CA - Marathon Gold: Patience Required

Summary

- Marathon Gold is one of the worst-performing gold developers over the past year, down over 70% from its 2021 highs, and suffering an ~80% drawdown.

- The significant underperformance can be attributed to inflationary pressures that have contributed to weaker economics and a higher build cost at Valentine, plus an avalanche of shares dropped on investors.

- Unfortunately, the recent FS confirmed concerns about the degradation in project economics, and while this continues to be a robust project, the NPV (5%) and projected margins have dropped sharply.

- While I continue to like the project and think there's tremendous value in being a contrarian after 70%+ declines, I don't see enough upside to justify being long, and I see better relative value elsewhere.

2022 was a rough year for many gold producers, but the gold developers took it on the chin the hardest, with many suffering 60% plus drawdowns and ending the year down 50% or more. Unfortunately, while Marathon Gold ( MGDPF ) has been a serial outperformer for years since I highlighted it at US$0.60 in 2017 , this trend of outperformance turned on a dime in Q2 2022, with Marathon declining 70% in 2022 and ~80% from its highs. While this considerable drawdown might appear unjustified, it can be partially attributed to the avalanche of shares dropped on shareholders with a ~$110 million capital raise with half-warrants at the worst possible time following negative capex revisions at its Valentine Project in Canada. Let's take a look below:

Unless otherwise noted, all figures are in United States Dollars and are calculated at a constant 0.77 CAD/USD exchange ratio. Those figures in Canadian Dollars are shown as C$.

Valentine Project, Newfoundland (Company Report)

{kind=link}

A Painful Past Year For Shareholders

2022 was a year to forget for most of the gold sector, except for a few outperformers like i-80 Gold ( IAUX ) which led the sector in performance for a second consecutive year, and Agnico Eagle ( AEM ), which beefed up its portfolio with a timely merger and two smart follow-on deals to solidify itself as the highest-growth 2.0+ million-ounce producer. However, while it initially looked like it might be a decent year for Marathon Gold, a Newfoundland-based developer working to move its Valentine Project into production, things quickly turned south, and it suffered one of the worst drawdowns among $500+ million market cap names within its peer group.

The root cause of this drawdown can be attributed to the significant capex revisions at its Valentine Project, where upfront costs have increased from ~$235 million in 2020 to ~$411 million as of its most recent Feasibility Study [FS]. Worse, sustaining capital has also increased due to inflationary pressures, and operating costs are considerably higher, with cash costs soaring from $704/oz to $902/oz, moving Valentine from a very high-margin project to a slightly higher-margin project vs. other undeveloped projects. However, the capex increase had the most significant impact on the share price, given that it resulted in Marathon having to raise over $100 million in additional capital through equity issuance with warrants attached at the worst possible time.

Some investors defend the company and argue that this was entirely out of its control. They would be absolutely right from the perspective of higher costs and less robust margins, given that Marathon wasn't responsible for leaving interest rates at zero and handing out money which was one major factory in the inflationary boom we've seen. It also wasn't to blame for global supply chain headwinds, nor is it at fault for the consistently tight labor market for mining with a lack of skilled labor, which has contributed to wage inflation. Still, it should have been aware of these headwinds and might have been able to soften the blow from a share dilution standpoint had it been quicker to act.

In fact, Marathon Gold was benefiting from expensive currency (a strong share price) sector-wide in 2021 as inflation began to rear its ugly head. Between quarterly conference calls for miners and disclosure from companies building projects, it was pretty clear that inflation could present a serious issue and that 2020 capex estimates were at least 10% stale, if not more, meaning Marathon's 2020 build costs were likely to come in above $260 million in a best-case scenario. In fact, we saw disclosure from Iamgold ( IAG ) in Q3 2021 202 at Cote (Ontario, Canada), where capex increased sharply ($1.41 billion to $1.79 billion), and this followed an update in July 2021, with costs initially flagged as being much higher than 2020 estimates . At the same time, another producer with a Canadian development project was flagging similar cost creep at Magino , where costs were expected to be at least 15% higher.

The Magino construction project is tracking on schedule. Argonaut is currently reviewing all inputs including potential cost inflation, impacts of foreign currency exchange rates and changes in scope related to the initial capital estimate. While this review is ongoing, based on the best available information to date, the Company believes the initial capital remains within 15% of the previous guided estimate of between C$480 million and C$510 million.

- Argonaut Gold ( ARNGF ), May 2021

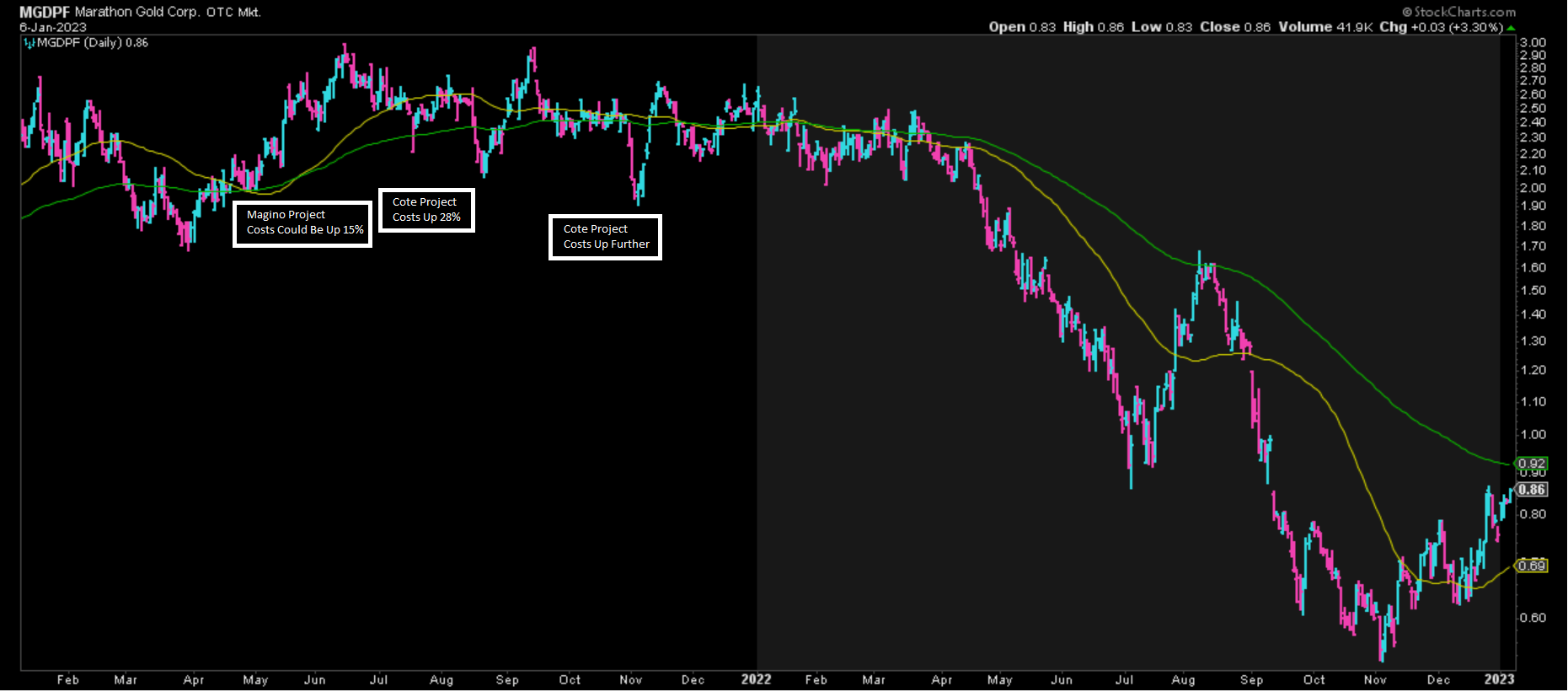

Marathon Share Price & Magino/Cost Cost Updates (StockCharts.com, Author's Notes)

{kind=link}

Given that two companies were flagging between 15% and 25% cost creep at other 10,000+ tonne per day Canadian projects in construction (which we now know turned out to be too conservative of estimates), Marathon didn't appear to be in any urgency to raise a moderate amount of contingency capital despite it being in a great position to raise money with its share price at multi-year highs despite these negative developments elsewhere. In fact, the company only completed one small flow-through deal for exploration dollars in May 2021 vs. raising hard dollars above US$1.80 in H2 2021 to take a more proactive approach.

This turned out to be a mistake, and I believe the time to raise money for juniors is when you don't need it but can do so very favorably. Not when you do need it, the market knows it, and you're in a weaker position. That said, Marathon is not the only company that waited far too long to raise capital which ultimately led to an avalanche of share dilution being dropped on shareholders, and SilverCrest ( SILV ) was one of the only companies that chose to be proactive and raised more than it needed for its Las Chispas build to be on the safe side.

Still, whether one chooses to blame Marathon for not seeing this significant inflation coming down the pike, I think some blame is warranted due to not being more conservative and adding some contingency. Unfortunately, the fully diluted share count has nearly doubled following its massive capital raise (~138 million shares + additional warrants) due to missing this window to raise at more favorable prices into a very hot equity market.

Marathon Financing (Company News Release)

{kind=link}

So, how does the project look today?

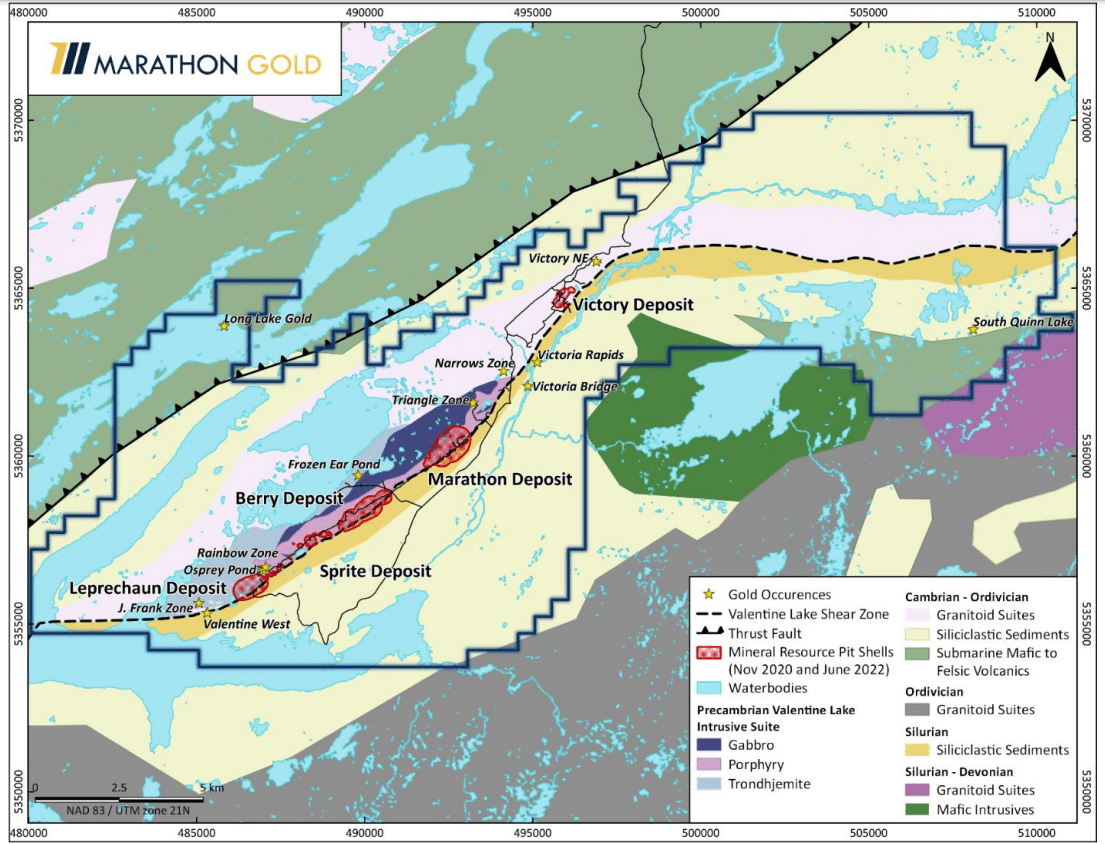

Looking at the below snapshot, the project is quite similar to 2020, with this still being a relatively owner-operated high-grade open-pit project with a ~6,800 tonne per day throughput rate, increasing to ~11,000 tonnes per day in Phase 2. The significant difference is that it is now a three-pit operation vs. two pits previously, with Marathon adding considerable ounces from its new Berry discovery that conveniently lies right next to the planned processing facility. Meanwhile, Marathon has focused on higher grades in its 2022 FS vs. its 2020 FS, resulting in a higher strip ratio by trimming more marginal blocks off its model. Some of these lower-grade ounces are expected to feed into the latter portion of the mine life anyways.

Valentine Project - Capex & Upfront Costs (Company Presentation)

{kind=link}

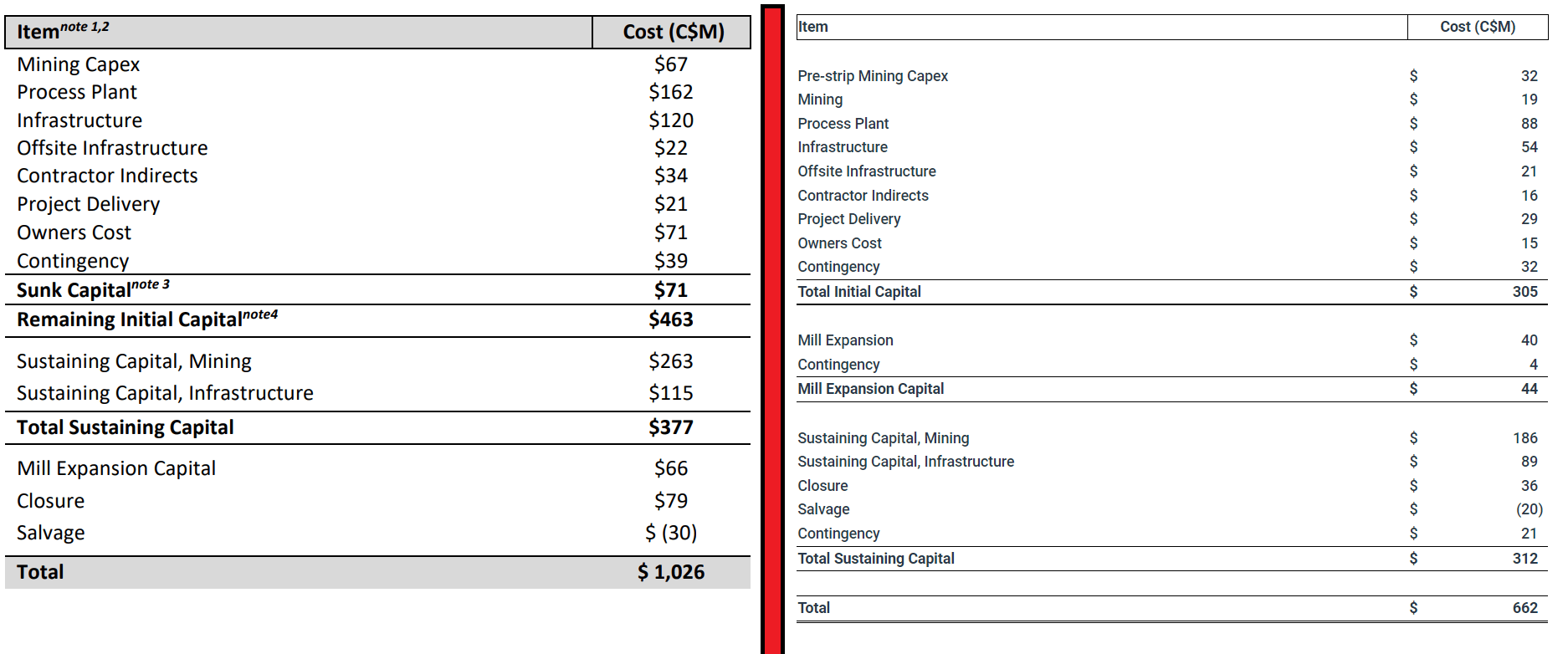

Looking at the project today, we can see that upfront capex has increased ~75% to ~$411 million ($55 million in sunk costs already). Total capex has increased to ~C$1.03 billion [US$790 million] while all-in-sustaining costs over the life mine are expected to average US$1,046/oz (2020 FS: $833/oz). However, this increase in capex is partially related to a larger project, with the production profile up 20% on a LOM basis due to the benefit of higher grades and more gold produced (~2.7 million ounces vs. ~2.1 million ounces). Finally, the project has a slightly longer mine life, which is now expected to produce an average of ~178,000 ounces over 14.2 years vs. ~148,000 ounces over 13 years.

Capital Costs 2022 vs. 2020 (Company Reports)

{kind=link}

That said, if we compare capex side by side, we can see that we've seen a massive increase in total capex, and this certainly weighs on the project economics. So much so that Valentine's After-Tax NPV (5%), despite a higher gold price ($1,700/oz gold vs. $1,500/oz) and another pit being added, has barely increased to just C$648 million [US$499 million] vs. C$600 million [US$462 million] in the 2020 FS. On an apples-to-apples $1,700/oz gold price comparison, its NPV (5%) has plunged from US$629 million to US$499 million, which is certainly not ideal. Unfortunately, this was quite a departure from my estimates of ~$350 million in capex and $970/oz AISC, but not a huge surprise, given that the updated FS is being completed at a time of potential peak inflation.

Then (2020) vs. Now

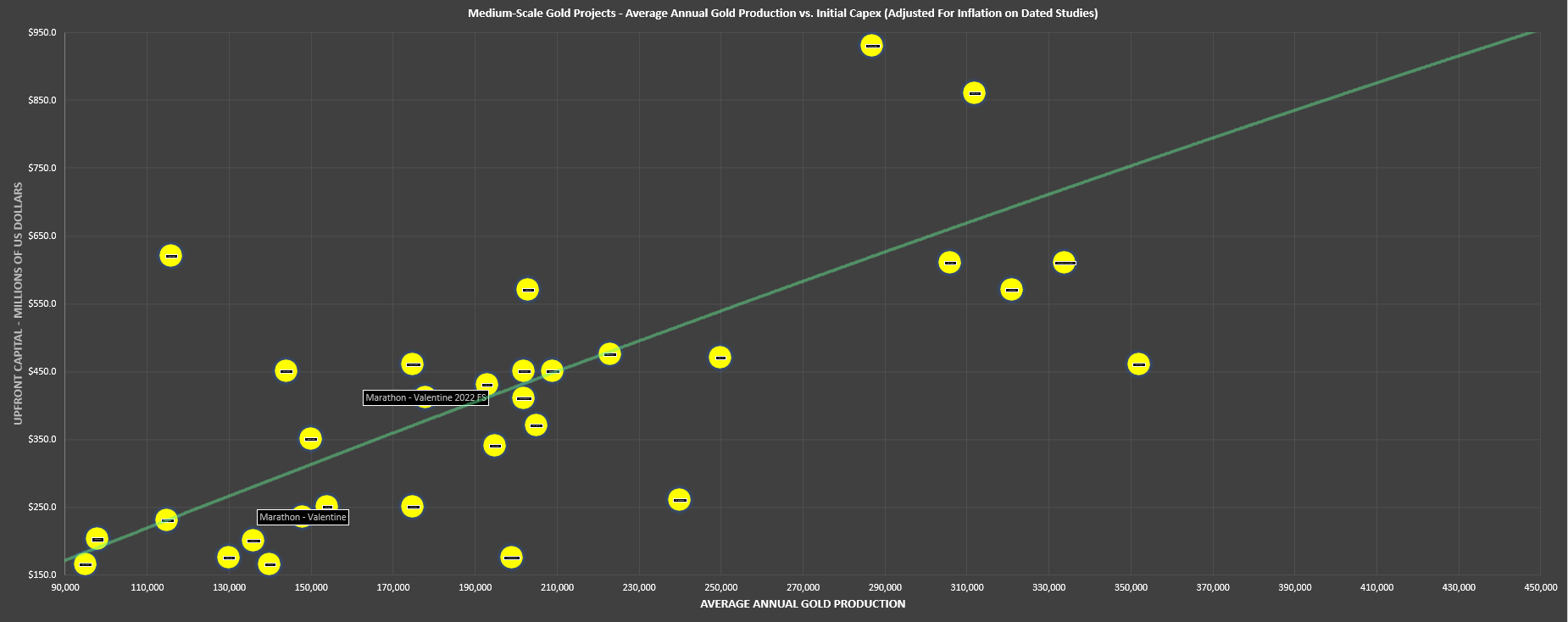

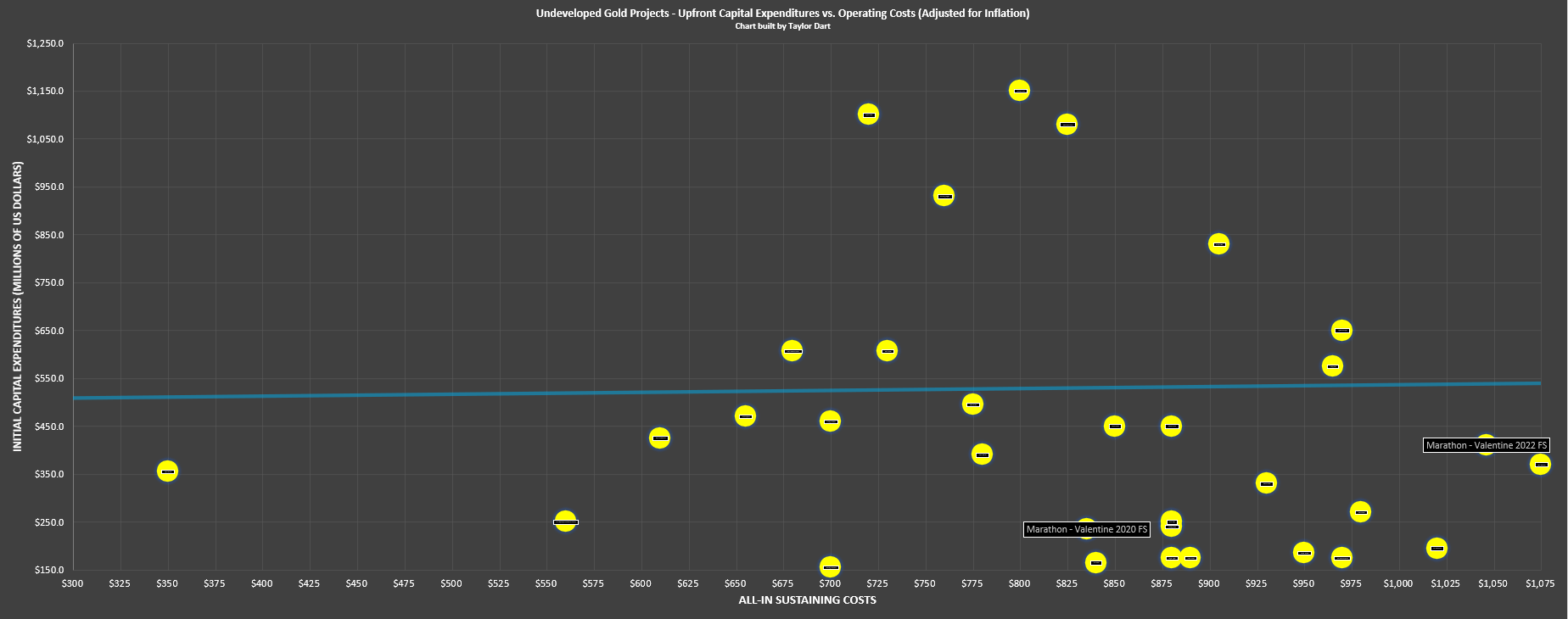

Looking at the 2020 FS vs. 2022 FS from a visual standpoint, we can see that this high-grade open-pit project has gone from being exceptional and a clear takeover target to more in line with the average sector-wide based on the trendline based on average annual production vs. upfront costs to get the project into production. Meanwhile, the project is no longer as attractive from an upfront capex vs. operating cost standpoint (second chart below). In fact, Valentine is now one of the higher-cost future mines among undeveloped projects I track with others also adjusted for inflation. This is disappointing and could make Marathon less of a takeover target, given that I expect intermediates and majors to focus on projects that can drive meaningful margin expansion (sub $900/oz AISC ideally).

Undeveloped Gold Projects - Average Annual Gold Production. vs Initial Capex (Company Filings, Author's Chart)

{kind=link}

Estimated Upfront Capex + Operating Costs (Inflation Adjusted) (Company Filings, Author's Chart & Estimates)

{kind=link}

That said, Valentine is still a very solid project; it's a much more conservative project with current pricing and higher strip assumptions, and procurement has already begun. Plus, grade control drilling is going well, suggesting that we could see some 'bonus' ounces in the mine plan, which never hurts. Finally, this project is permitted (though the Berry deposit has ~30 months to receive permits to move into the mine plan), and Valentine is set to see the first ore to the mill within 24 months.

Valentine Project Land Package & Geology (Company Filings)

{kind=link}

So, while the updated economics certainly isn't anywhere near what I expected pre-inflationary-pressures, a ~22% IRR at $1,700/oz gold is still very respectable, and this is better than many other projects globally that still have a year or two of permitting ahead and must be fully-financed. Additionally, this mine plan contains gold from just three deposits within its large land package, and given the team's drilling success to date; I wouldn't rule out another major pit being discovered that extend the mine life and slot in ahead of the transition to lower-grade feed from stockpiles later in the mine life (2036 and later), a potential boost to NAV. Let's dig into the valuation and see if the stock is worth buying after its violent decline:

Valuation

Based on ~493 million fully diluted shares and a share price of US$0.86, Marathon Gold trades at a market cap of ~$424 million, which is only a slightly lower market cap vs. where it traded a little over a year ago with ~260 million shares and a share price of US$1.90. While this might appear to be a dirt-cheap valuation for a company with an After-Tax NPV (5%) north of $650 million (previous study), it's a much less attractive proposition for an estimated NPV (5%) of $510 million today ($1,725/oz gold price).

Marathon - Fully Diluted Shares (Company Filings)

{kind=link}

The good news is that at least investors can rely on these figures as they appear much more conservative. If inflation moderates, Marathon could potentially deliver slightly under its updated capex estimate of ~$411 million.

Using what I believe to be a fair multiple of 0.90x P/NAV for a fully-funded Tier-1 jurisdiction developer in the construction stage with a project that should boast industry-leading margins (~$1,050/oz AISC), I see a fair value for Marathon of ~$459 million. Adding a combined $130 million for resource upside and potential proceeds from warrant exercises translates to a fair value of $589 million. After dividing this figure by 493 million fully diluted shares, Marathon's updated fair value comes in at US$1.19, translating to a 38% upside from current levels.

While this represents a decent upside from current levels, I believe investors should require a significant discount to fair value to justify buying non-cash-flowing developers vs. producers, especially in a risk-off period for the overall market. In fact, I prefer a minimum 45% discount to fair value for developers. Using an updated fair value of US$1.19 would result in a low-risk buy zone of US$0.66 or lower. Obviously, this doesn't mean that Marathon must decline to US$0.66 or that it can't head higher, and a rising gold price will lift all boats. Still, with cash-flowing producers trading at similar valuations, I don't see any need to step out on the risk curve unnecessarily. One example is Argonaut at a lower fully-diluted market cap with multiple mines, and it's within six months of its first gold pour at its fourth mine.

Summary

Marathon Gold was previously one of my favorite ideas in the sector, which was certainly justified given that it had a very robust project in a Tier-1 jurisdiction with very modest upfront capex. This hasn't changed today, and this is still an excellent project. Still, due to things outside of the company's control and the company's decision not to reduce the potential impacts of those adverse developments (not doing a more significant equity raise for hard dollars above US$2.00), the share structure is very different today. The result is that the company has a similar market cap to what it did at US$1.70 despite trading at a much lower share price.

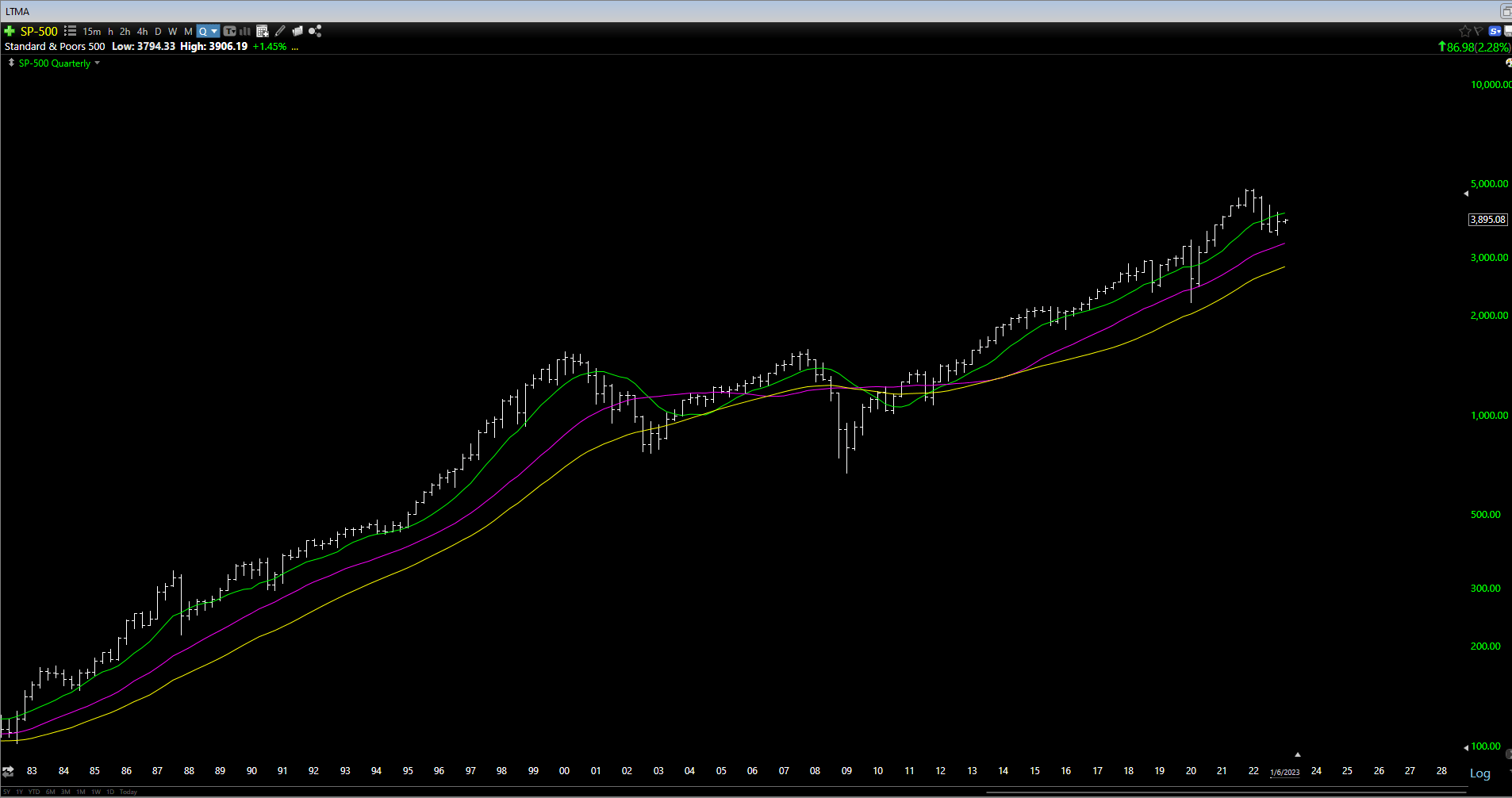

With all of the air out of the stock and sentiment remaining negative following the less robust economics in the 2022 FS, one could argue that the stock is a contrarian opportunity and a cheap way to get exposure to the gold price. While I agree with the contrarian point, I don't see an extreme valuation disconnect, and that should be a major consideration when trying to be a contrarian and buying the dip. For this reason, I remain focused elsewhere in the sector, given that I want significantly more upside to justify owning pre-cash-flow. This is especially true when the S&P 500 ( SPY ) closes below its key moving average (green line), which has often led to negative surprises in the past from a 1-year forward drawdown standpoint.

S&P-500 Quarterly Chart (TC2000.com)

{kind=link}

To summarize, while I still like the Valentine Project, I don't love the valuation, and I would need a sharp pullback in the stock to become interested in going long the stock, especially from a relative valuation standpoint when 300,000+ ounce producers like Argonaut trade at cheaper valuations (~$360 million vs. ~$420 million).

For further details see:

Marathon Gold: Patience Required