CA - Lundin Mining: Looking For (And Not Finding) Cheap Gold And Copper

Summary

- Lundin Mining is a somewhat controversial stock even here in Sweden, where the company is from. However, beyond controversy, we find a qualitative mining company.

- I'm going to initiate coverage on Lundin Mining as of this article. The company, at the right price, can become an absolute outperformer.

- I own a small stake in the company, and one intends to build up going forward as the company goes through cycles of volatility - but today's valuation worries me.

Dear readers/followers,

The fact that I like mining, metals, and basic commodity stocks should not come as a surprise to anyone, given my history on Norsk Hydro ( OTCQX:NHYDY ), and covering companies like Boliden ( OTCPK:BDNNY ) and SSAB ( OTCPK:SSAAF ) as well as other more international plays.

The time has come for me to take a look at Lundin Mining ( OTCPK:LUNMF ) - one of the most spoken-of mining stocks in Scandinavia. While the company is originally Swedish, it's actually incorporated in Toronto, Canada. This means that the company has a native NA ticker in the form of Canadian ticker LUN - which is the one I'm going to try and focus on here.

Let's get going.

Lundin Mining - a Company review

The reason that the company is controversial is not due to Lundin Mining, but due to Lundin generally, which is a Swedish "power sphere", similar to the Wallenberg family. These families own entire sectors of companies in Sweden, and in the case of Lundin, these companies are found not only in mining and prospecting but in oil and gas. The founder, Adolf Lundin, died in 2006, and the companies are mostly run by his children's proxies of them.

The reason why this company or sphere is viewed as controversial by some is that during the 80s and '90s, Lundin was accused of human rights breaches due to their operations in, above all, Africa. This included the mining of gold despite the boycott of the apartheid regime, prospecting, and mining in the war-torn regions of Kongo-Kinshasa as well as Sudan. The now-late Adolf Lundin was a magnet for controversial comments about the company's work in these regions, and he did business with areas like Libya, Sudan, and other nations which caused both accusations and embarrassments very high up in the Swedish political establishment. Adolf Lundin was recorded as seeing a competitive advantage compared to US businesses because Swedish businesses did not have to follow certain laws, and regulations, and the fact that Swedish NGOs were almost powerless at the time.

As I do sometimes in these articles, when there is controversy - I state it clearly without judgment and explain it as best I can. So if someone asks you about Lundin and investing, you now know why there might be some raised eyebrows. Lundin today, including Lundin mining, isn't really involved in those sorts of businesses any longer. I believe what can be said about Adolf Lundin is that he was a "gunslinger", a wildcat sort of investor that had no issues leveraging laws and regulations where he saw it as possible - a very "No guts, no glory" sort of approach, think of it what you will.

So, Lundin Mining. This is Lundin Sphere's mining company with a focus on specific metals, mostly copper, Zinc, Lead, and Gold.

{kind=link}

The company tries to push its responsible mining-agenda, highlighting safety, following protocol and sustainability, and emphasizing human rights and governance above all, now going on 20 years after the death of Adolf Lundin. And in some ways, the way things have been going is very impressive.

{kind=link}

Lundin mining is very much a play on copper, above all. In a positive copper environment, Lundin goes up - in negative, it's likely to go down. The company believes Copper to be one of the driving forces going forward, with the high-level positive copper outlook based on its importance in the energy transition. This coupled with a very inelastic supply of profitable copper mines means that the company has a very bullish outlook on the demand.

A typical BEV has 4x more copper than a normal car, and overall projects in the ESG/EV/Sustainability space are copper-heavy. The company also forecasts mine production to decline, and few new advanced-stage projects for new mines are available. Lundin foresees the very real possibility of a copper deficit as early as 2032, bringing a supply gap of 6.4Mtonnes, which accounts for nearly 25% of current copper consumption. In another way, the company expects prices to skyrocket.

Lundin mines and produces plenty of copper, and generally average between $2-$4B in annual sales, with the following split.

{kind=link}

The company does not have a credit rating, and currently has a market cap in Canadian dollars of $7.25B. This makes it perhaps one of the smaller players, but it also comes at a yield of 3.8% currently, which is above par for the segment. What's more, the company is currently valued at less than 14.1x P/E, which is well below where it usually trades - more on that later.

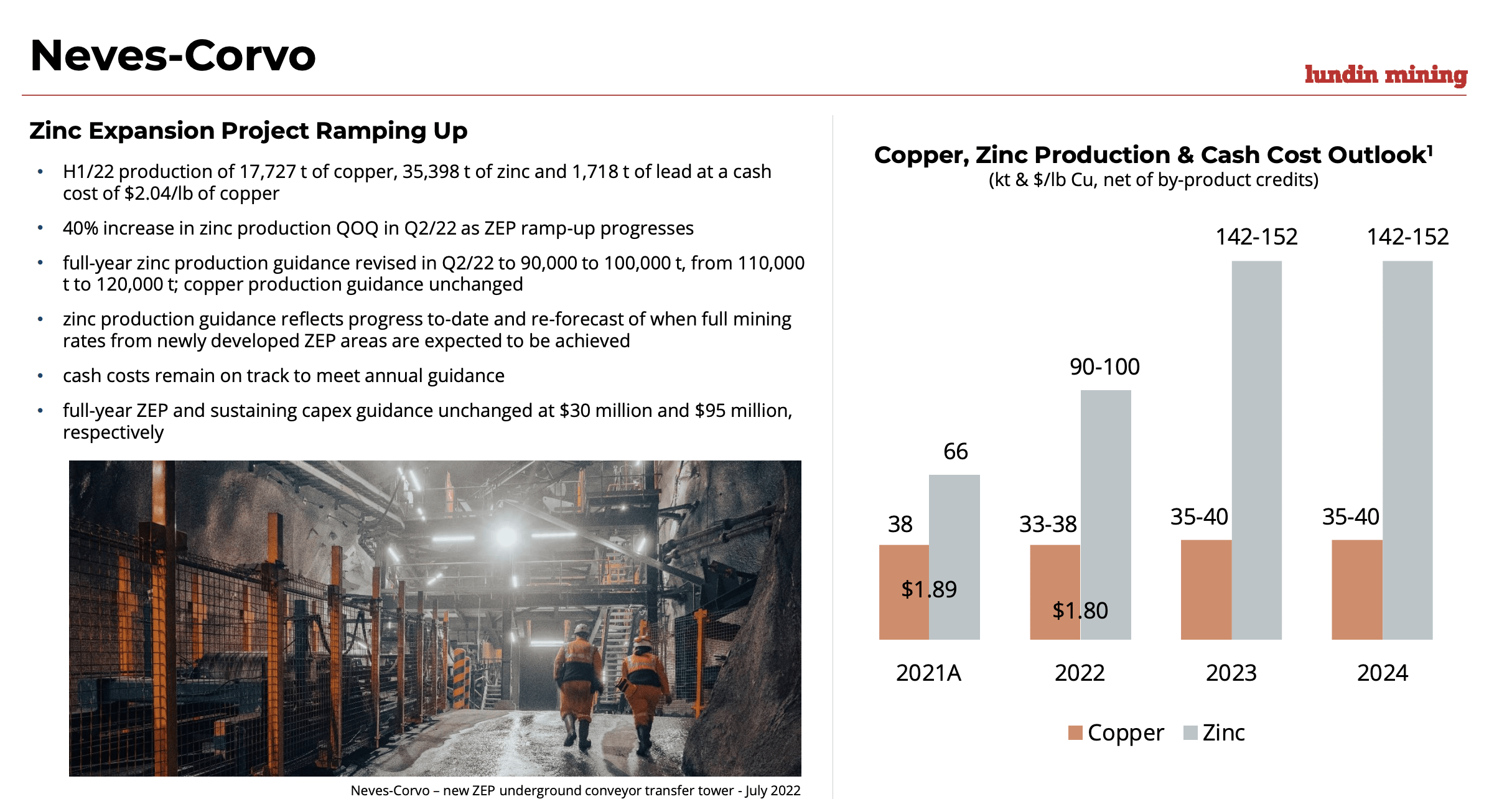

The company's main mines are Candelaria, Chapada, Eagle, Zinkgruvan, and Neves-Corvo. These are mostly working according to plan, with Production stable or growing in most areas - especially when it comes to copper, with the exception of Eagle, which is seeing production declines going into 2024. Neves-Corvo is interesting here because we're seeing the massive potential for more zinc production, upwards of 40%.

{kind=link}

And then here is the Zinkgruvan in Sweden, the company's legacy asset, which also remains on track with solid production and meeting guidance despite overall energy concerns and global shifts.

The company's focus is on operating high-quality competitive mines that are scalable, either doing so alone or with a mix of JV's/off-take partnerships for financing, with the Josemaria project one of the nearest, new projects.

The company has closed the books on the 2022 fiscal, and results here were solid, with 250,000 tonnes of copper mined. The most interesting development during the past year here aside from general operations and how things have gone, is as I see it, the company's Josemaria project, which is moving towards development.

{kind=link}

The company has also given us 2023 guidance, which calls for 10,000 more KT's mined in terms of copper, and improvements across most segments. CapEx is expected to be higher, due to $400M being spent on the Josemaria project.

The primary challenges for Lundin are not operational - they're valuational. Operationally, the company is a solid, if unrated player, in the mining industry. I wouldn't necessarily call it more attractive than some of the larger copper players out there, but I would consider the company attractive at a good price.

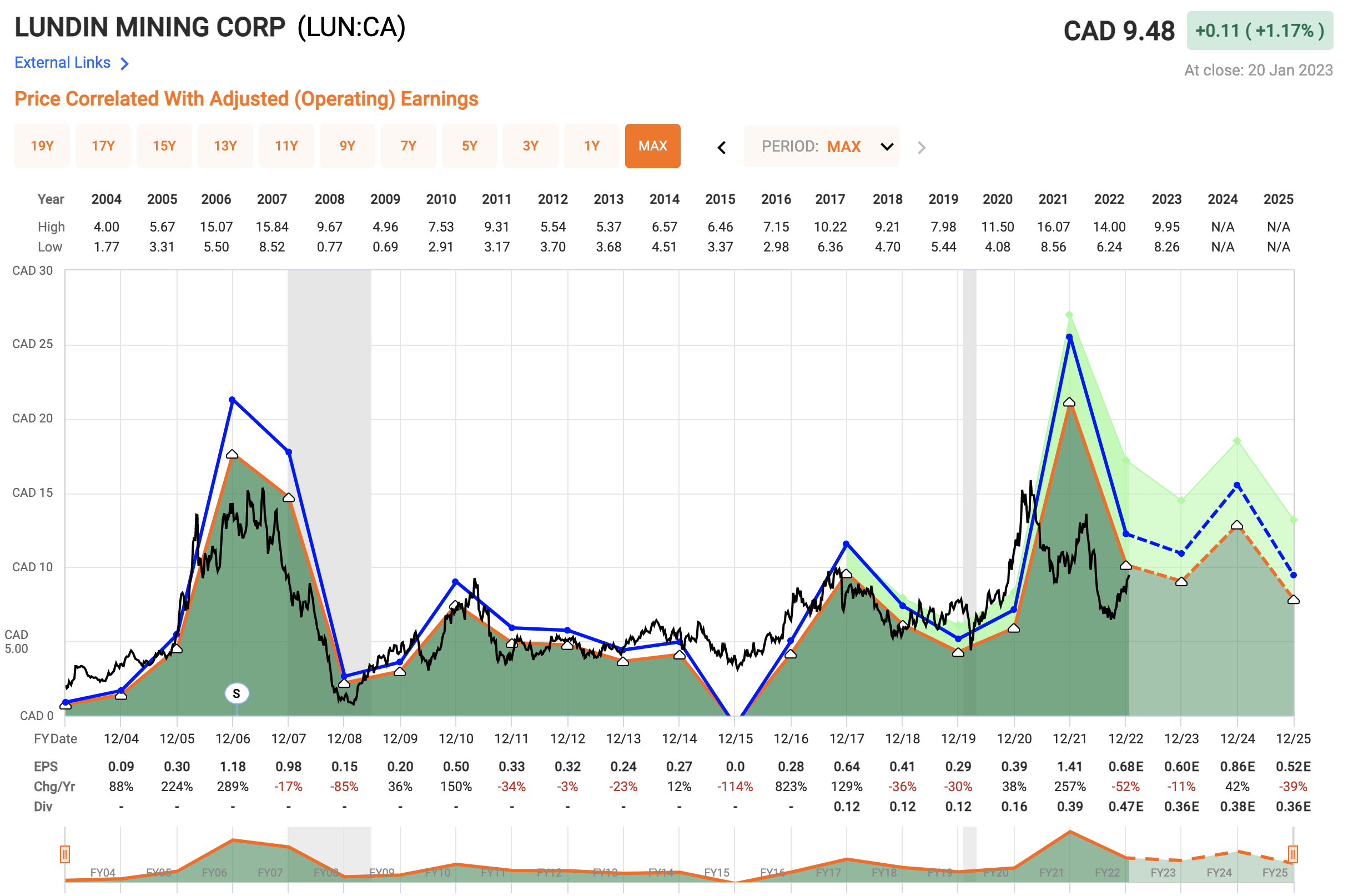

However, Lundin is entirely a valuation play. The 5-year returns of 0.7% per year, the 10-year returns of 5.9% per year...

{kind=link}

It all shows us the sort of trends that are endemic to a volatile mining business. As you can see, the company can go nowhere for entire years, and the yield does not weigh this up.

The only time to "BUY" Lundin is when the company is cheap. So let's see exactly what we have here when it comes to that.

Lundin Mining's valuation - stay away, despite an attractive market.

We come to the main issue here. Lundin Mining as a company is richly valued. There could be reasons for such a rich valuation, including the demand/supply imbalance that the company foresees coming in about 10 years or so - but I wouldn't use this as justification to invest at what is a higher valuation than the company typically find itself trading at. The volatility can be quite easily expressed using a graph such as this.

{kind=link}

Often time, Lundin does not even pay a dividend, and during certain years, EPS can go into negative or to essentially zero, before bouncing back up. While the underlying operations can be said to be qualitative, it's impossible to disconnect this investment from the unstable trends that make up the company's overall markets - and the company is even less stable than some peers here.

I'm not a fan of the ups and downs associated with Lundin, or the downs associated with buying the company at a relatively high point in valuation. Lundin has a broad group of peers, some of which I cover. Some include Glencore ( OTCPK:GLNCY ), Rio Tinto ( RIO ), BHP ( BHP ), Freeport-McMoRan ( FCX ), and Southern Copper ( SCCO ). Most of the companies mentioned show better size, credit rating, and stability than Lundin does.

Lundin is one of those companies I would only buy at a very low multiple. And currently trading at 14.63x for the native Canadian ticker, the company is ahead of everything except SCCO and FCX. Some might say this is a good indicator, because these latter are fairly copper-heavy, like Lundin. The problem is they're also materially better structured in terms of capital, stability, safety, and dividends, which doesn't put Lundin in the most favorable light at this particular time.

Using DCF or similar models that depend on or include the near-term or current pricing of copper often fails to take into consideration the volatility when this company drops. Because of this, I find the best way to value Lundin is to look closer at long-term averages and book/tangible multiples to ensure that we do not pay too much for this, below-average-rated company in terms of credit.

First off, Lundin is already being heavily discounted by analysts. 19 follow Lundin on market with its native Canadian ticker, and out of 19 analysts, only 2 are currently at a "BUY" at a $9.48 CAD share price. The range begins at $5.23 and goes up to $8.96, quite a bit below that $9+ current share price. This is the first problem, with an average of $6.73, which implies the company is actually over 5% overvalued here. The current share price puts Lundin at a 1x NAV multiple, which for a mining company would be something I paid only for the absolute best, BBB+ rated company.

That is not Lundin, and that's why it's not worth $9.5. I would not pay above 0.6x NAV for this company, which puts the indicative share price at around $7 - and even that is more than I'd really want to ideally pay for a good upside. 0.5x NAV would make me interested, because this accounts for the elevated risk of owning a set of mines across the world where things can (and often do) go wrong.

For that reason, I'm giving Lundin a conservative share price of around $6.5 to start with - which is below the current average, but also comes to a 0.5x to NAV. It also puts the company closer to a 0.8-1x Sales multiple, again something I look for here, and below a 1x book value multiple. All of these are more or less what I would look for in terms of how high I would consider the company to be of fair value.

Lundin has had an amazing Bull run for the past 1-3 years, being it's up 60-75% in the meantime, due to the demand for copper and the EV revolution. However, I believe the latest climb, especially since September, will revert back down a bit and normalize more closely to a longer-term fair value.

I'm also completely unwilling to pay close to 1x NAV, BV, or over 1.5x sales for a company like this. The controversy doesn't bother me that much - it was long ago - but the valuation does here.

For that reason, Lundin is an absolute "HOLD" here.

Thesis

- Lundin is a Canadian-based, originally Swedish miner in the Copper, Zinc, and Gold segments. The company doesn't have a credit rating, but does have a set of appealing assets across the globe, and has left behind its problematic operations in Africa to focus on South America, Europe, and NA.

- At the right valuation, the price for the company's assets is appealing enough to where you may garner a triple-digit rate of return for a good investment. However, that time is not now. The company is richly valued, and I see a strong potential for a flat valuation or even a downturn.

- The company is, to my mind, worth 0.5-0.6x NAV and below a 1x BV. That implies a PT of $6.5 CAD.

- This makes Lundin Mining a "HOLD" here.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.

The company fails the safe and valuation checks. The only way Lundin can become a "BUY" is if it falls to below $6.6 CAD. It's a "HOLD".

For further details see:

Lundin Mining: Looking For (And Not Finding) Cheap Gold And Copper