CA - Manulife Preferred Shares: The 7.8% Yield Prospect

2023-06-13 10:00:00 ET

Summary

- Manulife Financial Corporation delivered a solid Q1 2023 quarter and continued executing its strategy.

- The large asset to equity ratio though makes a big rerating unlikely until Manulife successfully navigates the next recession.

- We go over the Manulife preferred shares with big, conservative yields.

Note: All amounts discussed are in CAD unless specified otherwise.

When we last covered Manulife Financial Corporation ( MFC , MFC:CA ) we downgraded the outlook and booked our gains. Specifically, we said:

It has delivered great results considering the challenging environment. We are downgrading the shares to a Hold and think the upcoming financial market turmoil will create better entry points for all financial stocks. We still own the shares, and our version of reducing risk is to have covered calls on the stock.

Source: Time For A Little Caution .

The timing of that call was interesting as it happened just before the regional banking turmoil in the US. That selloff impacted all financial stocks, with the S&P Regional Banking ETF (KRE) taking the lead on the way down. Canadian large banks like Bank of Montreal (BMO) and Royal Bank of Canada (RY) also suffered.

Manulife has escaped relatively unscathed, and Sun Life Financial Inc. ( SLF , [[SLF:CA]]) is actually up over this timeframe. Has MFC become a defensive play in the era of financial upheaval? We look at the recently released Q1 2023 results and tell you why MFC marches to a different beat. We also tell you what is our favorite play for this company.

Q1 2023

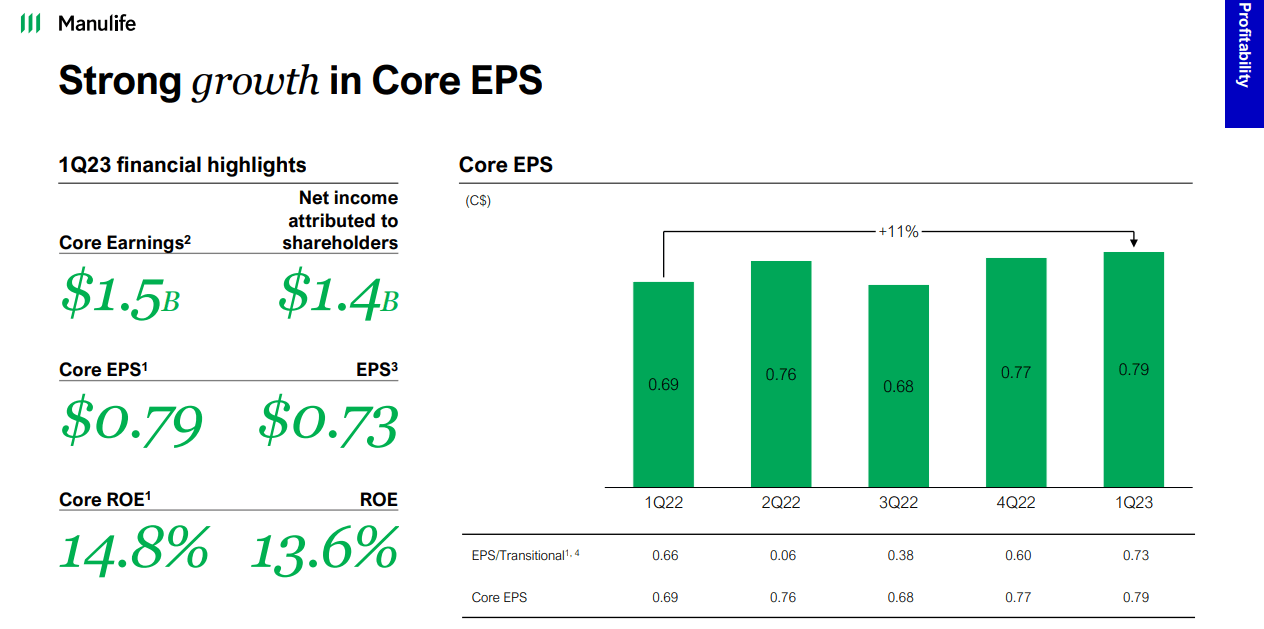

The MFC Q1 2023 was about in line with estimates at $0.79 per share.

{kind=link}

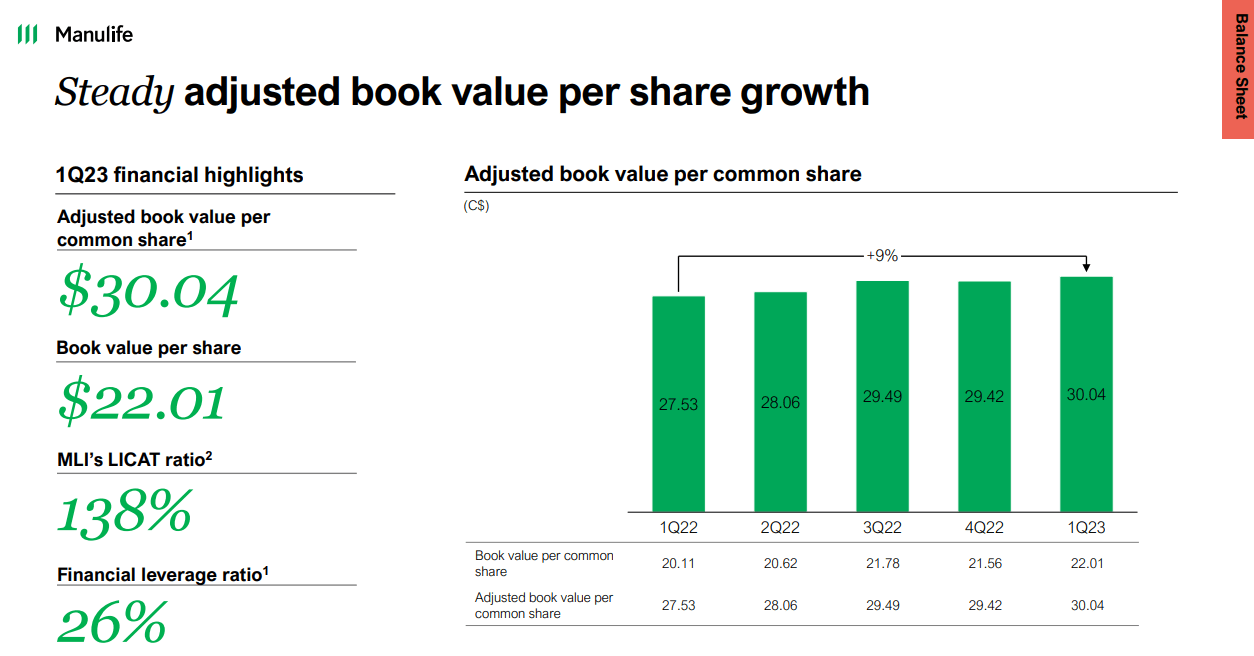

Book value rose by about 9% year-over-year, despite $141 million charge for potential commercial mortgage losses.

Manulife Presentation

The most watched LICAT ratio drifted higher to 138%, and the company delivered solid core return on equity of 14.8%.

{kind=link}

While overall Manulife Financial Corporation results were solid, Asia continued its weakness with earnings down about 4% versus 2022. Manulife actually increased sales in the region but operating expenses crept up enough to negate the sales growth. Global Wealth & Asset Management was another area of weakness where earnings were down a whopping a 17% year over year. This again was due to higher expenses.

Outlook

While the Q1 2023 earnings had a few things to chew on, the fundamental long case here rests primarily on valuation expansion. Manulife does not need to do much as the P/E ratio is just near 8.0X. If the company can maintain earnings and use the capital excess for buybacks, we could see good returns. After all, it has an earnings yield of over 12%. If you add a slight valuation expansion over the next 5 years and assume that the business has even 2-3% intrinsic growth rates, you get to an easy 15% plus annualized return. Manulife for its part has been quite focused on the capital return aspect, and we have seen steady buybacks over the last 2 years.

Manulife Presentation

So what's the problem?

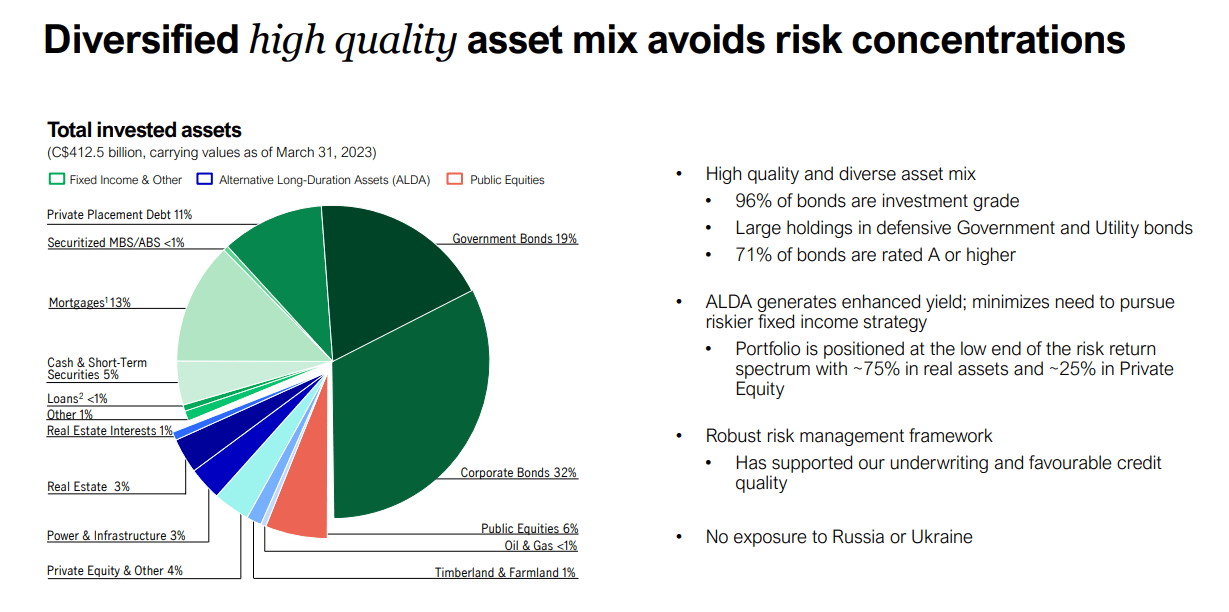

Well, the only issue from a long-term return perspective is how Manulife's massive balance sheet handles a recession. For those that don't get the picture, we will provide one.

A breakdown of some of these assets is shown next.

{kind=link}

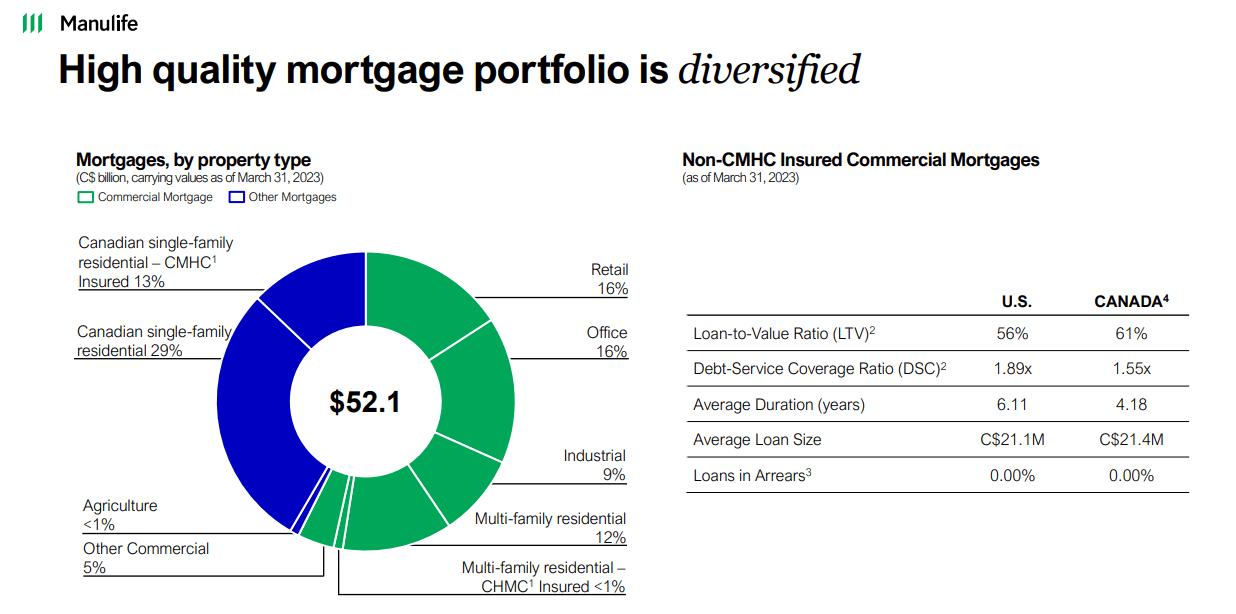

Most of that looks pretty good, but there is still risk in some segments. This segment below is like a commercial mortgage real estate investment trust, or REIT.

{kind=link}

Think of Blackstone Mortgage Trust, Inc. (BXMT) as being buried inside the company. Well BXMT has a market capitalization of just $3.3 billion USD, so Manulife's mortgage portfolio is several fold higher. While office exposure seems small in relation to this segment and certainly in relation to total assets, it is a very huge portion of the company's tangible equity.

This is the case with all financial companies and there is no denying the inbuilt leverage that these stocks have. You are generally not going to get them to trade at large multiples as some of them frequently blow -up. But Manulife still trades at a discount to both SLF and Great-West Lifeco ([[GWILF]], GWO:CA ).

Therein lies the potential and if Manulife can navigate the next recession well without losing too much ground, we think a multiple rerating can occur.

Our Pick

While we can wait and watch for the multiple expansion possibility we see the more immediate risks to the downside. Our data tells us that we are already in a recession and thanks to a very tight labor market, the Federal Reserve will hike a bit more than it should. The fallout won't be pretty and financial stocks are largely on our avoid list. For those interested in income though, Manulife's preferred shares which trade on the TSX offer a solid prospect. The entire list of Manulife's preferred shares can be found here .

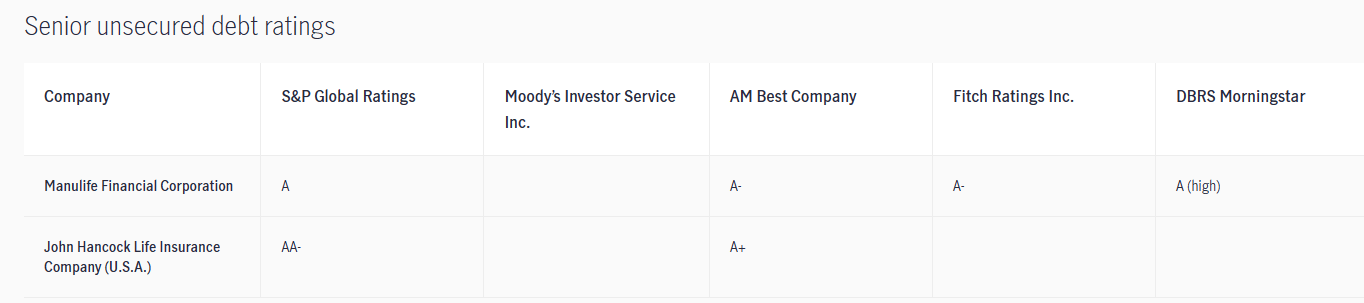

We will, however, be focusing on the one we like, Manulife Preferred Shares Series 13, ( MFC.PRK:CA ). These shares were issued in June 2013 and had their first reset in September 2018. They are now shortly due for their second reset this September. The features here are that they will reset at the Government of Canada ((GOC)) 5 year bond yield plus 2.22%. That will be the yield on par. Considering that the 5 year GOC yield has been on a tear, these shares have lagged on a relative basis. Currently the 5 year GOC yield is at 3.73% which would imply a reset rate of 5.95% on par. At the current price of $19.00, it would create a yield of about 7.82%. We see this as undervalued relative to its credit ratings. Manulife's senior unsecured debt carries A (Canadian Side) and AA- ratings (U.S. side) from S&P Global.

{kind=link}

Its preferred shares which rank below the unsecured debt carry a BBB+ rating from S&P global.

{kind=link}

Fitch ranks these two notches lower on the last run of investment grade. Note that like most banking and insurance segment preferred shares, these are non-cumulative. Of course a lot would have to go wrong to stop dividends here as preferred share dividends consume just 3% of core earnings.

Verdict

We think that focus on simplifying and de-risking the balance sheet (see this transaction), makes Manulife a solid choice for preferred share investment. On a pricing basis, the most recently reset Series 11 ( MFC.PRJ:CA ) provide a good idea of how much the market values certainty. Those were reset at 6.159% on par and currently $21.36, yielding 7.21% on the current price. We think that issue is undervalued as well, but we "prefer" MFC.PRK:CA. Those looking for "fixed" yields, i.e., non-resetting are likely to be disappointed. The two Manulife shares which have that feature, Series 2 ( MFC.PRB:CA ) and Series 3 ( MFC.PRC:CA ) only yield 6.3% at present.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

Manulife Preferred Shares: The 7.8% Yield Prospect