CA - McEwen Mining: Limited Margin Of Safety At Current Levels

2023-08-01 09:39:40 ET

Summary

- McEwen Mining will report its Q2 results in August and while we don't know how production from Gold Bar will look, San Jose's production was disappointing.

- Meanwhile, with disruptions to several operations due to severe power outages and wildfires in Ontario/Quebec, the Fox Complex may have seen lower production as well, impacting Q2 results.

- However, the bigger news is the recent Los Azules PEA by McEwen Copper and the MARA Project sale to Glencore, which came in at a lower price tag than expected.

- This could potentially weigh on MUX's valuation, with Los Azules being earlier-stage (PEA vs. nearing DFS completion) and a smaller-scale asset and it being difficult to justify MUX's current valuation using similar comps to the MARA sale given that Los Azules makes up a large portion of MUX's fair value.

It's been a mixed start to the Q2 Earnings Season for the Gold Miners Index ( GDX ) and while several large-cap names have reported, most of the small-cap producer universe is left to report, including McEwen Mining ( MUX ). In MUX's case, the company just came off a soft Q4 due to inclement weather in Nevada and production out of San Jose wasn't much better in the seasonally weak portion of the year. However, while I was expecting a much better Q2, San Jose's production numbers from Hochschild ( HCHDF ) came in below my expectations yet again on sharply lower grades, and it's not clear how MUX's production results at Fox Complex will look with weather related power outages and wildfires taking a toll on some Quebec/Ontario operations. Let's take a closer look at recent developments.

Upcoming Q2 Results

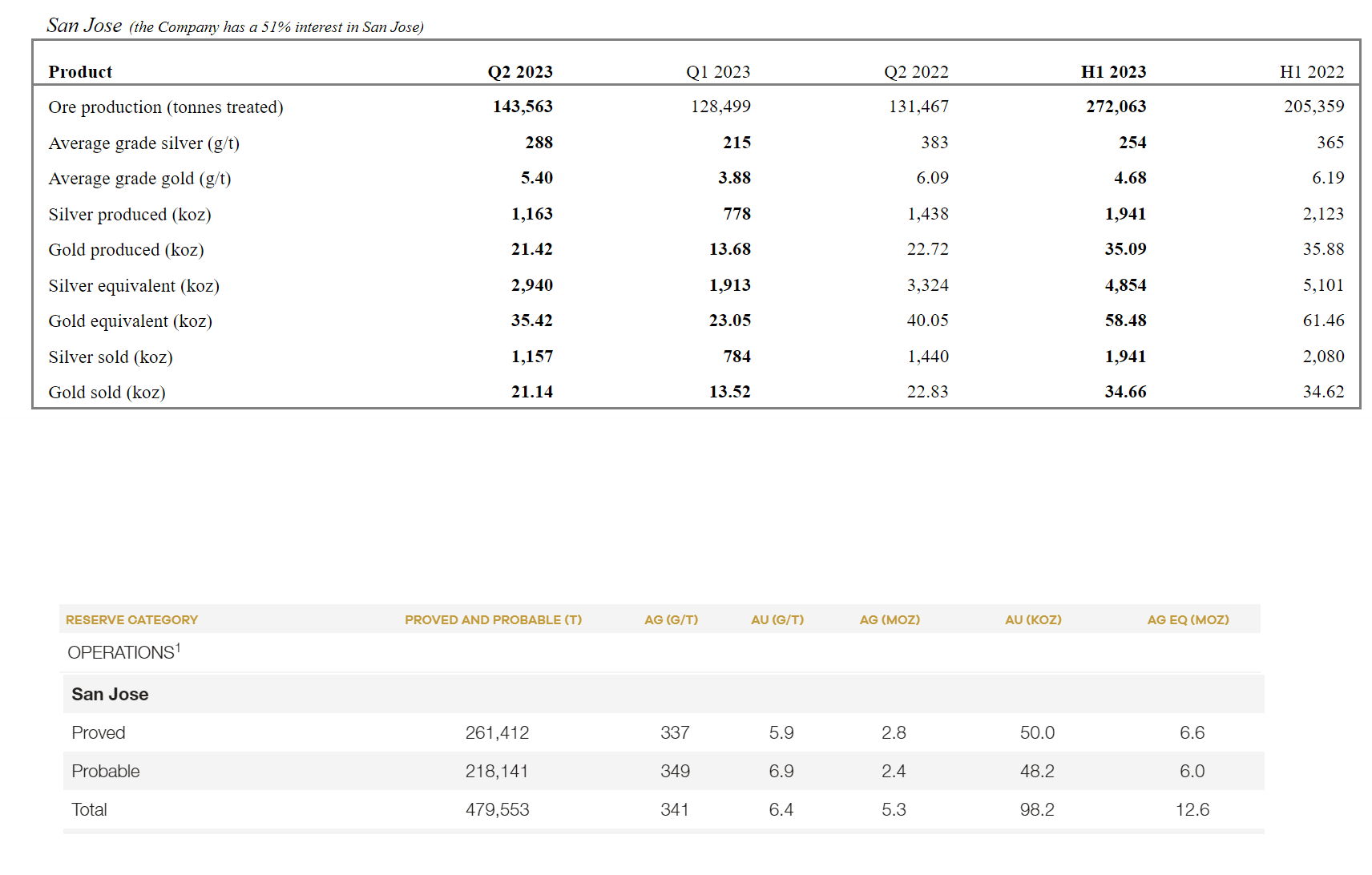

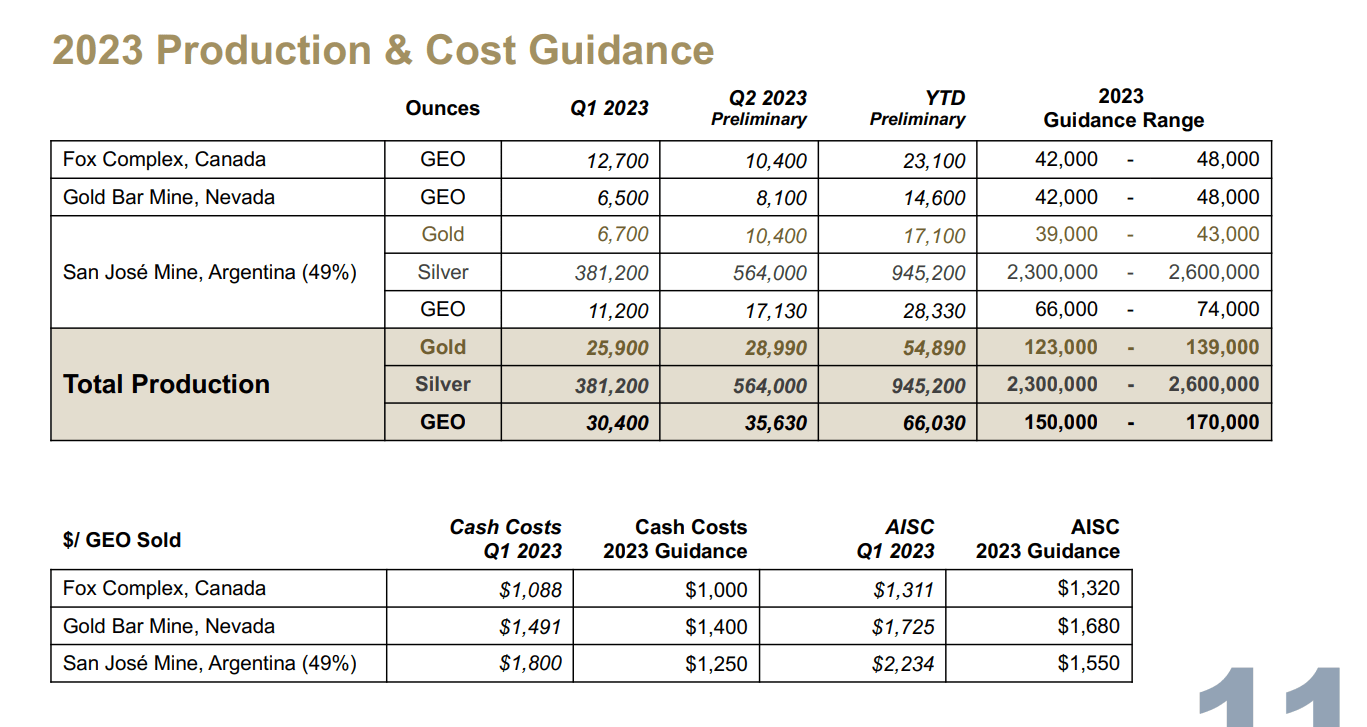

McEwen Mining should report its results in late August per usual, and while we don't know yet what its production results from its Fox Complex and Gold Bar will look like, there's a decent chance that Fox Complex production may have seen some impact from the weather related power outages and summer wildfires that affected air quality and visibility and led to unplanned downtime at several Ontario and Quebec operations (Young-Davidson, Island Gold, LaRonde, Casa Berardi). This is because many operators canceled some shifts, could not be as productive because of road closures, and saw increased mill downtime because of significant power outages. And while it's possible that the Fox Complex got through the quarter with no disruptions, we already know that it was another weak quarter at Hochschild's San Jose Mine, with gold-equivalent production [GEO] of just ~35,400 ounces, translating to attributable production of just ~17,300 ounces, a 12% decline year-over-year.

San Jose Q2 Production (100% Basis) and San Jose Reserves (Attributable Basis) (Hochschild Mining)

{kind=link}

At Hochschild's San Jose Mine where McEwen Mining holds a 49% interest, production was lower due to declining gold and silver grades, which were partially hit by higher throughput, but the bigger issue here continues to be reserves. And as noted in prior updates, it's difficult to have confidence in this mine's ability to continue production throughout this decade to help maintain McEwen Mining's production profile when the asset is sitting on just ~940,000 tonnes of reserves compared to an annual mine production rate closer to ~520,000 tonnes. This translates to just a 1.7 year mine life, and while the company may replace reserves successfully, the key will be to ensure it adds high-quality reserves given that this is an asset that produced at north of $21.00/oz costs last year on a silver-equivalent basis, meaning that average grades won't cut it for Hochschild if it wants to run this asset at a positive all-in sustaining cost margins.

Meanwhile, at the company's Gold Bar, most Nevada producers reported decent production and didn't note any major weather issues, and McEwen Mining has transitioned to a new mining contractor that should hopefully allow for a bounce back from the rough Q1 the mine experienced (Q1 production: ~6,500 GEOs). That said, this is an asset that's producing at all-in costs closer to $1,800/oz, so I would argue that the two more important operations to McEwen Mining are Fox Complex and San Jose (49%). And with San Jose tracking behind guidance with just ~28,500 GEOs produced year-to-date vs. a guidance midpoint of 70,000 GEOs provided by MUX, and Fox Complex potentially set to have a weaker quarter as well, it's tough to be overly optimistic about the company's upcoming Q2 results and H1 results overall.

So, was there any good news?

Fortunately, the gold price is cooperating for McEwen Mining and this matters for high-cost producers. In fact, producers that have reported quarter-to-date have enjoyed an average realized gold price of $1,950/oz or better, which should translate to a better Q2 financially for McEwen Mining. That said, the bigger story here which makes up a larger portion of the valuation is the company's stake in McEwen Copper, which holds a 100% interest in the Los Azules and Elder Creek Projects. And just recently, we saw an updated Preliminary Economic Assessment out of Los Azules that highlighted the project's economics with a new development plan vs. its conventional mill and float concentrator producing copper concentrate contemplated in its 2017 PEA. And while the economics were decent and better than I expected (albeit costs are likely to rise as cost assumptions tighten up in Feasibility Studies), there was some negative news which we'll discuss later.

Los Azules Updated PEA

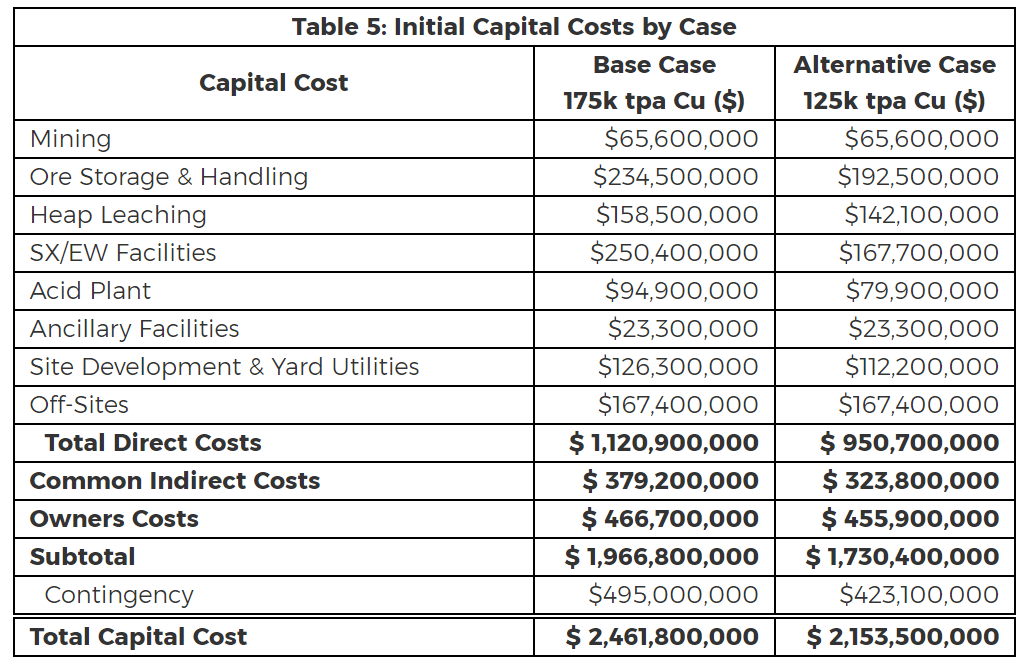

McEwen Copper (51.9% owned by McEwen Mining) released an updated PEA for its Los Azules Project in San Juan, Argentina, with a shift in plans to an open-pit heap-leach operation using solvent extraction-electrowinning vs. the plan to produce copper concentrate previously. The shift in plans was related to the benefits from reduced water consumption, lower permitting risk, and cathode production that can be used directly in the industry vs. concentrate to reduce export taxes and reliance on third-party smelters. Digging into the economics, the base case for the project is expected to produce average annual copper cathode production of ~182,000 tonnes during the first five years of operation and ~146,000 tonnes over its expected 27-year mine life. Meanwhile, total recoverable copper cathode is expected to be ~8.7 billion pounds at a 72.8% average copper recovery rate, and upfront capex is estimated at ~$2.46 billion, excluding ~$155 million for construction of a 132 kV power supply line to the site that's expected to be constructing by YPF Luz, an Argentinean power company.

{kind=link}

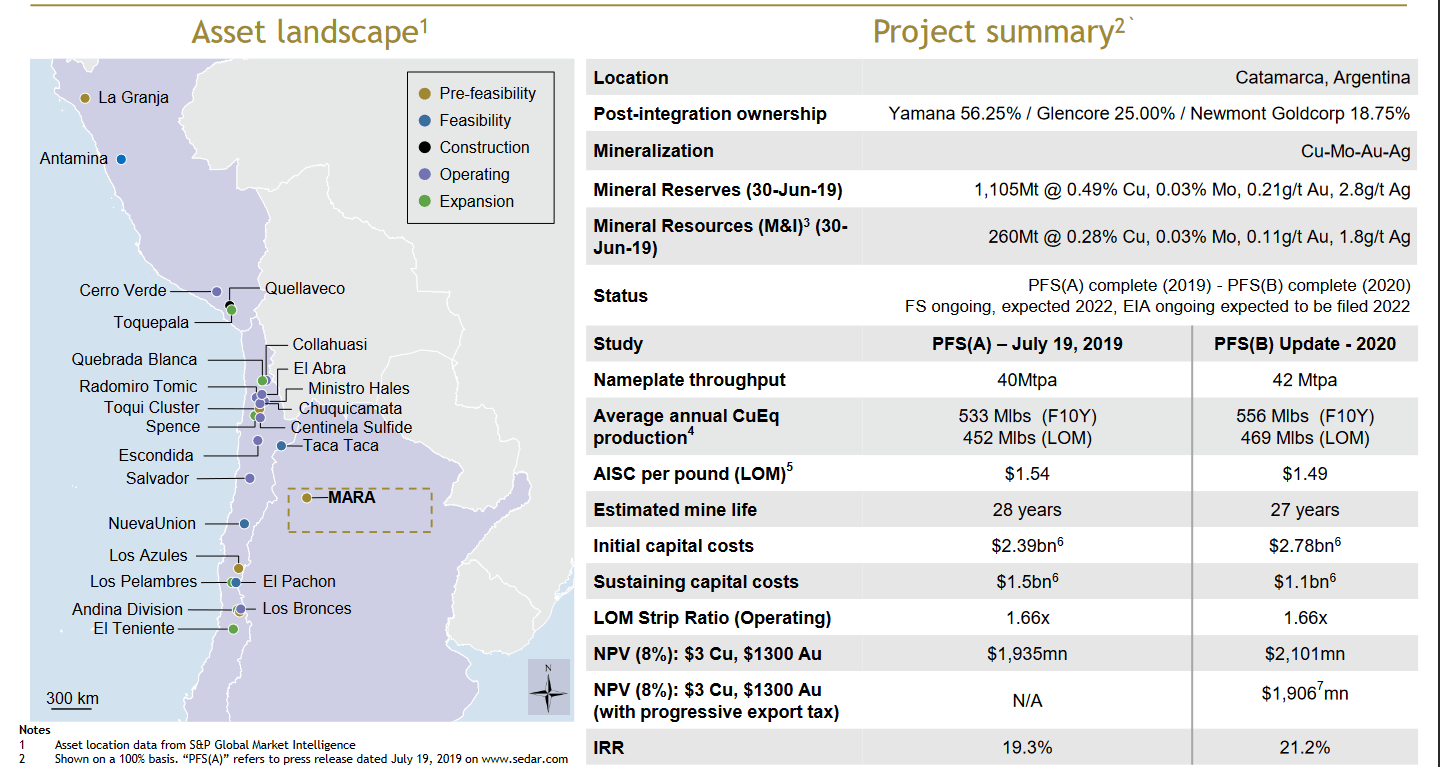

Using a $3.75/lb copper price assumption which is reasonable given that this is now the three-year average for the metal, the estimated NPV (8%) comes in at ~$2.66 billion or ~$1.93 billion in the smaller alternative case of 125,000 tonnes per annum (base case: 175,000 tonnes per annum). This translates to an NPV (8%) midpoint between the two cases of ~$2.29 billion, a value far above McEwen Mining's market cap even if it only has an interest in half of the project through its stake in McEwen Copper. However, this week we saw a major copper transaction in the sector that came in at an underwhelming picture, with Pan American Silver ( PAAS ) selling its stake in MARA (56.25%) for just ~$475 million. This implied an NPV (8%) multiple of just 0.24x on its PFS economics (excluding its royalty) using similar metals prices to the Los Azules PEA, suggesting that there's no reason to believe that Los Azules should be valued at anywhere near 1.0x NPV (8%), let alone 0.50x NPV (8%).

{kind=link}

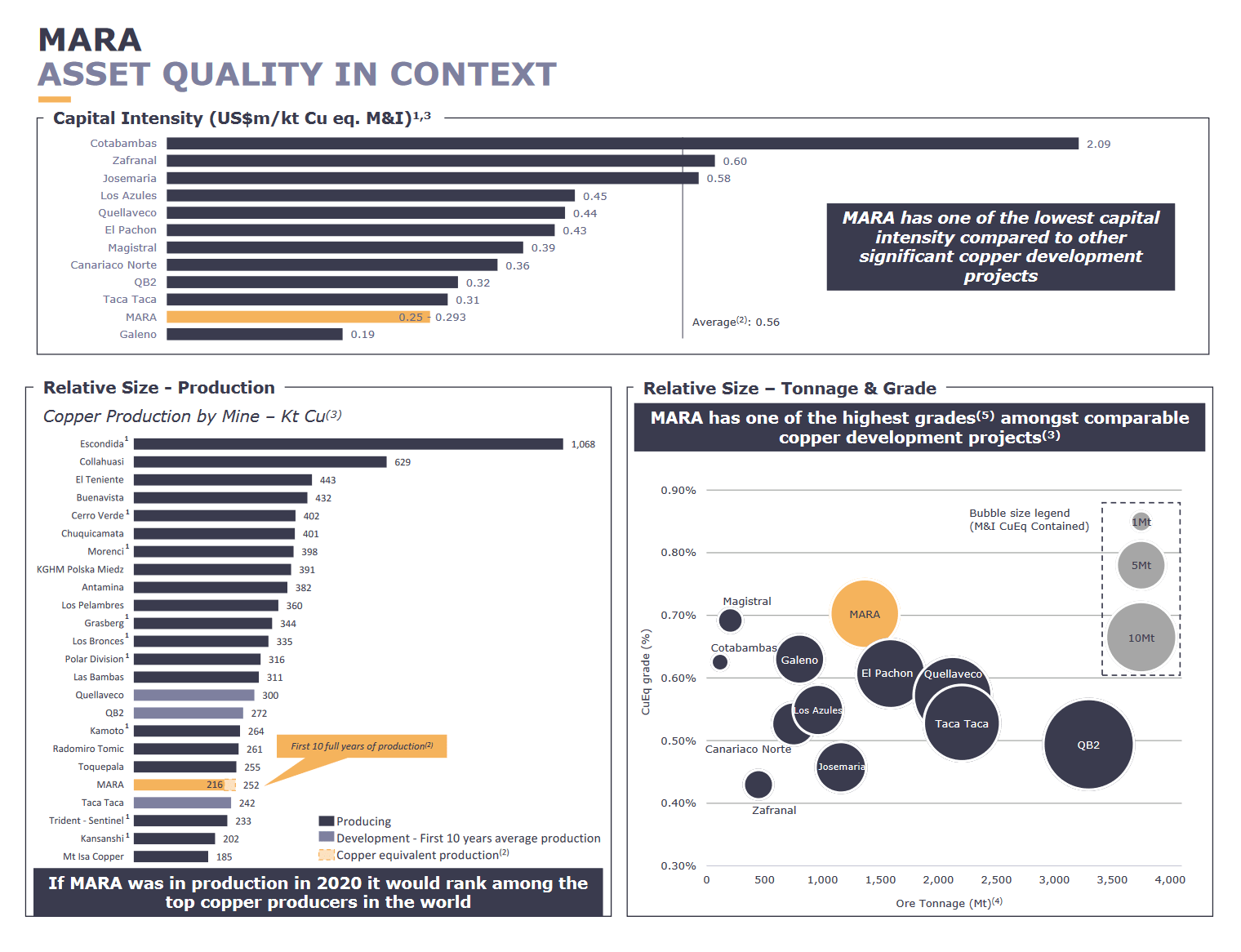

In fact, I would argue that MARA is the more attractive project of the two and a solid comparable asset given that it's also in Argentina and could begin production by the end of the decade. However, MARA is the more advanced of the two projects, it boasts a higher average copper equivalent grade, and it should head into production sooner assuming Glencore makes it a priority, with a 4-year construction period and the potential to be in production by 2028 vs. Los Azules initial production in 2029 in a best-case scenario. So, with MARA boasting greater scale than Los Azules (base and alternative case) and being one of the most capital-efficient undeveloped copper projects with the benefit of existing infrastructure at Alumbrera (concentrator plant, tailings dam with seven years of capacity and Alumbrera open-pit for in-pit tailings) and a concentrate transportation system, it should be valued at a premium to Los Azules.

To summarize, while the MARA deal is positive for Sandstorm Gold Royalties ( SAND ) which has an option to purchase a gold stream on the asset, and it's positive for Pan American Silver ((PAAS)) that just improved its balance sheet meaningfully, I don't see this deal as overly positive for McEwen Mining which also has an interest in an earlier-stage and smaller-scale copper project in Argentina with similar upfront capex that makes up a large portion of its current valuation. This is because the deal came in at lower levels than I expected even including the copper royalty granted by Glencore and one could argue that a fair value for Los Azules (being earlier-stage and smaller-scale, and not benefiting from existing infrastructure to reduce risk of a capex blowout) is 0.20x NPV (8%) or lower. Let's see how this affects MUX's valuation:

Valuation & Technical Picture

Based on ~51 million fully diluted shares and a share price of US$8.90, McEwen Mining trades at a market cap of ~$454 million. This may seem like a bargain at first glance for a company that operates two mines (Ontario and Nevada), has a 49% interest in another mine in Argentina, and has a 52% interest in McEwen Copper which owns the Los Azules Project (Argentina) and the Elder Creek Project in Nevada. However, as I've discussed in past updates, its precious metals operations leave much to be desired with razor-thin margins, evidenced by the Fox Complex and Gold Bar expecting to produce at average AISC of ~$1,500/oz per guidance. Meanwhile, in San Jose's case, which is operated by Hochschild ((HCHDF)), the mine's silver-equivalent all-in sustaining costs last year came in at $21.70, making it one of the highest cost operations in its peer group.

{kind=link}

Fortunately, McEwen Mining has succeeded in convincing the market that its 51.9% stake in McEwen Copper was worth a pretty penny (which has helped with its outperformance), noting that compared to other projects, its fair value was equal to $2.47 to $25.14 per share. However, the recent MARA Project transaction in Argentina by Glencore (GLCNF) has made the upside case for McEwen Copper's value look quite ambitious and makes the low end seem much more realistic for fair value. This is because Glencore purchased the remaining 56.25% stake in MARA for $475 million (excluding the 0.75% copper royalty), translating to a valuation of ~0.24x its NPV (8%) of ~$3.5 billion at ~$3.75/lb copper and $1,800/oz gold on a cash basis. And as noted previously, this is a project that is more advanced than Los Azules (nearing DFS completion vs. PEA stage), and one that boasts a larger scale (~252,000 tonnes of copper production first 10 years vs. Los Azules at ~132,000 to ~182,000 tonnes in its first five years).

{kind=link}

If we apply this same multiple to the mid-point NPV (8%) figure of ~$2.29 billion (base case and alternative case) for Los Azules at the same copper price assumption, the fair value for McEwen Mining's stake ($2.29 billion x 51.9% ownership x 0.24) would equal ~$285 million, or ~$5.60 per share on a fully diluted basis. And assuming we ascribe a value of $220 million for the rest of McEwen Mining's portfolio (precious metals assets, royalties, and Elder Creek interest), this translates to a total fair value for McEwen Mining of $505 million [US$9.90]. Some investors will point out that this is above today's share price and points to 10% upside. However, I am not willing to invest in precious metals names for just a 10% upside given their volatility and I want a minimum 40% discount to fair value to justify starting new positions, especially if I'm going to invest in names that have a track record of struggling to create shareholder value over the past decade.

{kind=link}

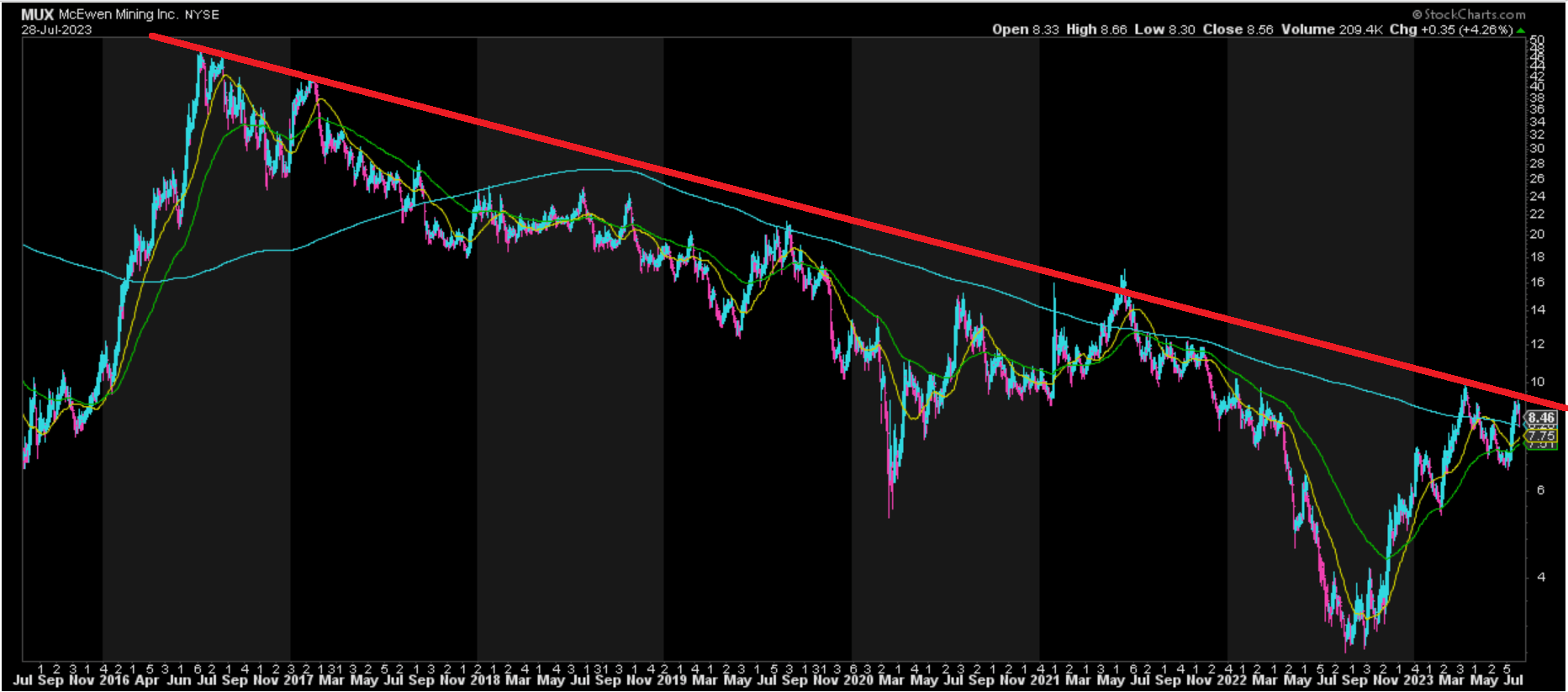

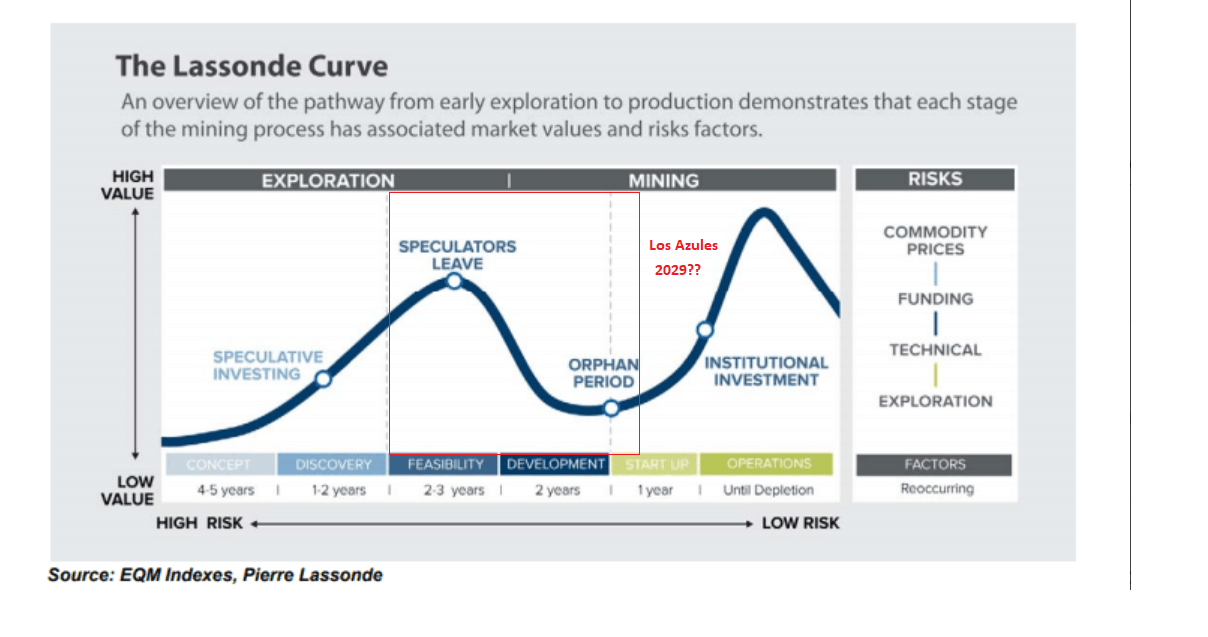

Finally, if we look at the technical picture, McEwen Mining has enjoyed material outperformance vs. its peer group but has now rallied straight into a multi-year downtrend line and continues to get rejected in this area. And with the stock now trading near its estimated fair value and with no clear catalysts on the horizon for a re-rating, it would not surprise me to see the stock stall out here at US$8.90 or even correct from current levels. The reason? For starters, there are several more attractive names from a relative value standpoint following MUX's outperformance vs. peers despite those companies having higher-quality assets, suggesting some rotation is possible. Second, Los Azules has a long and expensive road ahead to first construction and is sitting in the least favorable portion of the Lassonde Curve, with first production unlikely until 2029.

Lassonde Curve (Pierre Lassonde, EQM Indexes, Author's Notes)

{kind=link}

So, with a portfolio of precious metals assets struggling to consistently grind out a profit, a 49% interest in a mine whose reserves are dwindling, and Los Azules being years away from first production and being weeks out from boasting the most favorable economic assumptions following a PEA (given that we typically see large cost revisions from PEA --> PFS --> DFS), I don't see what will power the stock higher if the recent Los Azules PEA wasn't able to accomplish this. Besides, even if MUX does head higher, there are some names out there offering over 100% upside to fair value even at current gold price assumptions that are likely to outperform over the next year, making them far more attractive places to park one's money.

Summary

McEwen Mining has enjoyed significant outperformance relative to its peer group over the past year and when a serial laggard significantly outperforms the sector, it's often better to take the money and run. And the even larger mistake is paying up for these stocks in the later innings of their rally and exposing one's self to the potential for a sharp drawdown. Obviously, I could be wrong and MUX could continue its outperformance, which has continued longer than I expected. However, with the stock offering little margin of safety and its low-risk buy zone not coming in until US$5.90, I continue to see far more attractive bets elsewhere in the sector. To summarize, I don't see any reason to chase this rally in MUX above US$8.90, and I would view any rallies above US$9.60 before October as profit-taking opportunities.

For further details see:

McEwen Mining: Limited Margin Of Safety At Current Levels