XLY - Macro Headwinds Ahead Expect Volatility In Consumer Discretionary Select Sector SPDR ETF

2023-08-28 11:39:52 ET

Summary

- Consumer discretionary sector predicted to enter bear market due to macroeconomic headwinds.

- Resumption of student loan payments on Oct. 01, 2023 could impact market.

- Other factors include skyrocketing credit card debt and debt servicing as a percentage of disposable income.

THESIS

Due to the macroeconomic headwinds mentioned, we believe the consumer discretionary sector will struggle to grow earnings and enter bear market territory in the near term.

1. STUDENT LOAN PAYMENTS

The biggest catalyst to push markets lower is the fact that student loan payments will resume on Oct. 01, 2023. When student loan payments resume, there are two ways the market may react.

The first: the market may very well just ignore this fact and continue on the bullish path that A.I. has generously provided thus far in 2023. If this is the case, then the markets may enter into another historic bull market similar to what we saw from the second half of 2009 through 2018 and again from March 2020 to January 2022. This is, of course, provided that A.I. continues to fuel revenue growth for these major tech companies. The market recovery from the pandemic of 2020 was unparalleled to any other bull run/recovery in history. Within two years, the market recovered the roughly 35% losses seen in March 2020 plus added an additional roughly 40% in gains from the pre-COVID high! PHENOMENAL!

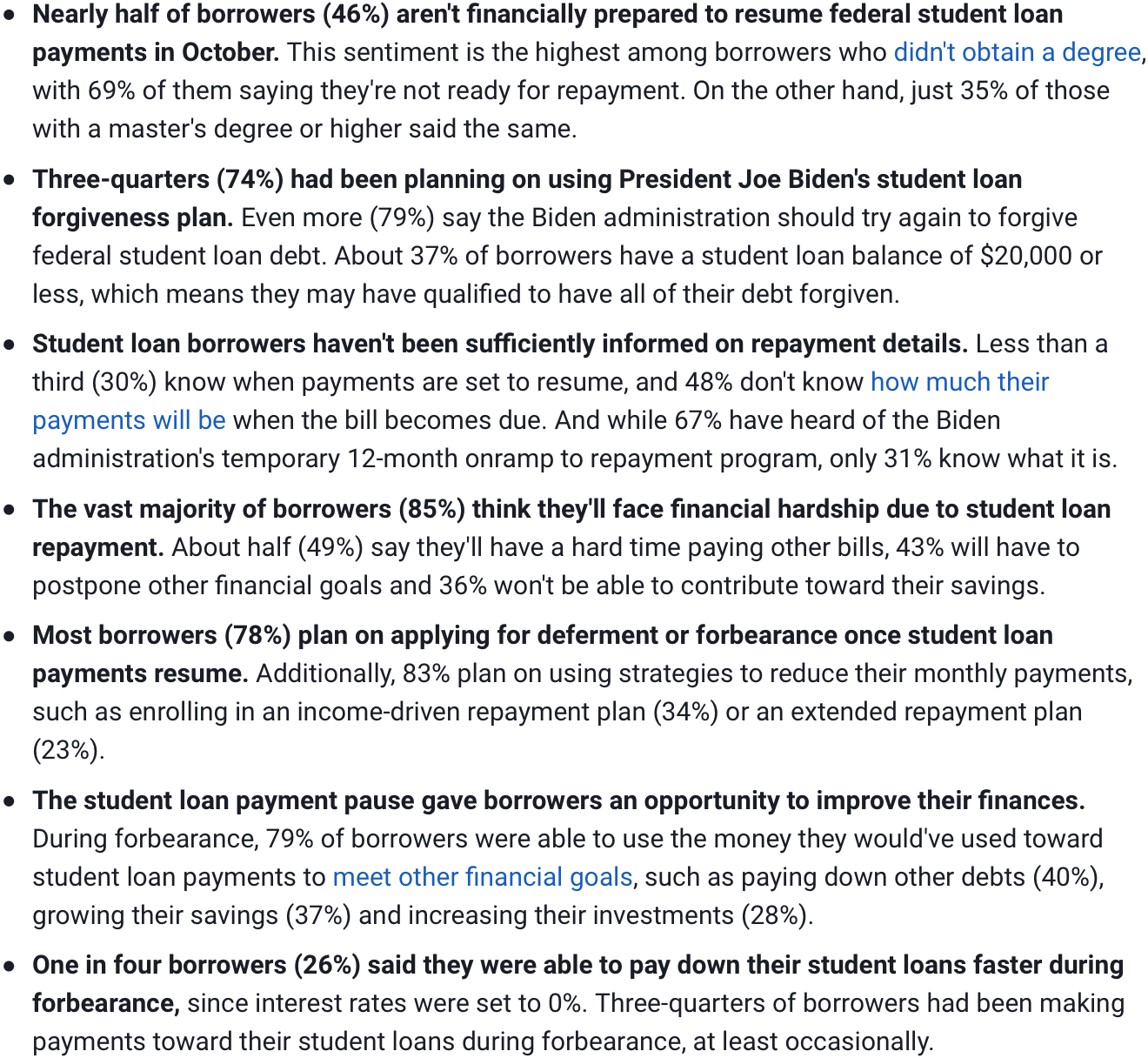

The second: the market may slide lower caused by a huge hit to the economy. Of the roughly $1.77 trillion in student debt, about 10% of that is held by private lenders (banks, credit unions, and other lenders). That leaves roughly $1.6 trillion in federal student loans that need to be paid. If the majority of student loan borrowers can pay back these loans and make the minimum payments, then all is well that ends well. However, the sentiment from the market and media is that borrowers cannot and will not be able to make these payments. One example of this is U.S. News recently surveyed 1,202 student loan borrowers. Of these, "(46%) aren't financially prepared" to make their student loan payments and "(85%) think they'll face financial hardship due to student loan repayment." Below is a snippet of the survey findings. Find the full survey article and results here.

{kind=link}

Summary of survey results (U.S. News)

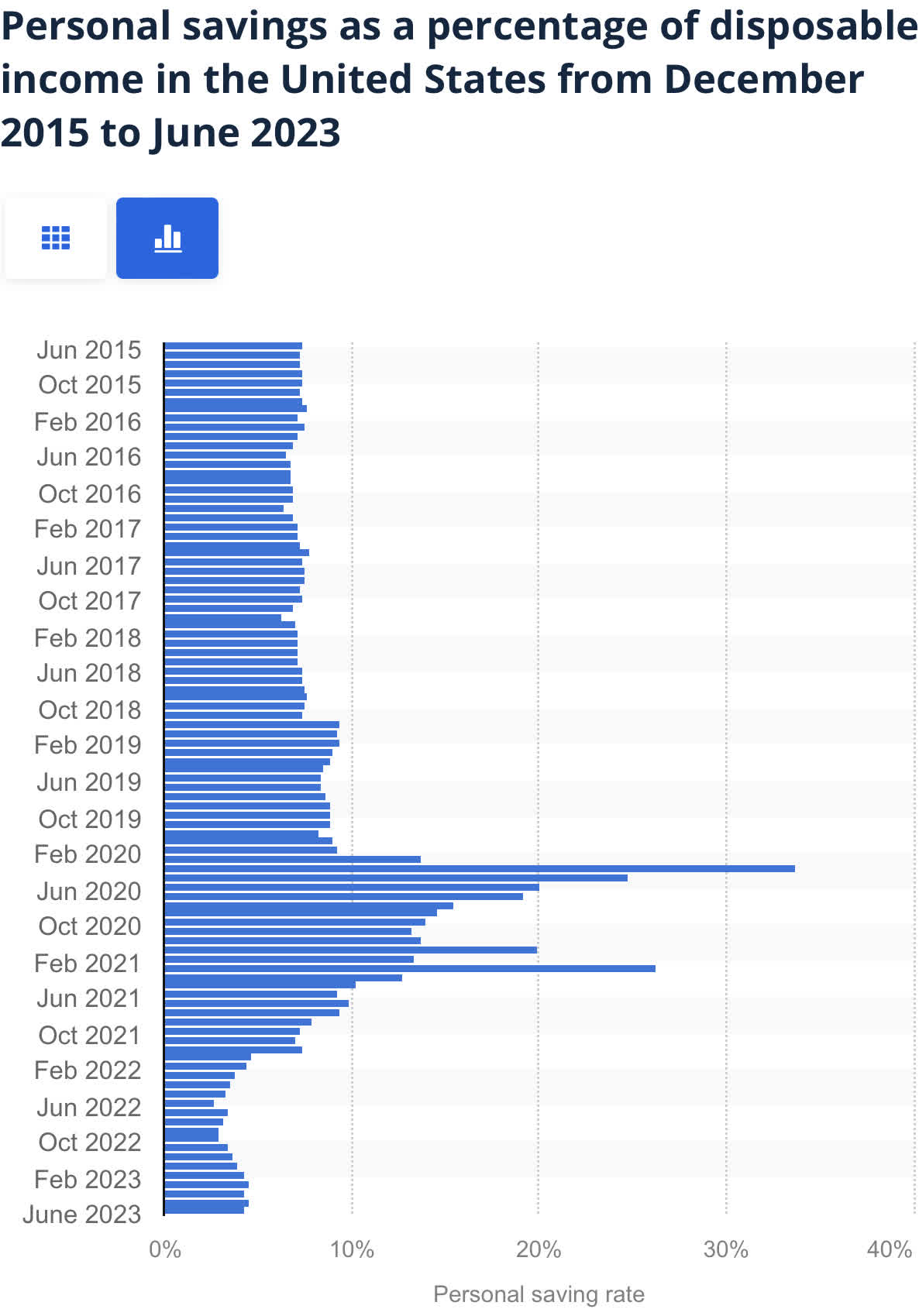

Since these student loans are held by both students and their parents, this will have a ripple effect throughout the economy. Consumer discretionary stocks will be hit the hardest due to the lack of "spending money" the typical consumer will have at their disposal. As you can see in the chart below, currently 9.63% of the average consumer's disposable income is going towards servicing their debt. Surely, that number will rise when these student loan minimums are thrown in the mix.

To give an estimate, the average household income in the U.S. is $70,784 according to the most recent U.S. Census Bureau Current Population Survey done in 2021. To give the consumer the best chances possible, let us assume that this consumer files their taxes married, filing jointly which would put them in the 12% federal tax bracket . The federal taxes owed on this income would come out to $8,054.08. Let us also assume that they also reside in a state that has no income tax. To make this example as simple as possible, let us also assume this consumer has no other expenses (housing, insurances, groceries, utility bills, auto payments, credit card payments, etc.). Although most, if not all, consumers have a combination of these expenses aforementioned. Now, let us take into account the range of minimum student loan monthly payments for the class of 2021 which ranges from $354/mo - $541/mo. On an annual basis, that range is $4,248/annum - $6,492/annum.

Using the net annual income after taxes of $62,729.92, the range of disposable income needed to service student loan debt alone sits anywhere between 6.77% - 10.35%.

That is, of course, assuming no other debt. Clearly from the chart above, debt servicing as of today (2023/08/25) is taking about 9.63% of the average consumer's disposable income. Now add in the student loan servicing requirements and that brings the debt servicing as a percentage of disposable income to 16.4% - 19.98%! This will surely take a toll on consumer spending!

2. CONSUMER CREDIT CARD DEBT ON THE RISE

If one good thing came out of the pandemic, it was that consumers were starting to save more money and get out of debt.

{kind=link}

Statista

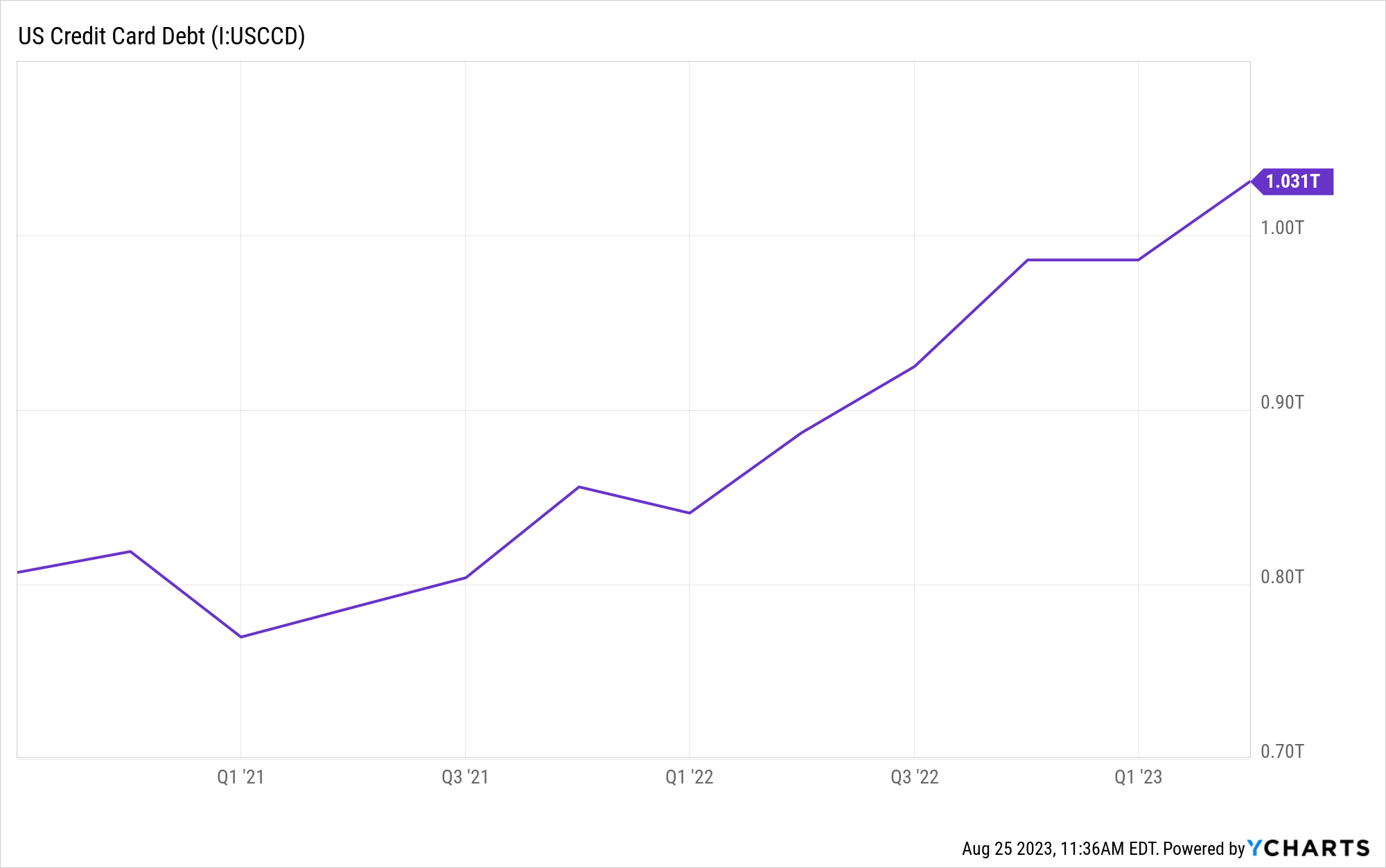

Now, all that progress is long gone. Since COVID, U.S. consumers have been digging themselves into a debt hole. This hole, is getting bigger by the minute. As you can see below, since the lows of COVID, consumer credit card debt has skyrocketed. This is due to several factors of which the most important is: inflation. Costs have been on the rise ever since, and at a fast pace. In order for most consumers to keep up with rising costs, most have been utilizing credit cards to make their everyday purchases. Below is a chart that shows the U.S. credit card debt on the rise ever since the pandemic. The U.S. consumer is strapped for cash now more than ever before, and it is not slowing down!

{kind=link}

YCharts

CONNECTION TO THE CONSUMER DISCRETIONARY SECTOR

After seeing the current state of the U.S. consumer, it is easy to see that discretionary spending will be on the decline going forward as consumers will have less and less "spending money." Consumers are already tying up almost 10% of their disposable income towards their debt. This is excluding student loans which will add another 6-10%, effectively doubling their debt servicing needs. The solution is clear. Consumer discretionary spending must fall to compensate for the rise in debt servicing. The expectation is consumer spending will fall at or more than the increase in debt servicing. With that being said, looking ahead to Q4 2023 and Q1 2024, consumer discretionary earnings will be a big focus for the state of the economy and market as a whole.

For further details see:

Macro Headwinds Ahead, Expect Volatility In Consumer Discretionary Select Sector SPDR ETF