MCD - McDonald's: The Growth Story Suggests A Hold

2023-09-24 02:28:06 ET

Summary

- McDonald's demonstrates consistent earnings growth and strong sales growth across major markets, attributed to strategic price adjustments and investment in digital channels.

- Digital orders make up 40% of sales in McDonald's top six markets, positioning the company well to capitalize on the growing trend of food delivery.

- Sales growth is expected to slow down in the second half of the year due to declining inflation and a challenging macro-economic environment, but foot traffic may increase with lower prices.

The McDonald's Corporation ( MCD ) has demonstrated a robust history of consistent earnings growth, solidifying its position as a stalwart in the fast-food industry. This sales growth has persisted in recent quarters, with strong sales growth reported across most of McDonald's major markets. This impressive performance is attributed in part to strategic price adjustments made to counter inflation, despite associated cost increases in key ingredients like cheese and meat. Remarkably, this did not deter patrons, as the number of visitors to McDonald's restaurants in the US continued to rise.

In an era increasingly defined by digitalization, McDonald's has also been proactively enhancing its online channels to further drive sales growth. In my view, strong investment in these digital channels positions McDonald's well to benefit from changing consumer behaviors, which sees consumers increasingly wanting to order in. Studies show that this shift in behavior spans across all age groups, solidifying food delivery as a permanent fixture in the restaurant industry. Currently, digital orders constitute a substantial 40% of sales in McDonald's top six markets, positioning the company well to capitalize on this evolving consumer trend and maintain its robust market share.

Sales growth and outlook

In the second quarter of 2023 McDonald's reported a 17.7% Year-over-Year (YoY) increase in sales at company owned restaurants and an increase in sales of just over 11% YoY at franchisee owned restaurants. Total global comparable sales increased by around 11.7% Quarter-over-Quarter (QoQ) which exceeded analysts' expectations of an increase of around 9.2%.

This strong sales growth has been partially attributed to increased prices to keep pace with inflation. The inflation driven increases were also coupled with increases in the costs associated with key ingredients such as cheese and meat and could potentially result in a reduction in the number of patrons. Despite this inflation driven increases, McDonald's also saw a growing number of visitors to its restaurants in the US. In my view, this is indicative of its relatively good pricing power, with an ability to increase prices to protect margins without losing its patrons.

As part of its efforts to continue driving sales growth, McDonald's has also actively worked on strengthening its online channels. In the United Kingdom, McDonald's has for example entered into a long-term partnership with Deliveroo to expand delivery options for McDonald's meals. In terms of this agreement, Deliveroo, whose largest customer base is in the UK, would join the McDelivery partners to deliver meals. In the US, McDonald's largest market, the company has also actively worked on improving its app with management noting that –

Last quarter, we introduced an enhanced ordering process through our app in the US with the goal of delivering a faster and more enjoyable experience for the customer. While we're still learning from this deployment, early results have been extremely positive with elevated sales initiated through the app, increased customer satisfaction and improved service times.

In my view, this continued focus on improving digital sales systems and delivery services will be crucial for McDonald's long term growth given the increased consumer preference for food delivered directly to their door. In a study commissioned by Next Bite it was found that around 43% of consumers now order food for delivery at least once a month while 23% of consumers order meals for delivery at least once a week. According to a study conducted by Next Bite, prior to the pandemic, the 18-34 age group predominantly utilized food delivery services, as they were the most adept at using mobile apps and their lifestyles prioritized speed and convenience. However, the pandemic brought about a shift in behavior driven by necessity and safety concerns, leading to widespread acceptance of ordering delivery across all age groups.

The study notes that while millennials remain the most frequent users (with 71% placing weekly orders), even older demographics have embraced online meal delivery platforms now considering it a normal part of their routine. As a result, food delivery has solidified its position as a permanent fixture within the restaurant industry, necessitating that delivery options cater to a much broader audience. For McDonald's itself, digital orders now make up around 40% of sales in its top six markets. Therefore, McDonald's is in my view well positioned to continue capitalizing on this change in consumer behavior, which should also assist it in maintaining its strong market share.

Nevertheless, management currently expects sales growth to slow down in the second half of the year. This decline in sales growth is expected to be driven by declining inflation and a more challenging macroeconomic environment in some of its key markets. Management has observed in this respect that –

..we certainly are seeing inflation start to gradually come down. I think that's been the case in the US business probably starting the end of last year. It's obviously still elevated, but I think we are seeing that gradual kind of decline. And I think in the majority of our international markets, we started to see, I think, as we head into the back half of the year, the gradual decline begin there as well. And so I think as inflation begins to come down, I would certainly expect our pricing levels to also start to come down … I think there are a number of our top markets where we know the macroeconomic conditions are challenging. We know there continues to be a lot of pressure on consumers. We know consumer sentiment continues to be impacted. And so we do expect the broader sector to kind of begin to kind of decline in those markets as we go through the back half of the year.

These factors certainly seem likely to contribute to a moderation in sales growth. However, in my view, a decline in prices might well result in a further increase in foot traffic which could offset any lower prices. Nevertheless, this is certainly an area for investors to monitor closely, particularly as analysts expect the broader quick service restaurant industry to face a more challenging operating environment in the quarters ahead.

Overtime rules

In a recent article posted on SeekingAlpha News, it was noted that a proposed change to overtime rules by the Department of Labour could pose significant challenges to quick service restaurants such as McDonald's. In terms of the proposal, the salary threshold for overtime eligibility under the Fair Labor Standards Act would be increased to $1,059 per week, equivalent to $55,068 annually. According to the Department of Labor, this is expected to expand coverage to 3.6 million additional workers.

While the exact number of workers at McDonald's who are likely to be affected is not known, the Department of Labor’s figures indicate that just over 21% of the potentially affected employees are employed in the leisure and hospitality sectors. This shows that the quick service restaurant sector will certainly be affected by the proposed rule should it take effect. However, I am of the view that the precise impact may be more limited, given that the Department of Labor’s own report notes that the majority of the potentially affected workers do not work overtime. In a representative week, only around 3.6% of these workers ordinarily work overtime.

Nevertheless, the Department of Labor expects the total direct cost of this proposal to amount to around $1.2 billion in additional wages to be paid in the first year of this proposal taking effect. This includes more than $400 million in expected regulatory familiarization costs. The effect of the increase would not accordingly be limited to the actual payment of the increased wages but also by general regulatory compliance cost which would arise even if the business had a relatively small number of affected employees. The effect of the rules are not accordingly insignificant to McDonald's in my view but seem more likely to be passed onto consumers than having a substantial effect on profitability. In my view, McDonald's strong pricing power, as evidenced by its ability to raise prices in the current high inflation environment without losing foot traffic, places it in a strong position to pass these costs onto customers without scaring customers off.

Valuation

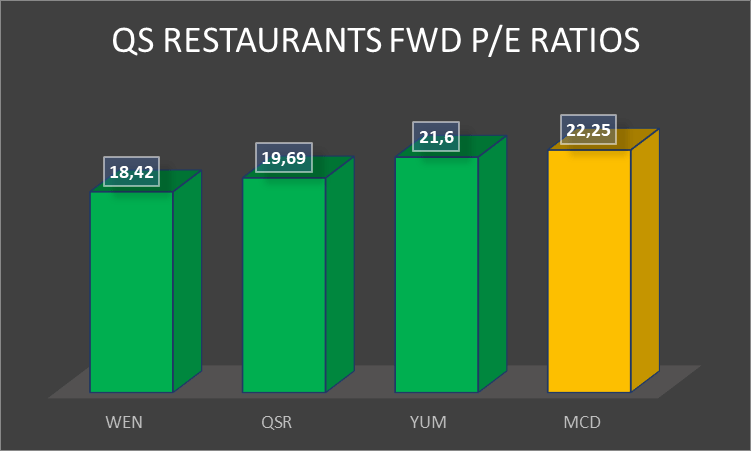

McDonald's is trading at a forward P/E ratio of around 22.25 which is the highest of the quick service restaurant groups considered in the peer comp chart below. This elevated valuation might be partially justified by strong sales growth and is lower than McDonald's historic forward P/E ratio, with its 5-year average forward P/E ratio of 24.9 and a 10-year average forward P/E ratio of 24.7.

QS Restaurants FWD P/E Ratios (Author created based on data from EquityRT)

{kind=link}

Despite its higher-than-peers valuation level, McDonald's stock does not accordingly appear overvalued in my view. Nevertheless, I am also not able to conclude that the stock is substantially undervalued. The current discount to its historical levels likely arise from concerns over slowing sales growth and might well justify a 10% discount to its historical average forward P/E ratio. In my view, the stock is currently trading around fair value and would start presenting an attractive buy around $260 per share.

Conclusion

McDonald's strong sales growth, attributed in part to strategic pricing adjustments, reflects its ability to navigate challenges like inflation and rising ingredient costs while maintaining customer loyalty. It is this strong pricing ability that also leads me to be less concerned about the newly proposed wage rules. Ultimately, I believe that McDonald's would be well positioned to pass on the bulk of these costs to its customers.

The company's proactive investment in digital channels and delivery services positions it favorably to capitalize on the growing consumer preference for convenience. With digital orders already comprising a significant portion of sales in key markets, McDonald's is well poised to sustain its market dominance. Looking ahead, the anticipated slowdown in sales growth could present a challenge, even though the potential increase in foot traffic with a decline in prices may offset this moderation.

The current valuation levels of the stock, while higher than those of its peers, also seem reasonable from a historical perspective. Nevertheless, I do not consider the stock undervalued at the moment, given the challenges presented by moderating sales growth. Ultimately, I rate McDonald's a hold at its current price level and would consider initiating a position anywhere from $260 per share.

For further details see:

McDonald's: The Growth Story Suggests A Hold