CA - Mako Mining: It's Time To Leverage Up On Gold

2023-11-23 07:55:24 ET

Summary

- Gold is projected to double by 2030 based on fundamental indicators such as the boom-bust cycle and the Fed funds rate.

- Central banks are increasing their gold holdings, indicating long-term support for the gold price.

- Mako Mining is a junior gold miner with high leverage, low production costs, potential for growth, and a clean balance sheet.

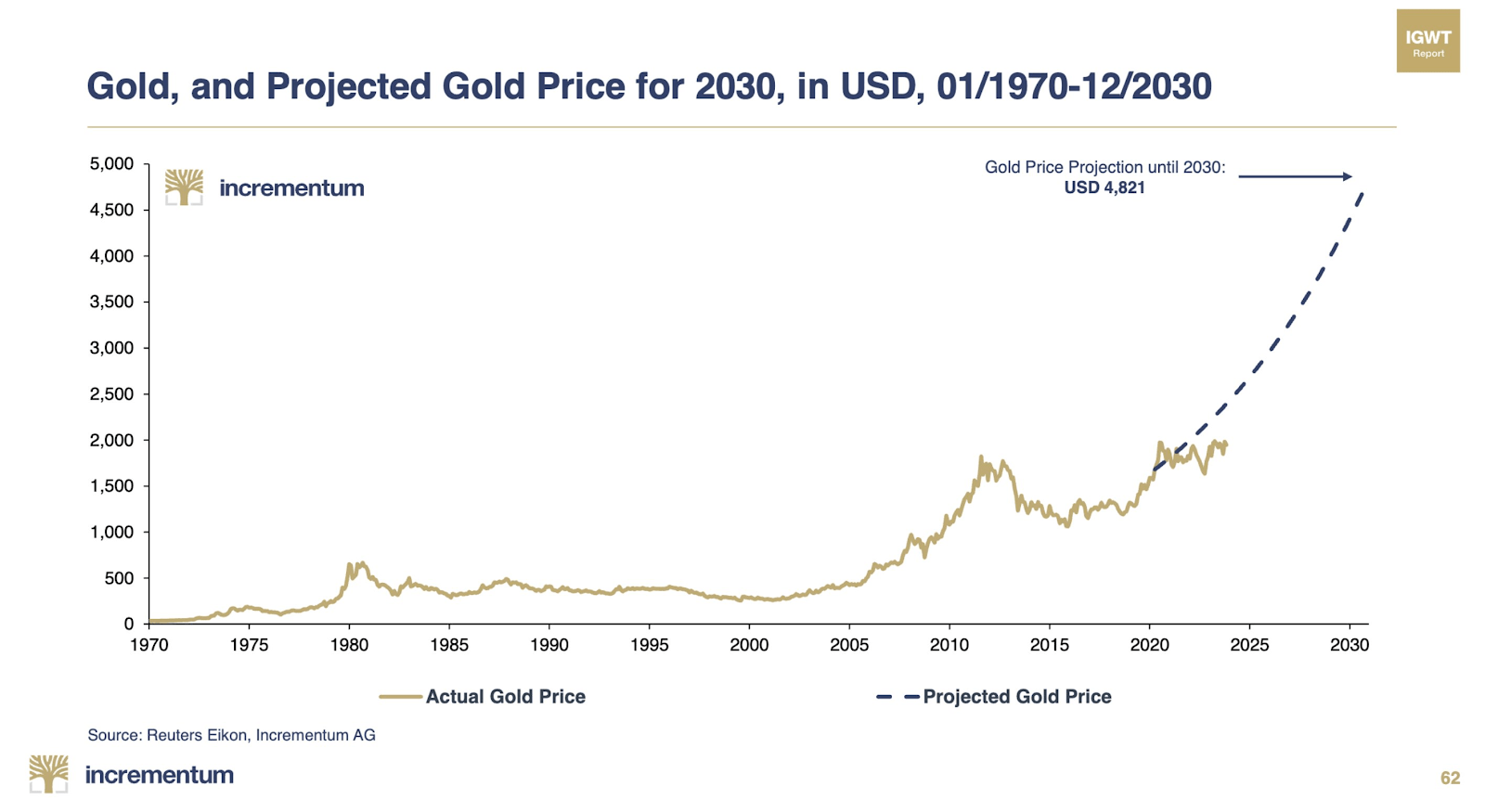

What if I told you gold is projected to double by 2030? It is not a fantasy, there are fundamental indicators that support this outlook.

{kind=link}

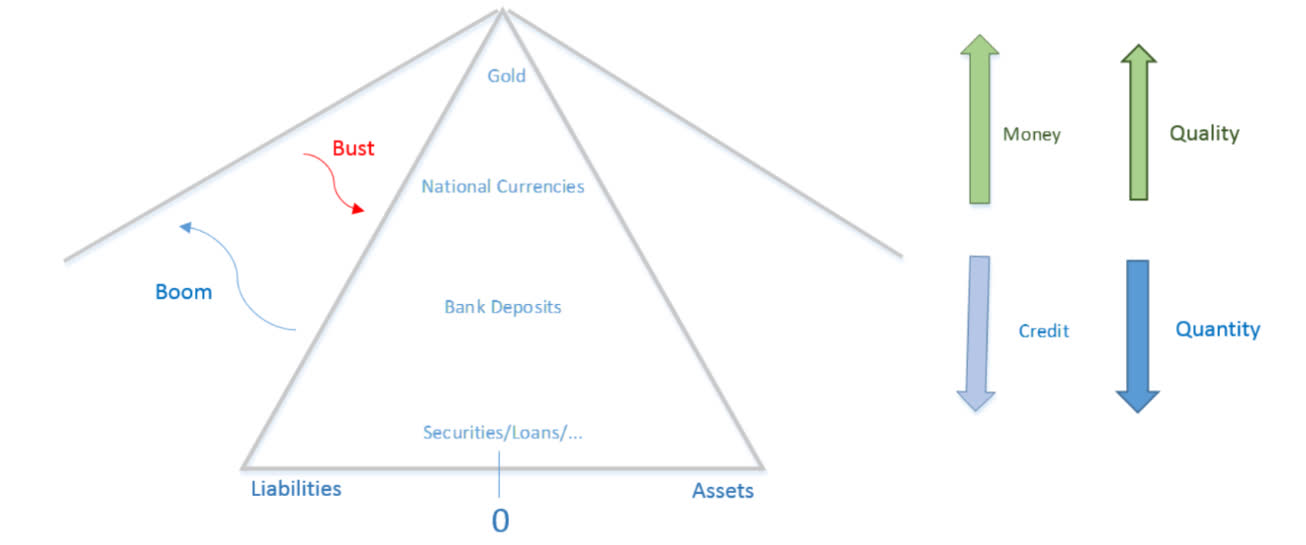

The most important indicator to look at is "The Boom-Bust Cycle". The economy expands and contracts. When we are in expansion, liquidity flows from money to credit. Conversely, when we are in contraction, liquidity returns from credit to money. Where are we currently in this cycle?

{kind=link}

Currently, we are in a period of scarcity, which means the yield curve is inverted. Short term maturity money markets are providing a higher yield than longer term treasury and equity securities. The natural equilibrium therefore pushes liquidity from credit back to real money: gold!

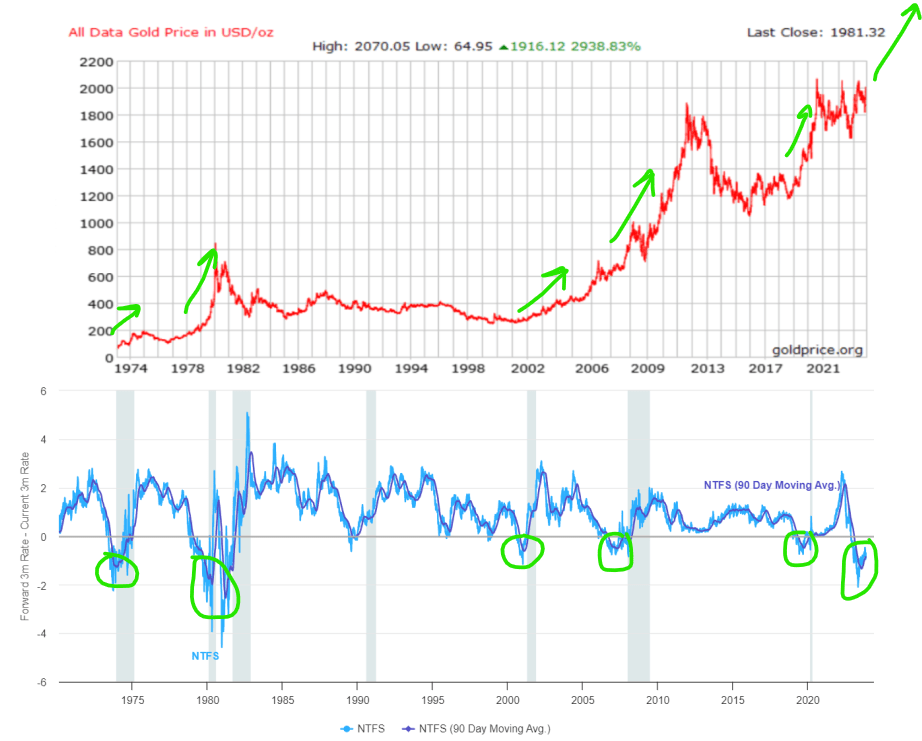

On the chart below (Near Term Forward Spread), we see periods of inversion encircled in green, which always lead to a higher gold price and today is not different.

Federal Reserve Board of Governors

{kind=link}

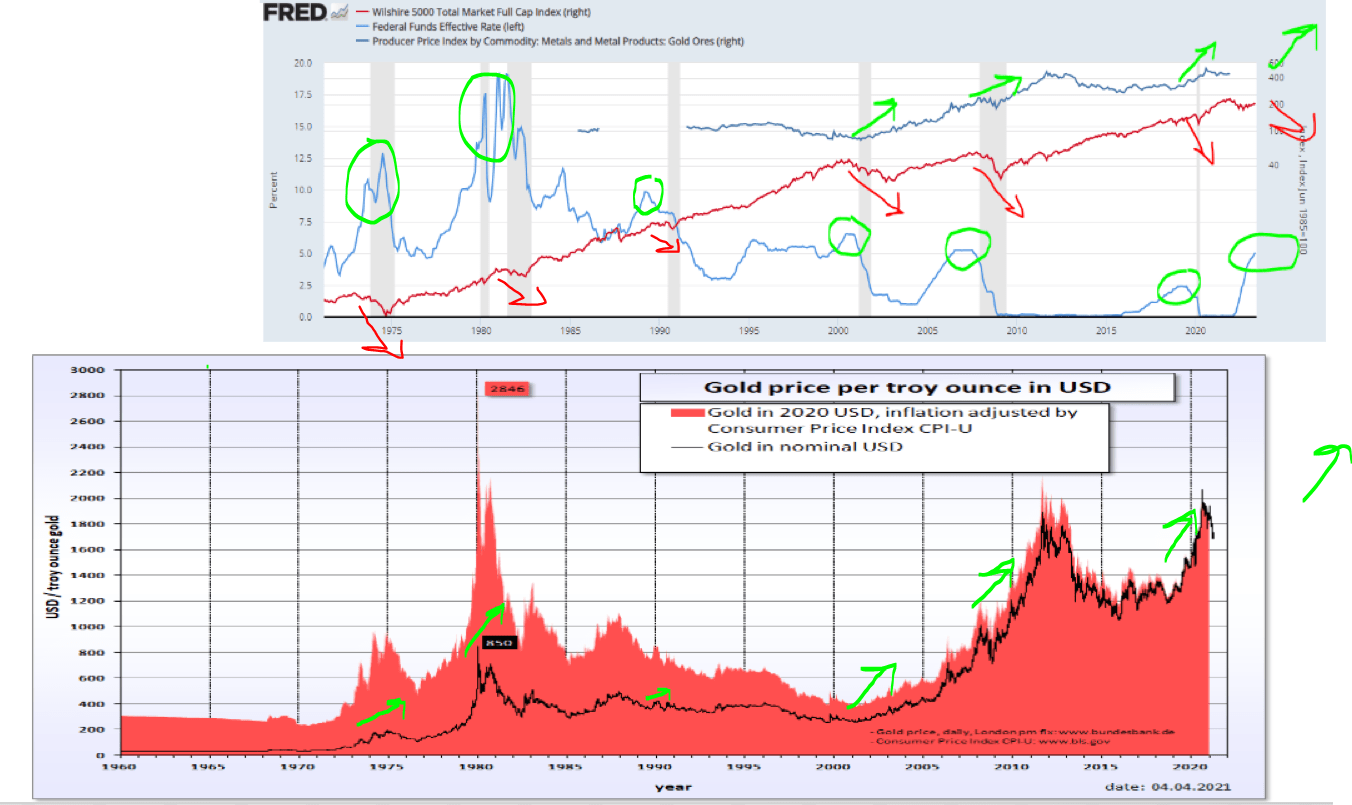

The second most important indicator is the Fed funds rate. The odds of a rate cut by the Federal Reserve at the May 2024 FOMC meeting has increased to 60% due to a weakening economy. The unemployment rate has moved up, manufacturing is deteriorating, forward earnings are downgraded, inflation is still elevated, there are increasing geopolitical risks and leading indicators are moving downwards. Whenever rates are cut, stocks move lower and gold moves higher. Additionally, the U.S. dollar will fall as interest rates go lower. This will give an additional boost to the gold price.

{kind=link}

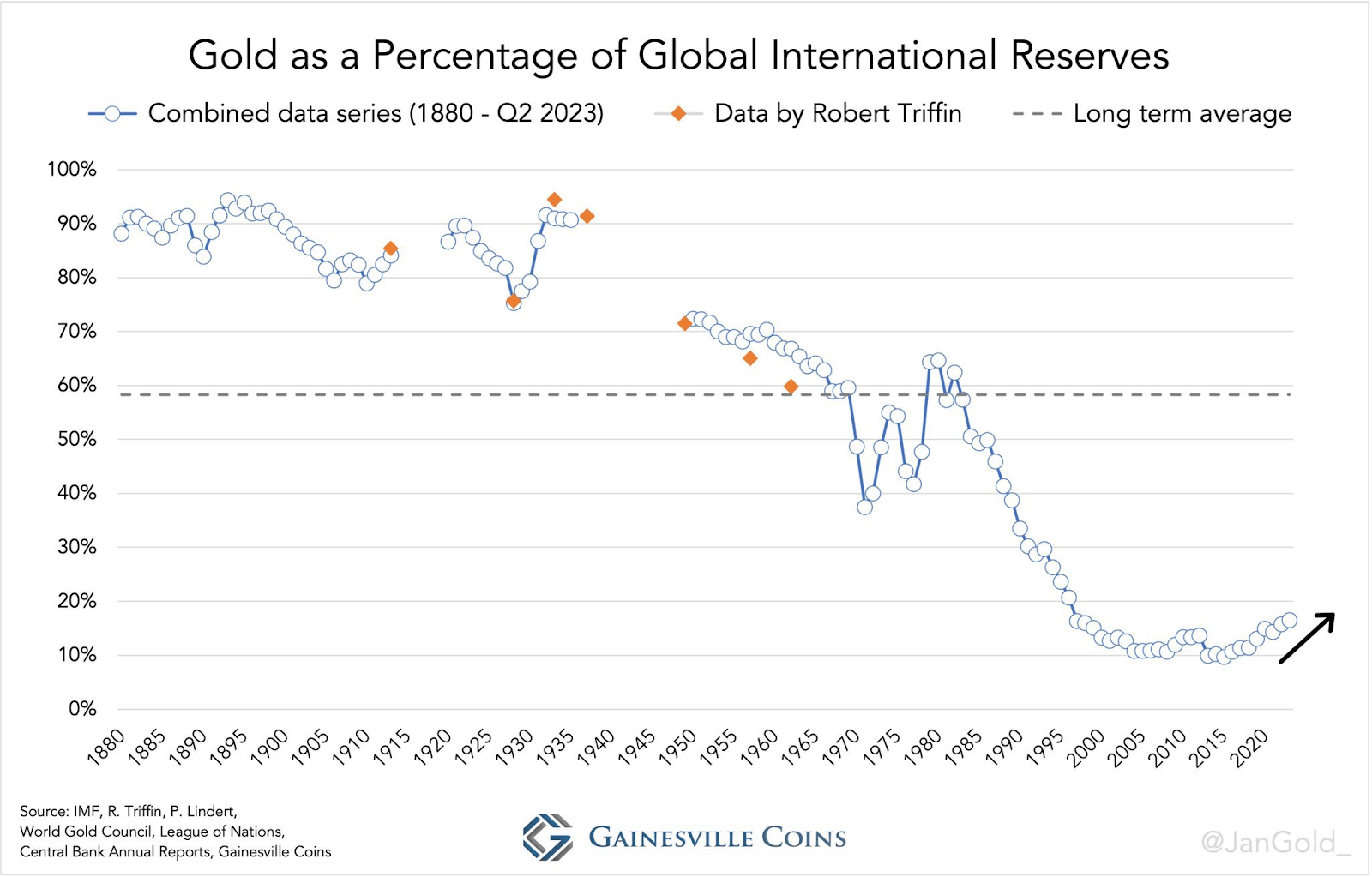

The third indicator comes from central banks. Since the 2008 financial crisis, gold demand from central banks has increased. The chart below shows that central banks have a long way to go to reach historic levels of gold as a percentage of global international reserves. I expect that central banks will keep supporting the gold price for many years to come.

{kind=link}

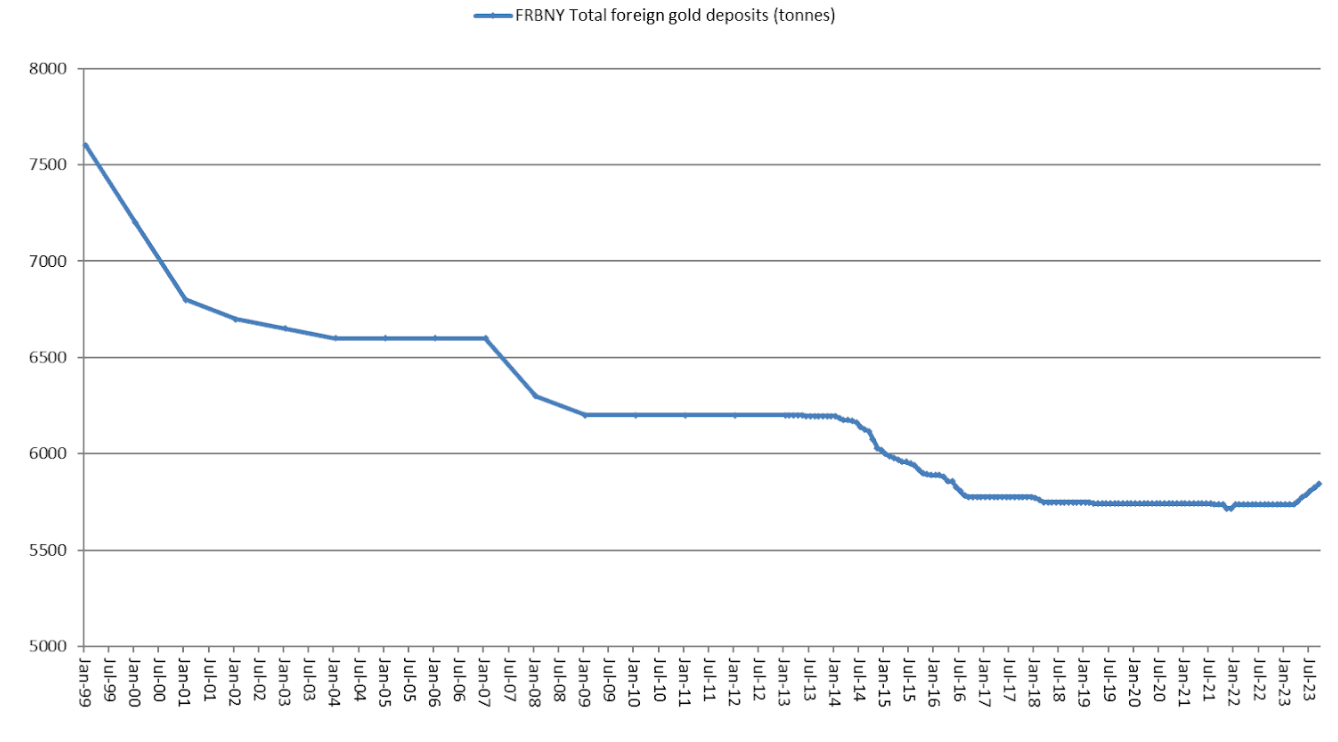

What is very peculiar is that foreign gold deposits at the Federal Reserve Bank of New York have moved up for the first time since two decades. This is evidence that central banks are serious about increasing their gold holdings.

Federal Reserve Bank of New York

{kind=link}

Other bullish indicators for gold are: good seasonality going into the end of the year, increasing debt to GDP and a high Shanghai gold premium compared to the spot price of gold.

I have laid out the case for gold going much higher, but how do we actually play this? The answer is: Leverage!

However, not all leverage is equal. There are several parameters that we need to assess to gain the highest leverage with the highest quality. The parameters are as follows:

- High leverage

- High margin

- High growth

- High mine life

- High grade

- Low valuation

- Low debt

- Low capex

- Great management

We might need a miracle to find a company that adheres to all these parameters, but I actually found one: Mako Mining ( OTCQX:MAKOF ).

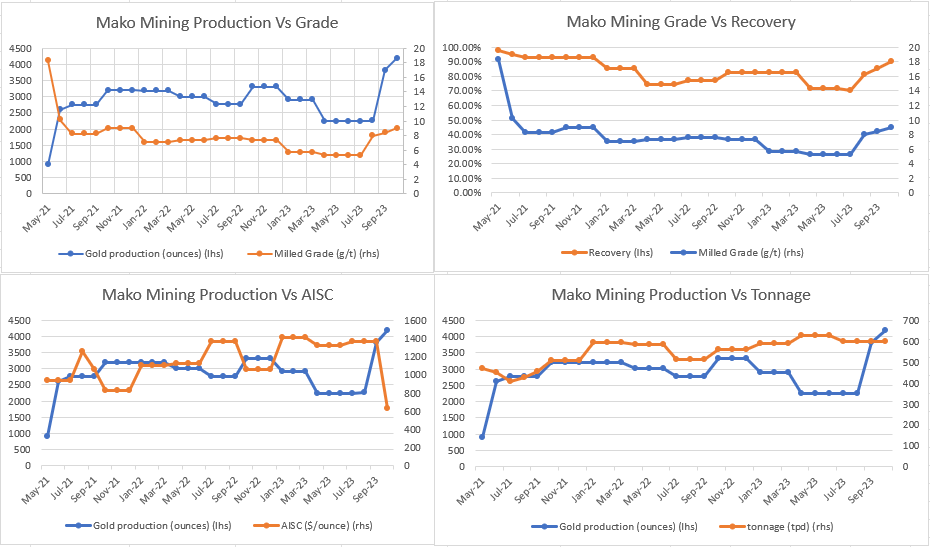

Mako Mining is a prospective junior gold miner with operations in Nicaragua engaged in a 600 tpd open pit operation, which went in commercial production in 2021. There have been hiccups during the startup (low recovery, low grades, low tonnage), but those problems have all been resolved today as can be witnessed from the charts below. I believe this is a turnaround story that hasn't been fully appreciated by the market yet. Let's go over the parameters now.

{kind=link}

1) Leverage

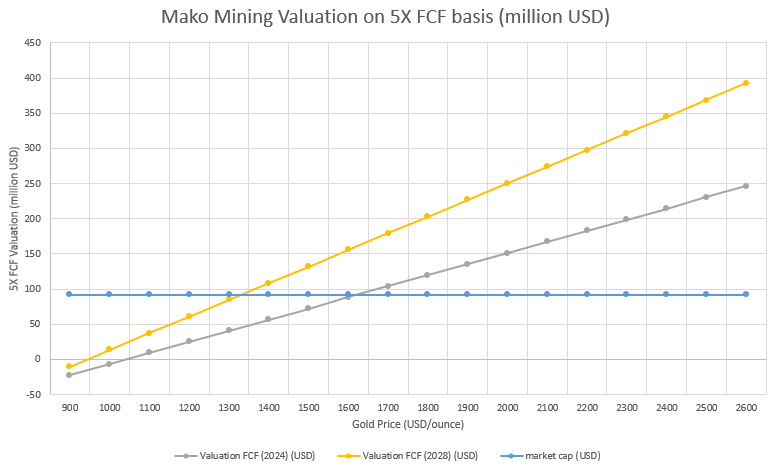

Out of 30 gold miners that I follow, Mako Mining provides above average leverage of 3.5 to the gold price. If the gold price goes up 10%, then the value of 5X net income goes up by 35%.

Correlationeconomics

The following chart illustrates the leverage in function of the gold price on a 5X after-tax free cash flow basis for the current 600 tpd operation (year 2024) and for a future 1000 tpd operation (year 2028).

{kind=link}

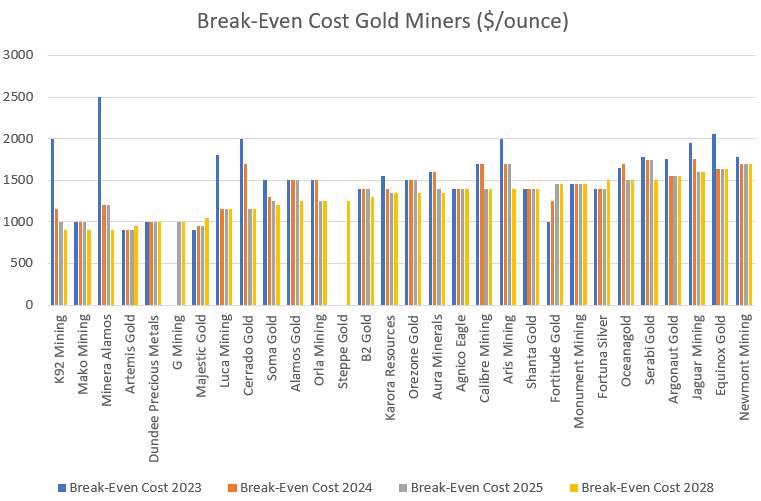

2) Margin

Not only does Mako Mining provide high leverage, it actually does this at a very low cost of production of US$900/ounce after operating cost, interest payments, CAPEX and tax. The AISC is projected to hit a number below US$700/ounce in Q4 2023.

{kind=link}

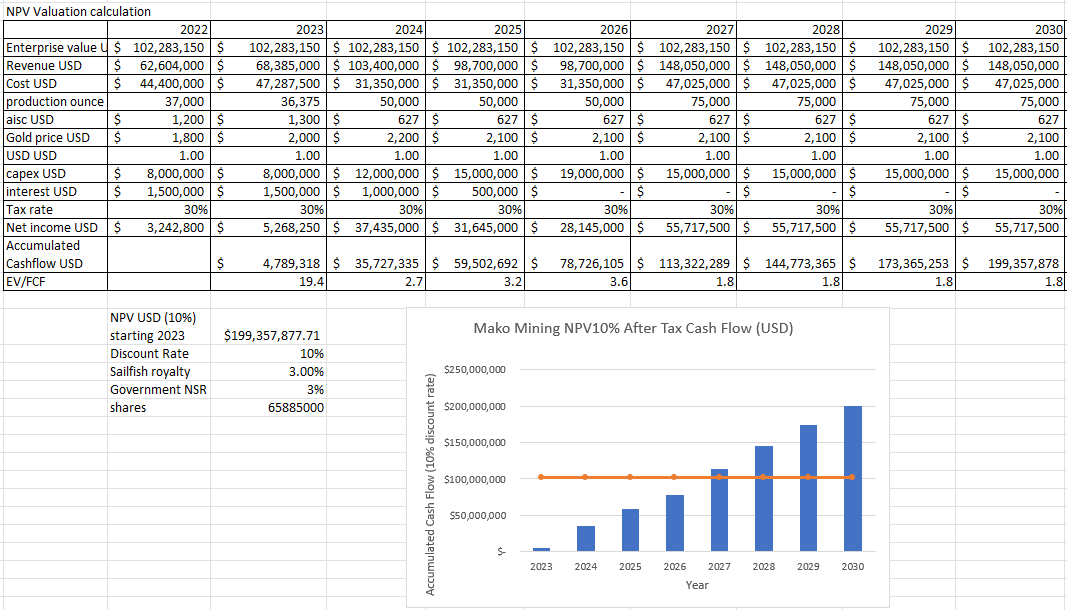

3) Growth

The company has high growth as it has potential to expand its operation from the current 600 tpd to 1000 tpd when the resource allows it. As a result, the Net Present Value (10% discount rate) is significantly higher than the current Enterprise Value.

{kind=link}

4) Mine Life

Mako Mining just released an updated mineral resource which supports a mine life of around 6 years at the current production rate, which is pretty good for a junior with a prospective undrilled land package.

Mako Mining NI43-101

5) Grade

The NI43-101 shows that the resource is very high grade at 16 g/t and what's even more impressive is that it is an open pit resource that is shallow. You don't get these kinds of grades anywhere for an open pit mine.

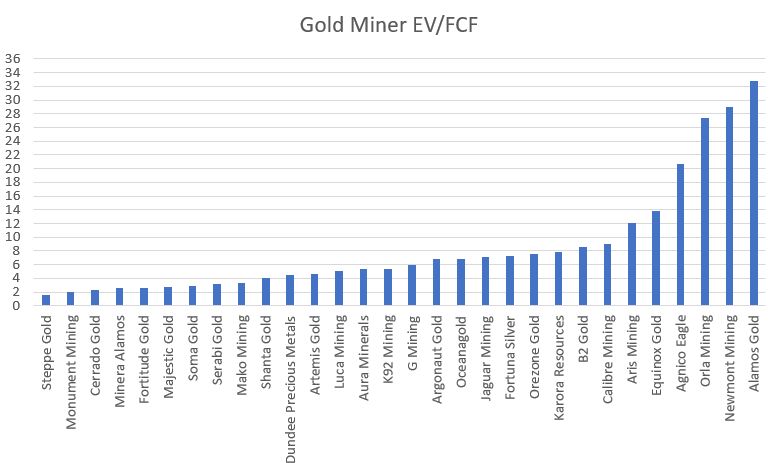

6) Valuation

The best thing of all is that the stock is still cheap at an after-tax EV/FCF of 3.5, which positions the company among the best opportunities in the gold miner space. Their cash flow allows them to execute buybacks (5% of outstanding shares), which will enhance shareholder returns.

{kind=link}

7) Debt

The company has a very clean balance sheet with little to no debt compared to its cash flow. Term loans outstanding are at US$12m while I'm expecting free cash flow to come in at a pace of US$25m per year at the current gold price.

Mako Mining Balance Sheet

8) CAPEX

Mako Mining is already in production and doesn't require any CAPEX to get the operation going. For the expansion from 600 tpd to 1000 tpd, the CAPEX is very low at $4m USD. Since the deposit is shallow, I don't expect a lot of CAPEX to get the other pits in production either. So you get more than 50% growth at almost no cost.

9) Management

Last but not least, management is key. The CEO Akiba Leisman, chemical engineer, has turned this operation around and what I really like is his communication. He's on top of everything and will help you out with any questions you might have. He's being assisted by COO Jesse Muñoz who has over 35 years of experience working in the domestic and international mining sector.

10) Conclusion

In conclusion, Mako Mining is a gem in the rough and a once in a lifetime opportunity to get into a gold miner with high quality leverage to the gold price. Seeing all these positives, it seems difficult to find possible risks to this story but there certainly are. First of all, the company operates in Nicaragua and is not a low risk country to invest in. Nicaragua is under sanctions of the U.S. due to its antidemocratic practices and attacks on civil society. However, Mako Mining's operations are not impacted by these sanctions. Second, the company has not shown profitability yet and had a cash burn of around US$2m per quarter. Also, in case gold goes down, cash flows could be further impacted. Third, since Mako Mining is a microcap, trading volume and liquidity is low. Investors should be aware that there could be challenges in building or exiting a position. And finally, operations are currently at capacity, but the company has a history of mistakes concerning permitting, recoveries, grades and tonnage. For example, the decline in grade and tonnage we saw last year was due to a permitting delay which originated from poor decision from management. Management has learned from these mistakes and that's visible from the operational data in the last two months.

For further details see:

Mako Mining: It's Time To Leverage Up On Gold