CA - Lundin Gold: On Track To Potentially Beat 2023 Output Guidance

2023-07-09 04:53:11 ET

Summary

- Lundin Gold reported a 16% increase in gold production in Q2, pushing its year-to-date production to 60% of its guidance midpoint.

- Hence, it's on track to deliver at or above the top end of 2023 guidance even after baking in a softer H2 ahead (lower grades and recoveries).

- That said, and despite the exceptional performance, I still don't see enough margin of safety here and think it's tough to justify paying up for the stock above US$12.30.

Just over six weeks ago, I wrote on Lundin Gold ( OTCQX:LUGDF ), noting that while it was one of the best-run producers sector-wide, there was no way to justify chasing the stock above US$13.00 on valuation and that any rallies above US$14.15 would provide an opportunity to book additional profits. Since its brief push above the US$14.15 level, the stock has suffered a 24% drawdown, resetting its very extended chart. However, the company has delivered another monster quarter from Fruta del Norte in Q2 and could beat the top end of its guidance range even if H2 will be softer than H1. In this update, we'll dig into the preliminary Q2 results and see whether the stock has dropped into a low-risk buy zone following its recent correction:

All figures are in United States Dollars unless otherwise noted.

{kind=link}

Q2 Production

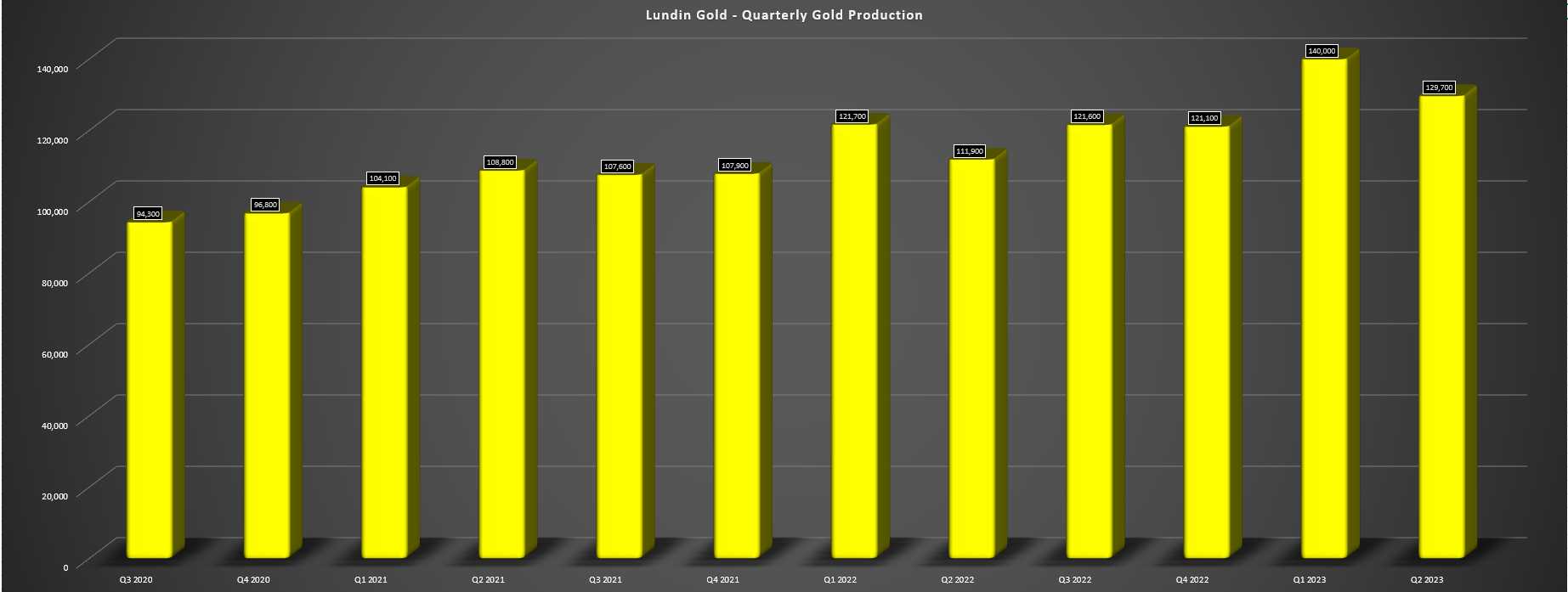

Lundin Gold released its preliminary Q2 results last week, reporting another blowout quarter with gold production of ~129,700 ounces, a ~16% increase from the year-ago period. This has pushed the company's year-to-date gold production to ~269,700 ounces, tracking at ~60.0% of the company's guidance mid-point of 450,000 ounces and ~56.8% vs. the top end of guidance of 475,000 ounces. So, while Lundin Gold is expecting lower recoveries in Q3 (Q2: 88.0%), the company looks to be in a solid position to deliver above the top end of guidance, with average production of just ~103,000 ounces needed in the next two quarters to beat the top end of its 2023 production guidance range. And while Q2 through Q4 should be higher cost quarters with increased sustaining capital offset by fewer ounces produced, Lundin looks to be positioned to easily beat its cost guidance mid-point as well ($905/oz).

Lundin Gold - Quarterly Gold Production (Company Filings, Author's Chart)

{kind=link}

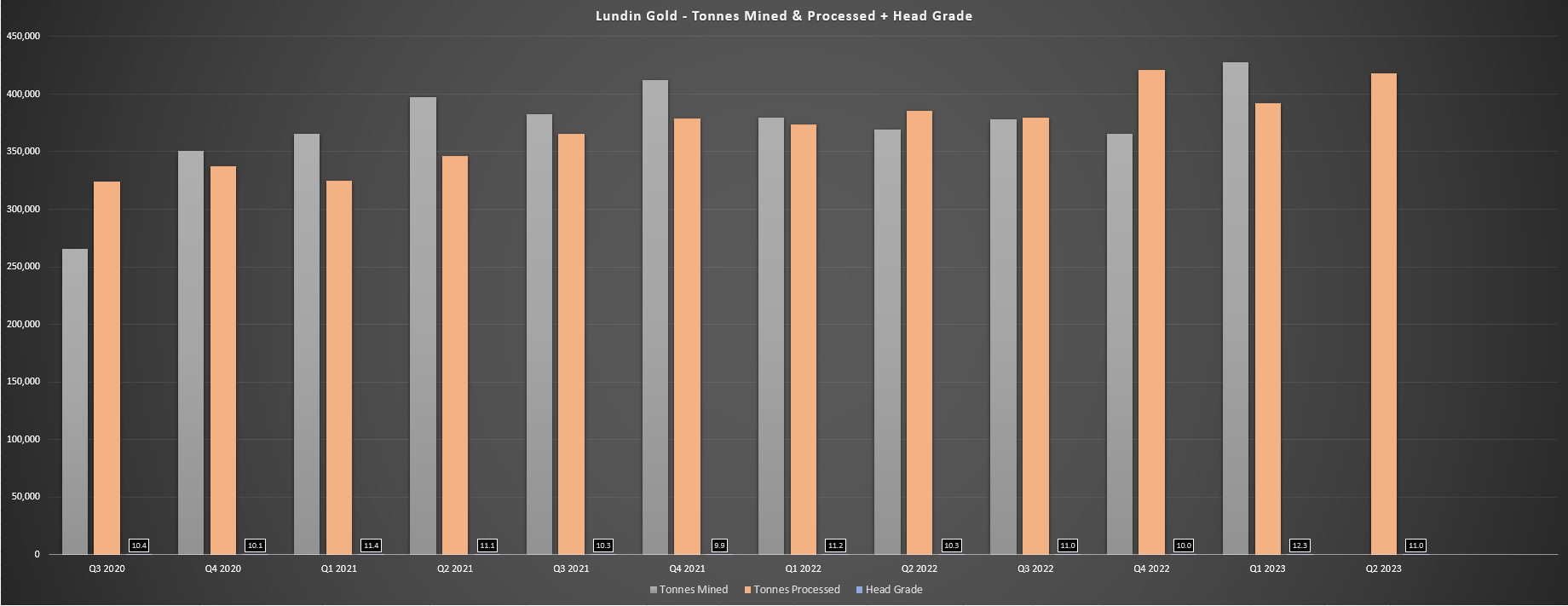

Digging into the company's Q1 results a little closer, Fruta del Norte's mill throughput has remained elevated and well above initial design of 3,500 tonnes per day, averaging 4,598 tonnes per day in Q1 or ~418,400 tonnes per day for the quarter. This near-record throughput combined with higher grades year-over-year (11.0 grams per tonne of gold vs. 10.3 grams per tonne of gold) that were above plan contributed to a phenomenal quarter, and helped to offset a dip in recoveries because of changes in ore type and the impact of oxidation on its coarse ore stockpile. This should help Lundin Gold to report another sub $850/oz AISC quarter in Q2 even with a step up in sustaining capital spend (fourth tailings dam raise), maintaining its profile as one of the lowest-cost producers sector-wide, just behind Orla Mining ( ORLA ), another single-asset producer that operates out of Zacatecas State in Mexico.

Lundin Gold - Tonnes Mined & Processed + Head Grade (Company Filings, Author's Chart)

{kind=link}

That said, while I expect another impressive Q2 report from a financial standpoint with an average realized gold price north of $1,940/oz and all-in sustaining cost margins of $1,100/oz or better, H2 could look much different, especially if the company ends up reporting an average head grade of less than 10.0 grams per tonne of gold for the year, which is above its initial guidance of ~9.7 grams per tonne of gold. In fact, if we assume slightly lower recoveries of 87.9%, total mill throughput of ~825,000 tonnes and a more normalized head grade of 8.6 grams per tonne of gold in H2, we would see H2 production of ~200,000 ounces of gold, a material step down from the ~269,700 ounces produced in H1. And while these are still exceptional results that place Lundin Gold well ahead of nearly all other single-asset gold producers, we are likely to see a material dip in sequential revenue and margins from Q2 to Q3.

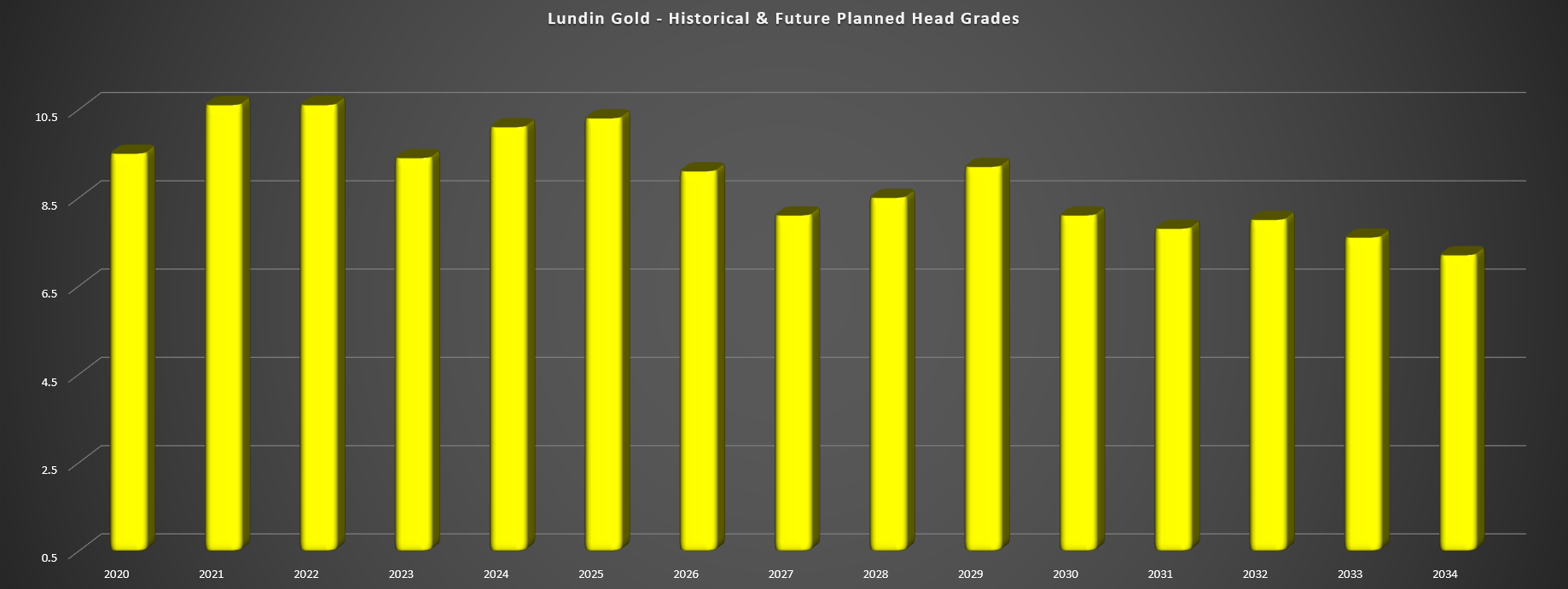

For investors treating Lundin Gold as a long-term investment, the expected dip from Q2 to Q3 is hardly an issue, and the company appears confident that it can increase throughput to 5,000 tonnes per day, besides potential improvements in recovery. The company noted at its Investor Day that it has installed a pilot Jameson Cell to potentially recovery finger gold not picked up in the flotation circuit and is working to improve recoveries through optimal blending. As for the plant expansion, the basic engineering work is expected to be completed this year and if the expansion were approved, this would be a low capex investment to boost overall throughput by over 10% helping to offset the gradual decline in grades expected post-2025 (shown below).

Lundin Gold Mine Plan - Historical & Future Planned Head Grades (Company Technical Report)

{kind=link}

5k TPD Expansion & Recent Developments

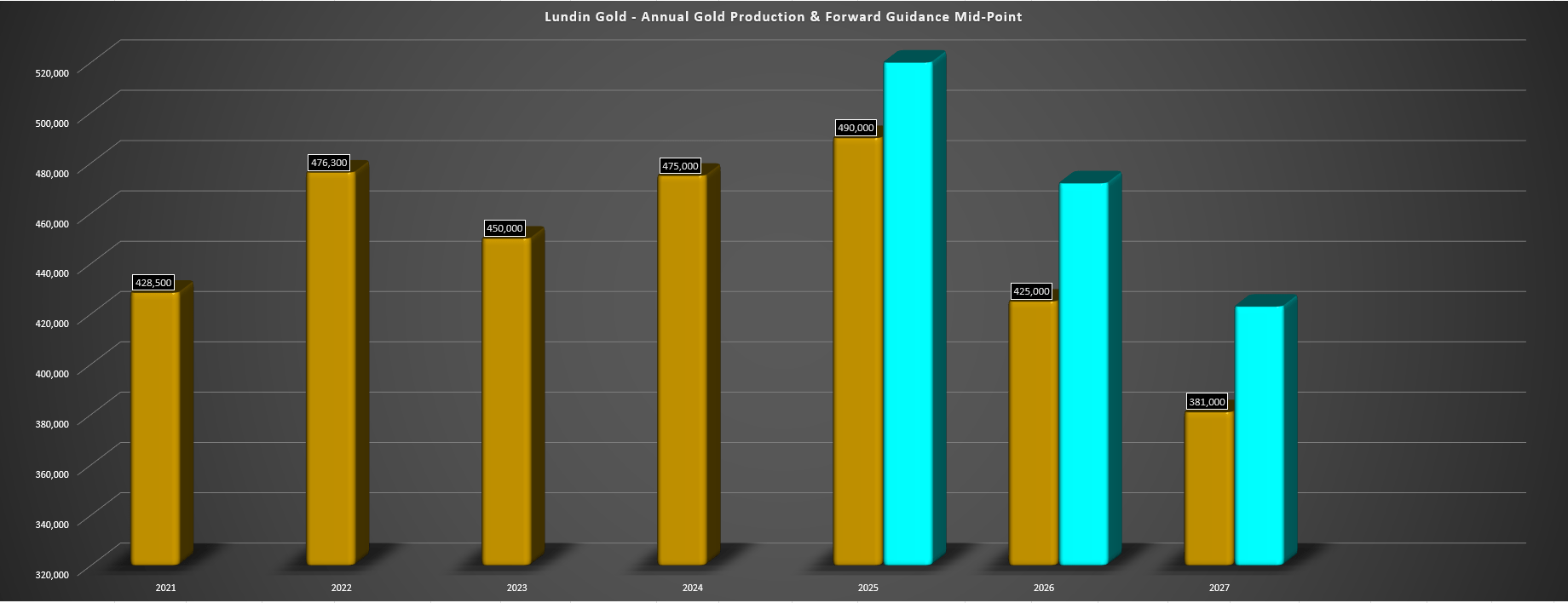

Looking at Lundin Gold's production profile below, we can see that gold production is expected to average ~472,000 ounces at the guidance mid-point from 2023 to 2025 before dropping off materially in 2026 and 2027. Given the company's ability to over-deliver on promises which suggests that the actual forward 3-year average is likely closer to 490,000 ounces (ex-mill expansion), this drop-off will be even more significant, with grades slipping to 9.1 and 8.1 grams per tonne of gold in 2026 and 2027, respectively, resulting in a material decline in overall production. And while new higher-grade near-mine discoveries could certainly improve this grade profile a little if they can be developed in a timely manner, it's no surprise that Lundin is looking at how to maintain a ~450,000-ounce production profile for longer, with a mill expansion offering one low-hanging opportunity to buttress its production profile.

Lundin Gold - Actual Annual Gold Production, Guidance Midpoint (2023-2025), Mine Plan (2026-2027) & 5k TPD Expansion Potential (2026, 2027) (Company Filings, Author's Chart)

{kind=link}

As the chart above shows, a 5k TPD expansion (~1.82 million tonnes per annum) would lift FY2025 production above 500,000 ounces and result in average production of ~450,000 ounces in 2026 and 2027, a significant improvement from the ~403,000 ounces expected under the current mine plan. This is certainly a major improvement, and if the company is able to find an accretive target to acquire given that it's open to M&A, this would also help to smooth out the declining production profile post-2025 depending on if it acquires a growing producer or an advanced-stage gold developer. That said, even without M&A, the production profile will benefit materially from the 5K TPD Expansion assuming it's approved, with possible further gains if the company can continue to improve its recoveries at Fruta del Norte.

The other positive news for Lundin Gold is the gold price, which just spent a record 17th week closing above the $1,900/oz level, which should result in year-over-year margin expansion despite the potential for similar unit costs on a year-over-year basis due to increased sustaining capital. In fact, if we assume a $1,970/oz gold price in Q2 2023 and AISC of $850/oz, Lundin Gold's AISC margins would improve to $1,120/oz, an ~8% improvement year-over-year. So, while Lundin is expecting a higher-cost year in FY2023, the better than expected H1 2023 production could help the company to deliver in the low end of its guidance range ($870/oz to $940/oz) and be among the top-5 lowest-cost producers sector-wide this year, which continues to contribute to the stock's premium multiple.

Let's take a look at the valuation below:

Valuation & Technical Picture

Based on ~242 million fully diluted shares and a share price of US$12.30, Lundin Gold trades at a market cap of ~$2.98 billion and an enterprise value of ~$3.22 billion. This is certainly an improvement from when it traded at a ~$3.7+ billion enterprise value briefly in May at its all-time highs, and it certainly helps that the company put up another solid quarter and the gold price continues to hold the $1,900/oz level, increasing the probability of the company generating over $430 million in operating cash flow this year. That said, this still represents a premium to its estimated net asset value of ~$2.80 billion. And even for the best producers sector-wide, it's rare for single-asset producers to consistently trade at a premium, especially if the assets are not in Tier-1 ranked jurisdictions (Australia, United States, Canada).

{kind=link}

Assuming a fair multiple of 1.1x P/NAV and 9.0x cash flow and using a weighted valuation of 65% assigned to P/NAV and 35% assigned to P/CF, we arrive at a fair value for Lundin Gold of US$14.00. And while this fair value estimate points to a 13% upside from current levels, I do not believe in buying precious metals stocks simply because they have decent upside potential. These are risky and volatile stocks with depleting assets that do not have pricing power and are at mercy to the gold price, and while we've seen only positive surprises from Lundin to date, the odd negative surprise does come along. For this reason, I require a minimum 35% discount to fair value to justify buying single-asset producers, which carry higher risk, even if they are being consistently over-delivering on promises, like we've seen from Lundin Gold under its CEO Ron Hochstein.

If we apply this required 35% discount to fair value to an estimated fair value of US$14.00, the ideal buy zone for Lundin Gold to bake in an adequate margin of safety comes in at US$9.10 or lower, significantly below current levels. And while this doesn't mean that the stock must drift back to this level, I prefer to buy stocks when they have a significant margin of safety in place, and I believe in paying in paying the right price or passing entirely. So, while there is no disputing that Fruta del Norte is one of the best assets sector-wide, and one could argue that Lundin Gold is a top-5 gold producer given its near flawless execution and ability to trounce guidance (even in previously difficult environments with above-average inflation and COVID-19 related staffing headwinds), I simply don't see any way to justify paying for the stock.

This could be an opportunity cost, but as Joel Greenblatt says: "there's no investing without valuation" . For this reason, I continue to focus on names trading at deeper discounts to fair value elsewhere.

Summary

Lundin Gold continues to fire on all cylinders and is one of the few examples of a "sleep-well-at-night" gold producer, given that it continues to surprise to the upside operationally. Plus, from a geological standpoint, there are few land packages sector-wide with more upside potential given that the company has a ~64,000 hectare land package (including earn-in agreement of ~15,700 hectares with Newcrest) that surround its ultra high-grade Fruta del Norte Mine in the Zamora Copper-Gold Belt. That said, the company's best two quarters of the year are in the rear-view mirror, and the market is typically forward looking, suggesting that while Lundin will post a blowout Q2 report, H2 could be softer and the company will need some cooperation from the gold price to trade up to fair value.

Meanwhile, we've seen several stocks battered elsewhere in the sector, and while they may not have Lundin's glowing 2-year track record of over-delivering on promises, they are trading at dirt-cheap valuations, and a low bar to beat because of easier comps has set some of these names up for outperformance, with one example being Pan American Silver ( PAAS ) which trades at lower FY2024 free cash flow multiple than Lundin Gold with a diversified business and a phenomenal pipeline (Escobal, La Arena Sulphide, MARA [62.5%], La Colorada Skarn). So, with Lundin remaining in vogue and not offering enough margin of safety, I see far better opportunities elsewhere in the sector. That said, if the stock were to decline below US$9.90 where it drops towards key technical support, I would consider this a low-risk buying opportunity.

For further details see:

Lundin Gold: On Track To Potentially Beat 2023 Output Guidance