TOL - Lowe's Companies: Weathering Short-Term Pain For The Long-Term Gain

2023-06-28 13:37:40 ET

Summary

- Lowe's Companies is expected to face short-term challenges in 2023 due to factors such as the absence of an extra operating week, the sale of its Canadian operations, and a projected decrease in comparable store sales.

- The company is expected to benefit from a continued shortage of homes in the long run, despite short-term pain from inflationary pressures, high interest rates, and a potential slowing or shrinking economy.

- Despite the short-term challenges, Lowe's Companies' shares are not unreasonably priced given the size and quality of the enterprise.

In a perfect world, investing would be easy. But there are so many challenges that investors need to face day to day. For instance, what do you do when you have an investment prospect that looks attractive for the long haul, but that you know is going to experience some pain in the short term? This is a kind of question that I'm confronted with when I look at specialty retailer Lowe's Companies ( LOW ). Based on all the data currently available, the company looks attractively priced. It has a strong long-term catalyst that should fuel growth and increase profits down the road. But at the same time, there are certain headwinds that already are starting to affect the enterprise, and those same headwinds are almost certain to intensify as this year progresses. For those truly focused on the short term, which is not something I recommend, I do think a case could be made that taking a step away from the company might make the most sense at this time. But for anybody who's a long-term, value-oriented investor like myself, buying into the weakness makes a great deal of sense.

Short-term pain, long-term gain

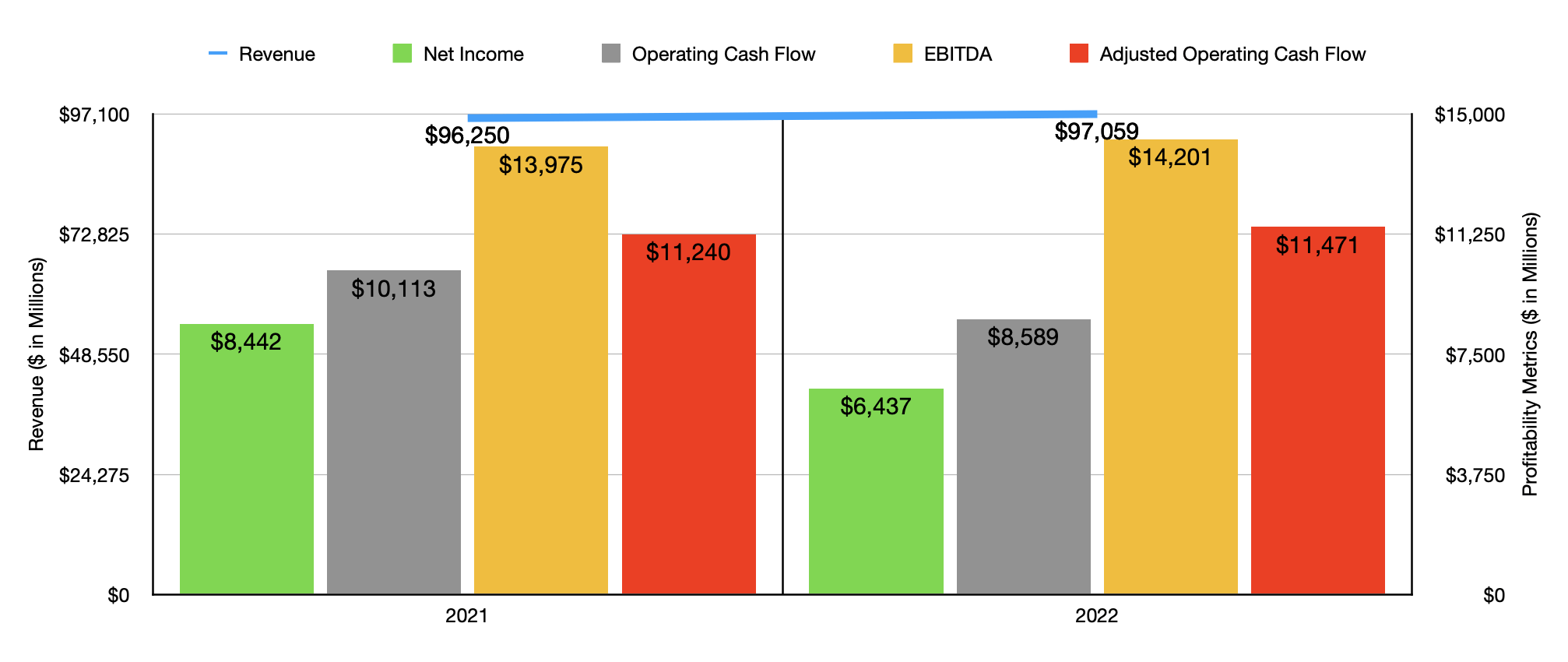

No matter how you stack it, the 2023 fiscal year is going to be an interesting time for Lowe's Companies. According to the most recent guidance provided by the company covering the 2023 fiscal year, revenue should come in between $87 billion and $89 billion. That's down from the prior expected range of between $88 billion and $90 billion. In addition to representing a downward revision compared to what the company previously anticipated, it also represents a sizable decline compared to the $97.06 billion that the business generated in 2022.

{kind=link}

There are multiple reasons behind this drop. For starters, there were 53 operating weeks during the 2022 fiscal year. So the company is suffering from the absence of that extra week this year. In addition, the company sold off its Canadian operations in January of this year for $491 million. This was instrumental in bringing the number of locations in operation down from 1,971 at the end of 2021 to 1,738 at the end of last year. There's also the expectation that comparable store sales would decline, with management targeting a decrease of between 2% and 4% relative to the same time last year.

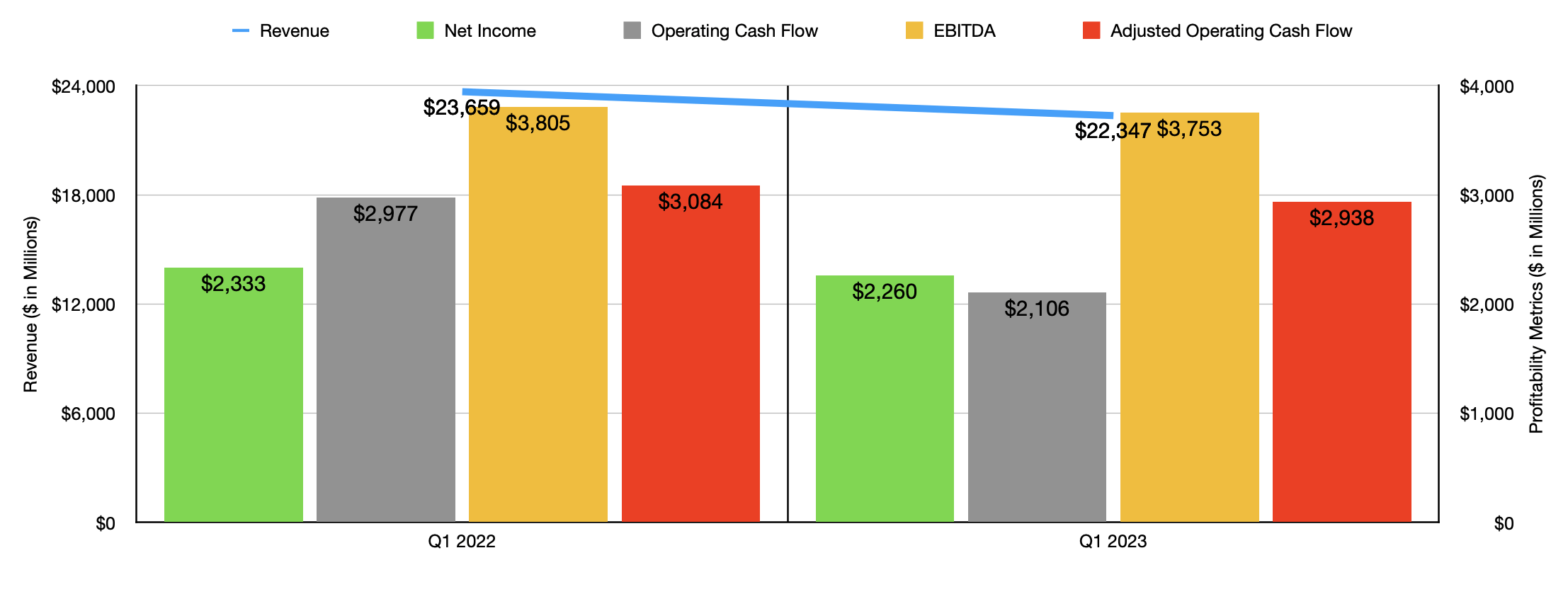

Earnings guidance is a bit tricky with the company because they only provide adjusted earnings per share estimates. But these also were revised lower from between $13.60 per share and $14 per share, down to between $13.20 per share and $13.60 per share. At the midpoint, this would translate to adjusted earnings of about $8 billion. However, if we look at data covering the first quarter of 2023 compared to the first quarter of 2022, net profits declined from $2.33 billion to $2.26 billion. This came as revenue dropped from $23.66 billion to $22.35 billion. Similarly, the cash flow metrics provided by management also are showing year-over-year declines.

{kind=link}

The weakness that the company is already experiencing for 2023 has been driven largely by a $1.2 billion hit associated with the absence of its Canadian retail business. Seasonal fluctuations helped to offset this by about $735 million. But that didn't stop comparable store sales in the first quarter from dropping 4.3%, driven by a 4% drop in comparable customer transactions and a 0.3% drop in comparable average ticket sizes. Management said that they saw strength in some key areas, largely those associated with its "Pro" customers. But the company also said that it experienced significant pain in the lumber category thanks to commodity price deflation that more than offset volume increases.

{kind=link}

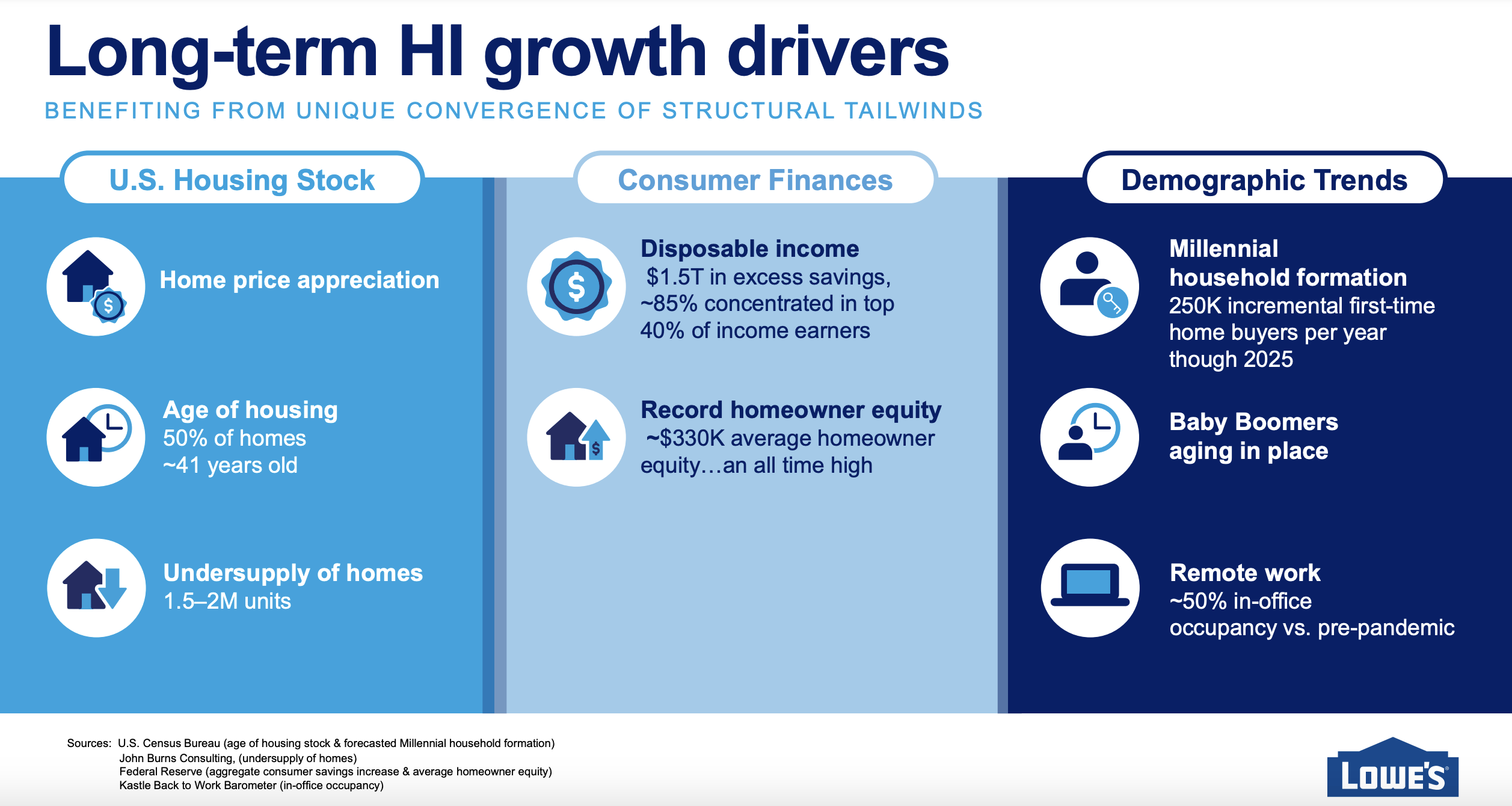

In its financial statements, Lowe's Companies makes very clear that its health is tied significantly to the health of the housing market. Long term, both it and rival Home Depot ( HD ) are optimistic about what the future holds in this space. In its investor presentation from December of last year, management talked about multiple drivers that should prove bullish for the company in the long run. For instance, according to management, home price appreciation has worked in the company's favor, in part because it has elevated average homeowner equity values. The company estimated that the average amount of equity in a home in the US was about $330,000. If that's accurate, it would mark an all-time high.

{kind=link}

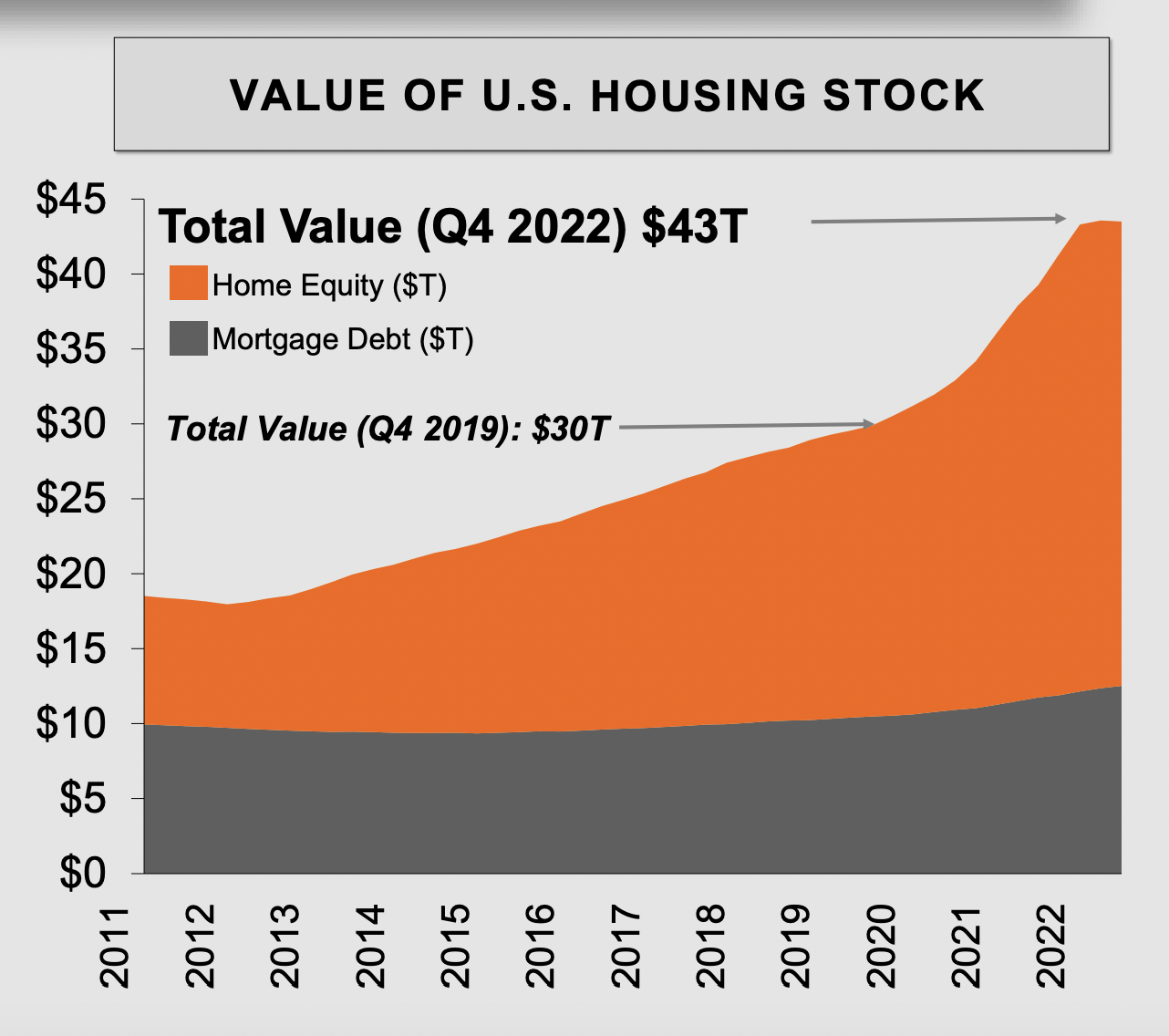

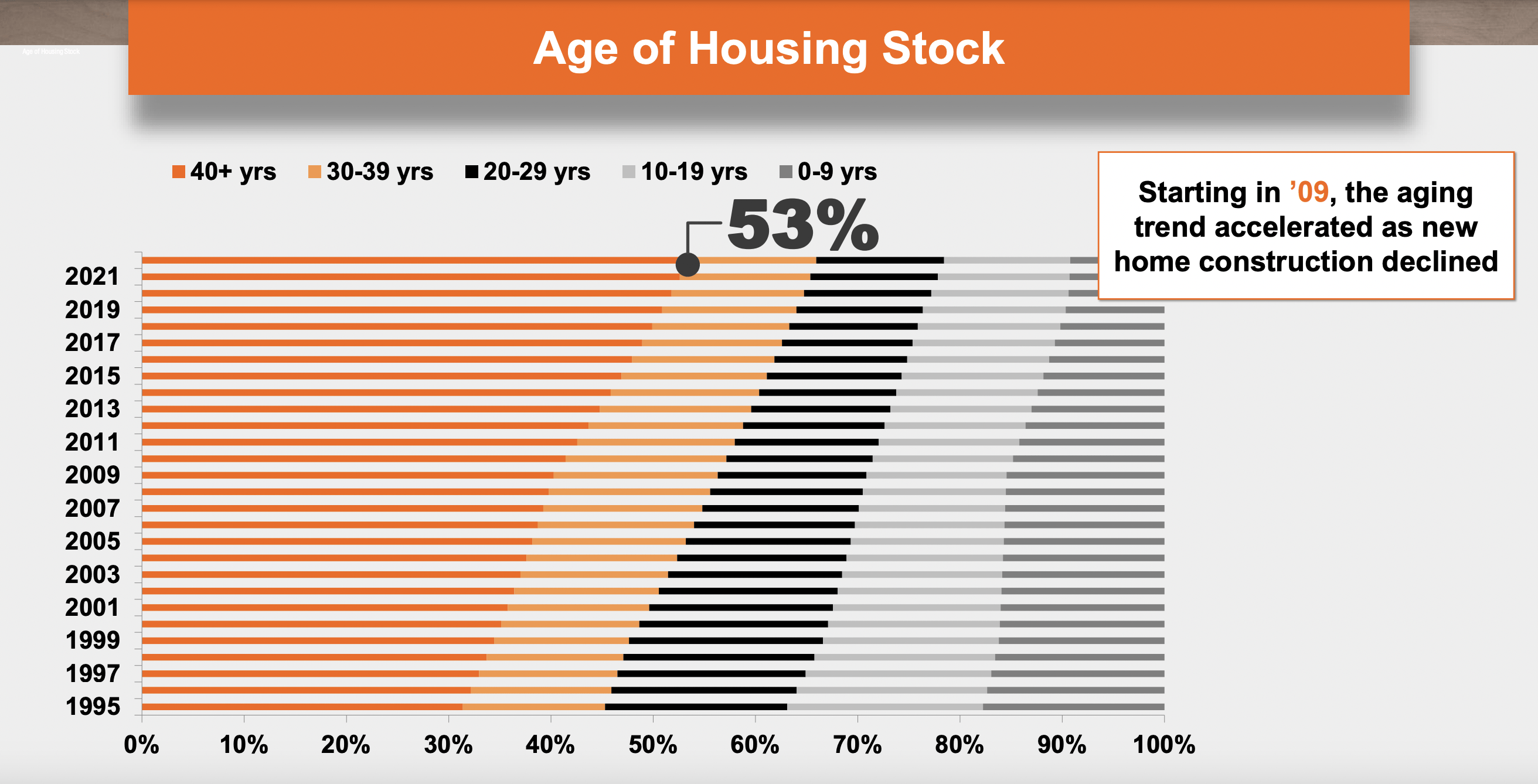

Home Depot presented very similar data regarding this. By the final quarter of 2019, there was an estimated $30 trillion worth of home equity built into the total value of US housing stock. By the final quarter of last year, this number had grown to $43 trillion. The specialty retailer also estimated that, in 2022, about 53% of all homes in the country were 40 years old or older. Of the homes that do have mortgages, 80% have locked in fixed rates of less than 5%. When combined with $1.5 trillion in estimated excess household savings, that creates a lot of opportunity for homeowners to invest in repair and maintenance activities for their homes. This is made further likely, according to Lowe's Companies, by the fact that there has been a significant shift in remote work. This shift exposes homeowners to their homes with greater regularity since they're literally working from them. And this should increase the probability that they will find reasons to invest in changes throughout said homes.

{kind=link}

| Company |

| Current Backlog |

| Backlog 1 Year Ago |

| Annual Change |

| KB Home ( KBH ) |

| 7,286 |

| 12,331 |

| -40.9% |

| Taylor Morrison Home Corporation ( TMHC ) |

| 6,267 |

| 9,400 |

| -33.3% |

| Meritage Homes Corporation ( MTH ) |

| 3,922 |

| 6,695 |

| -41.4% |

| Century Communities ( CCS ) |

| 1,920 |

| 5,247 |

| -63.4% |

| Beazer Homes USA ( BZH ) |

| 1,858 |

| 3,121 |

| -40.5% |

| PulteGroup ( PHM ) |

| 13,129 |

| 19,935 |

| -34.1% |

| Toll Brothers ( TOL ) |

| 7,733 |

| 11,302 |

| -31.6% |

| NVR, Inc. ( NVR ) |

| 10,411 |

| 13,443 |

| -22.6% |

| D.R. Horton ( DHI ) |

| 19,237 |

| 33,859 |

| -43.2% |

In addition to benefiting from this kind of catalyst, the company also should benefit, in the long run, from a continued shortage of homes. This is something I touched on when I last wrote about Lowe's Companies in a different article that I published in February of this year. However, there's certain to be a good deal of short-term pain. In addition to inflationary pressures, high interest rates, and a potential slowing or shrinking economy, all likely to create headwinds for the repair and maintenance space, I know that those same factors will also negatively impact the construction of new homes as well. Taking data from a prior article , and updating it for with one company that has recently announced updated financial results, I was able to create the table above and the table below. As you can see, backlog figures and orders for new homes have plummeted over the past year. Cancellation rates are sky-high when it comes to new residential construction.

| Company |

| Current Orders |

| Orders 1 Year Ago |

| Annual Change |

| KB Home |

| 3,936 |

| 3,914 |

| 0.56% |

| Taylor Morrison Home Corporation |

| 2,854 |

| 3,054 |

| -6.5% |

| Meritage Homes Corporation |

| 3,487 |

| 3,874 |

| -10.0% |

| Century Communities |

| 2,022 |

| 2,944 |

| -31.3% |

| Beazer Homes USA |

| 1,181 |

| 1,291 |

| -8.5% |

| PulteGroup |

| 7,354 |

| 7,971 |

| -7.7% |

| Toll Brothers |

| 1,461 |

| 2,929 |

| -50.1% |

| NVR, Inc. |

| 5,888 |

| 5,927 |

| -0.7% |

| D.R. Horton |

| 23,142 |

| 24,340 |

| -4.9% |

It's my opinion that all of this will create additional short-term pain, not only for Lowe's Companies but also its rivals. But the good news is that, once this pain is weathered, we should see pent-up demand help to push financial results for the companies in this space even higher. After all, just because the economy goes through a rough patch and home builders see a temporary decrease in demand, does not mean that we won't experience a continuously growing population and the need to keep up the homes that we live in.

{kind=link}

I can understand why some investors might want to take a step back from Lowe's Companies and firms similar to it. In the short term, the financial pain might be uncomfortable. But if you look at the long run, the company has some attractive catalysts. To make matters even better, shares don't look unreasonably priced given the size and quality of the enterprise. Based on my estimates for the 2023 fiscal year, net income for the company should come in at around $6.24 billion. Adjusted operating cash flow should be around $10.93 billion, while EBITDA should be approximately $14.01 billion. As you can see in the table below, shares of the company, even using the more expensive forward estimates as opposed to the slightly more attractive 2022 figures, look cheaper than Home Depot does, using two of the three valuation metrics that I utilized.

| Company |

| Price/Earnings |

| Price/Operating Cash Flow |

| EV/EBITDA |

| Lowe's Companies (2022 Figures) |

| 19.6 |

| 11.0 |

| 11.2 |

| Lowe's Companies (2023 Estimates) |

| 20.2 |

| 11.5 |

| 11.4 |

| The Home Depot |

| 18.3 |

| 18.4 |

| 13.1 |

Takeaway

Fundamentally speaking, Lowe's Companies looks to be going through a bit of a rough patch. This is not surprising to me at all. In the near term, that pain will almost certainly persist. It may even worsen from here. Those who are focused on short-term gains might be best off divesting their shares. But this is not a strategy I recommend. As a long-term investor, I believe that buying into this weakness might be the best approach at this time. This is especially true when you consider how shares are priced, not only on an absolute basis but also relative to its only significant publicly traded rival.

For further details see:

Lowe's Companies: Weathering Short-Term Pain For The Long-Term Gain