CA - Lundin Gold: Trouncing Guidance In A Sea Of Misses

2023-04-04 17:06:04 ET

Summary

- Lundin Gold was one of the best-performing gold producers last year, up 19% for the year vs. an 11% decline in the Gold Miners Index.

- This outperformance has continued in 202e, with Lundin up over 20% year-to-date on the back of impressive 2022 operating and financial results and significant reserve growth.

- However, while this is easily a top-10 producer, that's mining of the richest ore bodies globally, the stock is becoming extended short term.

- So, with the stock trading at a large premium to its peer group with no margin of safety above US$12.20, I see this as an opportune time to book some profits into strength.

The Q4 Earnings Season for the Gold Miners Index (GDX) is finally over and it was a disappointing earnings season overall. Not only did we see several companies miss their production guidance, but the delivery against cost guidance was pitiful, with many gold producers forced to move the goalposts (guidance range) entirely. In fairness, the misses on costs were because of stickier than expected inflationary pressures and some miners had tougher years due to supply chain headwinds. However, one name stood head and shoulders above the rest regarding delivering into guidance, and this was Lundin Gold (LUGDF).

Not only did Lundin Gold ("Lundin") beat its initial FY2022 guidance midpoint of 425,000 ounces by over 10% by producing ~476,300 ounces, but it beat the top end of its updated guidance range of 430,000 to 460,000 ounces. Just as impressively, it easily beat its upgraded all-in sustaining cost [AISC] guidance of $820/oz to $870/oz, and reported some of the highest margins sector-wide due to its ultra-low FY2022 AISC of $805/oz. However, I believe the ideal time to buy miners is when they're out of favor and sentiment is in the gutter, and with Lundin up 101% off its lows in six months, this is hardly the setup today. Hence, I see this push to new highs as an opportunity to book more profits.

Q4 and FY2022 Production

Lundin Gold released its Q4 and FY2022 results in late February, reporting quarterly production of ~121,100 ounces of gold, helping the company to deliver well above its initial FY2022 guidance of 405,000 to 445,000 ounces. In fact, the company beat its guidance midpoint (425,000 ounces) by over 11% by producing ~476,300 ounces, and this impressive production profile made its Fruta del Norte mine one of the most productive assets in the sector in 2022. In fact, the asset produced more gold than nearly all of Agnico Eagle's ( AEM ) mines, except for Detour Lake and Canadian Malartic, which are 700,000-plus ounce per annum assets.

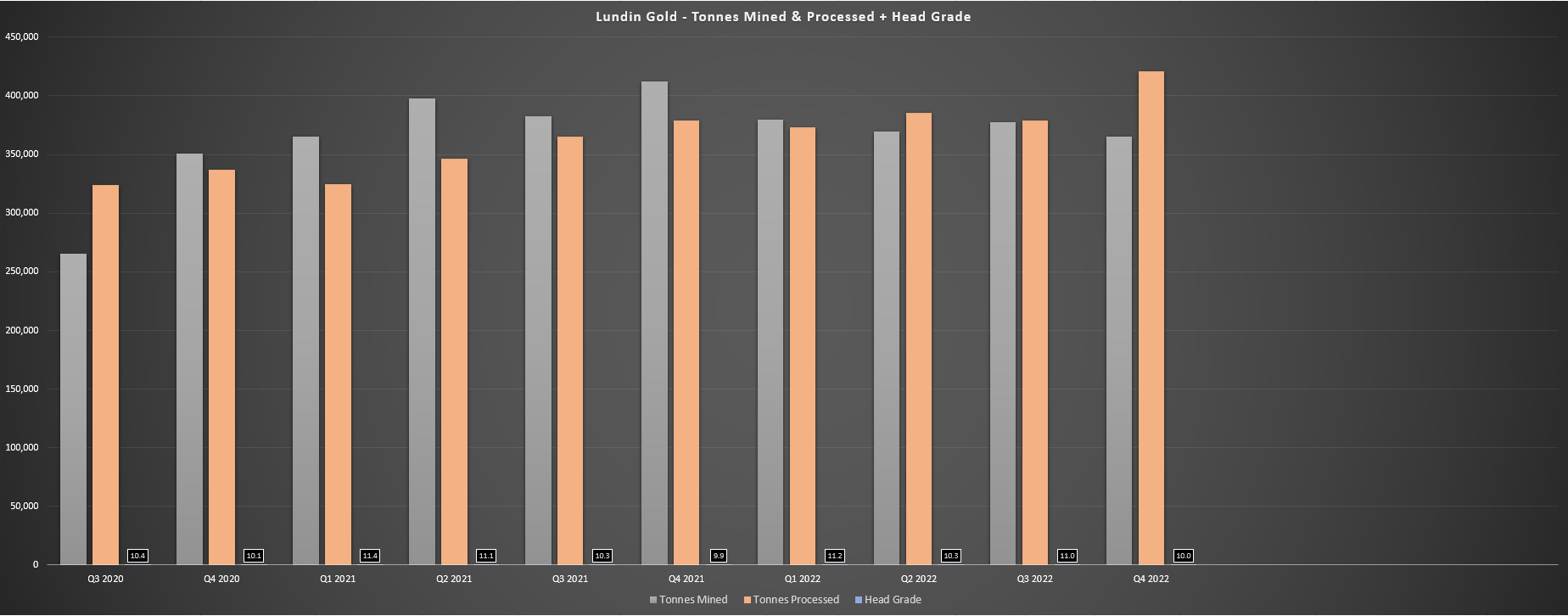

Lundin Gold - Tonnes Mined, Tonnes Processed & Head Grades (Company Filings, Author's Chart)

{kind=link}

Digging into the results a little closer, we can see that the strong Q4 performance was driven by record quarterly throughput of ~420,800 tonnes, an 11% increase from the year-ago period. This record throughput (average of 4,574 tonnes per day) combined with strong grades (10.0 grams per tonne of gold) helped the asset to deliver a third 120,000-ounce plus quarter in FY2022. On a full-year basis, Lundin Gold processed ~1.56 million tonnes at 10.6 grams per tonne of gold to report an 11% increase in output, with the lower tonnes mined in Q4 not being productivity related, but because of the company lower its mining rate in Q4 to process some of its growing stockpiles.

Fruta del Norte Operations (Company Website)

{kind=link}

Given the impressive reserve replacement reported last month, Lundin Gold investors can look forward to several more years of 9.0+ gram per tonne grades, allowing Fruta del Norte to maintain its spot as one of the highest-grade mines globally. In fact, the mine continues to climb the ranks as one of the gold mines globally from a grade standpoint, especially as grades normalize at previous top mines from a grade standpoint like Fosterville, Kainantu, and Yaramoko. To put in context just how impressive Lundin Gold's reserve replacement was, the company reported 115% replacement of reserves since the operation began production in November 2019, a reserve replacement figure that's peer-leading especially when some companies continue to see declining reserves like Fortuna ( FSM ) and First Majestic ( AG ).

Costs and Margins

Moving over to costs and margins, it was a phenomenal year in this department as well, with Lundin reporting Q4 all-in sustaining costs of $865/oz and Q4 AISC margins of $949/oz. On a full-year basis, the company's AISC came in at $805/oz which was up just over 5% year-over-year, while AISC margins came in just shy of FY2021 levels ($1,010/oz) at $984/oz. Given the inflationary pressures experienced sector-wide, the performance was incredible, with Lundin fortunate that it saw "limited inflationary impact in Ecuador" and it benefited most of its power being from hydroelectricity. The result was that Lundin reported some of the highest AISC margins sector-wide, only slightly behind Orla Mining ( ORLA ), with Lundin's FY2022 AISC margins nearly double the industry average at ~$490/oz.

Lundin Gold - Quarterly Production & Costs (Company Filings, Author's Chart)

{kind=link}

As the above chart shows, Lundin Gold's AISC spiked in Q4 because of higher sustaining capital (third raise for tailings dam), but costs have remained well below the industry average. And while costs will increase based on FY2023 guidance to $870/oz to $940/oz (assuming the company doesn't trounce guidance yet again), this is largely because of higher sustaining capital this year and shouldn't impact margins. This is because even if AISC were to come in $90/oz higher year-over-year at $890/oz, this should be offset by what looks like it will be an average realized gold price of at least $1,880/oz in FY2023, which would translate to AISC margins of $990/oz, up marginally vs. the $984/oz reported last year.

Financial Results

Not surprisingly, Lundin Gold had a blowout year from a financial standpoint, reporting record revenue of $815.7 million, an 11% increase from the year-ago period. This was driven by higher sales volume and a slightly higher average realized gold price of $1,789/oz, which helped the company generate operating cash flow of $421.4 million and annual free cash flow of $269.4 million. Looking at the Q4 results, revenue came in at $211.0 million with free cash flow of $91.1 million, making Lundin one of the most profitable producers sector-wide despite the lull in the gold price. So, with the gold price averaging over $1,900/oz year-to-date, investors can look forward to a very strong H1 from a financial standpoint.

Lundin Gold - Quarterly Revenue, Free Cash Flow & Cash Position (Company Filings, Author's Chart)

{kind=link}

Given the strong financial performance, Lundin finished the year with net debt down to just ~$305 million despite paying one of the highest dividend yields sector-wide in 2022 and it noted in its Q4 Conference Call that cash flow will be directed to near-mine and regional exploration, a future throughput expansion, further debt reduction and M&A. Regarding potential M&A, the goal would be to diversify by acquiring somewhere other than Ecuador. The only tough thing for a company like Lundin when it has an asset this incredible is that it can be very tough to find something that matches up or even comes close, especially at an attractive price. One asset that would come close to comparing is Osisko Mining (OBNNF) but the stock is no longer nearly as cheap after its recent rally.

Given Lundin's industry-leading cash flow generation, which was well above that of multi-asset peer, SSR Mining ( SSRM ), this is certainly one of the sector's best buy-the-dip candidates and a name that investors can sleep well at night knowing there won't be any share dilution. In fact, if Lundin Gold were to go on sale and suffer a deep correction, the company certainly has the cash to support a buyback program to support its share price. So, with a 3.0% plus dividend yield, industry-leading AISC margins yet again in 2023 despite elevated sustaining capital and the potential to add a second asset through M&A that could lead to a re-rating, I continue to see Lundin Gold as one of the top names in the sector.

That said, the ideal time to accumulate a position has come and gone since I noted the stock would move into a low-risk buy zone below US$6.25 in September, and I no longer see the valuation as attractive. Let's take a look:

Valuation and Technical Picture

Based on ~241 million fully diluted shares and a share price of US$12.22, the stock trades at a market cap of ~$2.95 billion and an enterprise value of ~$3.26 billion. This makes Lundin Gold the most expensive single-asset producer that I'm aware of sector-wide, which is deserved in some sense given that it's the proud owner of one of the richest ore bodies globally with a massive land package surrounding the mine. That said, the valuation is getting stretched following this recent move to new highs, with Lundin now trading well above its estimated net asset value of ~$2.47 billion, which already assigns $240 million in exploration upside. And, even using a 1.1x P/NAV multiple which is above its peer average, I see a fair value for the stock of US$12.00, leaving it trading slightly above fair value currently.

{kind=link}

Moving to the technical picture, Lundin Gold has broken out to new all-time highs with no resistance overhead, but its next support level doesn't come in until US$9.35 and it has an overbought zone just overhead at US$12.55 that could provide a sticking point. This doesn't mean that the stock must fail here, and it could certainly continue its outperformance vs. its peers. That said, the current reward/risk ratio comes in at just 0.09 to 1.0, with $0.25 in potential upside to its overbought zone and $2.85 in potential downside to support. So, if I were long the stock, I would use this rally as an opportunity to book more profits with the stock trading above conservative fair value and becoming vulnerable to a correction.

Summary

To say Lundin Gold knocked it out of the park in 2022 would be an understatement, with the company trouncing its initial guidance in a year where many struggled to even meet the high end of their cost guidance ranges. That said, and as Joel Greenblatt has stated, there's no investing without valuation, and with Lundin Gold trading well above 1.0x P/NAV and at a massive premium to its peer group, I don't see any way to justify chasing the stock here. In fact, I see this rally as an opportunity to take more profits, given that I see zero margin of safety at current levels. If I were interested in putting more capital to work, I see Marathon Gold ( OTCQX:MGDPF ) as one name on the sale rack that is still in a buyable position.

For further details see:

Lundin Gold: Trouncing Guidance In A Sea Of Misses