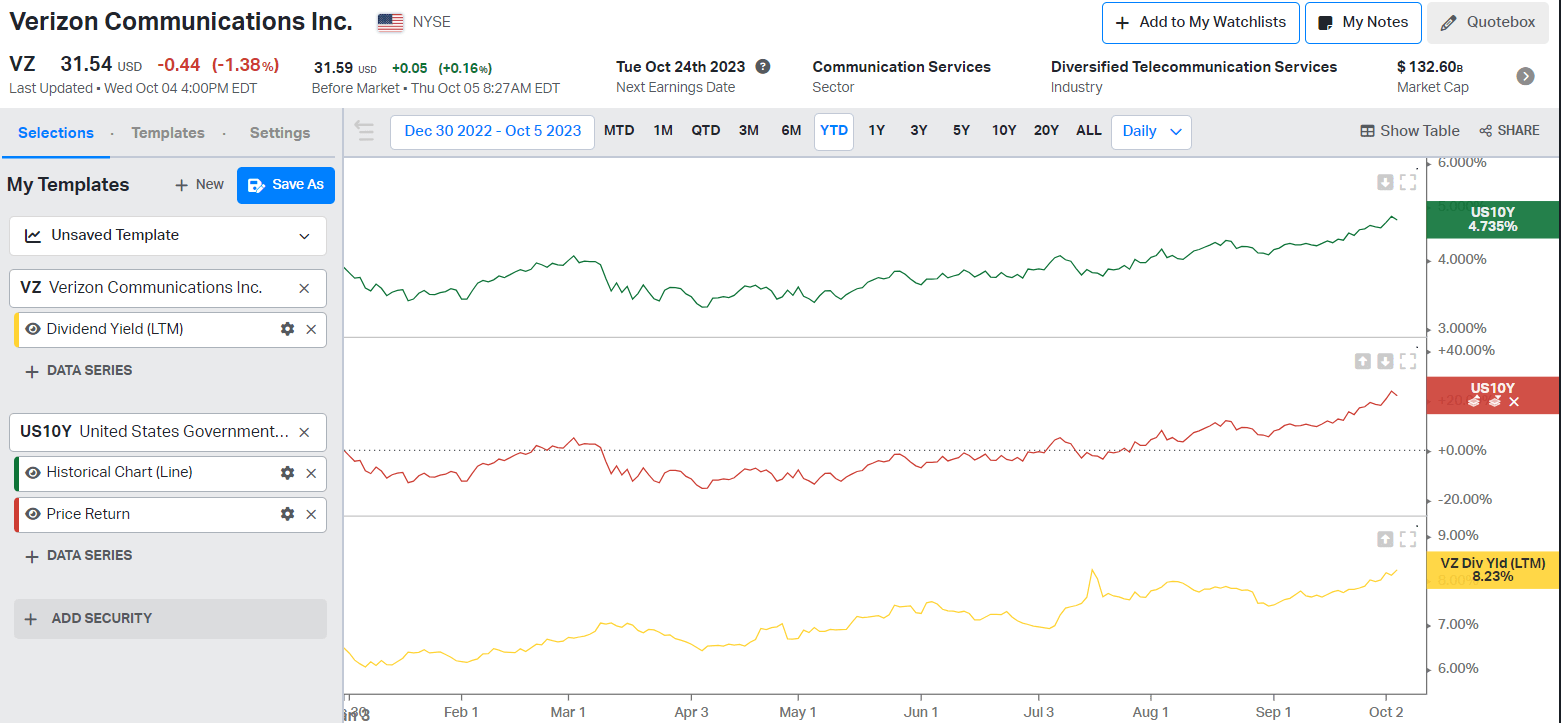

Verizon's stock ( VZ ) has been on a steady decline this year, with the plunge picking up speed in recent weeks, in tandem with the broader market slump following Fed Chair Jerome Powell’s reaffirmation on maintaining a higher for longer rate environment. Its dividend yield is now pushing beyond 8%, nearing an all-time high and besting the payout from telco rival AT&T ( T ).

Meanwhile, Verizon’s cash flows are also on the horizon of expansion following the completion of its multi-year 5G investment cycle. ARPA expansion observed in recent quarters is also compensating for market share loss in its business and consumer wireless segments due to secular declines and stiffening competition, respectively. Coupled with the consideration of Verizon’s utility-like business model in the digital-first economy, which provides protection against looming recessionary risks, we believe the stock’s underperformance against the broader market this year is a function of surging Treasury yields.

Considering Verizon’s solid fundamentals, with its cash flows expected to resume gradual expansion, we believe the stock is a reasonable buy for its 8%+ yield at current levels. We expect the stock’s valuation to re-rate upwardly toward levels more reflective of the underlying business’ intrinsic value when further tightening of economic conditions – or a likely recession – triggers monetary easing and subsequent normalization of both Treasury and Verizon’s dividend yields lower.

Verizon’s Performance is a Direct Function of Treasury Yield

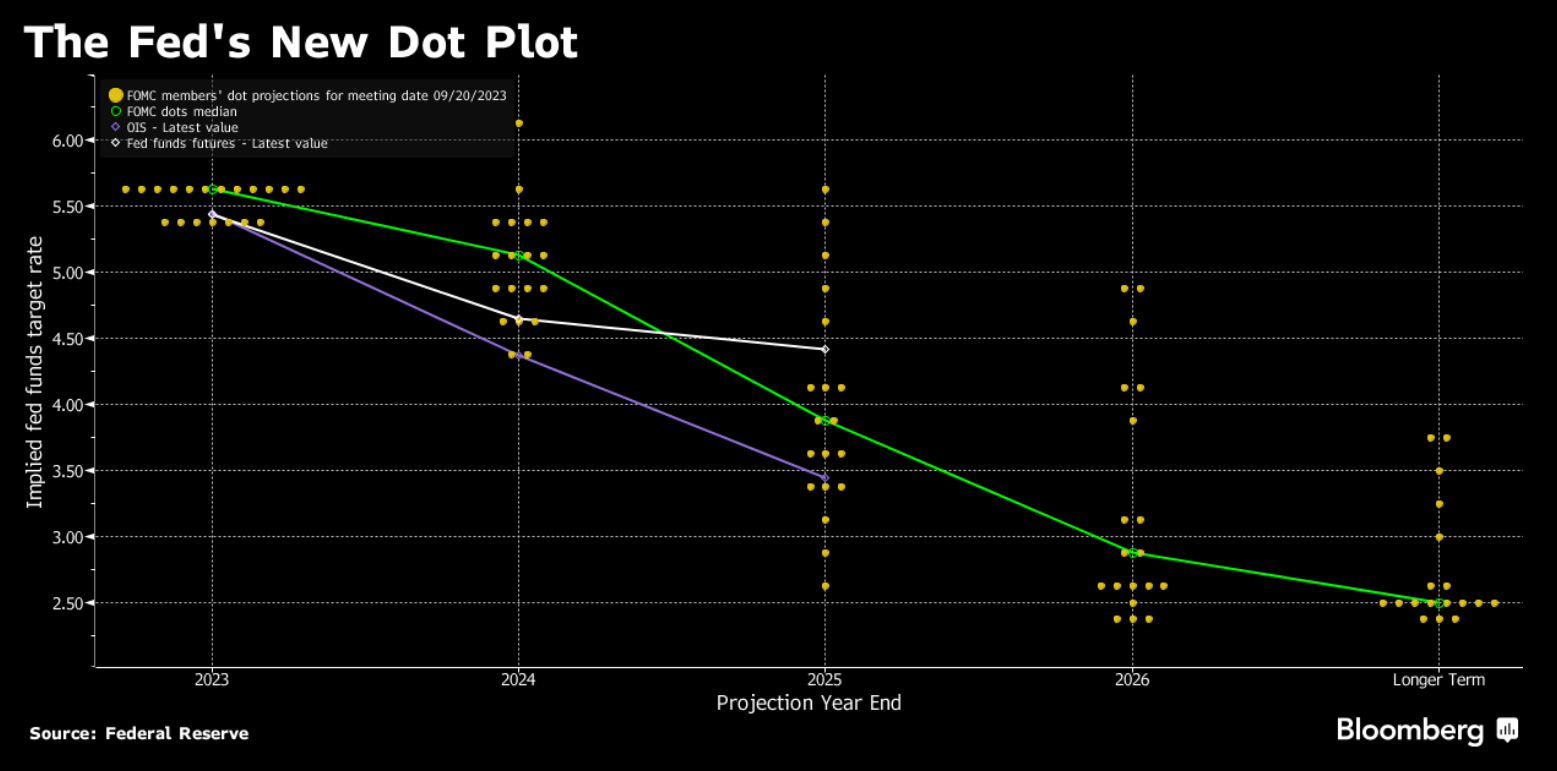

The higher for longer narrative on interest rates is gradually becoming a reality. Recent labour market data continues to show an economy that is running hotter than the Fed would like, reinforcing the need to keep monetary policy in restrictive territory for longer. This is in line with the Fed’s latest projections for stronger economic growth this year and the next compared to previous estimates – 2023 GDP growth is estimated at 2.1% , up from 1% in the previous projection released in June, while the anticipated unemployment rate was also adjusted lower from 4.5% to 4.1%.

Fed policymakers have also acknowledged that inflation resurgence risks are still “ tilted to the upside ”, bolstering calls for further monetary tightening. The latest dot plot released by the Fed shows support for one more 25 bps increase to the current benchmark rate of 5.25% to 5.5% before the end of the year. Rate cut expectations have also been pushed back, with the latest projections showing the Fed Funds rate at 5.1% exiting 2024, compared to 4.6% estimated in June.

{kind=link}

This has accordingly pushed the 10-year yield on a relentless run towards new 16-year highs this week. Specifically, yield on the 10-year notes has surged over 70 bps in the past month to 4.8% earlier this week, and currently hovers in the 4.7% range. Verizon’s dividend yield has also pushed higher in tandem with the trend observed in the benchmark Treasury, as the stock continues to plummet towards new lows this year.

{kind=link}

Historically, Verizon has traded with a dividend yield premium of about 4 to 5 percentage points above the benchmark Treasury yield. And the stock’s recent declines, which has inadvertently driven up Verizon’s dividend yield, also continue to maintain this differential, underscoring the driving influence of broader macroeconomic factors on its near-term valuation performance.

Fundamental Considerations

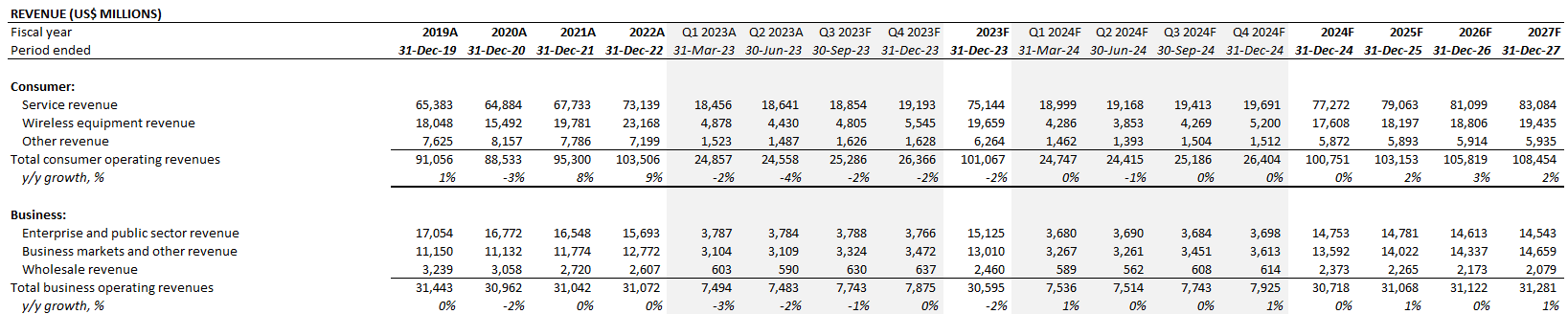

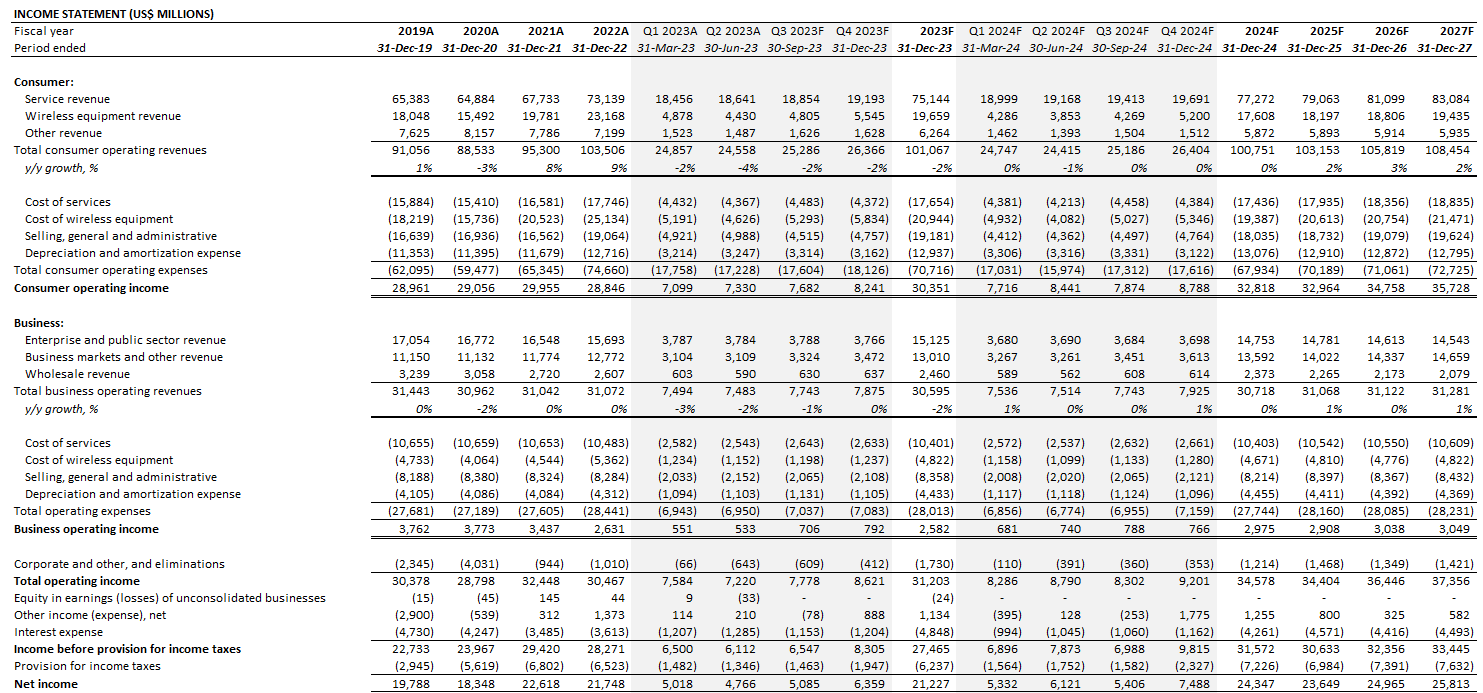

We believe Verizon’s underlying business fundamentals remain a secondary driver to the stock’s near-term performance given volatility in rates alongside a broader risk-off market sentiment. Admittedly, the telco industry is inherently competitive, as evidenced in Verizon’s continued pace of subscription losses to rivals AT&T and, more notably, T-Mobile ( TMUS ) over the past year. But Verizon’s revenue and earnings outperformance in recent quarters underscore strong pricing power bolstered by a differentiated value proposition to customers, resulting in ARPA expansion alongside cost-cutting efforts that are also tracking favourably towards management’s target. Recall that management has guided annualized savings of $2 billion to $3 billion by 2025, and is on track to delivering $200 million to $300 million of it in the current year.

Taken together, we expect Verizon’s revenue to expand at a 1% five-year CAGR.

{kind=link}

Anticipated strength in consumer wireless mobility and broadband is expected to more than offset continued secular declines in the business wireline foray and compensate for ongoing uncertainties in integrating and expanding the prepaid business. Profit margins are also expected to gradually expand in tandem with growth in ARPA, underpinned by the increasing mix of higher-priced long-term Unlimited Plan subscriptions.

{kind=link}

Verizon_-_Forecasted_Financial_Information.pdf

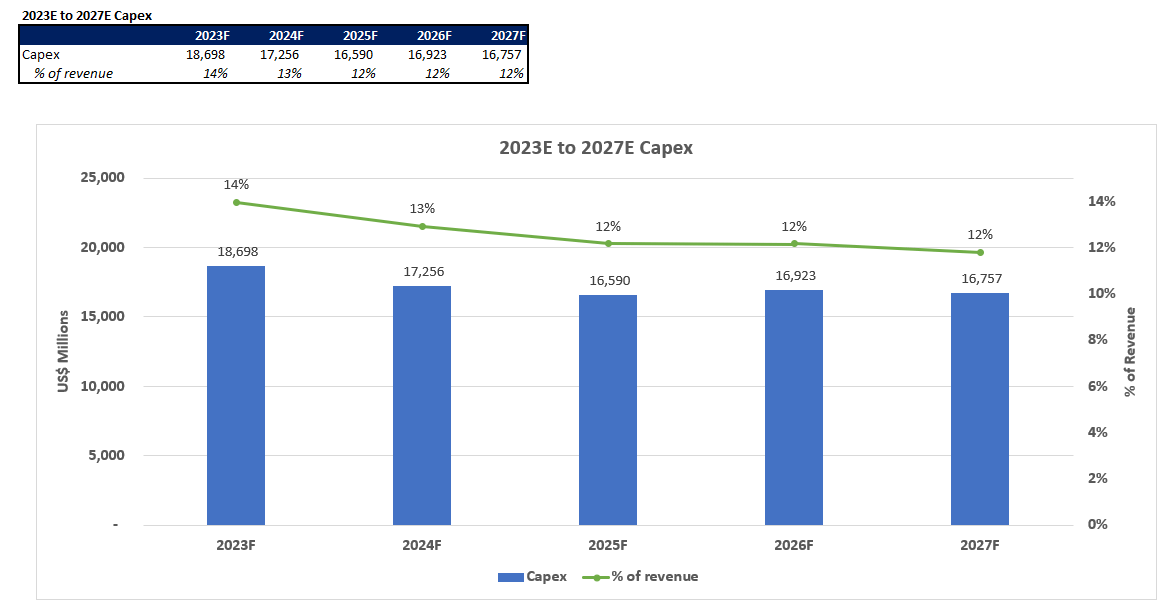

Meanwhile, completion of peak capital deployment primarily attributable to the multi-year build-out of 5G infrastructure is another tailwind to cash flow. Capital spending is likely to normalize back towards historical levels in the sub-$20 billion range exiting 2023, which reinforces management’s expectations for more than $17 billion of free cash flow generated by the end of the year, with no remaining debt repayment obligations in 2H23.

{kind=link}

In addition to freeing up capital to support a “much-improved dividend payout ratio” in the future, the development also lessens concerns that the near-term impact of industry and macroeconomic headwinds on Verizon’s fundamental prospects could disrupt its dividends. With increased visibility on its roadmap to achieving more than $17 billion of free cash flow by the end of the year, there is a favourable margin of safety for Verizon to carry out its annualized dividend payment total of about $11 billion – a key priority for the stock’s income-focused investor base.

Valuation Considerations

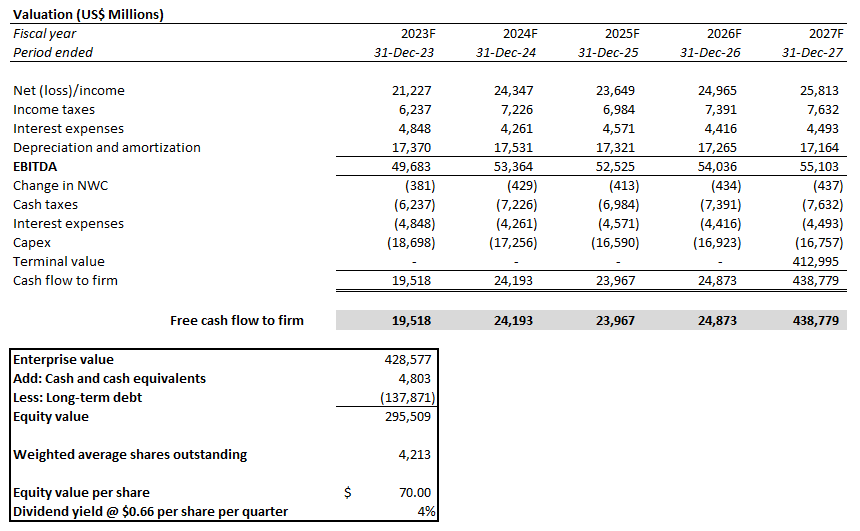

A discounted cash flow analysis on projections taken in conjunction with the fundamental forecast discussed in the earlier section estimates Verizon’s intrinsic value at about $70 apiece. The analysis applies a conservative terminal value multiple of about 8x, considering Verizon’s exposure to risks of ongoing competitive headwinds and secular industry declines, which could weigh on its longer-term cash flow prospects. Projected cash flows are discounted by a 6.2% WACC, consistent with Verizon’s capital structure in risk profile.

{kind=link}

At such a per share value, Verizon’s dividend yield – if the payout is left unchanged – accordingly falls back to the historical level of about 4%. We expect this upside potential on the stock to materialize when further tightening of financial conditions and economic deterioration greenlights the Fed to pivot towards easing. The impending recessionary pressure is likely to trigger the anticipated rate cuts exiting 2024 and drive gradual normalization of Treasury yields and, inadvertently, drive Verizon’s dividend yield lower.

The Bottom Line

We do not foresee structural weakness to Verizon’s ability to support its current dividends, especially with its cash flow prospects improving on the back of continued growth and margin expansion and disciplined capital deployment. The anticipated improvements are further supported by management’s continued commitment to a measured promotional strategy, which has historically been a pressure point for the broader telco industry’s bottom-line performance. Verizon’s recent introduction of new offerings, such as “ myPlan ”, to better address different consumer preferences also allows it to lock-in higher-priced subscriptions under extended contract terms. This will contribute to a more profitable growth trajectory by enabling market share retention and ARPA expansion over the long-run. The company’s normalizing capex spend trajectory post-5G build-out is another tailwind to cash flows.

With its underlying business fundamentals and cash flow prospects intact, Verizon's stock demonstrates a favourable recovery outlook when recession hits and Treasury yield normalizes back towards lower levels. We believe now is a good time to buy Verizon stock for an 8%+ yield, and we suggest holding until a recession hits, and pent-up valuation gains are expected to materialize.

For further details see:

Long Verizon, And Holding Until Recession