SHEL - LyondellBasell Industries To See Lower Costs Keeps ESG Focus

Summary

- LyondellBasell is a $32.2 billion market cap company paying a 4.8% regular dividend. Its primary business is global chemicals - it is a leading ethylene producer, for example.

- The company was less profitable in 2022 than in 2021 due to higher energy and feedstock costs, but that situation has reversed.

- Strategic initiatives include shutting down its Gulf Coast oil refinery, creating a recycling and low-carbon business unit, and starting up additional chemicals capacity.

LyondellBasell Industries, N.V. ( LYB ) is a global petrochemicals company. It also owns a US Gulf Coast refinery it plans to shutter at the end of 2023. Per the company's description , it currently "operates in six segments: Olefins and Polyolefins-Americas; Olefins and Polyolefins-Europe, Asia, International; Intermediates and Derivatives; Advanced Polymer Solutions; Refining; and Technology." The company has 55 sites in 17 countries and serves 100 international markets.

For example, its Channelview complex has a capacity of 1.86 million tons per year (mtpa) of ethylene, 1.54 mtpa of propylene, and 1.47 mtpa of ethylbenzene.

Key to improved prospects for 2023 are lower natural gas and natural gas liquids prices. For example, Michael McMurray, CFO for LyondellBasell, estimates each $1/MMBTU chang e in natural gas prices means a $175 million/year change in energy costs across the company, 80% in the US and 20% in Europe. This does not include feedstock cost effects. However, in answer to an analyst question, with European gas prices so high ($37/MMBTU vs. $17/MMBTU now) the ratio does not precisely hold, the company cautions, (e.g. not an extra $700 million cost hit), since LyondellBasell was also able to raise product prices and implement energy surcharges.

Despite refining EBITDA of $249 million (31% of total EBITDA) 4Q22 and EBITDA of $921 million for the full year (15% of total EBIDA) LyondellBasell is still planning to exit the refining business and expects to take a $300 million subtraction from earnings in 2023 for doing so, on top of the $157 million subtraction in 2022.

Ironically, refining-especially of the heavy crude LyondellBasell's Houston refinery can use--appears slated to be quite profitable for at least the first half of 2023.

The company devotes considerable website real estate and financial reporting to its Diversity Equity and Inclusion ((DEI)) and Environmental Social and Governance ((ESG)) initiatives, including Scopes 1, 2, and 3 compliances. While ESG seems to be a bigger emphasis for European companies (LyondellBasell has joint European-US roots), it is less profitable than many project priorities, as energy giant BP ( BP ) has experienced. Indeed, even BP has slowed its "energy transition" talk and spending.

Still, assuming the very substantial US (and some European) cost benefit from lower natural gas and gas liquids costs in 2023 is not yet fully incorporated in the stock price and with its 4.8% dividend, I recommend LyondellBasell to investors-including ESG investors-hunting for dividends and capital appreciation.

Fourth Quarter and full year 2022 Results and Guidance

In the fourth quarter of 2022 LyondellBasell reported net income of $353 million, compared to 4Q21 net income more than twice that of $726 million.

Full-year 2022 net income was $3.9 billion, or $11.81/share, compared to 2021 net income of $5.6 billion or $16.75/share.

Cash from operations in 2022 was $6.1 billion.

Other strategic initiatives for 2023, in addition to exiting refining, include creating a Circular (recycle) & Low Carbon Solutions business unit and starting up more propylene oxide ((PO)) and tertiary-butyl alcohol ((TBA)) capacity in Houston. The company also references a value enhancement program comprising commercial, manufacturing, and operational processes as well as procurement and supply chain changes that is expected to generate $150 million/year of additional EBITDA by the end of 2023 and more in later years.

In 2023, the estimated EBITDA effect of major maintenance is expected to be -$290 million while t hat of exiting refining is -$320 million.

For the first half of 2023, the company expects stable demand with lower energy and feedstock costs.

Natural Gas and Natural Gas Liquids Prices

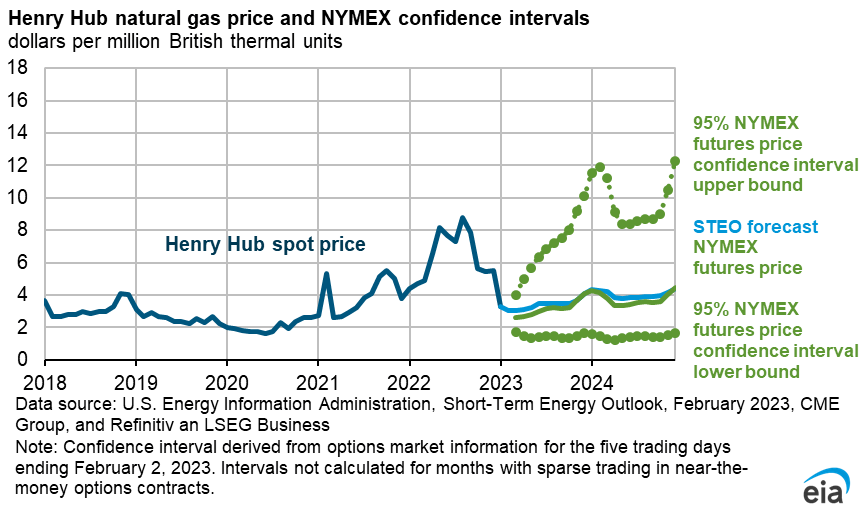

In the Energy Information Administration's (EIA's) newest Short Term Energy Outlook (STEO) forecast and 5-95 confidence interval shown below, 2023 natural gas prices are projected at $3.40/MMBTU for 2023, nearly 50% lower than in 2022 and even 30% lower than the EIA's own January 2023 forecast.

{kind=link}

However, the February 7, 2023, closing NYMEX futures Henry Hub natural gas price for delivery in March 2023 was lower still, at $2.58/MMBTU.

Internationally, for reference to the Henry Hub US gas prices of $2.58/MMBTU, liquefied natural gas is:

*$17.41/MMBTU for March 2023 at TTF (Title Transfer Facility in the Netherlands);

*$18.19/MMBTU for March 2023 for the JKM (Japan Korea Marker) Asian reference price.

Investors should be aware that European LNG prices spiked to nearly $100/MMBTU in 2022; thus, current gas prices are far more affordable.

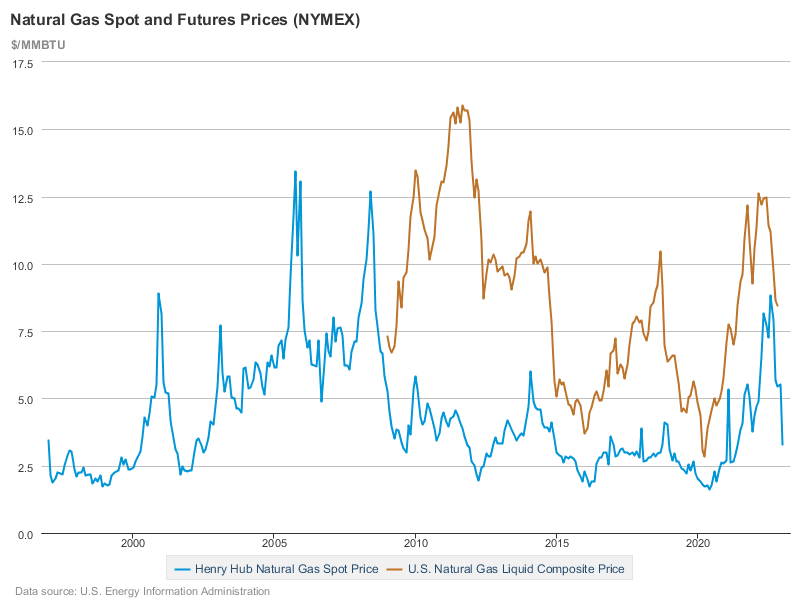

An EIA graph comparing natural gas to natural gas liquids prices from 2009 forward is shown below. Per the EIA, "the natural gas liquids (NGPL) composite price is derived from daily Bloomberg spot price data for natural gas liquids at Mont Belvieu, Texas, weighted by gas processing plant production volumes of each product as reported on Form EIA-816, "Monthly Natural Gas Liquids Report."

Natural gas liquids comprise key olefin feedstocks like ethane and propane. Clearly these prices, too, are falling from recent highs.

{kind=link}

Macro

Also in the STEO, the EIA predicts US real GDP will decline in the first half of 2023 (nominal GDP will increase with inflation), but that real GDP will increase in the second half of 2023 and will average 2.1% in 2024. Chemicals use tends to track GDP fairly closely, although note that LYB is global and this estimate is for the US only.

The major disruption for natural gas, natural gas liquids, oil, and distillate is the Russia-Ukraine war and the consequent sanctions against Russian exports by the west, followed by Russia's redirection of its exports. All introduced considerable trade friction, and higher prices (costs for LyondellBasell) in 2022.

After a recent 0.25% increase, the Federal Reserve's chair, Jerome Powell, suggests they Fed may continue to raise rates in 2023: the inflation target is 2.0% and inflation is still well above that.

Competitors

LyondellBasell is headquartered i n Houston, Texas; however, its SEC reporting addresses are in Houston, London, and Rotterdam.

Among US-based companies or those with significant US operations, ethylene competitors include CP Chem, a Chevron ( CVX ), Phillips 66 ( PSX ) joint venture, DuPont ( DD ), Westlake Chemical ( WLK ), and the chemicals divisions of Exxon Mobil ( XOM ) and Shell ( SHEL ).

Other chemicals competitors include BASF, Bayer, Celanese ( CE ), China Petroleum & Chemicals ( OTCPK:SNPTY ), Dow ( DOW ), Eastman Chemical ( EMN ), INEOS, Mitsubishi Chemicals, Saudi Basic Industries (SABIC) and Sumitomo Chemicals.

LyondellBasell competes with virtually every US refiner. Total US operable oil refining capacity is 17.9 million barrels per day, so LyondellBasell's capacity share is a tiny 1.5%.

Governance

At February 1, 2023, Institutional Shareholder Services ranked LyondellBasell's overall governance as an excellent 1, with sub-scores of audit (5), board (1), shareholder rights (2), and compensation (4). In this measurement, a score of 1 represents lower governance risk and a score of 10 represents higher governance risk.

As of August 2022, LyondellBasell's ESG ratings from Sustainalytics were "medium" with a total risk score of 25 (42nd percentile). Component parts are environmental risk 16.6, social 2.1, and governance 5.8. Controversy level is 2 (moderate) on a scale of 0-5, with 5 as the worst.

At January 13, 2023, shorts were 2.75% of the floated stock.

Insider ownership is a large 21.8%. This is primarily private Access Industries whose interest in LyondellBasell appears similar to those of public investors.

The company's beta is 1.24, representing steeper volatility than the market due to more cyclicality in chemicals (and refining margins.)

On September 29, 2022, except for the large inside ownership, a majority of LyondellBasell's stock was held by institutions, some of which represents index fund investments that match the overall market. The six largest institutional holders were Vanguard (9.9%), BlackRock (7.4%), Dodge and Cox (4.4%), Capital International (3.8%), State Street (3.7%), and Wellington (3.3%).

BlackRock, Capital, State Street, and Wellington are signatories to the Net Zero Asset Managers Initiative, a group that, as of December 31, 2022, manages $59 trillion (down from $66 trillion in November 2022) in assets worldwide and which--despite less energy supply due to reduced Russian exports to Europe--limits hydrocarbon investment via its commitment to achieve net zero alignment by 2050 or sooner.

Vanguard has withdrawn from the group.

Although LyondellBasell is not an energy producer, its need for feedstock of affordable hydrocarbons to make petrochemicals could conflict with this initiative.

Financial and Stock Highlights

LyondellBasell's market capitalization at the February 8, 2023, stock closing price of $98.91/share is $32.2 billion.

The 52-week price range is $71.46-$117.22 per share, so its closing price is 84% of the one-year high.

Trailing twelve months' earnings per share ((EPS)) of $11.81 gives a trailing price/earnings ratio of 8.4.

The average of analysts' estimated EPS for 2023 is $9.19 and for 2024 is $10.72 for forward price-earnings ratios of 10.8 for 2023 and 9.2 for 2024. LyondellBasell has beat analysts' EPS estimates by $0.07-$0.48/share in three of the last four quarters but missed it by -$0.88/share in 3Q22.

Twelve-month returns on assets and equity are both excellent at 10.2% and 35.2%, respectively.

At September 30, 2022-the most recently-available balance sheet--the company had $24.3 billion in liabilities, including long-term debt of $10.4 billion, and $36.5 billion in assets giving LYB a liability-to-asset ratio of 67% .

Trailing twelve months' operating cash flow was $7.6 billion and levered free cash flow was $3.9 billion.

LYB pays a regular dividend of $4.76/share, a yield of 4.8%. During 2022, it paid $9.90/share in regular and special dividends. For the year, LyondellBasell's returns to shareholders from dividends and share repurchases were about $3.7 billion, the majority--$3.2 billion-as dividends.

The company's mean analyst rating is 2.7, or "hold," leaning toward "buy" from twenty-four analysts. At least one analyst considers it very undervalued.

LyondellBasell will host a Capital Markets Day in New York on March 14, 2023.

Notes on Valuation

Book value per share is $37.44, much less than half its current market price, indicating positive investor sentiment.

The EV/EBITDA ratio is 6.8, well below the preferred ratio of 10 or less and suggesting LYB stock is a bargain.

Positive and Negative Risks

The two key negative risks for LyondellBasell are a) oversupply of plastics capacity, particularly from Asia and b) prices of natural gas (energy) and natural gas liquids (feedstock) rising again, particularly in Europe and Asia. The positive risk is that natural gas and NGL prices have been falling particularly in the US, a key manufacturing hub for LyondellBasell, but also globally.

More generally, potential investors should consider their overall global economic outlook and how chemicals demand may change.

Inflation is a negative risk, as is the possibility of an equity market downdraft.

Recommendations for LyondellBasell

I recommend LyondellBasell to dividend investors for its 4.8% dividend yield. A special dividend, as occurred in 2022, would be a bonus but is not expected.

While not all investors have caught up to the cyclic benefit to chemicals companies from lower natural gas (energy) and NGL (feedstock) prices, it is also the case that manufacturing costs in Europe, and to some extent Asia-both where LYB has plants-have not fallen as far or as fast as those in North America.

With joint US-European roots, LyondellBasell is particularly ESG-focused, adding a Circular and Low Carbons business unit to its operations and preparing to shutter its oil refinery.

It has an excellent governance rating.

The ratio of enterprise value to EBITDA indicates a relative bargain. The trailing and forward price/earnings ratios are also moderate.

Like every natural gas and NGL consumer, LyondellBasell is advantaged by now-lower costs of both. Investors seeking capital appreciation should, as always, pick their entry points, and consider that the benefit of lower costs may already be reflected in the stock price rise.

lyondellbasell.com

For further details see:

LyondellBasell Industries To See Lower Costs, Keeps ESG Focus