CA - Massif Capital Fourth Quarter 2022 Letter To Investors

Summary

- Massif Capital employs a long/short equity strategy focused on global opportunities in listed real assets, principally mining, energy, and infrastructure.

- Although the Massif Capital Real Assets Strategy delivered strong relative performance in 2022, the strategy posted a negative absolute return for both the calendar year and the fourth quarter.

- In our 4Q 2022 investor letter, we review what worked, what didn’t work, and how we’ve responded.

Dear Friends and Investors,

The Massif Capital Real Assets strategy returned -1.14% net of fees in the fourth quarter of 2022. Year-to-date, the strategy returned -5.8% net of fees.

It was a challenging year, and although we did well vs. most comparables on a relative basis, we still finished the year down on an absolute basis — a loss made worse by the erosion of our investment partners' purchasing power due to inflation.

Exceptional fundamental equity managers are wrong 40% to 50% of the time, so it matters enormously how they react to those periods. We like to use the period of underperformance to upgrade our portfolio, reassess assumptions, jettison some positions, and double down on others. Any investor paying for active management should expect this at a minimum. They should also expect their managers to provide insight and clarity into that process and its results. This letter is our attempt at such a thoughtful portfolio review.

ATTRIBUTION

Coming into the fourth quarter, the year-to-date performance generated by our short book was a modest 3.51% vs. a -7.23% drawdown in the long book. During the fourth quarter, we generated a 6.55% return from the long book, which was offset by our worst-ever quarter in the short book, which drew down 7.49%. This drawdown is particularly disappointing from a psychological perspective, as before the fourth quarter, we had managed to generate a roughly 1.13% annualized return from the short book since inception. This is an admittedly small annualized return but a minor win that we took pride in due to the difficulty of shorting stocks over the last few years. Since its inception, the short book is now flat.

The disappointing performance of the short book during the quarter was primarily driven by two poorly timed shorts of U.S. industrials. These two shorts outperformed their industry by roughly 16% during the quarter. We remain skeptical of both firms and have sustained our short positions. Together, these two shorts accounted for approximately 32% of the drawdown in the short book over the period.

Long book returns during the quarter were driven by exposure to industrials, materials, and utilities, all of which rebounded nicely to end the year.

Given some of the drawdowns we experienced in individual positions, combined with the portfolio's relative concentration, we view our portfolio construction and management as essential contributors to our strong relative performance. Our portfolio-level decision in March/April to trim and exit some winners in the long book and sit on more cash for the year than usual helped shield investment partners from some of the worst of the market's fall in 2022.

PORTFOLIO REVIEW

Trading in the fourth quarter was quiet. We exited one position on the long side and one position on the short side. We added one new position to the long book and averaged down into a few of our existing positions.

Investors in the fund will have received a December-end portfolio update that included a discussion of one of our new long-positions. At this time, we continue to build that position and so will avoid discussing it in this letter.

POSITION EXITS

Cornerstone Resources ( CGP:CA )

We entered Cornerstone Resources in January 2020. The firm was an underfollowed holding company of mineral properties in South America. Our interest in the company was driven by its ownership stake in SolGold ( SOLG:CA ), a London-listed copper and gold developer focused on Ecuador, and the firm's ownership percentage of the land package on which SolGold's crown jewel asset, Cascabel, is located. We owned the stock with an average price of CAD 4.5 and sold out at CAD 3.2 for a loss of 28%.

The investment goal was to benefit from an expected sale of the company, with the value derived from CGP's stake in the Cascabel asset. We expected that the sale would take place within two years. On October 7, 2022, the firm announced it was merging with SolGold. Our timeline proved roughly correct, but we lost money.

Our first misstep was the timing of the purchase. We started accumulating shares in January 2020, expecting SolGold to release an updated technical report on the asset sometime during the first quarter. We expected that the asset would improve with the release of this technical report. Rather than release new technical information, the firm reconfirmed the existing technical report and then delayed the release of a pre-feasibility study that had already been delayed once. As SolGold and Cascabel were the assets on which CGP traded, it fell on this news.

The delays should have been a red flag, and we should have exited, but at the same time, Nick Mather, the CEO of SolGold, stepped down. Nick had been forward-looking in building SolGold, having ventured into Ecuador and staked out large land packages that were highly prospective long before Ecuador became a hot spot for exploration. We are unaware of any shareholders who liked him. Liking management is not necessary as long as they are competent. Still, Nick was sufficiently disliked (in part because of his lack of a particular type of competence) that 44% of shareholders voted against him at the December 2020 AGM.

Nick was hell-bent on building the Cascabel mine. We viewed this as a problem. The deposit is fantastic, but only if you want to build a large, deep block cave mine. Block cave mining is a very complex method of monetizing an asset. It has a substantial upfront cost and requires tremendous expertise, which SolGold did not have. We viewed his departure as a positive, opening the way for the asset to be sold alongside Cornerstone's stake in both the deposit and the SolGold. Within that context, a delay in the PFS release, giving the new management team time to reassess options, was not an obvious red flag.

The new management team that was put in place was headed by Darryl Cuzzubbo, the past president of Olympic Dam and veteran of 24 years at BHP. This seemed an excellent fit for an eventual sale of the asset to BHP, already an owner of 13% of SolGold. It never came to pass though, and Cuzzubbo was shown the exit in November of 2022. Meanwhile, as the SolGold soap opera played out on the London Stock Exchange, Cornerstone was either range-bound or slowly bleeding, and copper prices were strong. Cornerstone management, late in 2022, got an opportunity to exit the asset on decent terms, and given the drama at SolGold, we can hardly fault them for that. They made a decent profit for the company (and they were all large owners of the company), even if it was not necessarily a good return for Massif Capital. In the end, the Cornerstone management team sold their stake in SolGold and the Cascabala asset for $0.04 per pound of copper in the ground vs. the $0.06 to $0.07 per pound we expected as a result of our review of 21 precedent transactions dating back to 2010.

We were not sure we would have made any different decisions based on our information. Our expectation that Cornerstone was a seller and that SolGold would eventually need/ want to consolidate the asset was correct. Our timeline was accurate, and our read on management incentives was roughly correct. Still, our read on the magnitude of return needed to justify a sale in management's eyes was off by ~50%. We played our hand well, but we should have been playing the management team's hand when we thought through the prices at which the transaction could be acceptably completed in the context of their incentives. If we had done that, we might have been more cautious with our entry point.

Ormat Technologies ( ORA )

We shorted Ormat Technologies last year as the firm appeared to be an unprofitable geothermal-focused independent energy producer borrowing money to grow an even less-profitable U.S. renewables energy business. Along with eroding the company's margins, we expected numerous executional challenges in the build-out of Ormat's new U.S. renewable business. We got impatient as it increased from our short price of roughly $75 to $100, and we closed out the position. At the time, we noted the following:

"Reviewed earnings [3rd Qtr 2022] and found that although execution had struggled, the impact was minimal, the future impact of the IRA [Inflation Reduction Act] on the firm's independent power production is uncertain (although almost assuredly positive), as such the business appears likely to maintain, at least for some period, its high earnings margins relative to independent power producing peers. We cannot find a reason to question the high margins' near-term sustainability, but long-term sustainability should be in question. Nevertheless, we do not see a catalyst in the future to prompt a repricing or reevaluation of the multiple being placed on unsustainably high earnings or a catalyst that will send the high margins lower in short order, despite the fact the stock is clearly overvalued on fundamental earnings and cash flow basis. Absent a catalyst, it seemed prudent to exit the position."

Given the weakness of our initial catalyst, a rather vague, non-specific idea that the firm would struggle to execute its build-out of a U.S. renewable business and struggle in a sufficiently public way that management could not paper over those struggles with a positive outlook, this should probably be summed up as a valuation short. The longer term issue of margin dilution via the introduction of a new lower-margin business that would eventually be sufficiently sized to drive the firm's margins is still a reality, but the timeline associated with it is somewhat difficult to judge.

As such, we probably should have never shorted Ormat in the first place, as it lacked a material catalyst that would result in a long-term fundamental trend getting incorporated into the immediate narrative surrounding the company. Shorting on pure valuation is challenging and rarely works in a way that allows the short seller to hold the position with conviction through the realization of the return. Many readers will be familiar with the old Wall Street adage that the market can stay irrational far longer than you can remain solvent; this adage seems to encapsulate the challenge of shorting based on valuation. Ormat can stay afloat a while longer and probably far longer than we are happy sitting on a roughly 33% draw down on a 3% position, but we will keep an eye on it; one never knows when a useful catalyst may appear.

COMMENTARY ON EXISTING POSITIONS

Short Positions

The rate of interest over the last ten years has meant that shorting stocks costs money. At this time, and for most of last year, that has changed. Our blended cost of borrowing on stocks in the short book is 0.86% per year. The cash we receive in exchange for shorting is then reinvested into short-term T-bills with a blended annualized yield of 4.42%, netting to fund 3.56% on cash generated from short selling. This is not new, not unique, and not something that is foreign to most short sellers. It is just an opportunity that has not been available in the past ten years due to the interest rate regime.

U.S. Industrials

We are currently short five U.S. industrial companies, representing roughly 20% of total exposure. All the positions were put on in either the second or third quarter of 2022. We are presently underwater on three of the five and slightly positive on two. As a group, these positions are currently producing a roughly 3.3% drag on the portfolio.

The poor performance of these positions has been driven by the somewhat flabbergasting outperformance of the equity of the U.S. industrial sector in the fourth quarter of 2022. Despite growing evidence that the economy is slowing, the S&P 500 Industrials subsector outperformed the main index by 10% (up 19% vs. 9%). We can only surmise that the narrative driving this positive trend is general optimism around China re-opening and the potential for a soft landing in the U.S. (a narrative that has continued to build in the new year), but we believe this narrative falls short of explaining the magnitude of outperformance.

The IRA and CHIPS Act will provide secular tailwinds to CAPEX during the next decade by incentivizing spending on reshoring supply chains and the transition to green energy, but these are long-term tailwinds for a sector of the economy that appears to face significant near-term risk. According to data reported by Bloomberg, the consensus aggregate 2023 earnings growth outlook for U.S. Industrials (represented by the S&P 500 Industrial subsector) is 12.1%.

With industrial operating margins currently sitting at 11.3% (near the all-time high of 13.1% set in 2015) and well off the recession average of 8.6% (excluding the COVID recession when operating margins fell to 5.6%) and the economy that can at best be described as soft, 12% seems overly optimistic. Especially given the much more muted 2.5% to 4% consensus EPS growth outlook for the S&P 500 Index.

Clean Energy Shorts

We are currently short three clean energy companies. Two are equipment manufacturers, and one operates in the residential solar market. Together, they have a collective drag on the portfolio of roughly 3.1% as of this letter's writing. We put all three positions on during the March/April period of 2022, and two positions ended the year with double-digit gains.

The two that closed the year with double-digit gains have 14 years of operations as public companies. During this time, they have lost $2.3 billion, accumulated $1.3 billion in debt, and had cash losses on operations totaling $1.2 billion. If we add in our third clean energy short, which was down last year, resulting in a minimal gain for the portfolio, these numbers get more significant: the debt grows to $7.9 billion on $2.6 billion in negative cash flow from operations.

These companies are desperate to be seen as innovators, tapping fast-growing markets that justify the significant investment, hence the losses. Unfortunately, across 23 years of collective public company operations, they have produced only two measly years of positive return on invested capital. They have all grown their top line, yet all that topline growth appears value destructive. We would be remiss if we did not admit that they have made some progress; after all, losing $68 million from continuing operations on $54 million in revenue is technically worse than losing $843 million on $2.1 billion in revenue. Still, we remain skeptical that such improvement represents investable progress.

Fleas abound on these three shorts, but sentiment has turned against us, especially following the Inflation Reduction Act (IRA) being signed into law. All of these businesses look shaky to us. One produces an obsolete product, another a product that fails to achieve what the manufacturer says it will, and the third has a questionable business model and is being given credit in the market for future value creation that is speculative at best.

For the moment, we remain short these companies and are sticking with those shorts.

When viewed through the factor lens, all three companies share many factor exposures. Market Sensitivity, Volatility, Medium Term Momentum, and Leverage are just a few factors that explain a significant percentage of the stock movement. The importance of these factors to the underlying stock returns is a trait all three share with the ARKK ETF; high volatility but significant collapse potential. At the same time, if the market starts to roll, it likely means we are better off exiting these positions.

Polysilicon Industry Short

We are short a diversified polysilicon producer. The position was added to the portfolio during the third quarter and is currently flat. This will be an interesting position to watch over the next two quarters. A key catalyst for the realization of value on this short is margin erosion driven by a collapse in polysilicon prices. This short is a classic example of the market linearly extrapolating a trend long into the future and bidding up company stock.

Between its IPO and the end of 2020, the firm's long-term quarterly operating margin range is roughly 1% to 10%, with a few negative years. Since 2020, quarterly operating margins have been in the range of 15% to 25%. This margin trend corresponds with a shift from a multi-quarter downward trend in Polysilicon prices to a roughly two-year period of high polysilicon prices. That trend has reversed, with the average polysilicon price collapsing 30.8% in December and a further 31% thus far in January 2023.

The last time Polysilicon prices were at the current level was in the fourth quarter of 2020, when our short had operating margins of 2.83%. We expect the stock to fall precipitously if margin compression is that severe. This short is not without challenges in the upcoming year. First, we must contend with the positive sentiment and narrative around the future of solar. This is a problematic narrative to fight against, as it holds considerable future option value. Second, there remains the possibility that ongoing government subsidies related to the financing and build-out of renewables grow the top line sufficiently that investors ignore margin compression and the bottom line.

The combination of RePowerEurope, the U.S. IRA, and whatever Chinese stimulus comes out of the 2025-2030 five-year plan for power industry development could significantly boost the industry—perhaps reversing the polysilicon price trend, even with significant incremental supply hitting the market in 2023. We suspect that the timelines associated with the distribution of that capital (in the case of, for example, the IRA, money will be spread out over the next ten years) will create a sufficiently large window in which there is a time mismatch between the solar industries' ability to consume new excess polysilicon supply and the impact of government-driven CAPEX, allowing for a period of weak polysilicon pricing and weak margins at our short. It is unclear how long that window will last, but given the exponential rate of growth in solar deployment, it will likely be tight, probably no longer than two or so years at a maximum.

LONG POSITIONS

Siemens Energy ( SMEGF )

The world has been a tad short of energy as of late, which creates some urgency to speed up investments in renewables, grid systems, gas turbine retrofits, and energy-efficiency solutions for process industries. Siemens Energy should be one of the few beneficiaries of these needs in the medium term, resulting in a strong commercial operating environment for the firm, regardless of the macroeconomic backdrop. We continue to see significant value in the shares, with an upside of at least 35%. FCF volatility and the prospect of a €1bn equity raise to finance the SGRE transaction will probably continue to weigh on the share price in the near term, or at least until the completion of the deal, but once completed, the transaction will simplify ENR's structure and governance, removing part of the stock's overhang.

With the removal of the overhang, ENR will become the best investment vehicle for exposure to offshore wind market growth. Management will still need to address the firm's onshore wind segment, but there is positive momentum. We are optimistic that the merger will help stabilize the SGRE business and deliver on its full potential. It will benefit from ENR's closer involvement in day-to-day operations and turnaround expertise. The integration of SGRE will also make the group a unique one-stop shop, supporting its customers in the energy transition.

Although the merger is a potential catalyst, we believe value realization is more likely to occur after the union and once the market has seen progress. This means we don't expect much from ENR this year, but it could surprise us.

Pre-Production Miners

We currently have roughly 20% of the portfolio invested in four pre-production junior miners: Adriatic Metals ( ADMLF ), Centaurus Metals ( CTTZF ), Ionic Rare Earths Metals ( IXRRF ), and Lithium Americas ( LAC ). All four made good progress in advancing their projects in 2022 and have attractive catalysts to watch out for in 2023.

Adriatic Metals is the mining firm in our portfolio closest to an exit due to the price approaching our valuation estimate. We invested in the company in April 2020 and built our 3% position over the remainder of 2020 at an average price of AUD 1.4. The stock is currently trading at AUD 3.2, a 128% return. Our probability-weighted valuation is AUD 3.9. The firm's primary Varas project, a silver-heavy polymetallic asset, will probably go into production during the third quarter of this year. As such, we would expect the final gap between the probability-weighted price target and the current market price to close within the next 12 to 18 months, after which we surmise the firm will trade more like a producer and less like a junior with a near-term catalyst, making it a good time to exit our position.

In the run-up to the mine turning on in the third quarter, we expect a good flow of news to help close that valuation gap. Important upcoming events include the conclusion of construction of both the processing plant and the haul road during the first quarter, as well as the underground development reaching the ore body. Some slippage of these events and their announcement in the second quarter would not be surprising or overly concerning. During the second quarter, the commissioning of the processing plant will start and run through the state of operations in the third quarter.

Although the firm is currently approaching our valuation target, there are two additional paths to further asset growth that are not priced into our valuation and that we need to evaluate before we make an exit decision. The first is the Rupice deposit, another polymetallic silver-focused asset, which is a high probability bet for being a project the firm moves to build in relatively short order after completing Varas (short order in the mining world is years). The second is the Raska Zinc-Silver project, a deposit we expect to see a maiden mineral resource estimate and scoping study for in 2023. Although including one or both of these projects in our valuation is not challenging from a technical valuation standpoint, many more ethereal variables might prompt an exit, regardless of the potential valuation extension these projects provide. Note that we do not say valuation addition but rather valuation extension. The project-like nature of young mining firms often means future projects extend a stable valuation into the future but don't necessarily create additional value.

The first important variable to assess is the management team's ability to grow a mining business. Very few management teams can grow a mining business beyond a single project. The nature of the management of a complex multi-asset corporation is very different from the management of a firm that could be fairly considered more of a project than a business. The other consideration, the more challenging judgment call, is around timelines of project execution, as the wrong sequencing can result in a cash flow profile that does not add value but extends the period of the peak value.

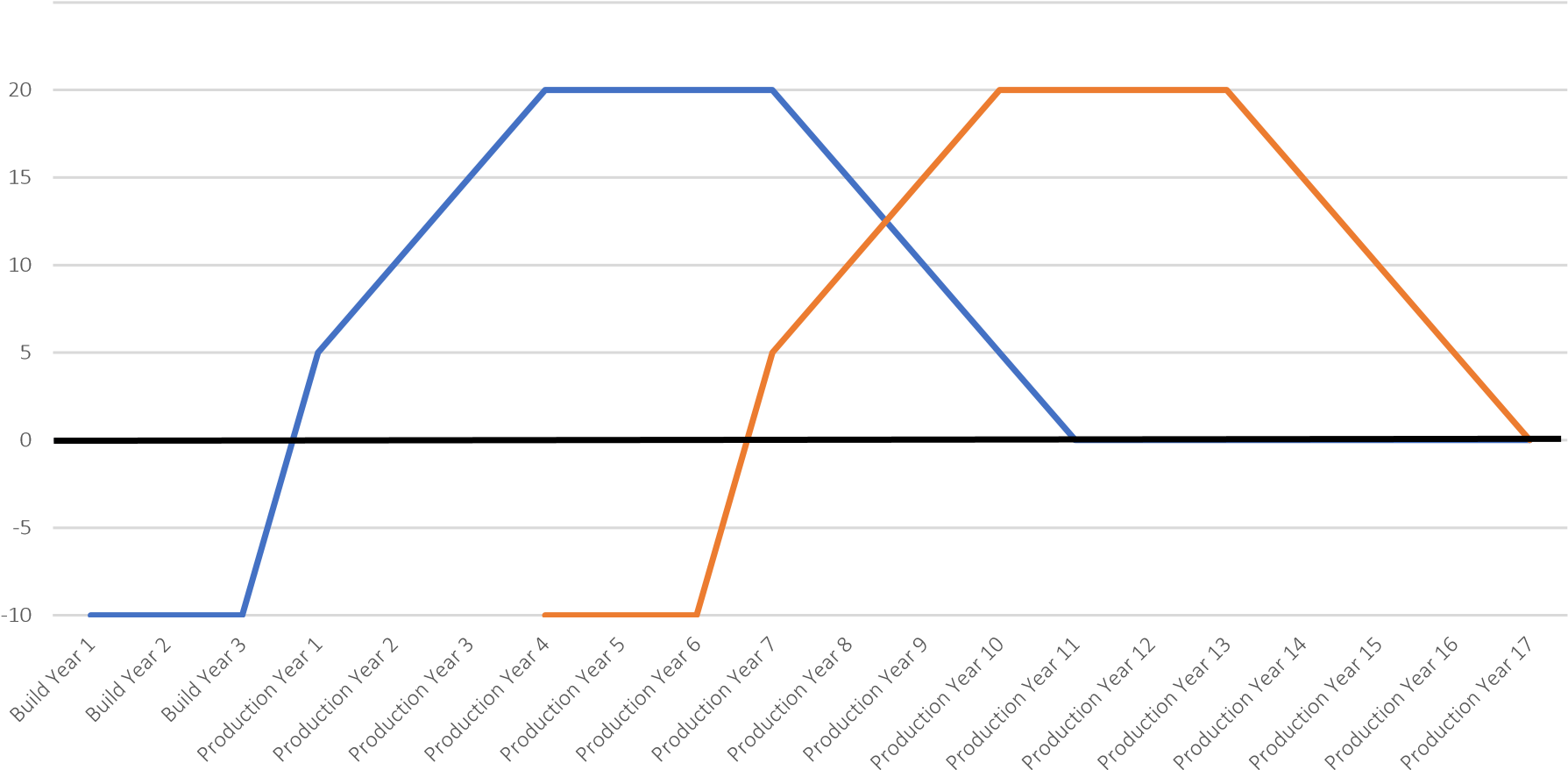

If we envision a multi-asset mining firm as a collection of projects, the highly stylized cash flows of that business on a project level look like the following:

{kind=link}

These two projects are the same: a three-year construction period followed by a 10-year production period with construction on project two starting at year 5 of production for project 1.

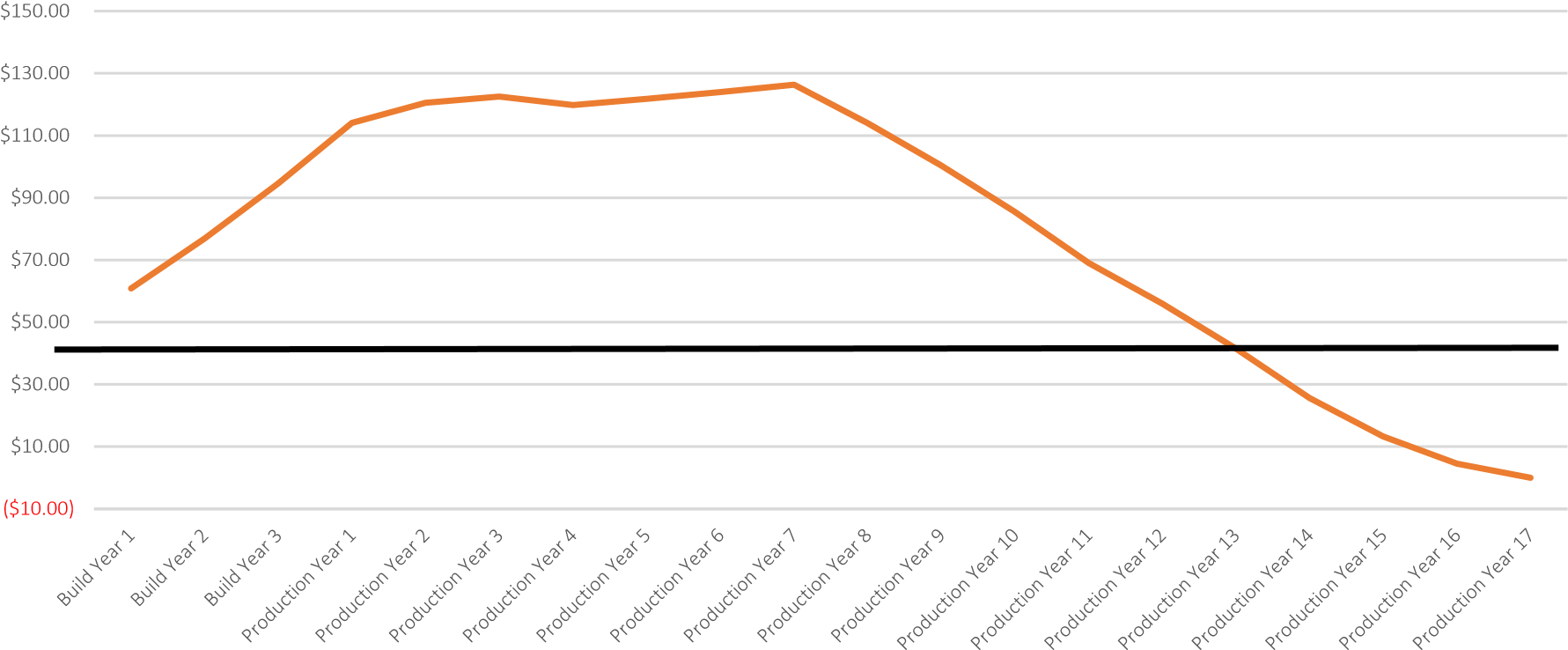

If we assume a 10% discount rate, the forward-looking Net Present Value of those cash flows is as follows:

{kind=link}

In essence, because of time and sequence, the existence of additional in-ground value does not necessarily add much value to the business relative to the initial value creation of the first project. In this case, the peak value occurred in year seven, but the peak is only marginally higher than in the single project peak in year three. The opportunity cost of squeezing out the difference between the year three and seven peaks is likely not worth it. In situations like Adriatic, in holding for the second mine, there is a strong possibility that we are left with an investment that does little more than add volatility to the portfolio's return without adding meaningful value to that return stream.

Turning to our most junior mining firm: Ionic Rare Earth Metals ( IXR ). We initiated our position in IXR in May of 2022. IXR could have an exciting year ahead as it unveils its scoping study for a rare earth refinery in Europe or the U.S. This is a big deal geopolitically because when IXR successfully builds its heavy rare earth refinery, it will be the only heavy rare earth-focused refinery outside of China and Vietnam. When IXR turns its mine on, it will also be the sole operator of a primary heavy rare earth mine outside China.

This is important because when people talk about shortages of rare earth metals, they are talking about a lack of processing capabilities in the non-Chinese world and heavy rare earth metals. Competitors, like mining neophyte Chamath Palihapitiya's MP Materials ( MP ), not only mine the much more widely available lite rare earth materials but also ship their ore to China for processing, even though they are based in California. MP Materials is looking to build a processing plant. Still, given the more pressing need for heavy rare earth metals that don't touch China, their lack of a heavy rare earth metals deposit means they fail to address the core challenge, regardless of their marketing. On the other hand, Ionic possesses the only known primary heavy rare earth deposit outside of Southern China/Vietnam. Progress with its Uganda Makuutu Ionic-Clay Heavy Rare Earth Deposit is also expected, as the firm continues to target its first production in 2024.

Our final pre-production mining firm in the portfolio is Lithium America. We have been invested in Lithium America since January 2020, with an average price of roughly $2.8 per share. Interestingly enough, as a result of successfully trading options around our core position, we have generated options premium per share of $2.03, so our effective cost of ownership is $0.77. The shares are currently trading for $20.72, an unrealized return of 2,590%, although it is worth noting that the stock got as high as $38.94 per share, a 4,957% return.

In retrospect, we probably misplayed this. When the stock peaked at $38 per share in February/March 2022, we believed the firm, in the fullness of time, could be worth as much as $46 per share, an additional 21% return. At the same time, we felt that the stock had run well ahead of itself; after all, we believed it could be worth $46 per share with two mines operating, not when it was pre-production at two mines.

The stock plunged, and we may have to wait several years before it returns to those levels. Hindsight is always 20/20, but with time, it seems apparent that we should have approached the position's price action from a different angle. We knew it was overvalued; we knew that the first production from the firm's Cauchari asset would not be until the first half of 2023 and that Thacker Pass, the firm's second asset, would not turn on until several years later. We did not ask the question: What are the odds that a pre-production mining firm bringing on an asset in Argentina with a Chinese partner remains valued at roughly 10x-12x a projected EBIT that is still two years away? That is a question we could have asked at the time with the information we had, and it would probably have caused us to take a different course of action.

At the very least, we could have trimmed with reasonably high confidence that we would be able to re-enter at a later date and lower price. These types of calls remain a struggle for us.

The reality is that managing a position like LAC, which runs up more than 1,000%, is a challenge, regardless of whether you consider yourself an investor or a trader (a difference, in our opinion, of timelines and little else). Positions like this create concentration, diversification, and return harvesting decision challenges. Rules and guidelines for managing a position through its lifecycle are helpful. Still, in the end, many of these decisions have a heavy market-timing element, which makes them judgment calls at best. At the core of the challenge is the math of expected returns in the presence of price movement and risk management.

We have two starting position sizes, 6%, and 3%. For us, the difference between a 6% position size and a 3% position size stems from one of two variables: portfolio concentration and position-level risk. We may like a company and a management team but believe, for example, that a project they are pursuing hinges on a regulator permit that has not yet been secured. In this situation, we may view the future as somewhat binary; the resulting probability-weighted return then looks something like the following:

| PROBABILITY |

| CURRENT PRICE |

| EXPECTED VALUE |

| SCENARIO |

| 50% |

| $1.00 |

| $5.00 |

| Permit Issued |

| 50% |

| $1.00 |

| $0.00 |

| Permit Declined |

| Probability Weighted Expected Value |

| $2.50 |

| Expected Return |

| 250% |

If we have a portfolio of $100, we can either allocate $3 or $6 to this bet (investment, trade, etc., all the same). The expected return makes sense, but the downside is not something we can live with at a 6% allocation. In this example, despite the positive expected return, we may not feel comfortable allocating 6% of our capital to trade with a potential to draw down to zero, but perhaps we are comfortable risking 3% of the portfolio given the risk/reward. We may also allocate 3% instead of 6% because we already have sufficient exposure to ideas that create a similar market exposure in the portfolio.

The thought process behind that situation is very similar. We invest in individual companies for idiosyncratic reasons, but between the time an idiosyncratic variable takes hold of the narrative of a stock, a company might trade with the market, its industry, its peers, or any number of other groupings. With that in mind, we are only willing to allocate so much capital to that industry, group of peers, etc., as they can functionally act like the situation described above for an individual company. We may have three oil companies that we believe have a specific reason for appreciating in the future, but they may all trade with oil prices until the company-level factors take hold of price action.

Put another way; we think about position sizing and portfolio allocation in terms of capital at risk relative to expected return. An issue with a position like LAC is that, given its price movement, we need to figure out a way to maximize our return while managing our capital at risk. Suppose we allocate 6% of a $100 portfolio to Oil Company A with an expected return of 200%. In that case, we implicitly say we are comfortable risking $6 to make $12 (a 200% return on a $1 stock rising to $3). If Oil Company A trades at $1 when we enter the position and then quickly rises to $2, we are now risking $12 to make a 50% return.

That is a much less appealing bet. You can take profit, as we suggested we should have, but then we are functionally decreasing our portfolio concentration in an idea that a) is moving and b) we have high conviction in. Put another way by Brent Donnelly in his excellent book Alpha Trader; this is the same thing as truncating your right tail, which is not ideal. Another idea Brent Donnelly suggests is to run a moving stop loss behind your trade such that you are always running a trade with the same risk/reward tradeoff. In the example above, that would mean putting a stop loss at $1.50, reducing your trade from $2 to make $3 to $0.50 to earn $1.50.

This is an appealing idea but suffers from disconnecting the trade's life in the portfolio from fundamental factors. Inevitably, Oil Company A trades down to $1.25, triggering the stop-loss, before rallying to $3.50. At the same time, it is not completely clear that integrating more systematic guardrails into actively managed portfolios is necessarily a bad thing. The challenge then becomes figuring out when you can ignore the guardrails.

Looking ahead, 2023 should be an exciting year for Lithium America, with the firm turning on Cauchari, a possible split into two publically traded businesses, and legal resolutions on their U.S. asset, Thacker Pass. We are optimistic that splitting the assets up, and thus isolating the U.S.-based assets from the firm's relationship with Chinese lithium giant Gangfeng (JV partner for Cauchari) will result in the U.S.-focused firm eventually earning a premium, as it feeds product into the nascent but rapidly expanding U.S. battery and EV infrastructure.

Producing Miners

Equinox ( EQX ) is a long-term holding we have written about several times. While maintaining our positive outlook, we sold the position in November to harvest tax losses. We have since re-established the position, but it warrants noting, as we had concerns about selling it and missing a possible surprise end-of-year move in the price of gold or a rush into gold miners by investors fearful of any number of things one could be afraid of at the moment.

Before we made the sale, we looked for a way to address the issue. We concluded that an effective way of handling this concern, which boils down to a concern for high volatility within the gold equity space, was buying call options on the GDX, where we found what we considered very cheap optionality. We purchased $35 calls on the GDX maturing in January of 2024, giving us, at the time of purchase, 13 months of control for $1.69 a share.

In essence, we established an options position that mimics the return of a roughly 6% notional position at a cash cost to the portfolio of just 17bps when the GDX is trading above $35 and responds well to volatility below $35 given the sensitivity of longerdated options to volatility. Whenever we have an opportunity to use similar non-recourse leverage, we always attempt to do so. Good returns will accrue from good ideas and figuring out the most effective instrument to express the idea. This is an excellent example of an alternative to straight equity allocation and a more efficient use of capital than if we had allocated 6% of the portfolio to GDX. We got lucky and bottom-ticked the purchase on the GDX 4th quarter local low. The position is up 221% for a modest

0.34bps portfolio-level gain. Given the optionality of controlling the shares, we intend to hold on to the options. We also re-established our Equinox position, only 2.9% off our exit price, and have benefited from a subsequent rally.

Utilities

We currently have roughly 13% of the portfolio allocated to two utilities: AES and Polaris ( PIF ). We invested in AES in December 2020 at an average entry price of $21.3 and invested in PIF in July 2020 at an average entry price of 16.36 CAD. We are currently underwater on PIF and making money in AES. Our near-term outlook for both positions is mixed. AES had a solid year in 2022, up 13%; it has telegraphed growth in earnings and cash flow through 2025 and seems to be hitting its targets. We will have to see what the year holds for utilities and AES, but another year like last year, and the firm will be touching our full value expectations.

PIF is in a very different situation. It is a young company attempting an ambitious buildout. It is leveraging its balance sheet to build productive assets that we, and management, believe will generate rich, stable, long-term cash flows. Unfortunately, PIF is undersized and building out renewable assets in a handful of Latin American countries. Its cost of capital was high before 2022. In the wake of interest rate rises, its significant floating rate debt is concerning. We expect the firm's effective interest paid on the debt in 2022 will be roughly 9.0% to 11.0%. This makes for a tight earnings and cash flow situation. If PIF navigates this challenge, it could have a long growth path ahead of it.

In conversations with management, we have raised the question of why a company building renewable energy assets in developing countries with off-take agreements cannot secure a better cost of capital and, specifically, why they have not pursued green bond financing? They told us that the firm is currently sourcing debt at the project level, partly due to size, and that they have not managed to secure better rates. Management hopes to finalize transactions in progress before attempting a sizeable green bond issuance that allows them to take out all the project financing debt, which, when pooled together, they believe will be of sufficient size to warrant a meaningful bond issuance. We have encouraged management to get on with it, suspecting that even low-rate green bonds will eventually disappear and that a bond issuance of roughly CAD 200 million is more than large enough, but as of yet, management continues to focus elsewhere.

OPPORTUNITIES IN 2023

We have roughly 7% to add to the portfolio's long book by averaging down into a few positions. With all else equal, this leaves room for about six positions at 6% each before we hit our target gross exposure of 150%. We are not looking to add to the long book now if we are not also adding to the short book, and while the lack of a short idea won't stop us from adding a suitable-looking long idea, we are aiming for more balance given the current market environment.

The obvious next question is where we are looking to find opportunities to fill out the portfolio. From our perspective, the big unfilled hole in the portfolio is copper. The macro setup for copper is excellent; there are reasonable long-term demand growth scenarios and a nasty imbalance between the rates of change of demand growth and supply growth. The industry cannot ramp production to meet even the slightest acceleration in demand. This means that not only do new mines — of which there are only a handful of candidates — need to be brought online, but they will come online in an environment we believe will provide them with a tailwind. Furthermore, many of the more impactful assets that could come online over the next decade appear to be priced as if the firms will never monetize their resource, let alone monetize with a tailwind.

Looking further afield, we continue to search for opportunities in oil. It is hard not to have a positive long-term outlook for oil, but that positive long-term outlook must be tempered by the messy near-term economic backdrop and oil price sensitivity to even slight changes in demand. We would also note that a positive outlook for oil need not be one in which oil goes to $140 a barrel; a positive outlook includes a scenario in which oil is range bound between $60 and $80 a barrel. In fact, that might be the goldilocks scenario for oil companies, as it is a high oil price but not high enough to limit economic growth. This scenario would not be particularly great for oil equities, however. The companies would benefit fundamentally, but given that most oil stocks are already priced for oil at roughly $70 a barrel, that range would not necessarily translate into equity gains.

The places we are finding significant discrepancies between price and value within the oil and natural gas universe tend to be heavy on political risk. At first blush, one might say that is great for us, as we consider ourselves experts in dealing with such situations. Unfortunately, that expertise also means we understand that political risk cannot be hedged or diversified away within a portfolio; one either must accept it or not. We have found several exciting situations that fall into this bucket and have started building a position in one. More may follow, but our research continues.

Despite the seeming absence of opportunities in two sectors that usually represent a sizable 12% to 24% of the portfolio, we are finding interesting situations in sectors of the economy that make it into our portfolio less frequently. For example, we are looking at several businesses within the agriculture space that have developed seeds that are both drought resistant and have low fertilizer needs. Given the importance of oil and natural gas to the food industry and the concentration of various fertilizers and fertilizer precursors in less-than-friendly countries, this technological advancement is of interest. It is also of interest from a portfolio construction perspective. Should the companies meet the standard to make it into the portfolio, they may represent a very different type of return stream than most businesses we invest in. Long-term compounding opportunities are in short supply within real assets, but some of the ag-tech companies we are looking at have the potential to compound for many years, as we have seen in the past with companies like Monsanto.

Finally, we continue to believe that Europe, and specifically certain types of energy-focused European industrials, offer great long-term potential. Firms like our current Siemens Energy investment, businesses with interesting engineering and product development capabilities within the energy industry, are of great interest to us.

As always, we appreciate the trust and confidence you have shown in Massif Capital by investing with us. We hope that you and your families stay healthy over the coming months. Should you have any questions or concerns, please do not hesitate to reach out.

Best Regards,

WILL THOMSON, CHIP RUSSELL

DISCLOSURESOpinions expressed herein by Massif Capital, LLC (Massif Capital) are not an investment recommendation and are not meant to be relied upon in investment decisions. Massif Capital’s opinions expressed herein address only select aspects of potential investment in securities of the companies mentioned and cannot be a substitute for comprehensive investment analysis. Any analysis presented herein is limited in scope, based on anincomplete set of information, and has limitations to its accuracy. Massif Capital recommends that potential and existing investors conduct thorough investment research of their own, including a detailed review of the companies’ regulatory filings, public statements, and competitors. Consulting a qualified investment adviser may be prudent. The information upon which this material is based and was obtained from sources believed to be reliable but has not been independently verified. Therefore, Massif Capital cannot guarantee its accuracy. Any opinions or estimates constitute Massif Capital’s best judgment as of the date of publication and are subject to change without notice. Massif Capital explicitly disclaims any liability that may arise fromthe use of this material; reliance upon information in this publication is at the sole discretion of the reader. Furthermore, under no circumstances is this publication an offer to sell or a solicitation to buy securities or services discussed herein. |

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Massif Capital Fourth Quarter 2022 Letter To Investors