MCD - McDonald's: Good Growth Prospects And A Reasonable Valuation (Rating Upgrade)

2023-08-23 11:34:42 ET

Summary

- McDonald's revenue growth is expected to benefit from consumer demand for affordable and convenient dining options in an inflationary environment.

- The company's value offerings, core menu enhancements, and growing digital channel are attracting demand and contributing to revenue growth.

- Moderating inflation and productivity gains should support margin growth for McDonald's.

Investment Thesis

McDonald's Corporation’s ( MCD ) revenue growth should benefit from good and resilient consumer demand for takeaway and quick-service restaurants in the current inflationary environment as consumers are favoring dining options that are more affordable and convenient. MCD being the QSR giant and having leadership market positions across the globe is well poised to capitalize on this trend. Additionally, MCD's value offering, core menu enhancement, and growing digital channel should further attract demand and contribute to revenue growth in the coming years.

On the margin front, the company should benefit from moderating inflation, productivity gains, and sales leverage. In addition, the company’s highly efficient franchise business model also makes it resilient across the macroeconomic cycle. So the company’s revenue and margin growth prospects look good. Further, the stock is currently trading below the historical averages, which provides a reasonable entry point. Therefore, I am upgrading my rating to buy.

Revenue Analysis and Outlook

In my previous article on McDonald’s, I discussed the company’s growth prospects ahead benefiting from good demand due to consumer trade downs to affordable meal options in an inflationary environment. However, I preferred to stay on the sidelines as the valuation multiple was not attractive enough. The company reported first and second quarter earnings since my previous article and the company reported good growth as anticipated. However, the stock price decreased slightly, validating my previous neutral stance based on valuation.

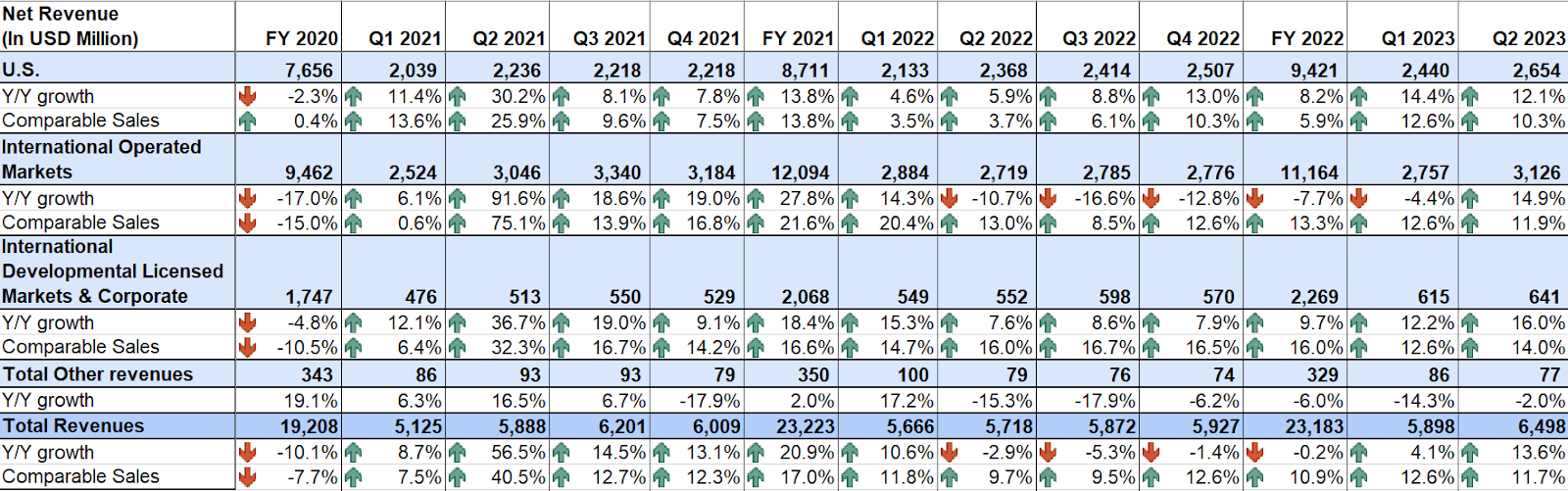

In the recent quarter, the company’s revenue growth continued to benefit from good demand for affordable meal options and attractive value offerings. In addition, the company’s efforts to increase traffic growth through advertising its core menu and price increases also helped sales growth. This led to a 13.6% YoY increase in sales to $6.49 billion, while on a constant currency basis, sales increased by 15% YoY. On a same-store sales basis, global comparable sales increased by 11.7% YoY. The increase in comparable sales reflected double-digit comparable sales growth across all operating segments and was led by the 14% YoY growth in International Developmental Licensed Markets & Corporate segment, where sales growth benefited from strength in the U.K. and German markets.

{kind=link}

MCD’s Historical Revenue (Company Data, GS Analytics Research)

Looking ahead, I believe the company should be able to continue delivering revenue growth benefiting from good end market demand, a focus on value meal offerings, core menu innovations, market share gains, and strength in the digital channel.

The Quick-Service Restaurant ((QSR)) industry often experiences benefits from consumer trade-downs in an inflationary environment. In such situations, consumers usually shift their dining preferences from full-service restaurants to quick-service restaurants. This change is primarily motivated by the need to manage expenses during periods of escalating prices. Quick-service restaurants typically present more economical menu options and faster service, rendering them particularly appealing to budget-conscious consumers.

While full-service restaurants might offer a more lavish dining experience, consumers who are mindful of costs tend to prioritize savings. This trend underscores how economic conditions, like inflation, can wield significant influence over consumer behavior and reshape the dynamics of the restaurant industry. In this landscape, quick-service establishments reap the rewards of their affordability and convenience.

McDonald’s, being a QSR giant and having leadership market positions in the majority of its end markets globally, is attracting these budget-conscious customers to its restaurants. I expect this trend to continue benefiting the company’s sales growth moving forward as well. Moreover, the company is also focusing on value meal offerings to further attract consumers while they are looking for good affordable dining options. MCD launched a McSmart menu in Germany in the first quarter of 2023, which refreshed its everyday value bundles to provide smaller and entry-level affordable meal options to value-seeking and budget-conscious customers. The success of this value offering led to the best-ever sales for that market in the second quarter and lifted overall topline growth.

In June, the U.K. market launched a similar option called the Saver Meals deals. This is a permanent menu addition, which is aimed at ensuring customers that they can still enjoy their favorite items, like the Double Cheeseburger while dealing with the increasing cost inflation. The goal is to consistently offer affordable choices for everyday meals and I expect this increased focus on everyday value offerings in the U.K. should gain similar traction to Germany. This should continue to increase demand and help the company’s sales growth.

In addition to everyday value offerings, the company is also focusing on its core menu items like the Big Mac, Chicken McNuggets, or McChicken Sandwich, through modernizing and innovating them to better resonate with changing consumer behaviors as these menu items are very popular among customers globally. During the second quarter, MCD in the U.K. had a special promotion where they paired limited-time sauces with their Chicken McNuggets. This, combined with increased advertising for their core menu items, led to an increase in guest traffic as consumers felt comfortable spending their money on familiar foods. In China, the company introduced a 20-piece Chicken McNuggets option, which was well-received and boosted customer traffic. Additionally, they expanded the availability of Spicy McNuggets, a popular menu addition from 2020, to various markets in the second quarter, including Australia and Germany. Both markets achieved a significant lift to the McNuggets line as a result.

The company is planning to further scale the innovations in the core menu to more markets moving forward. I expect MCD’s effort to promote and expand its core menu items should help it adapt and meet changing customer taste profiles while gaining market share in the chicken items category by scaling these ideas across the globe, all while supporting sales growth.

Lastly, the company’s digital channel is also delivering good results in boosting top-line growth. The company has its loyalty program now in over 50 markets across the globe, and in MCD’s top-6 markets, digital sales represent nearly 40% of system-wide sales, with 90-day active loyalty members of over 52 million across those top-6 markets. The company is leveraging data and insights from these active members regarding their visit frequency, visit timings, and their purchase pattern to better execute against consumer demand, which is helping its sales. Moreover, the company is also enhancing customers' digital experience and increasing customer convenience by improving the ordering process through its application. This helped in increasing digital sales in the U.S. in the second quarter and I expect as customer experience improves further, and the number of loyalty members goes up, digital channels should continue to help the sales growth for the company.

These efforts of increasing value offerings, promoting core menu items, and enhancing digital channels should help the company in driving additional demand on top of secular trends from consumer trade down in an inflationary environment and also increase the market share for the company across the globe. So, I remain optimistic about the company’s sales growth prospects ahead.

Margin Analysis and Outlook

In the second quarter of 2022, the company continued to face inflationary headwinds from food and labor costs which pressured the company-owned restaurant margins. However, the company was able to offset these headwinds with good contributions from the franchise restaurant's margin (as ~90% of the company’s margin is driven by its asset-light franchise business model). In addition, sales leverage, price increases, and lower G&A expense as a percentage of sales also helped the company deliver margin growth. As a result, the adjusted operating margin increased by 260 bps YoY to 48%.

MCD’s Historical Restaurant Margin and Adjusted Operating Margin (Company Data, GS Analytics Research)

Looking forward, I believe the company should be able to deliver margin growth. Last year, MCD incurred mid-teens inflationary headwinds. However, for the full year 2023, management expects a mid to high single-digit inflation. I expect that inflation should continue to moderate as we move forward and become less of a drag on the margins. Moreover, the company’s employee turnover has stabilized, implying that new hiring and training costs should also stabilize in the coming quarters, which should also help margin growth.

Additionally, the company has been taking several measures to speed up its operations. MCD is working to enhance the digital ordering process, making it more convenient for customers. This also helps restaurant staff track orders more accurately using location data. They can begin preparing orders before customers arrive, ensuring that the food is fresh and ready when customers pick it up, which speeds up service. This boosts productivity in restaurants. Further, MCD is investing in digitizing the company and introducing new tools and platforms to make it easier for employees to access information, gain insights, and perform better. This should free up more time for the company to focus on understanding the needs of customers, franchisees, and staff in the restaurants and improve efficiency, supporting margins.

Furthermore, MCD’s margins should also benefit from operating leverage as sales continue to increase. Moreover, the company’s highly efficient franchise model is the major driver of its margin growth. With ~90% of restaurant margins coming from franchises, the company has well-shielded itself from external macroeconomic headwinds. This asset-light business should help the company remain resilient during an economic crisis. Management has guided for a 46% adjusted operating margin for the full year 2023, which is about a 120 bps YoY increase from 2022. I believe the guidance is achievable and the company can even beat it given it was already at 48% adjusted operating margin last quarter and inflationary headwinds are moderating which should pave the way for further improvement.

Valuation and Conclusion

McDonald’s is currently trading at 24.20x FY23 consensus EPS estimate of $11.58 and 22.54x FY24 consensus EPS estimate of $12.44, which is below the historical 5-year average forward P/E of 26.82x . The company has good growth prospects and its leadership position in the QSR industry along with a highly efficient franchise model should help it sustain both the top and bottom lines during any kind of adverse macroeconomic situation. I also like the company’s execution and how it is able to improve sales and margins despite broader macro concerns. I believe the valuation is attractive, especially on FY24 P/E multiple given the growth prospects ahead. Moreover, the stock also offers a 2.17% forward dividend yield, which should further enhance total return moving forward. Hence, I am upgrading my rating to a buy.

For further details see:

McDonald's: Good Growth Prospects And A Reasonable Valuation (Rating Upgrade)