WDC - Marvell Technology: Upgrade To Buy Post-Haircut

2023-03-28 14:46:17 ET

Summary

- We’re upgrading Marvell Technology to a buy after the stock dropped materially, reflecting our investment thesis of customers’ inventory correction post-industry-wide double-ordering, especially in the data center market.

- We now see a limited downside risk for Marvell Technology stock in spite of the weaker macro environment.

- Still, we see a mixed demand in its data center, enterprise networking, and carrier infrastructure businesses.

- However, we believe the company's financial performance can improve toward 2H23 and into 2024 as enterprise spending recovers.

- We recommend investors look for potential entry points in Marvell Technology, Inc. stock.

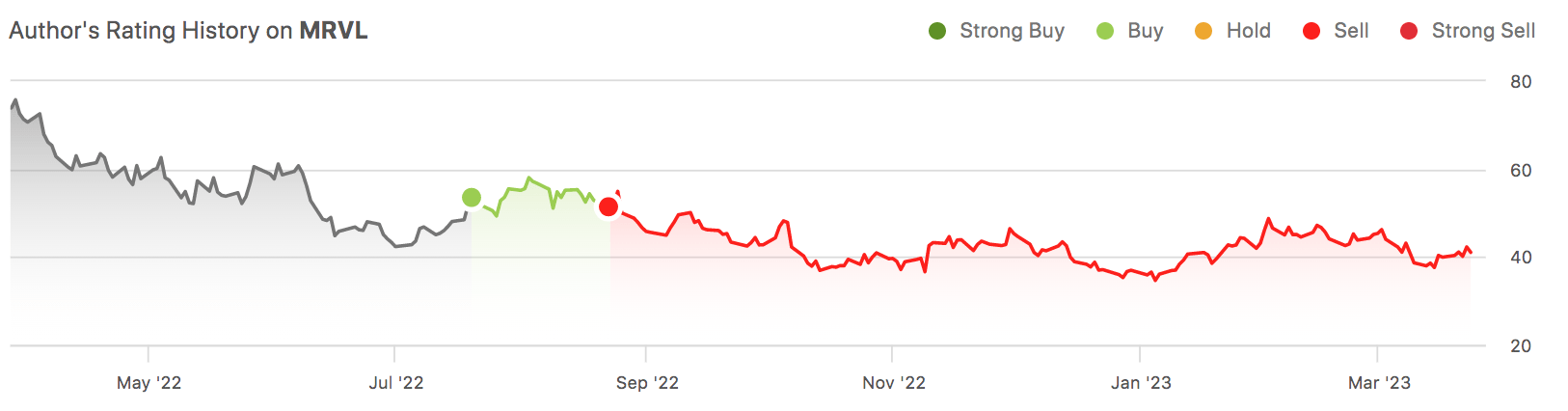

Marvell Technology, Inc. ( MRVL ) stock is down nearly 21% since our sell-rating in late August - we believe the stock has dropped materially, factoring in our forecast of customers' inventory correction and double-ordering. Now, we're upgrading Marvell Technology stock to a buy.

Our bullish sentiment is driven by our belief that Marvell has limited downside risk, despite the weaker macroeconomic environment. We believe the inventory correction cycle is nearing its end in the first half of the year. Hence, we expect MRVL's financial performance to improve toward 2024. We recommend investors begin looking for entry points into the stock at current levels, as we see better times ahead for MRVL.

The following graph outlines our rating history on MRVL.

{kind=link}

Bullish post-industry-wide inventory correction

Our previous note on Marvell Technology, Inc. pitched a sell rating based on our belief that the company would experience supply chain issues and demand normalization in its data center, enterprise networking, and consumer-related businesses. Now, we expect the stock has priced in the near-term headwinds we foresaw and is better positioned to outperform toward the end of the year.

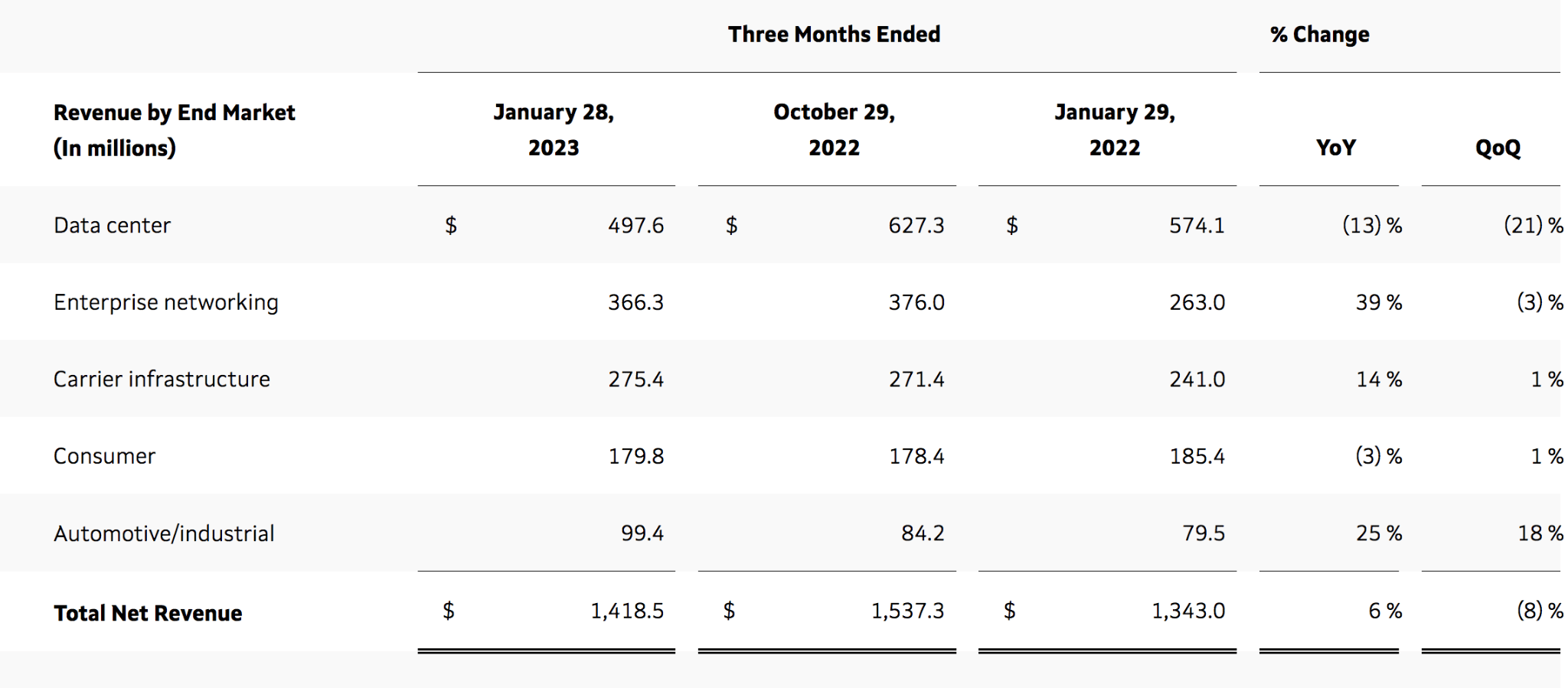

We saw MRVL go through somewhat of a rite of passage in the semi-space at the moment: a pullback due to supply chain issues and inventory correction cycles, similar to Nvidia Corporation (NVDA), Western Digital Corporation (WDC), and Micron Technology, Inc. (MU). MRVL's 4Q23 earning results clearly reflect our forecast of a stock pullback; the company reported EPS of $0.46, missing slightly by $0.01, and reported revenue of $1.42B, up 6% Y/Y. MRVL saw weaker demand through its 4Q23 quarter due to customers' inventory correction cycles; data center-related sales dropped 21% sequentially and 13% Y/Y. We also saw weaker networking demand, with enterprise sales declining 3% sequentially due to orders normalizing as supply issues fade.

The company's guidance also affirms our belief that management is trying to de-risk its 1Q24 from the harsh macro environment. MRVL's guidance is trailing consensus estimates; sales are expected to drop 8% sequentially to $1.30B versus consensus of $1.38B. The following table outlines MRVL's 4Q23 earning results.

{kind=link}

We believe the inventory correction cycles are nearing their end and expect Marvell Technology, Inc. to be better positioned to improve its financial performance toward the end of the year. We believe MRVL is shipping below demand in data center markets and expect HDD industry dynamics to improve towards the end of the year, creating an upward trend for FY2024. The stock is down nearly 45% from its 52-week-high of $76.59- we recommend investors take advantage of the pullback and begin looking for entry points during 1H23.

Exposure to high-growth runways

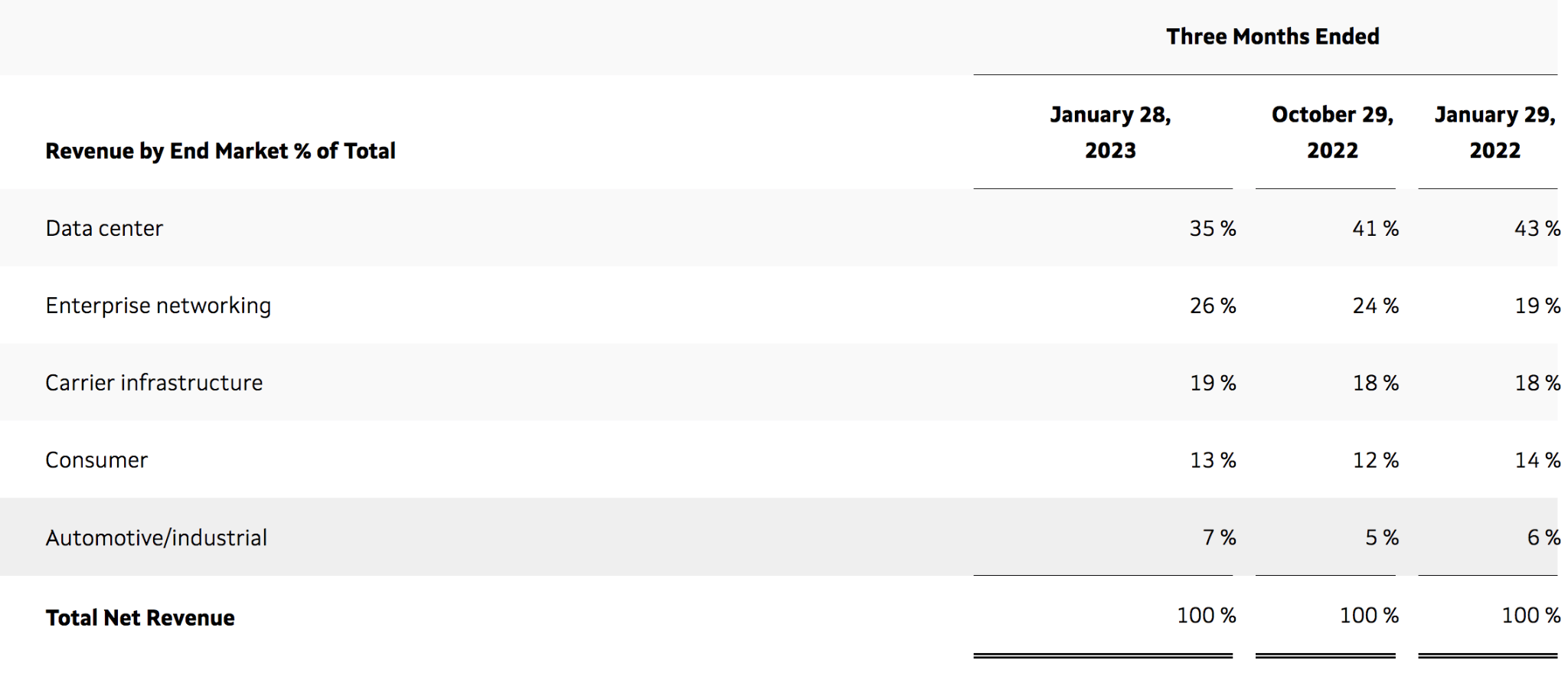

We expect MRVL's financial performance to recover more meaningfully towards the end of the year due to its exposure to high-growth areas: data center and enterprise networking. The former, data centers end-markets, make 35% of MRVL's revenue, while the latter, enterprise networking, accounts for 26%. The following graph outlines MRVL's revenue by end market.

{kind=link}

We expect the demand slowdown in data center segments to be temporary and the result of a demand slowdown in cloud spending due to tightening IT budgets amid market uncertainty. We have seen the demand slowdown in data center end markets impact NVDA and Intel Corporation (INTC), among other semis, but we're more optimistic that the worst of the weaker demand is in the rearview mirror.

We expect the HDD industry supply-demand dynamics to improve toward the end of CY2023. We recently upgraded storage company Seagate ( STX ) to buy based on our belief that STX would benefit from improved ASP and cloud customer demand for higher capacity HDDs. We expect MRVL to benefit from demand recovery in data center storage. The data center market size was $263.3B in 2022 and is expected to expand at a CAGR of 10.9% between 2022-2030. We expect MRVL to experience demand tailwinds in the data center storage and networking infrastructure as enterprise IT spending picks up towards the end of CY2023.

We attribute Marvell Technology, Inc. stock's 45% pullback over the past year and mixed earning results to the weaker spending environment weighing down HDD storage demand related to data centers and enterprise IT spending. We continue to expect a mixed demand environment for the company in the first half of the year but believe the company's outlook has been de-risked. We believe long-term investors buying Marvell Technology, Inc. stock at current levels will be well-reward in the mid-to-long term.

Valuation

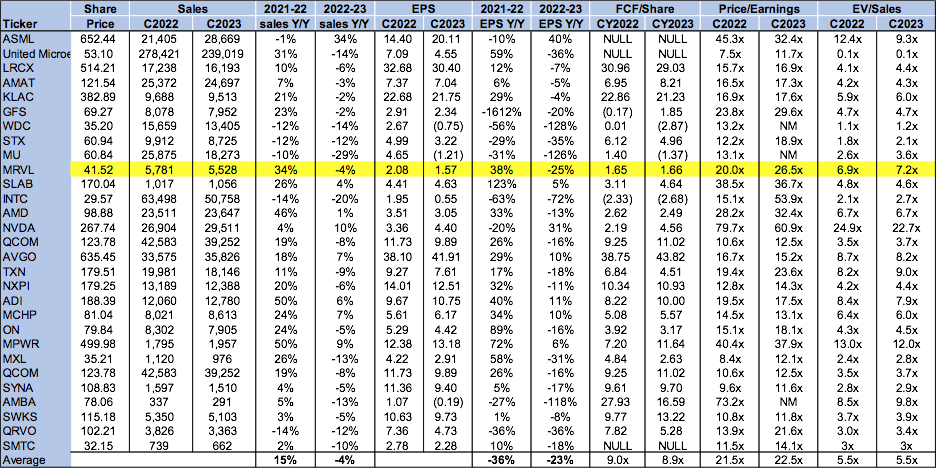

Marvell Technology, Inc. is not relatively cheap. On a P/E basis, the stock is trading at 26.5x C2023 EPS $1.57 compared to the peer group average of 22.5x. The stock is trading at 7.2x EV/C2023 sales versus the peer group average of 5.5x. We believe MRVL is a growth stock and recommend investors looking for semi-growth stocks add MRVL to their portfolio.

The following graph outlines MRVL's valuation compared to the peer group.

{kind=link}

Word on Wall Street

Wall Street shares our bullish sentiment on Marvell Technology, Inc. stock. Of the 30 analysts covering the stock, 27 are buy-rated, and the remaining are hold-rated. The stock is currently priced at $42 per share. The median sell-side price target is $54, while the mean is $57, with a potential 30-38% upside.

The following graphs outline the company's sell-side ratings and price targets.

Tech Stock Pros

What to do with the stock

We're upgrading Marvell Technology, Inc. to a buy. We expect customers' inventory correction cycles and double-ordering impact will wash out towards 2H23. The stock price remains volatile in the near term, and we see a mixed demand environment in the first half of FY2024; still, we believe Marvell Technology, Inc. is better positioned to improve its financial performance going forward and see favorable entry points for long-term investors at current levels.

For further details see:

Marvell Technology: Upgrade To Buy Post-Haircut