CA - Lundin Gold: Set Up To Beat Upward Revised Guidance

2023-10-17 10:01:21 ET

Summary

- Lundin Gold had a softer Q3 report on the back of lower grades and recoveries and planned mill maintenance in the period.

- That said, LUGDF is on track to beat the top end of FY2023 guidance even with a mediocre quarter in Q4 and this is on its already upward revised guidance.

- In this update, we'll dig into the Q3 results, why a beat vs. the top end of guidance looks likely, and whether the stock is worthy of investment.

We're just one week away from the start of the Q3 Earnings Season for the precious metals sector and one of the most recent names to report its preliminary results was Lundin Gold ( LUGDF ). From a headline standpoint, the numbers may have looked softer than some had hoped, with output down 8% year-over-year and well below Q1 and Q2 levels. However, the company was up against tough comparisons on a sequential and year-over-year basis, lapping what was a tie for a record-quarter in Q3 2022, and a slight dip in throughput with a planned SAG mill liner change in the period. That said, Lundin Gold ("Lundin") is still set up to beat the top end of its already upward revised guidance even with a mediocre Q4, and this would mark yet another record year for the company. Let's inspect a little closer below:

{kind=link}

All figures are in United States Dollars unless otherwise noted.

Q3 Production & Sales

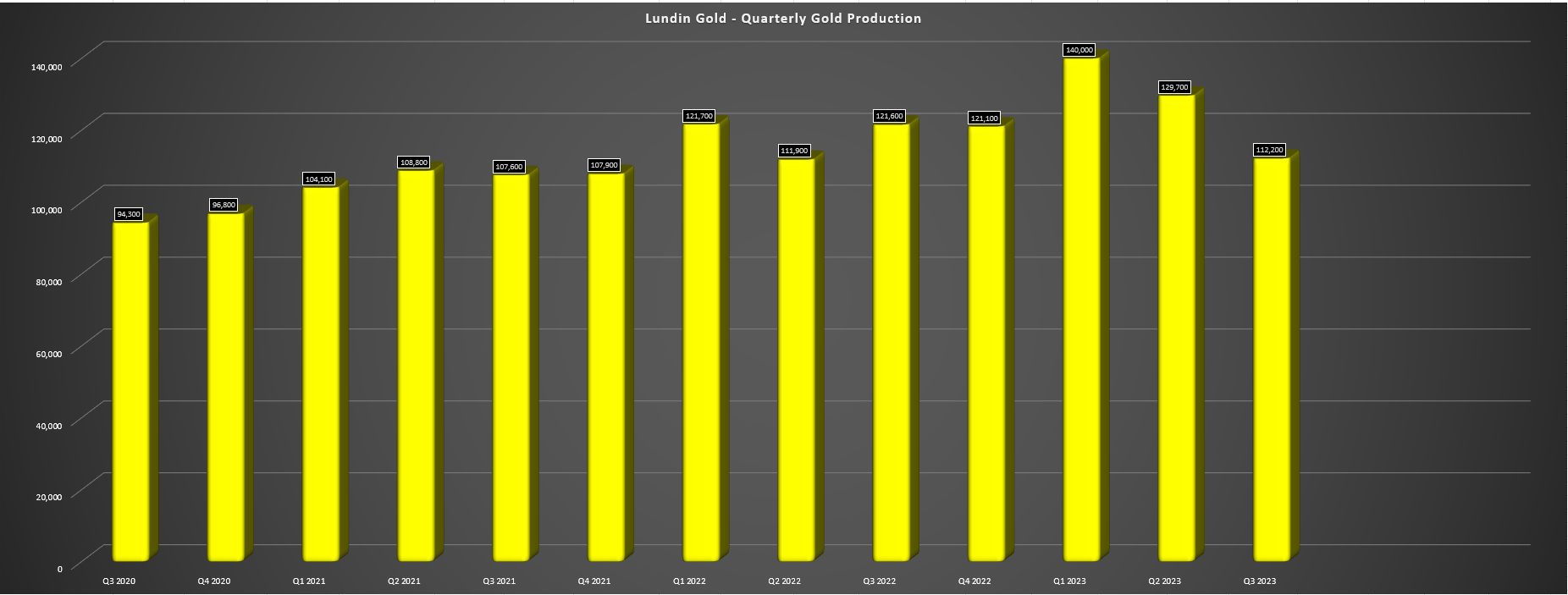

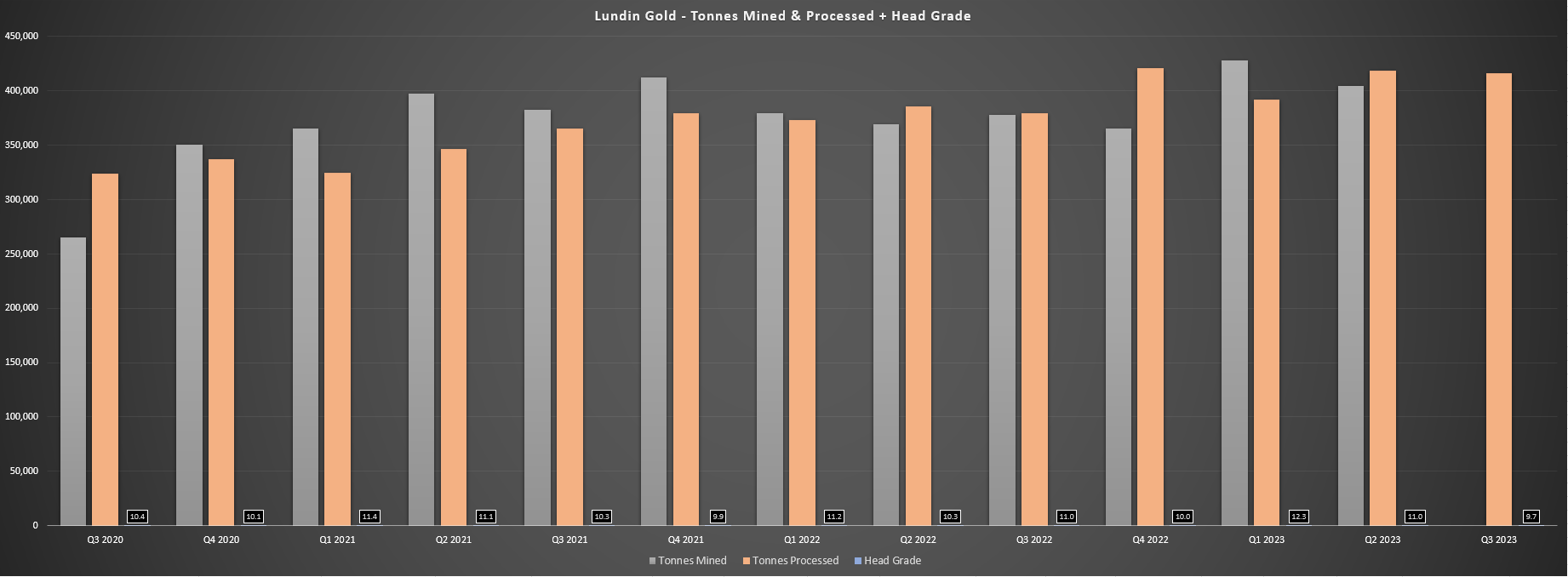

Lundin Gold released its Q3 results last week, reporting quarterly production of ~112,200 ounces of gold, an 8% decline from the year-ago period and a ~14% decline sequentially. This sharp decline in production was related to lower grades of 9.7 grams per tonne of gold (Q2 2023: 11.0 grams per tonne of gold), and fewer tonnes processed (~416,100 tonnes vs. ~418,700 tonnes) with the company not benefiting from being able to sprinkle high-grade stockpiles on top of its mined material like it did in H1-2023. However, this was still a phenomenal quarter with an annualized production rate of ~450,000 ounces of gold, well above the average annual production initially envisioned in its 2016 Feasibility Study. Besides, mill throughput was affected by scheduled maintenance in the period and recoveries came in a little lighter than I expected at 86.5% (Q3 2022: 90.3%).

{kind=link}

Lundin Gold - Quarterly Gold Production - Company Filings, Author's Chart

{kind=link}

Fruta del Norte Throughput & Grades - Company Filings, Author's Chart

Although the results might be disappointing to some investors and were certainly a drop-off, it's important to note that year-to-date production is currently sitting at ~81.7% of the company's already upwardly revised FY2023 guidance (450,000 to 485,000 ounces) and is sitting at ~78.7% of the top end of guidance based on ~381,900 ounces produced year-to-date. And according to the company in its Q2 2022 Conference Call, it expected grades mined in Q2 (9.0 grams per tonne of gold) to be similar to what we see in H2 2023. So, if we assume throughput of ~414,000 tonnes in Q4, an average grade of 9.2 grams per tonne of gold (balancing the slight dip in grades in Q3), and recoveries of 87.0%, Lundin could produce ~106,500 ounces of gold, placing it above the top end of its FY2023 guidance range. Hence, I don't think a beat on the top end of guidance is out of the question at all, and in a market where few names in this sector can consistently over-deliver on promises, Lundin stands out as somewhat of a unicorn.

Recent Developments

Moving over to recent developments, the price of gold may have come off over the past few weeks, which certainly is a thorn in the side of relatively high-cost and more sensitive producers like Argonaut Gold ( ARNGF ), Harmony Gold ( HMY ), Iamgold ( IAG ) and Equinox ( EQX ), at least ahead of the latter two's ramp-up of their shared Tier-1 scale operations next year. That said, a $100/oz move lower in the gold price hardly phases a high-margin producer like Lundin Gold that looks set up to report sub $850/oz all-in sustaining costs this year, or $1,000/oz plus margins even if we assume gold hangs out near its recent lows for the rest of the year. So, while the recent weakness in the gold price may be reason to be more careful with some sensitive producers and especially careful with those names with weak balance sheets that may have to dilute if cash flow comes in below expectations, names like Lundin and Orla ( ORLA ) are not names where one has to worry, and even a deeper correction below $1,700/oz in gold would not hurt the thesis for either stock.

As for other key developments, Lundin Gold has shared more than once that it's looking at the possibilities of M&A, especially with most of its debt paid down, a strong balance sheet, and the benefit of strong currency vs. its industry peers. However, as it stated in its Investor Day Presentation, it will not grow for the sake of growth, and the difficulty in M&A will be that few assets hold a candle to Fruta del Norte [FDN] from a quality and margin standpoint. Hence, while it shared that its focus would be on development-type opportunities in Latin America and North America, the list of potential names is quite small, especially with Gold Fields ( GFI ) coming in for half of Windfall which might have otherwise been an option for Lundin given that this certainly fits the bill from a grade, scale, and jurisdiction standpoint.

Some investors might prefer to shy away from Lundin Gold if M&A is on the horizon, and given the terrible performance of suitors post-acquisition in most cases, this isn't an unreasonable argument. That said, if Lundin is shopping around for developers, the level of dilution and share overhang after a deal would be minimal if it used a mix of equity and cash/debt to complete a deal given its market cap vs. most developers, and with how disciplined the company has been to wait for opportunities, the deal would likely be quite accretive given that developer valuations are sitting at their lowest levels since 2016 and 2018 near major lows. To summarize, I think an acquisition could actually benefit the stock long term, given that valuations are finally at a level where even some of the best assets are deeply discounted because of the violent bear market we've seen in small cap gold names, and even when using higher discount rates of 7-10%.

Valuation

Based on ~242 million fully diluted shares and a share price of US$12.50, Lundin Gold trades at a market cap of ~$3.02 billion and an enterprise value of ~$3.15 billion. This makes it the highest capitalization single-asset producer in the market today, commanding a valuation north of what Newcrest ( NCMGF ) would fork over for Pretium (~$2.8 billion), with Brucejack being a high-grade and Tier-1 jurisdiction asset that also had regional potential given that the takeover came within weeks of the Golden Marmot Discovery (53.5 meters at 72.5 grams per tonne of gold). And while one could easily argue that Lundin is better run; that FDN has the same regional potential, and that FDN has better margins, this continues to be a rich valuation relative to peers at ~1.1x P/NAV. Hence, I am surprised that Lundin Gold hasn't made a move from an M&A standpoint and used some of its strong currency to do M&A, which would also help justify its premium multiple as it would shed its single-asset producer status.

From a cash flow standpoint, the picture is quite different, and while Lundin Gold may trade at a premium to peers on a P/NAV standpoint, it continues to trade at one of the more attractive free cash flow multiples, sitting at a ~13.5% FY2024 free cash flow yield based on FY2024 estimates of ~$385 million. This is one of the higher free cash flow yields sector-wide among producers with Tier-1 scale assets (450,000+ ounces), and certainly among those with the operational track record of Lundin, which is beat, raise, and rinse and repeat. That said, using what I believe to be a fair value of US$14.80, Lundin Gold may have an 18% upside, but this pales compared to the 50% upside available in more beaten-up miners. Therefore, while Lundin Gold is undoubtedly a top-10 gold producer and owns one of the few world-class assets not held by a major, I continue to see more attractive bets from a relative value standpoint elsewhere.

Summary

Lundin Gold is one of the few producers that continues to consistently deliver on its promises, and while unprecedented inflationary pressures have hit most producers, it has been shielded with low inflation rates in Ecuador, access to low-cost grid power, and less competition for skilled labor given that it's not in a prolific mining jurisdiction. Meanwhile, the company continues to work to improve recoveries and is progressing a de-bottlenecking project to potentially push through to 5,000 tonnes per day, helping to maintain a 425,000+ ounce production profile as grades begin to taper off post-2025. Finally, the company certainly has an attractive exploration component to it, with it offering bonus upside if there is a new major discovery from a regional standpoint, with there being no better place to find a major mine than next to one of the 21st century's most impressive gold discoveries.

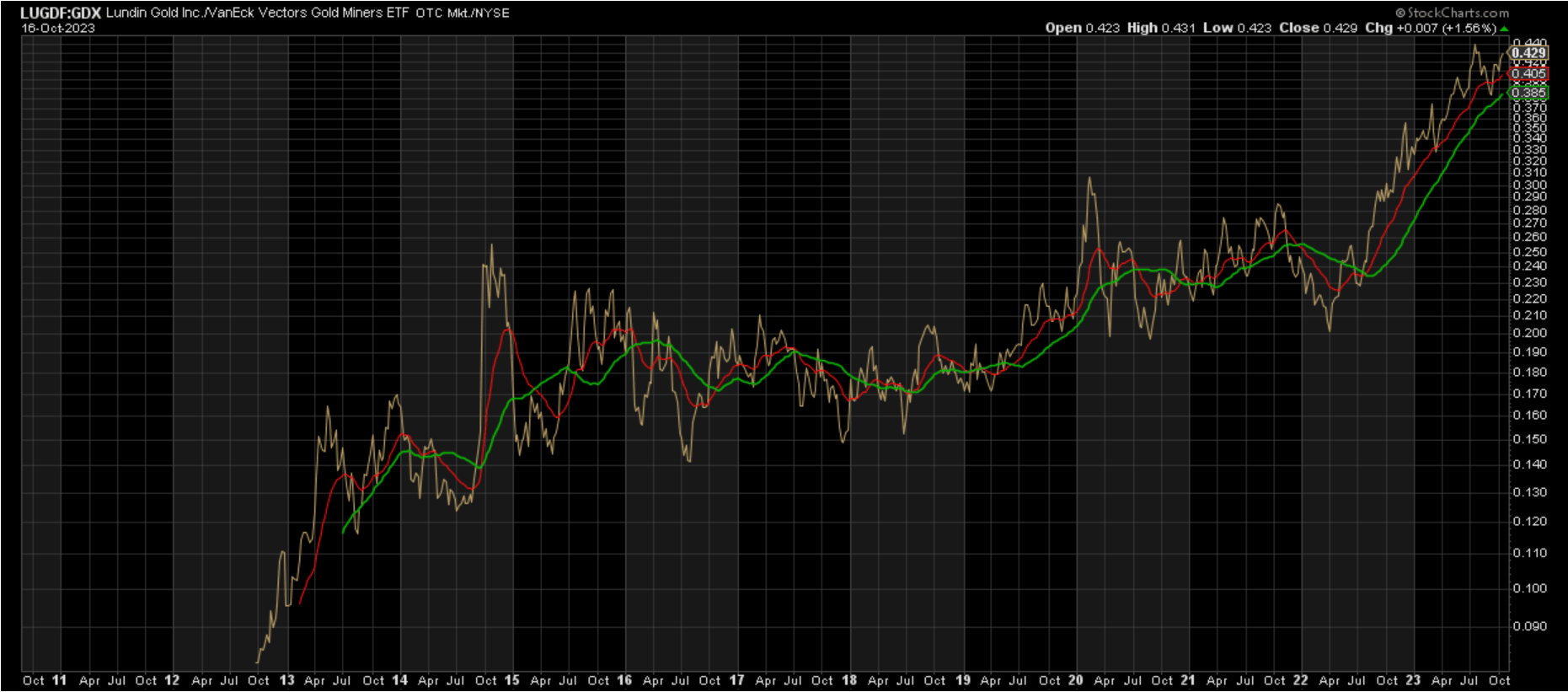

Lundin Gold Outperformance vs. Gold Miners Index - StockCharts.com

{kind=link}

All that being said, some of this is priced into the stock given its considerable outperformance (shown above) vs. its peer group, and while the company's near flawless operational execution and industry-leading yield suggest that it will continue to perform well, it's possible that other miners that have been left for dead could take the baton and outperform in the 2024-2027 period. Therefore, I continue to see more attractive bets elsewhere in the sector that may be more volatile, but likely offer far more upside if they're able to execute successfully. One name that stands out is Marathon Gold ( MGDPF ) which trades at just less than 0.30x P/NAV (8% discount rate), making it an absolute steal at current levels, and one of the most attractive valuations I've seen in a construction-stage Tier-1 jurisdiction developer in years.

For further details see:

Lundin Gold: Set Up To Beat Upward Revised Guidance