XOM - Matador Resources: Near-Term Earnings Growth May Be Fleeting But Still An Attractive Company

2023-05-08 10:04:18 ET

Summary

- Matador Resources is an independent E&P that just increased its size in the Permian Basin through an acquisition.

- The company is also likely to grow its production over the remainder of this year due to this acquisition.

- This production growth may not translate to earnings growth because energy prices may prove to be stubborn.

- The company has a very strong balance sheet, despite the money that it borrowed in order to fund the acquisition.

- The stock appears to be substantially undervalued today.

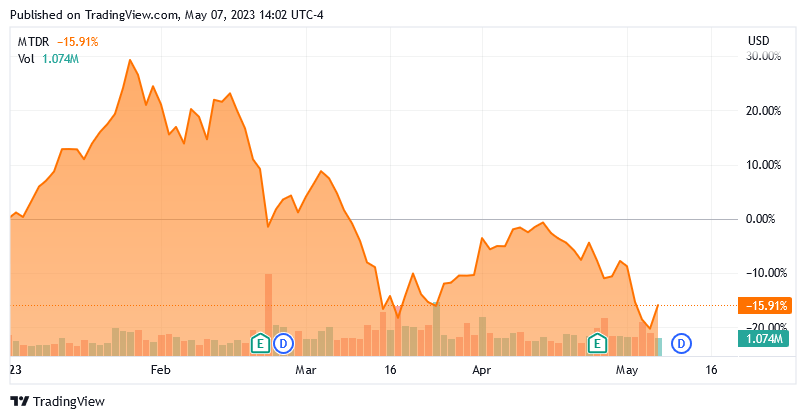

Matador Resources Company ( MTDR ) is an independent exploration and production company that primarily operates in the resource-rich Permian Basin of West Texas. The company’s stock has unfortunately delivered a rather disappointing performance year-to-date, which was likely caused by the decline in energy prices:

{kind=link}

However, there may be some reasons to invest in this company today. In particular, Matador Resources recently reported a strong first quarter that beat the expectations of its analysts, yet the stock appears to be undervalued on a variety of metrics. The company also boasts a reasonably strong balance sheet and a respectable 1.34% yield, although this yield is still lower than many other companies in the sector. While Matador Resources is likely to generate significant production growth this year, it requires high energy prices in order to truly benefit from this. It is uncertain if that will actually occur as some signs point to rising energy prices over the course of this year, but the very real possibility of an economic slowdown in the United States could derail this. I have discussed this company before and overall, the thesis remains intact, although the macroeconomic backdrop has weakened significantly and that appears to be likely to weigh on the company over the coming months.

About Matador Resources Company

As mentioned in the introduction, Matador Resources Company is an independent exploration and production company that operates primarily in the Permian Basin in West Texas. The company controls 150,000 net acres in the Basin, which represents a fairly significant increase since the start of this year:

Matador Resources

The biggest reason for this increase is that Matador Resources acquired Advance Energy for $1.6 billion a few weeks ago. I discussed the implications of this acquisition in my last article on the company. One of the largest of these benefits is that it increased Matador Resources’ proven reserves to 463.1 million barrels of oil equivalent compared to the 356.7 million barrels of oil equivalent that the company had at the end of 2022. This represents a very significant 30% increase, which unfortunately may have been overlooked by investors. As I have pointed out numerous times in the past though, an energy company’s reserves are critically important because the production of crude oil and natural gas is by its nature an extractive process. An energy company literally obtains its products by pulling them out of basins in the ground, which contain a finite quantity of resources. Thus, it is possible that the company will run out of products to sell if it fails to consistently discover new sources of resources to replace those that it removes from the ground. This is by no means guaranteed, which is the purpose of the company’s reserves. Its reserves ultimately dictate how long it can produce without needing to discover or otherwise obtain new sources of hydrocarbons. In the first quarter of 2023, Matador Resources produced an average of 106,654 barrels of oil equivalents per day. At this production rate, the company has sufficient resources to continue to operate for almost twelve years. That is certainly a very respectable reserve life that is easily in line with that of supermajor energy companies like ExxonMobil ( XOM ) or Chevron ( CVX ). It is also comparable to many of the independent shale operators, who tend to have slightly larger reserves relative to production than the supermajors do. This is something that should prove reasonably comforting to the company’s investors.

The acquisition of Advance Energy did more than just boost Matador Resources’ reserves. This is because Advance Energy also had some producing wells that will continue to produce under the new ownership. For this reason, Matador Resources has provided production guidance of 125,500 to 127,500 barrels of oil equivalents per day beginning in the second quarter. That would represent a 17.67% to 19.54% increase over the company’s first quarter levels. This is unfortunately not as good as the 20%+ production increase that I projected in my last article on the company, but Matador Resources’ first quarter production also came in higher than expected. It is still a reasonable amount of production growth, though.

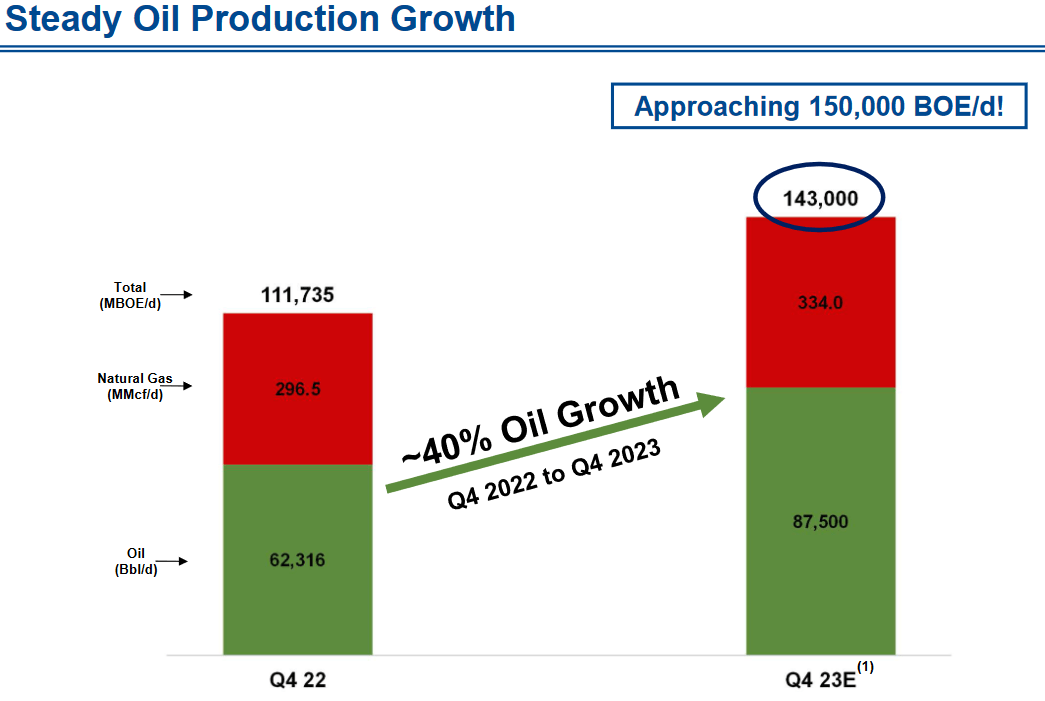

Matador Resources intends to continue this production growth going forward. The company states that it intends to be producing approximately 143,000 barrels of oil equivalent per day by the end of this year:

{kind=link}

On the surface, this would be expected to boost the company’s revenue, EBITDA, and net income. However, that is not necessarily the case with the energy industry. This is because the price of crude oil plays a significant role in the financial performance of these companies, and this is completely out of their control. After all, Matador Resources does not produce nearly enough crude oil to have any impact on the world price considering that the world consumes approximately 94.088 million barrels of crude oil per day. Thus, this company only produces 0.11% of the global supply. In the first quarter of 2022, Matador Resources produced an average of 93,969 barrels of oil equivalents per day, which was obviously substantially below the 106,654 barrels of oil equivalents per day that it produced on average during the first quarter of 2023. However, the company’s revenues and income were actually higher during the year-ago quarter:

| Q1 2023 |

| Q1 2022 |

| Revenue |

| $560,276 |

| $565,692 |

| Operating Income |

| $251,433 |

| $309,307 |

| Net Income |

| $178,924 |

| $224,185 |

(all figures in thousands)

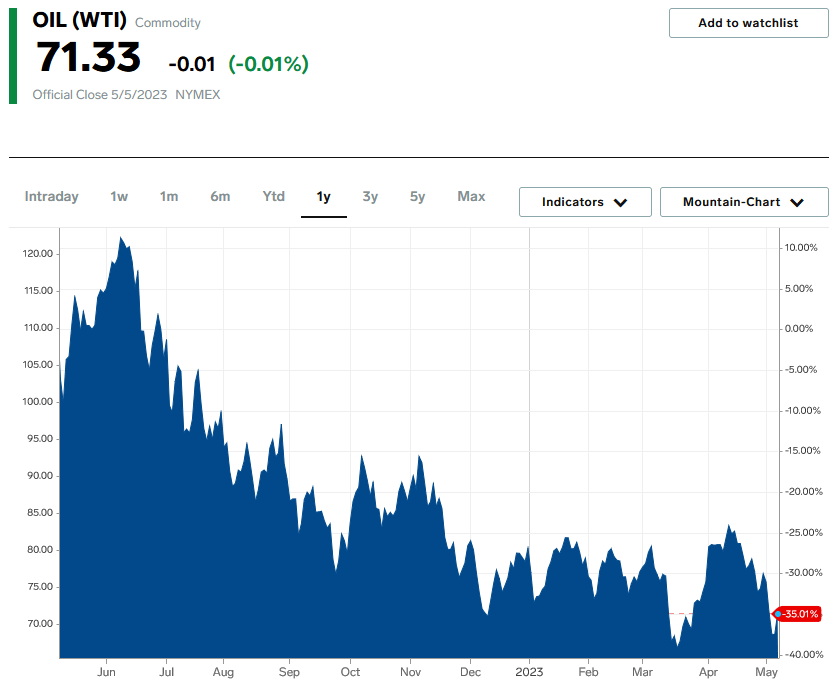

The stronger results last year were caused by the fact that energy prices were significantly higher then than they are now. We can see that quite clearly here:

{kind=link}

Thus, the price of oil is going to have a huge impact on whether the company’s increased production this year results in improved financial performance. That is a difficult question to answer right now. As I pointed out in the introduction to this article, global oil production has been declining. Over the past year, the Organization of Petroleum Exporting Countries has imposed a series of production cuts upon its members, resulting in this organization producing 3.66 million barrels of crude oil per day less than it did last summer. While the United States has managed to grow production over this period, it is nowhere near enough to completely offset these cuts. Overall, the supply of crude oil is smaller than it was last summer. This would normally be enough to cause oil prices to rise, and indeed they did the month immediately following the announcement of the latest round of cuts. However, the boost to energy prices was short-lived as demand in the United States appears to be declining due to economic concerns. Thus, the real question is whether or not the United States will fall into a recession this year. As of the time of writing, the majority of the economic data is pointing to a slowdown in the American economy, which would reduce the demand for gasoline. That could continue to have a negative impact on crude oil prices and cause Matador Resources’ planned growth to fail to actually cause its financial performance to improve.

Fortunately, though, Matador Resources does appear able to produce profitably even if crude oil prices do decline further than we have already seen. In the first quarter of 2023, the company reported a cash flow breakeven of $12.75 per barrel of oil equivalent produced:

{kind=link}

This is well below the average price during 2020, which was the worst year for energy prices that we have seen in a generation. Thus, it seems unlikely that we will need to worry too much about the company suddenly becoming unprofitable if energy prices do weaken this year. Matador Resources appears to be reasonably well-positioned to weather any potential economic climate that could be coming down the pike. When we consider how fearful many investors are right now in the face of the various bank collapses and last year’s weak market, this should be comforting.

Financial Considerations

It is always important that we investigate the way that a company finances itself before making an investment in it. This is because debt is a riskier way to finance a company than equity because debt must be repaid at maturity. This is usually accomplished by issuing new debt and using the proceeds to repay the existing debt. That can naturally cause a company’s interest expenses to go up following the rollover in certain market conditions. When we consider that interest rates are at the highest level that we have seen since 2007, that is a very real risk today. In addition to interest rate risk, a company must make regular payments on its debt if it is to remain solvent. Thus, an event that causes a company’s cash flow to decline could push it into insolvency if it has too much debt. As we have already seen, Matador Resources has significant exposure to commodity prices so this is a risk that we should always be cognizant of.

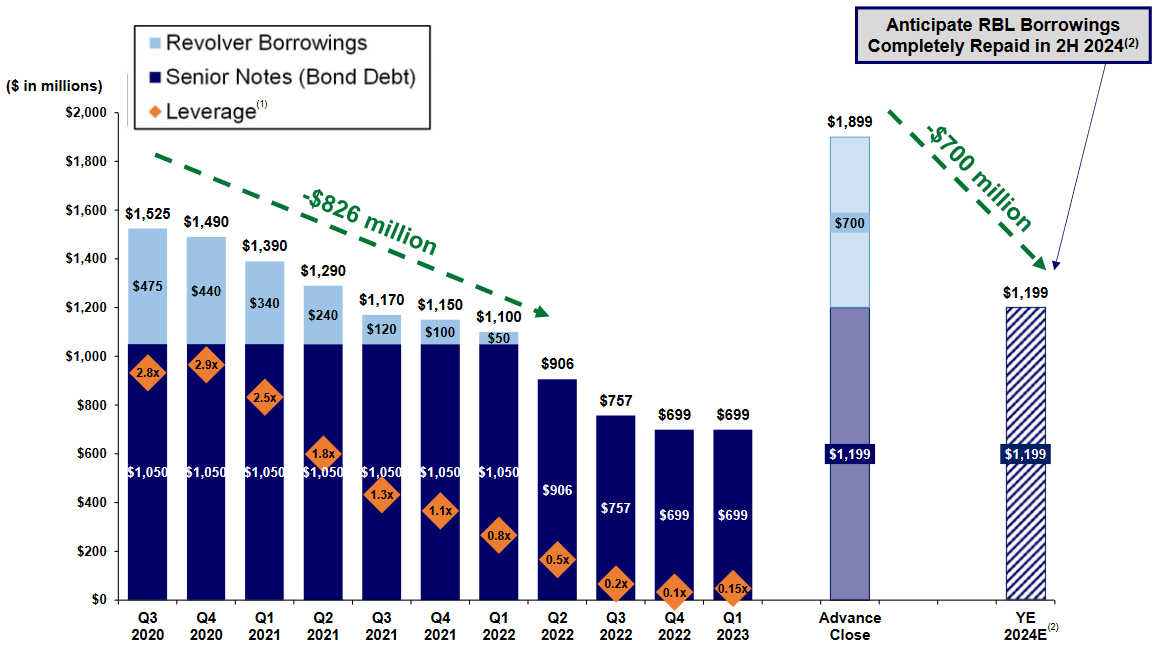

One metric that we can use to measure the debt level of an exploration and production company like Matador Resources is the leverage ratio. The leverage ratio is defined as net debt-to-adjusted EBITDA, and it basically tells us how long it would take the company to completely pay off its debt if it were to devote all of its pre-tax cash flow to that task. As of the end of the first quarter of 2023, Matador Resources had a leverage ratio of 0.15x based on its trailing twelve-month adjusted EBITDA. This is a slight increase over the 0.10x that the company had at the end of 2022, but it is still much better than the company’s past ratios:

{kind=link}

However, the company’s leverage did increase significantly due to the Advance Energy acquisition. This was because Matador Resources partly funded this acquisition by borrowing against its reserves-based revolver. It expects to use the cash flow generated by the acquired assets to pay down this loan over the next two years. While this is a bit disappointing, the company should still be able to keep its leverage ratio under 1.0x for the foreseeable future unless crude oil prices decline significantly. This is a reasonable level that is still among the best companies in the industry. As I have discussed in various previous articles, many upstream companies have managed to get their leverage under 1.0x since the last energy price collapse so Matador Resources is in good company here.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to earn a suboptimal return on that asset. In the case of an exploration and production company like Matador Resources, we can value it by looking at the company’s forward price-to-earnings ratio. This ratio basically tells us how much we would have to pay today for each dollar of earnings that the company is expected to generate over the next year.

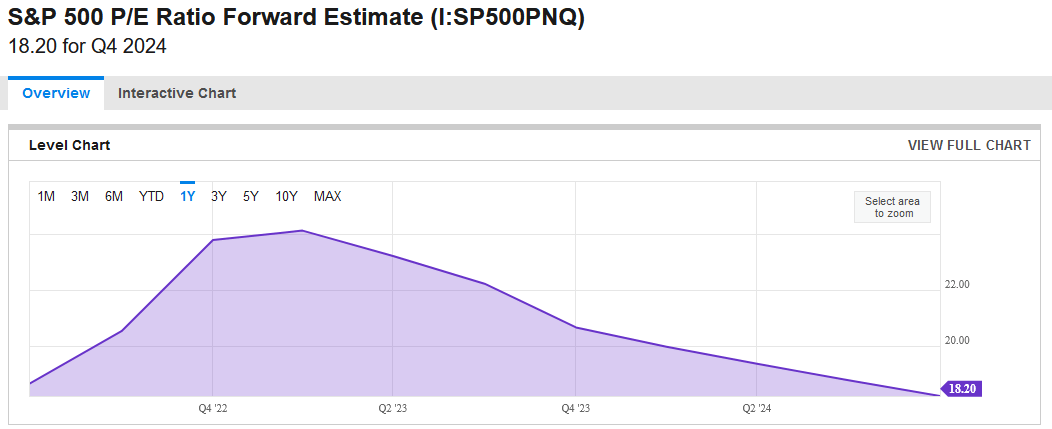

According to Zacks Investment Research , Matador Resources has a forward price-to-earnings ratio of 6.47 at the current price. This is substantially below the 18.20 forward price-to-earnings ratio of the S&P 500 Index ( SP500 ):

{kind=link}

However, as I pointed out last week , pretty much everything in the traditional energy sector is substantially undervalued right now. As such, it is a good idea to compare Matador Resources to some of its peers in order to determine which energy company offers the most attractive relative valuation:

| Company |

| Forward P/E Ratio |

| Matador Resources |

| 6.47 |

| Diamondback Energy ( FANG ) |

| 6.43 |

| Devon Energy ( DVN ) |

| 7.74 |

| Pioneer Natural Resources ( PXD ) |

| 9.81 |

| APA Corporation ( APA ) |

| 6.01 |

As we can see here, Matador Resources generally compares reasonably well to most of its peers. It is not the cheapest company on this list, but it is not the most expensive either. While on the surface, it may seem that the company is fairly valued, it is still well below the S&P 500 Index so still offers a very good thesis for a value investor.

Conclusion

In conclusion, Matador Resources is a somewhat underfollowed independent exploration and production company operating in the Permian Basin. The company is well positioned to deliver reasonably strong production growth, but it, unfortunately, may not be able to deliver near-term earnings growth due to weakness in energy prices and the broader economy. Fortunately, the firm is very well positioned to handle any near-term weakness due to its low-cost financial structure and strong balance sheet. When this is combined with a very attractive valuation, there are some reasons to consider adding Matador Resources to a portfolio today.

For further details see:

Matador Resources: Near-Term Earnings Growth May Be Fleeting, But Still An Attractive Company