CA - Lundin Gold: Another Year Of Successful Reserve Replacement

2023-09-21 08:34:07 ET

Summary

- Lundin reported another year of successful reserve replacement at Fruta del Norte.

- Meanwhile, it continues to have one of the better reserve per share trends sector-wide, with limited share dilution since 2019 and successful replacement of mined depletion.

- In this update, we'll look at how its reserves (grade/size) stack up vs. other large producers and if the stock has moved into a low-risk buy zone.

It's been a volatile past year and a half for the Gold Miners Index ( GDX ), with the index struggling to make any upside progress and continuing to trade in a 2 steps forward, 1.8 steps back fashion. However, Lundin Gold ( LUGDF ) has certainly been an exception since I highlighted the stock as a Buy at US$6.25 or lower , more than doubling off its lows at its recent high and holding onto most of its gains. This can be attributed to the company's flawless operational execution and steady grade outperformance vs. expectations, with grades coming in 5% above modeled levels from a reconciliation standpoint last year, and output hitting a record high at ~476,000 ounces.

However, like any great high-grade production growth story like Red Lake, Fosterville, Pogo, and Meikle, the best grades eventually taper off and we see a significant production cliff if new high-grade discoveries can't replace the bonanza grade material. Fortunately, Lundin's Fruta del Norte benefits from relatively high tonnage at above average grades compared to most mines today (~18.0 million tonnes at ~8.7 grams per tonne of gold), and the company's recent drilling success suggests upside to the south with the property wide open from a regional standpoint as well. In this update, we'll look at the most recent reserve update and whether the stock is getting closer to a buy zone after its ~30% correction.

Fruta del Norte Operations - Company Website

{kind=link}

All figures are in United States Dollars unless otherwise noted.

Reserves & Resources

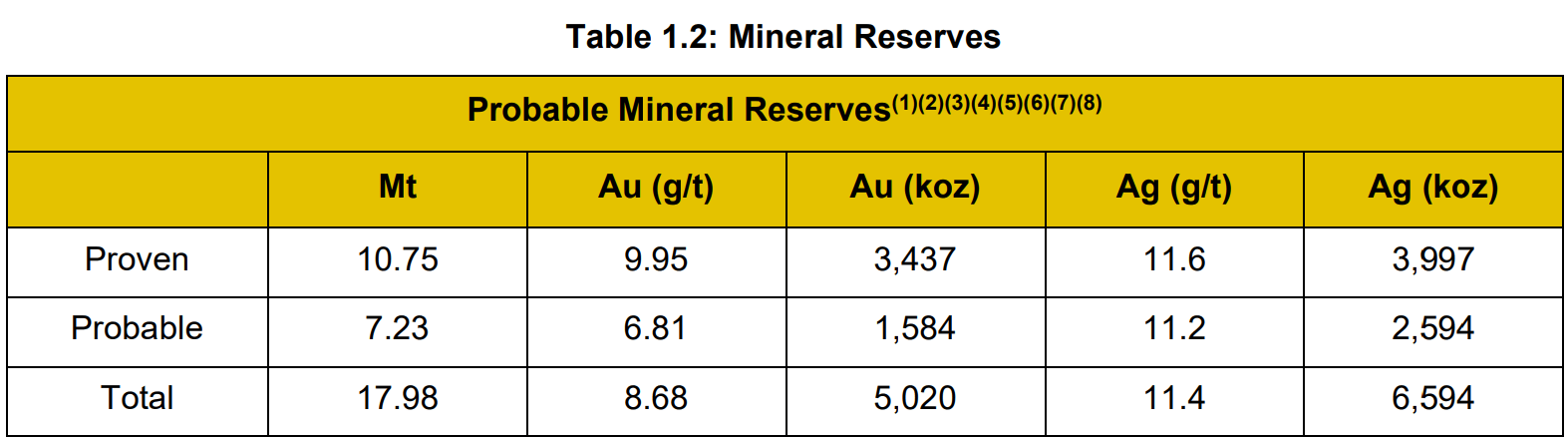

Lundin Gold ("Lundin") released its updated Reserves & Resources earlier this year and has followed this up with multiple positive exploration updates, in addition to the news that it would be further increasing its drill program despite maintaining its upwards revised budget due to improved field productivities. As it stands, Lundin's reserve base stands at ~5.02 million ounces at year-end 2022 at an average grade of ~8.7 grams per tonne of gold, making it one of the top-15 highest grade mines on a reserve basis sector-wide, and certainly one of the largest, with most 5.0+ million ounce high-grade deposits in the portfolios of senior producers, not mid-caps like Lundin. Meanwhile, the company's resource base is just as impressive, finishing the year, with ~8.5 million ounces (~6.8 million ounces in M&I category). Importantly, this reserve and resource is based on a conservative gold price assumption of $1,400/oz and $1,600/oz, respectively.

Lundin Gold Reserves - 2022 TR

{kind=link}

Looking at the reserve base below, reserves are based on a cut-off grade of 4.2 - 5.0 grams per tonne of gold for transverse stopping and drift and fill, respectively, and the reserve price has increased only marginally from the $1,350/oz used in the 2016 FS before construction began. Just as impressively, Lundin has managed to grow its reserve base by ~5% after mining depletion of ~1.2 million ounces, a very impressive feat especially given that grades have remained relatively stable at ~8.7 grams per tonne of gold vs. ~9.7 grams per tonne of gold previously. This supports an 11-year mine life with average annual production of ~412,000 ounces, significantly above the ~340,000 ounce production profile envisioned in 2016 given the successive increases to the planned throughput rate.

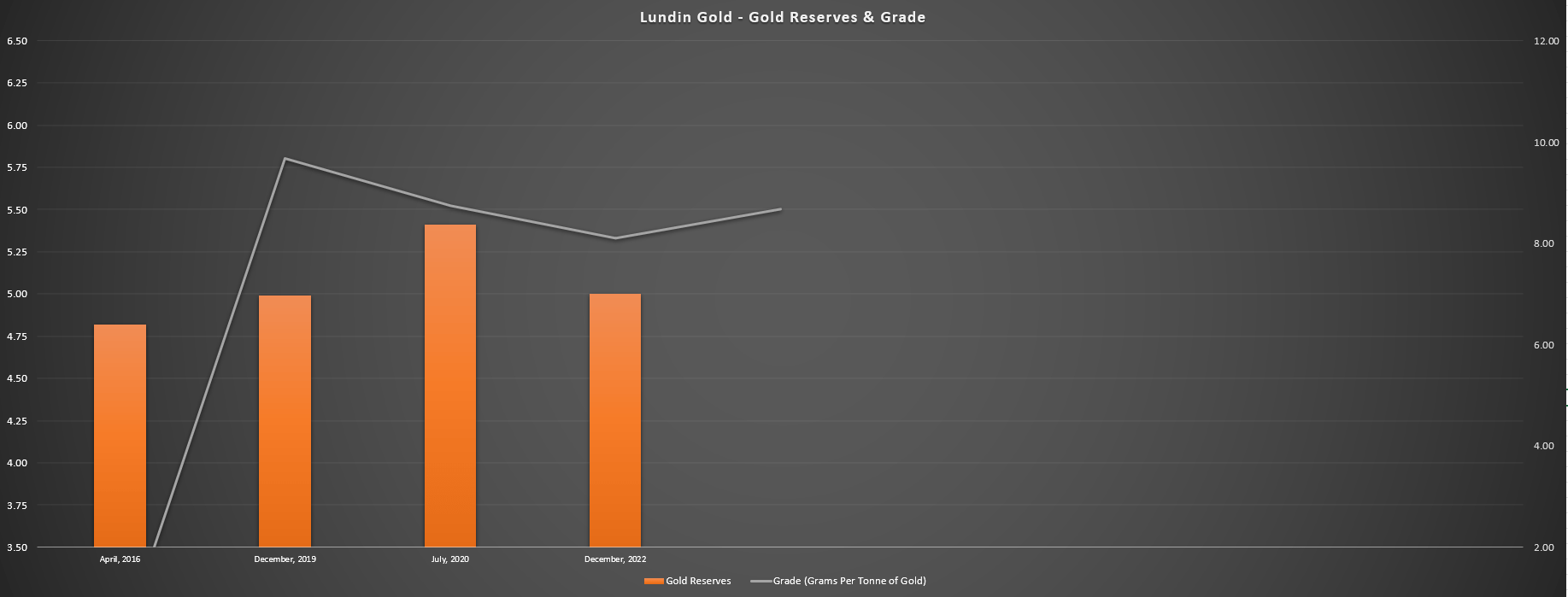

Lundin - Gold Reserves & Grade - Company Filings, Author's Chart

{kind=link}

Lundin Gold has noted that it is looking at a potential expansion to 5,000 tonnes per day, which would translate to peak production closer to ~500,000 ounces per annum.

Reserves Per Share

While reserve growth for any miner is important, the real metric investors should be watching is reserve growth per share. This is because while many companies may be successful maintaining or growing their reserve base, this is meaningless if the share count is growing at a much faster pace, which in many cases is due to overpriced and ill-timed M&A. One example of a company that has grown reserves successfully through exploration and timely acquisitions is Agnico Eagle ( AEM ), but for every Agnico there are 10 producers failing to grow this metric, with examples including Coeur Mining ( CDE ), First Majestic Silver ( AG ), Kinross Gold ( KGC ), and Jaguar Mining ( JAGGF ), among many others.

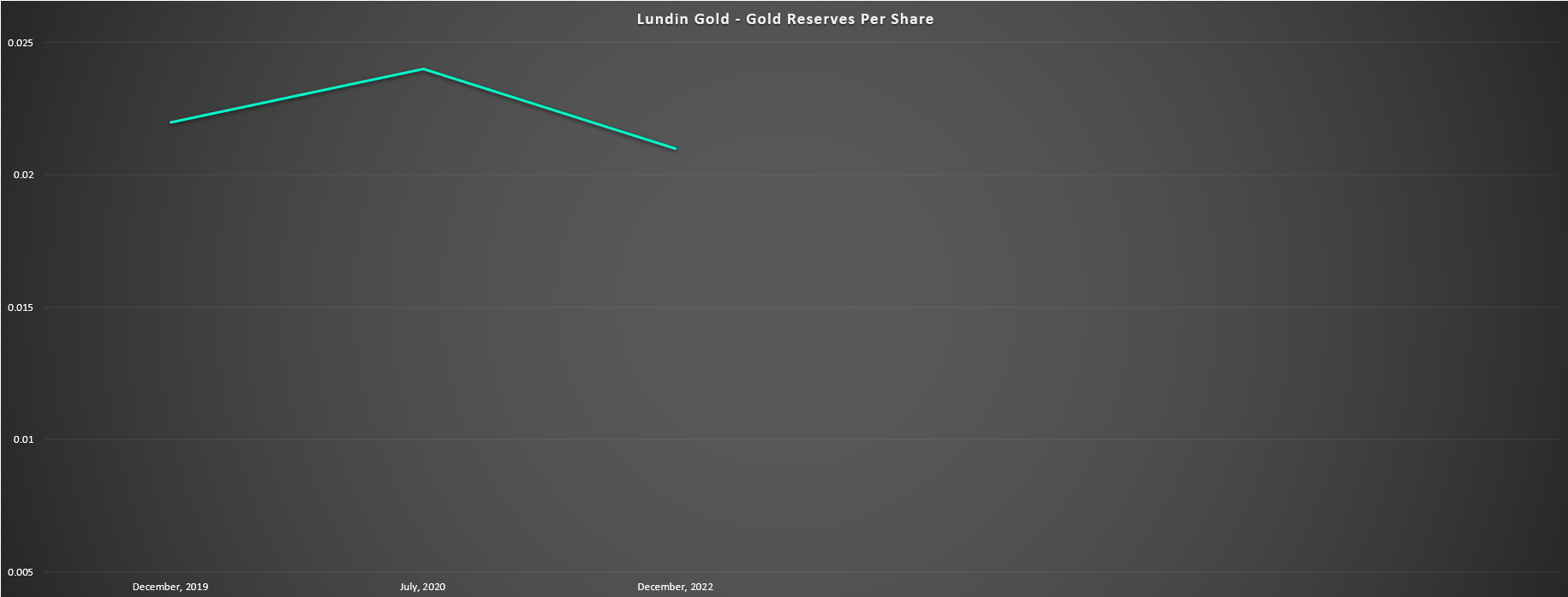

Lundin - Gold Reserves Per Share - Company Filings, Author's Chart

{kind=link}

As the chart above shows, Lundin Gold may not be growing this metric given that it has seen its share count has increased ~7% since year-end 2019 while reserves have remained flat, it has done a solid job of holding the line here, especially given the difficulty of replacing ~450,000 ounces per annum of high-grade gold. And while the company looks like it should be able to add another 800,000 to 1.5 million ounces of gold given its near-mine exploration success, conversion drilling and step-outs to the south, this still replaces just ~30% of its reserve base at the high end. Hence, I am surprised that the company has not used M&A as a tool to grow reserves and diversify, especially with the company not operating in a Tier-1 ranked jurisdiction (Canada, United States, Western Australia). And while the company's currency is less favorable than when I noted it was likely to make a double top near US$14.00 , its currency is still favorable relative to most companies it might look to acquire (smaller high-margin producers or high-grade developers).

Resource Upside

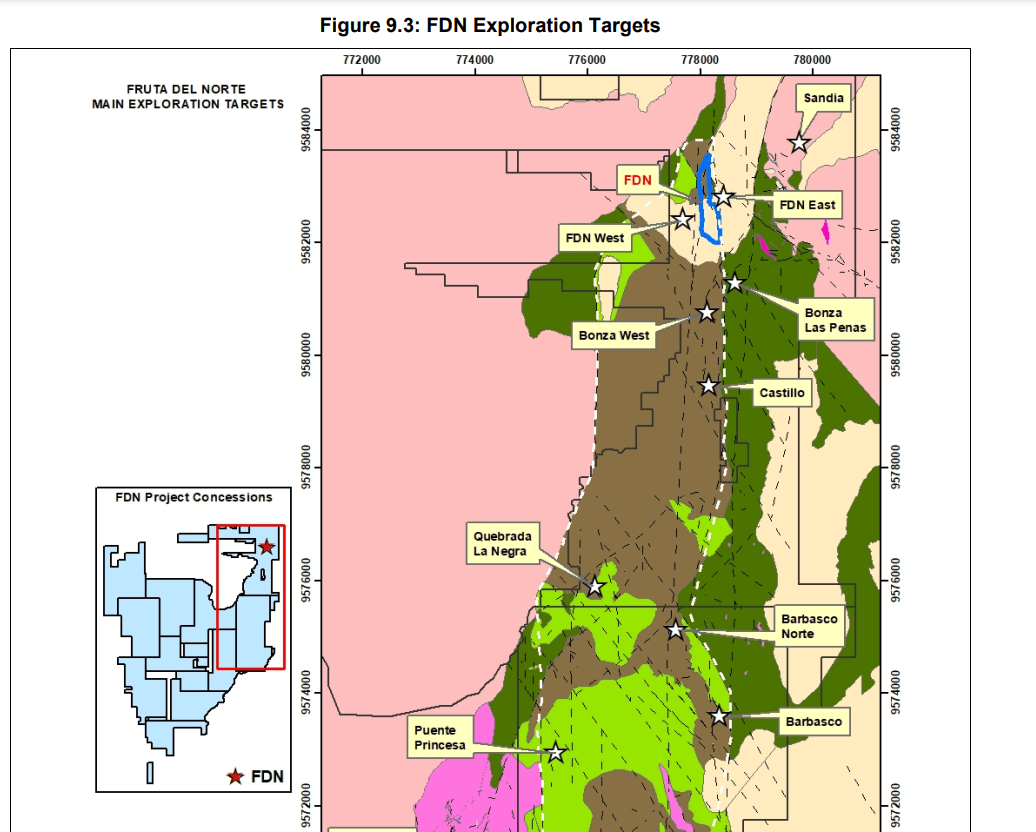

Moving to resource upside, Lundin Gold has had a decent year from an exploration standpoint, and it has multiple potential regional untapped opportunities given its district land package (~64,000 hectares). These regional opportunities on the southern portion of the Suarez Basin include Barbasco, Barbasco Norte, Puente Princesa and Quebrada La Negra where the company hasn't made hit anything overly exciting yet, while there are other targets outside of the Suarez Basin that include Emperador, Chanchito, Roble and Gata Salvaje (17 kilometers and 13 kilometers south of Fruta del Norte, respectively). And while no major intercepts have been released from Barbasco since it was drilled in 2021, the company had some success stepping out directly south of its mine, with promising intercepts at Castillo and Bonza Sur, with the latter being a 1.2 kilometer long soil geochemical anomaly directly southeast of FDN South and where it's conducting its conversion drilling program to move inferred ounces into higher confidence categories.

Fruta del Norte & Regional Targets - 2023 TR

{kind=link}

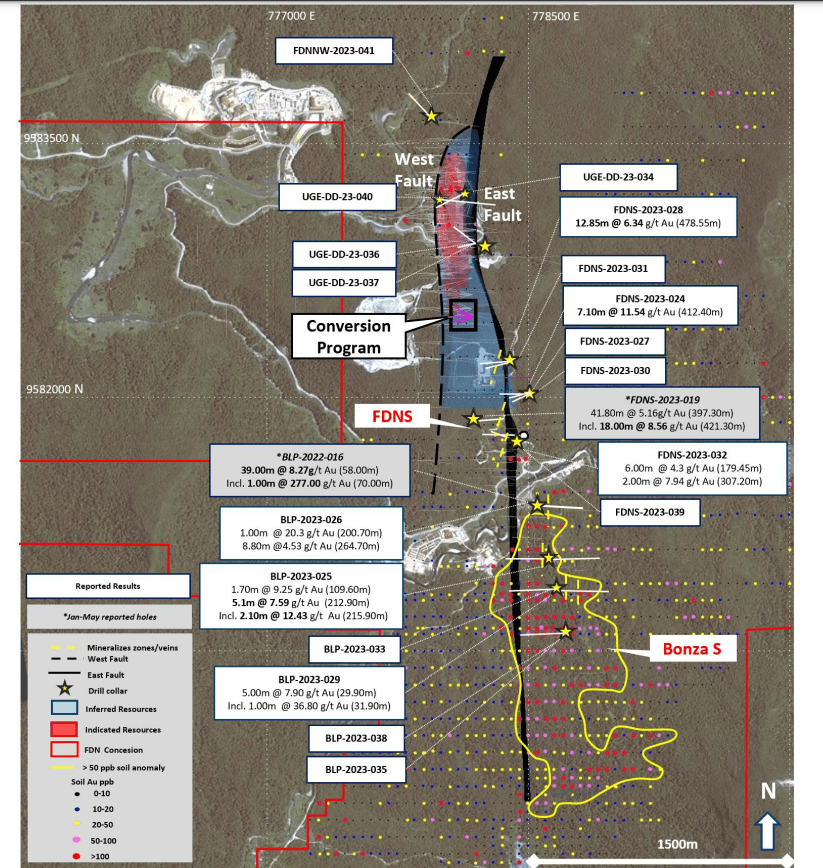

As shown in the below drill map, the company's drill program has delivered high-grade results to the south and at depth from the Fruta del Norte resource area, and the further step out hits to the south are promising. Some decent intercepts include 30.3 meters at 5.11 grams per tonne of gold, 8.1 meters at 4.4 grams per tonne of gold, 23.0 meters at 4.11 grams per tonne of gold. Meanwhile, Bonza Sur delivered two impressive intercepts of 39 meters at 8.27 grams per tonne of gold, 5.0 meters at 7.9 grams per tonne of gold and 3.5 meters at 46.98 grams per tonne of gold, while Castillo hit 2.0 meters at 12.14 grams per tonne of gold. However, while impressive, these are not FDN Main caliber still results yet, even if many of the hits south of Fruta del Norte are above the cut-off grade for mining and point to further resource growth.

Recent Drilling Highlights - Company Website

{kind=link}

Valuation & Technical Picture

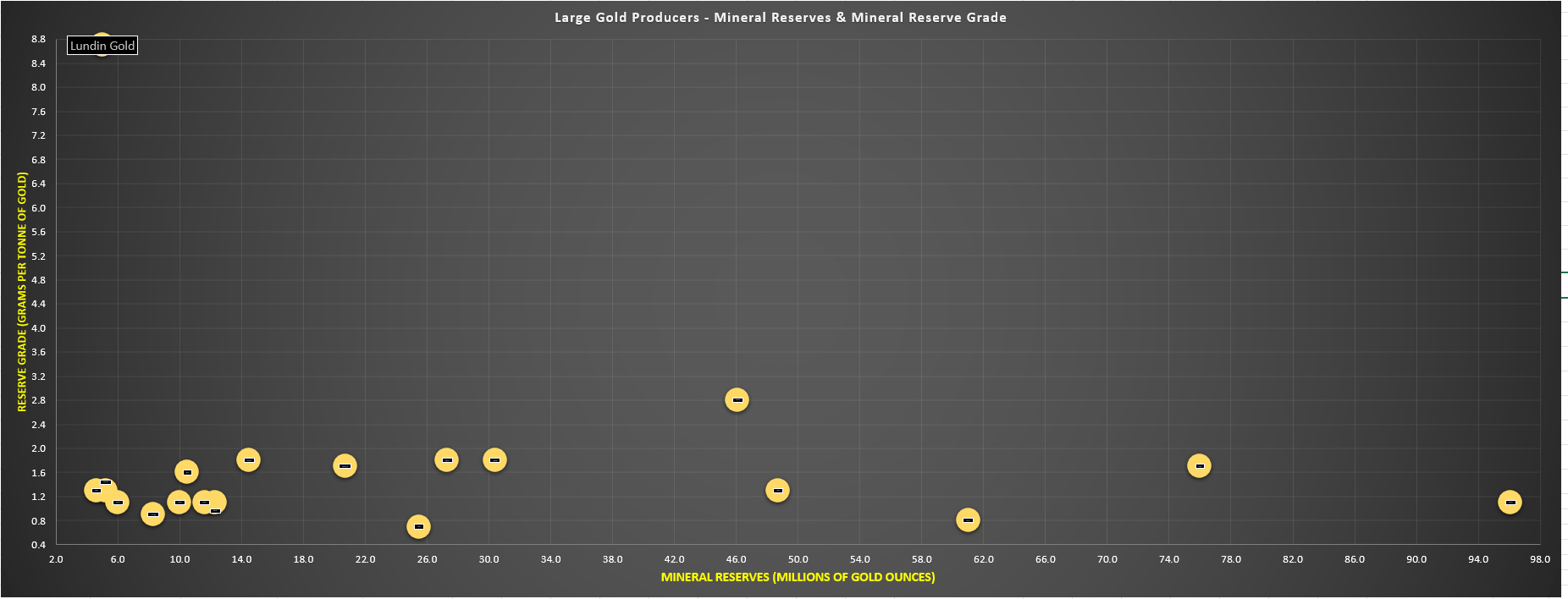

Lundin Gold trades at a market cap of ~$2.90 billion and an enterprise value of ~$3.02 billion at a share price of US$12.10, more than double the market of some other mid-tier producers (300,000 to 450,000 ounce production profiles), which would make the stock seem expensive at first glance. However, Lundin Gold stands out among its peer group of both mid-tier producers and senior producers, with an unrivaled reserve grade among large producers that is a massive outlier vs. its peers. Of course, the company benefits having just one asset vs. average reserve grades being divided by multiple assets for most other producers. Still, Fruta del Norte is one of a kind with ~5.0 million ounces of high-grade gold, and it's a deposit that keeps on giving from a discovery standpoint, suggesting that Lundin Gold should command a premium multiple.

Large Gold Producers - Mineral Reserves & Mineral Reserve Grade - Company Filings, Author's Chart

{kind=link}

However, while Lundin Gold easily ranks as a top-10 gold producer on quality (track record of over-delivering on promises and having a world-class gold asset), I continue to see Lundin Gold as less attractive from a relative value standpoint. This is because it trades at over 1.0x P/NAV while several million-ounce producers that are diversified trade at similar or lower levels. And while it remains reasonably valued from a P/CF standpoint, I don't see enough margin of safety with an ideal buy zone of US$9.30 or lower vs. its estimated fair value of US$14.30 (required 35% discount to fair value). Plus, this view is corroborated by the technical picture, with Lundin remaining in the upper portion of its 1-year range and still not confirming a technical buy signal. Finally, its relative value is less attractive given its outperformance.

Obviously, I could be wrong and Lundin Gold may have already bottomed, and as the stock has proven in the past, it beats to its own drum with massive outperformance vs. the Gold Miners Index (~90% return vs. ~30% return for GDX in the past year). Still, I prefer to buy when a stock is hated and trading at a deep discount to fair value, not simply reasonably valued, and this is not the setup for Lundin Gold today. And while there's no guarantee that the stock trades back to US$9.45, there are an abundance of other opportunities sector-wide at very attractive P/CF and P/NAV multiples. Hence, although I see Lundin as one of the sector's best buy-the-dip candidates, I continue to see more compelling reward/risk setups elsewhere.

So, what would change my mind?

If Lundin Gold was to make a major regional discovery of a similar caliber to Fruta del Norte like the initial drill results we saw coming out of Aurelian, this would be a major development and I would be more than willing to adjust my fair value on the stock. This is because this might support a second stand-alone mine on the property in a best-case scenario, or if they found a mini FDN, this could support a further plant expansion to push production well above the 525,000 ounce level consistently and support a longer mine life. That said, while I am cautiously optimistic that its district scale land package will yield another multi-million ounce deposit, finding a second FDN won't be easy.

Still, for those that want to keep their eyes peeled for signs that Lundin is onto something big, Fruta Del Norte 1.0 (Aurelian Resources, 2006) started with the intercepts shown below in bullets, and any intercepts near this thickness at similar grades or better from a regional standpoint would suggest the company has a proverbial sturgeon on their hook.

- Hole 51: 204 meters at 8.40 grams per ton of gold

- Hole 57: 189 meters at 24.0 grams per ton of gold

- Hole 58: 255 meters at 12.55 grams per ton of gold

- Hole 59: 195.7 meters at 5.97 grams per ton of gold

- Hole 63: 215.9 meters at 10.12 grams per ton of gold

- Hole 100: 250 meters at 35.2 grams per ton of gold

- Hole 139: 158.40 meters at 25.21 grams per ton of gold

- Hole 151: 140.45 meters at 16.91 grams per ton of gold

- Hole 152: 216.6 meters at 12.85 grams per ton of gold

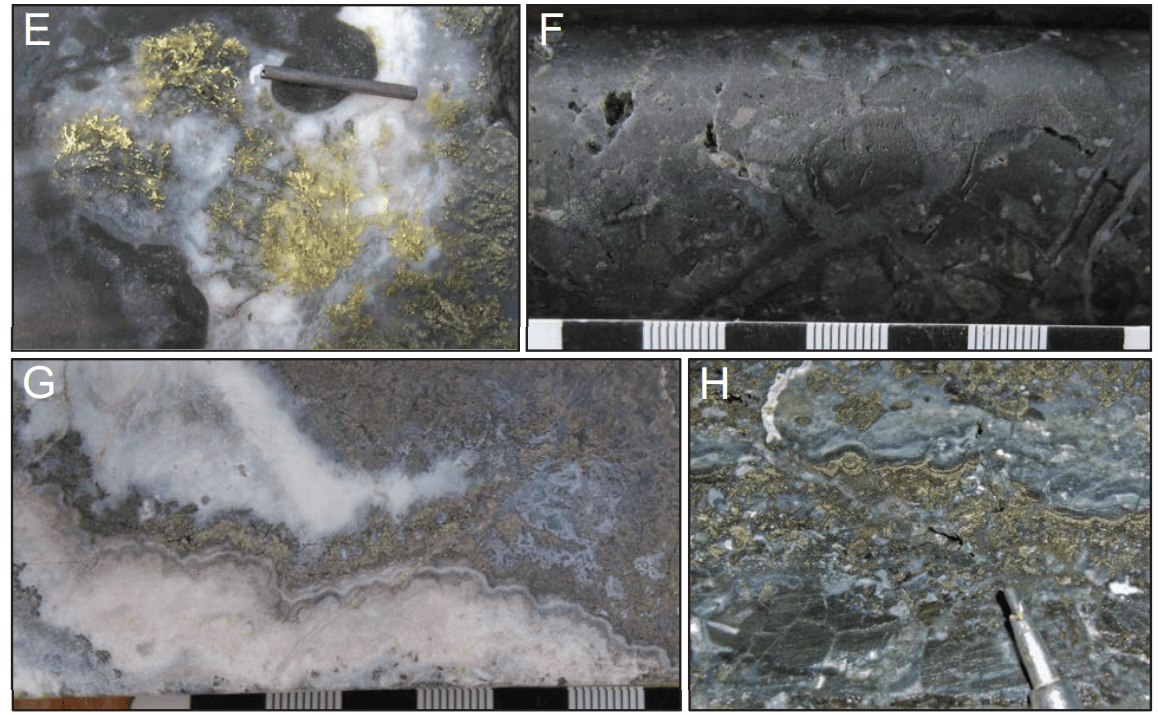

Fruta Del Norte Drill Core - Discovery, Geology & Origin of the FDN Epithermal Gold Silver Deposits, S. Leary, R. Sillitoe, P. Stewart, K. Roa, B. Nicolson

{kind=link}

Summary

Lundin Gold is somewhat of a unicorn in a sector filled with several companies that consistently disappoint and dilute shareholders at every turn. For starters, it consistently over-delivers on its promises, has steadily grown its gold production and production per share , and is mostly holding the line on reserves per share despite pushing out over 420,000+ ounces of high-grade gold per year, a similar level to Fosterville which eventually hit a steep production cliff. Simultaneously, it is miles ahead of its peer group from a shareholder returns standpoint (~3.5% dividend yield), and investors get the bonus upside of a potential new discovery on the company's massive land package in Ecuador with multiple gold and even porphyry targets. In summary, I see Lundin Gold as one of the better ways to get exposure to the gold price if it goes back on the sale rack, and I would view any pullbacks below US$9.30 as buying opportunities.

For further details see:

Lundin Gold: Another Year Of Successful Reserve Replacement