CA - Looking Back On Exchange Income Corporation And My RoR

2023-05-05 11:05:20 ET

Summary

- I've been a long-time investor of Exchange Income Corp. Since my first article on the company, I'm up significantly - and at this time, I'm keeping my position.

- However, the valuation is starting to look stretched here - and for the first time, I haven't outperformed the market since my last article.

- I'll update on Exchange Income here, and tell you why I remain positive on the business.

Dear readers/followers,

It shouldn't be a surprise to you, after over 10 articles on the company since 2018-2019, that I am positive and bullish on Exchange Income Corporation (EIFZF). This gem of a company is one that I've pushed money into and never looked back. What's more, since my very first article here on SA, the investment has allowed me to significantly outperform the broader indexes, including the S&P500.

Exchange Income RoR (Seeking Alpha)

It's truly an argument for the benefits of conservative value investing, with an eye on the dividends. While the company's current yield is less than 5%, my own yield is over 8.5%, and that yield is paid on a monthly basis, much like a paycheck. My paychecks from Exchange Income are now at a non-trivial level, and the position is 2.5% of my overall portfolio.

It is the single largest non-IG rated and smaller-cap business I have in my holdings.

I also have no plans to sell Exchange Income - not in the least.

Let me show you why, and update my thesis for 2Q23.

Exchange Income Corporation - The upside remains, if smaller

Exchange Income is, by almost every perspective and context, and excellent business. To put it in any context or segment comp is hard because the company's revenue mix can't really be compared to anything out there. Most of the analytical sites and services put the company in transportation. This might be partially true, but the company's mixed exposure to manufacturing makes this almost moot. Furthermore, its structure makes comparisons on debt hard and inaccurate.

As an example, EIF is currently at a 1.75x debt to equity, which in the context of the sector is high, but when you look at the company's mix isn't that bad. It also hasn't impacted EIF's profitability in the least. The company is a very profitable business, and in terms of profitability over the past 10 years, is in the 99.98 percentile in the industry. Only 9 companies out of the nearly 1,000 compared in logistics have managed this sort of profitability in a 10-year period.

And profitability is what I look at. Its dividend yield might on a comparative basis be worse than almost at any time in its history given the valuation the company is at here. Still, it's also important to note that the company has seen impressive growth in its earnings and FFO, and is likely to continue to see that as they tack on and grow more of their business and operations.

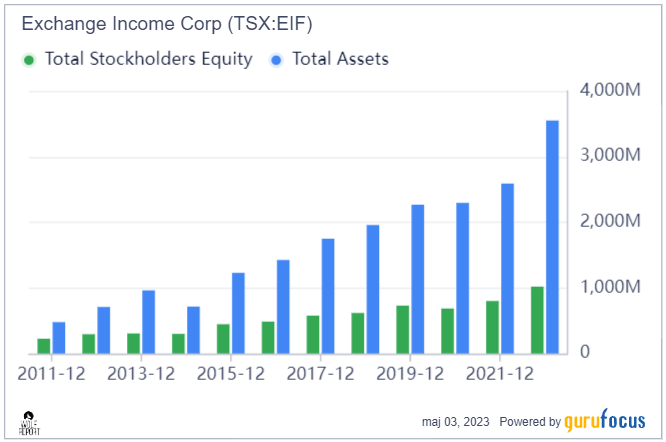

Exchange Income has been a very effective grower of shareholder equity and assets for the past decade.

Exchange Income SE/Assets (GuruFocus)

{kind=link}

Its overall top-line to bottom-line also shows a very attractive flow, with gross margins of almost 24%, operating in the double digits, and net margins of over 5%. Over the past few years, the manufacturing sector has become an integral part of Exchange Income, and I expect it to become 50% of the company's top-line mix within a few years if this pace of growth is continued.

And there is reason to believe the company will do this.

The company quite recently added to its portfolio Hansen Industries for over $40M - both through new shares and the use of the company's credit facility. Hansen is an industrial manufacturer with over 30 CNC-equipped machines producing components in several divisions, and this means that Exchange is now in a market-leading position in British Columbia.

This was a no-nonsense M&A by EIF, which pretty much went along the same line of thought we've seen from Mike Pyle and his colleagues for the past few years. The company has become apt at recognizing leadership, management, reputation, and operational excellence, and acquiring it at a good price.

Adding superior operations to its own lineup like this only makes Exchange Income more attractive in my eyes, and I've added a rough estimate of what I expect this company can bring to the table. 2022 was a decline in FFO/operating cash flow on a per-share basis, but I now expect at least $8.75/share for 2023, potentially as much as $9.1 depending on how the next few quarters go. Beyond that, I'm applying a 7% FFO growth rate as the company continues to expand.

We'll go into it more in the valuation section, but this really means that even at $52.3 on a CAD basis, this company still isn't massively overvalued.

I will say that if Exchange wasn't growing more, the company could be considered fairly valued here.

If there is a material change to the thesis following Q1, I will update this article. But for now, I expect the results in the first quarter to speak for themselves and be in line with what is expected here.

One of the core reasons I'm such a big investor in EIF is that I feel that management's own view is so aligned with my own. I've been in contact with IR for this company. And what impresses me, for the years I've been covering Mr. Pyle and his team is their almost obsessive focus on getting the right returns on their money. That's the same focus that I have, for every investment I make these days. It's really all that matters - can I see a good return for my money, on a conservative basis?

This has become harder with valuation the way it is. My latest PT for EIF was $58, but that's CAD. We're not there yet, but I want to make perfectly clear that this is the most you should pay for Exchange at this time. Even with the expected results for 2023, that's already part of this consideration.

I expect 1Q to bring very few surprises for this company. Despite COVID-19, Exchange has remained stable and cash flows have remained very attractive. The adjusted dividend payout ratios, which do need adjustment given the top-line and cost mix here with aerospace as part of operations, are conservative to a high degree - especially compared to how things looked during COVID-19.

For the basic operations and company profile, I refer you to my earlier articles on the company. I'm stating here that I believe the continued M&A to be accretive to the company's FFO and allow for EIF to continue to grow. I also believe that the company's average FFO growth rate for the next 3 years will be between 11-14% - that's somewhat below the FactSet estimate of over 16%, but more conservative is good here. Let's look at what this would do to the company's valuation.

Exchange Income - The valuation

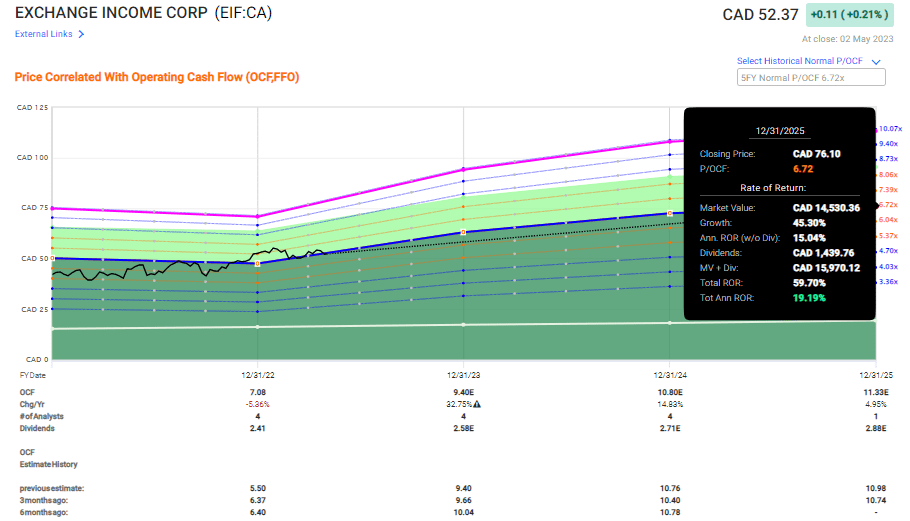

While this is not the most expensive we've seen the company trading at, Exchange Income is still, on the basis of normalized earnings/FFO, at a fair value/not overvalued level. The current share price relative to its earnings and forecasts puts it around 6.66x to OCF, which is just south of the 5-year average of 6.72x. Including the company's expected OCF growth rate of 11-14%, this comes to a conservative double-digit growth rate on such a forecast, and an even higher of almost 20% per year on a FactSet forecast of 6.72x for 2025E.

FA.S.T graphs Exchange Income Upside (F.A.S.T Graphs)

{kind=link}

This upside, at this point, is highly optimistic. And as you can see, from a historical perspective, it calls for Exchange income keeping premiums that we haven't seen the company hold consistently for some years. I believe the mix improvement might lead to a stabilization of income, but it won't reduce the overall cyclicality of the business. Though if you look at the company from a 10-year perspective, the business is surprisingly stable in terms of cash flows. Only 3 years with negative results, and those I would consider relatively trivial.

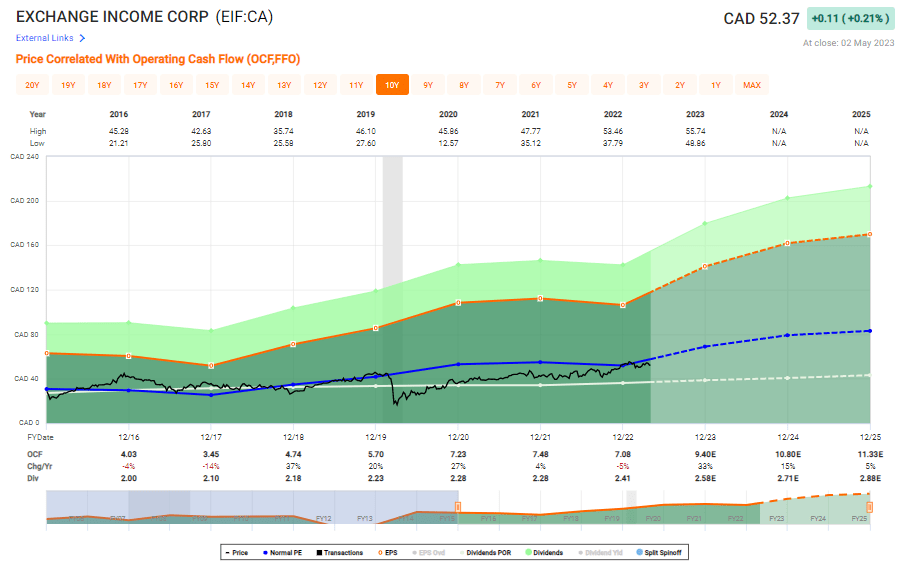

Exchange Income Valuation/Earnings (F.A.S.T graphs)

{kind=link}

So, the overall upside is still there - but at this point, I would consider it mostly driven by growth, not by reversal. I've personally mostly invested in Exchange income when it has been based on both growth and reversal, so this is somewhat new territory for me as well. The company's performance since my last article really showcases that we're now at a level where returns for this investment might not necessarily be positive, at least not always.

Seeking Alpha Exchange Income RoR (Seeking Alpha)

So it wouldn't be a completely crazy notion to entertain the idea of trimming or rotating here. In fact, I wouldn't call it "wrong" to do so, especially if you're sitting on as high a return as I am for portions of that investment.

The underlying case for the growth in FFO remains solid from an operational side. Talking risk, the problem is that the forecast accuracy for how these analysts have been able to estimate this company is low - a negative failure ratio of over 40% on a 1-year basis with a 10% margin of error. So there's some uncertainty here, and I don't see that this is necessarily going to improve things.

I already said in my last article that I saw signs of exuberance in the stock. This also includes analysts going higher and higher. Many disliked EIF as an investment when I called for it at $40/share, but they're now calling for it to be worth over $60/share. It's an interesting case with every value investment I make, and one I saw particularly relevant in Unum (UNM) when I bought it below $20/share.

The current price target for Exchange Income Corp from S&P Global comes to almost $ 64 CAD for the native EIF ticker. This is almost ridiculous considering that it was less than $50/share around 1.5 years back, and the company hasn't materially changed its operational profile or risk profile in that time. 11 analysts follow the company, more are at a "BUY" now at a higher price than they were when it was cheap. Back 1.5 years ago, 3 out of 11 were at "HOLD". Now no one is below an "Outperform".

It goes to show, and confirms to you, market psychology.

Well, I take a different approach. When a company reaches heights like this, I become more careful - not more exuberant.

While I am not yet at a point to declare this company "expensive", it's certainly no longer cheap.

Because of this, I'm at the following thesis.

Thesis

My thesis for Exchange Income is fairly simple.

- This is a small operator with a big upside. Fundamentals are solid, and I like their operations and their niche. At an attractive price, and for the right investor, this is a definite "BUY" at a $58 PT. I'm not changing this PT, because I don't see any reason for the time being to adjust it either down or up.

- Risks do exist, but they're on a more subjective and "what-if" level, with very few actual logical risks to the company's balance sheet or operations.

- My stance is a "Buy", but at this level, we're getting pretty close to the company being fully valued.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

EIF is no longer cheap, but it's still solid here.

For further details see:

Looking Back On Exchange Income Corporation, And My RoR