CA - McEwen Mining: Tracking To Low End Of 2023 Guidance

2023-12-20 05:10:33 ET

Summary

- McEwen Mining's Q3 production improved in Q3, with the Fox Complex having one of its best quarters in years.

- However, consolidated costs have remained well above the industry average, and it's difficult to generate free cash flow with Gold Bar's AISC consistently above $1,900/oz.

- In this update, we'll look at the Q3/quarter-to-date production results, the stock's updated valuation after its recent share dilution, and whether MUX is worthy of investment at current levels.

Just over six months ago, I wrote on McEwen Mining (MUX), noting that while the stock had momentum at its back and was one of the best performers year-to-date, there was no reason to chase the stock above US$9.20. This is because the stock was trading within 10% of what I believed to be its fair value (even using a generous value for its low-margin precious metals mines), and was running into key resistance near US$9.00. Since then, the stock has suffered a ~35% drawdown, but has since recovered and is back to challenging short-term resistance near US$8.30. In this update we'll look at the Q3 and quarter-to-date production results, the stock's updated valuation, and whether the stock is worthy of investment at current levels.

{kind=link}

Q3 Production & Sales

McEwen Mining released its Q3 results in November, reporting quarterly production of ~38,500 gold-equivalent ounces, an improvement from the year-ago period. Notably, the company's Fox Complex (Ontario) had one of its best quarters in years with ~11,200 GEOs produced at all-in sustaining costs [AISC] of $1,288/oz. This was a meaningful step in the right direction, with the higher production profile helping to leverage fixed costs. In addition, it was despite lower grades of ~3.19 grams per tonne gold (driven entirely by throughput), with grades expected to tick up in Q4, albeit helped by relatively low sustaining capital spend in the period. Unfortunately, this was offset by another high-cost quarter at its Gold Bar Mine (Nevada) with relatively low production, plus lower grades at San Jose (49% ownership, Argentina), resulting in only an 8% increase in consolidated output year-over-year.

McEwen Mining - Quarterly Production by Mine - Company Filings, Author's Chart

{kind=link}

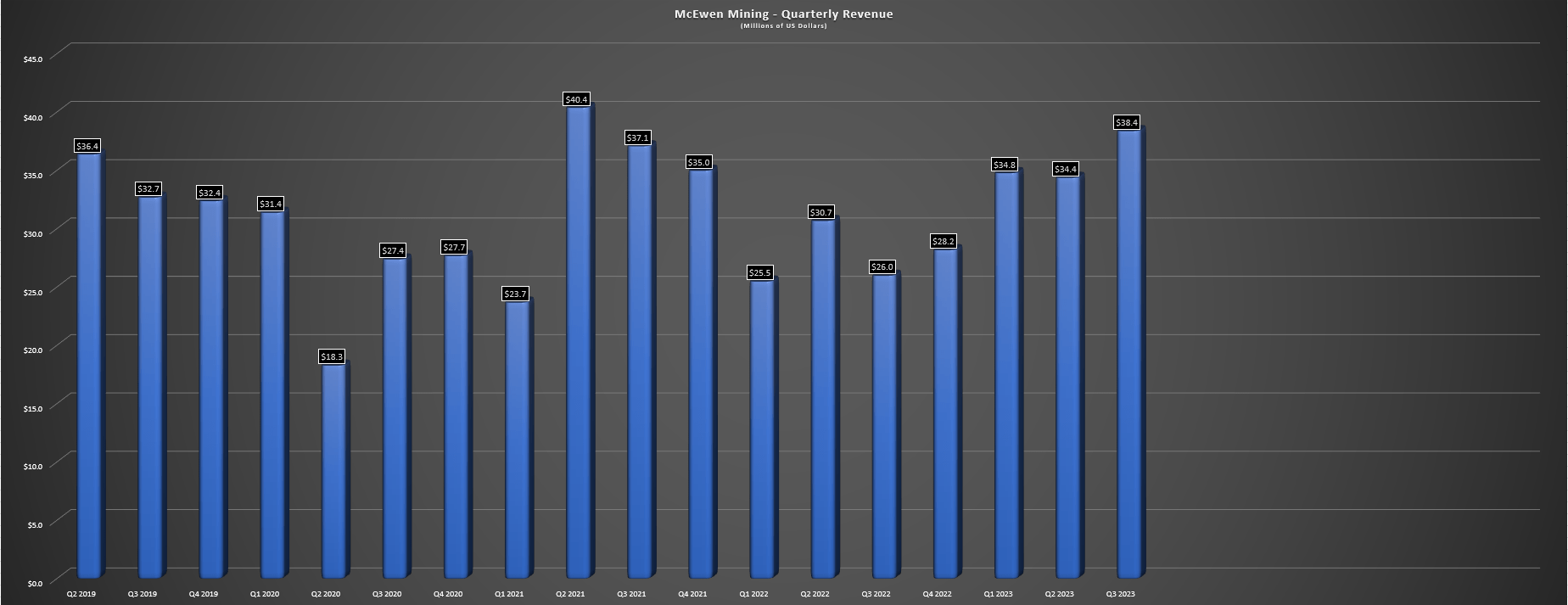

Digging into McEwen's other 100% owned operation, Gold Bar reported production of ~9,500 GEOs at industry-lagging costs of $2,160/oz which was partially related to higher sustaining capital spend (heap-leach pad expansion). On a positive note, mining rates improved with a new mine contractor on site, and the heap leach expansion was mostly completed in Q3, with the company just waiting for the final permits allowing for application of solution that are expected this quarter. That being said, while Q3 revenue was higher at $38.4 million, McEwen Mining's margins remain well below the industry average, even if costs were abnormally high in Q3 at its Gold Bar Mine.

McEwen Mining - Quarterly Revenue - Company Filings, Author's Chart

{kind=link}

On a positive note, the better production results at Gold Bar have carried over into Q4, with Gold Bar's quarter-to-date (November + December) production coming in at ~11,400 GEOs, which would represent the best quarter for the mine since Q2 2021 (~14,100 GEOs) if this pace keeps up. This higher production should help pick up the slack for the Fox Complex and San Jose, where production has been softer sequentially (~18,500 GEOs combined quarter-to-date vs. ~29,000 GEOs in Q3 2023). Unfortunately, the company is still tracking to the low end of its FY2023 guidance range (150,000 to 170,000 GEOs) despite the strong finish at Gold Bar, with McEwen Mining noting that production is expected to come in near 154,000 GEOs for the full year.

Costs & Margins

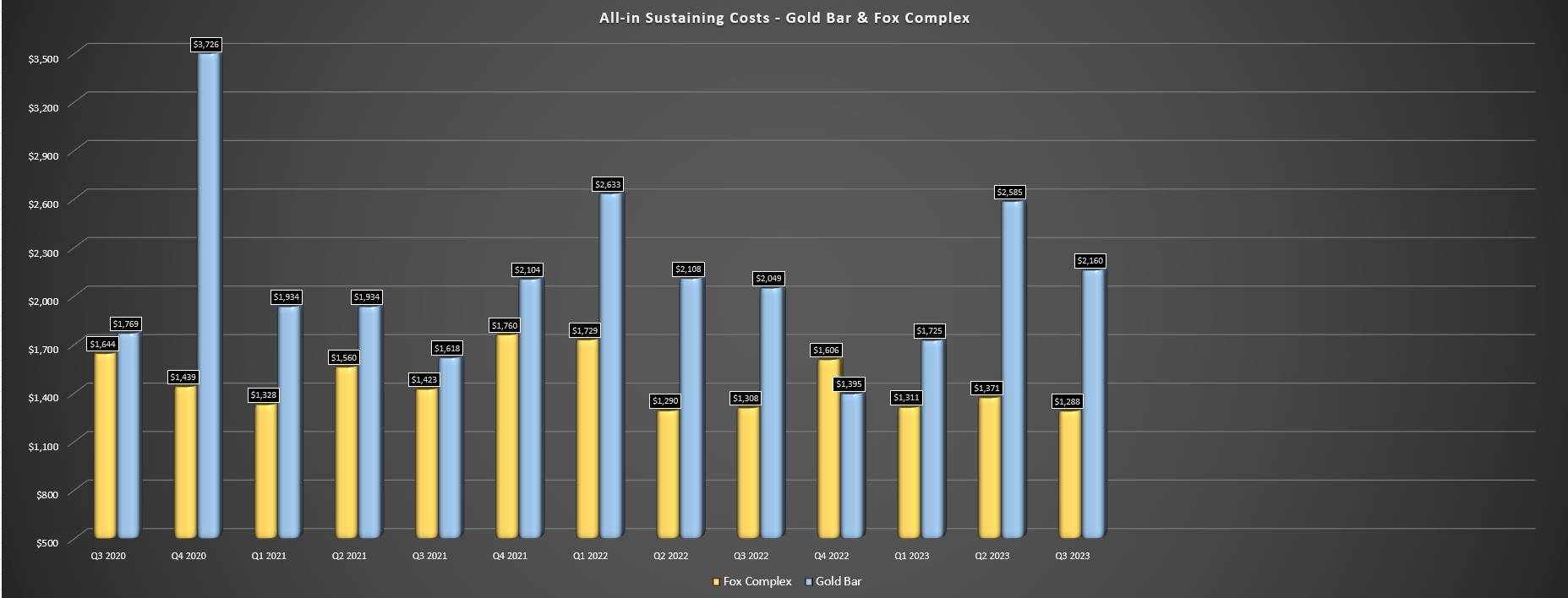

Moving over to costs and margins, the better performance at Fox was encouraging in Q3 (down 2% year-over-year to $1,288/oz), but consistently high AISC at its Nevada mine has overshadowed the improving performance at the Fox Complex. And while Gold Bar's costs could improve to sub $1,900/oz AISC with the benefit of higher production/sales, this still doesn't do much from a free cash flow standpoint for the company. Hence, it wasn't surprising to see the company raise additional capital earlier this month with ~1.9 million flow-through shares sold, translating to nearly 4% share dilution. And this is one reason I dislike owning high-cost producers like McEwen Mining and Endeavour Silver ( EXK ) because they're often continuing to dilute shareholders even in periods of metals price strength as they need a sustained period of significantly higher metals prices to improve their balance sheet.

Gold Bar & Fox Complex Quarterly AISC - Company Filings, Author's Chart

{kind=link}

Finally, while many investors point to MUX having a significant upside, given that it remains over 70% from its 2016 highs, this is largely explained by share dilution and margins. As the chart below shows, AISC is up over 60% in the period with minimal benefit from higher metals prices, and the company has diluted shareholders, with its share count up 65% since 2016 following the recent raise. This has led to a significant decline in production per share, and I don't have much confidence in Gold Bar or San Jose extending their mine lives past 2027 without much higher metals prices, suggesting that McEwen Mining may need to make an acquisition to grow production from current levels, which would lead to further share dilution. Let's look at the stock's valuation to see whether its position as a high-cost producer with a low weighted average mine life is being priced in at these levels.

McEwen Mining - Annual AISC, FY2023 YTD & Average Gold Price - Company Filings, Author's Chart

{kind=link}

Valuation

Based on ~51 million fully diluted shares (excluding warrants) and a share price of US$8.10, McEwen Mining trades at a market cap of ~$415 million. This leaves it as one of the lower capitalization producers in the precious metals space, behind other junior producers like Karora Resources (KRRGF) and Orla Mining (ORLA), but ahead of more beaten-up names like Jaguar Mining (JAGGF), and Americas Gold and Silver (USAS). However, McEwen Mining is unusual because it has a massive development-stage copper project on the side (Los Azules), and with investments from much larger companies like Stellantis (STLA) and Rio Tinto (RIO), we have seen the market put some value on this asset following its creation of McEwen Copper vs. lying dormant in the MUX portfolio with little value ascribed to it for years. In fact, the most recent financing round placed a value on McEwen Copper of ~$800 million, with MUX owning 47.7% of McEwen Copper.

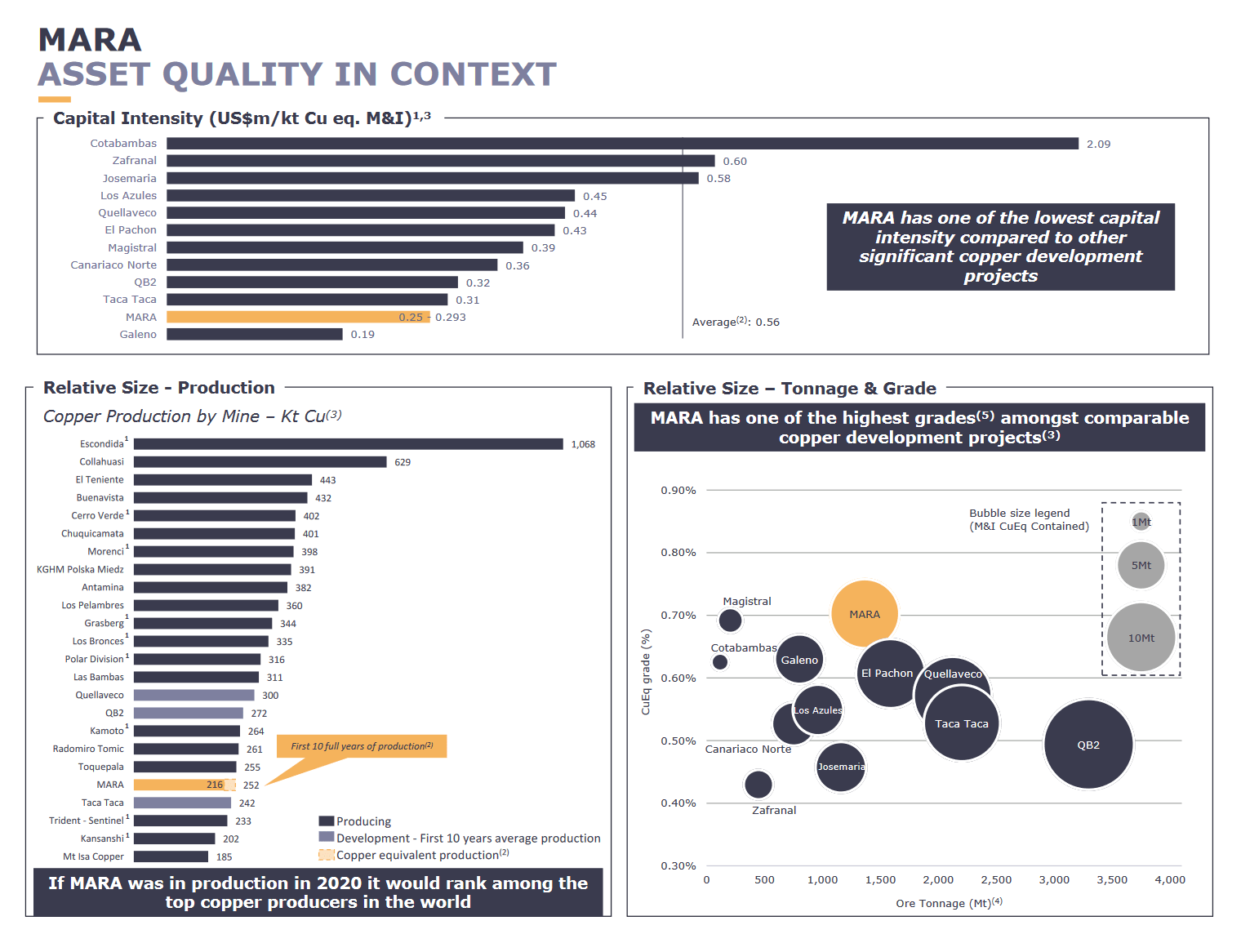

MARA Project vs. Other Undeveloped Copper Projects - Yamana Investor Day

{kind=link}

Given this change in the thesis with value being surfaced outside of its precious metals assets, the best way to value McEwen Mining is on a sum-of-the-parts basis, and I believe a more conservative valuation for Los Azules is ~$285 million [$5.60 per share] which is based on the mid-point NPV (8%) on the Los Azules PEA and a similar multiple to what Glencore (GLCNF) paid for MARA, a more advanced project in the Catamarca province of Argentina, with it also being a larger project. And if we assign $200 million [US$3.90] to the rest of its portfolio made up of low-margin precious metals mines, royalties, and its Elder Creek interest, I see a fair value for the stock of US$9.50, translating to a 17% upside from current levels.

However, I am looking for a minimum 40% discount to fair value when it comes to small-cap cyclical stocks, and ideally closer to 50% for high-cost producers that are more sensitive to the gold price. So, even if we use the low end of this required discount range to ensure an adequate margin of safety, MUX's ideal buy zone comes in at US$5.70. Plus, I continue to see far better reward/risk bets elsewhere in the sector that control their own destiny, such as Argonaut Gold (ARNGF) which trades at a lower market cap with a much larger production profile, and with the previous CEO of Teranga Gold at its helm that led the small-cap gold sector in per share growth in his tenure. Hence, if I was looking to put capital to work, I think Argonaut Gold has a far more attractive setup than McEwen Mining.

Summary

McEwen Mining will report a better Q4 with quarter-to-date production of ~29,600 GEOs, but it will still deliver into the low end of annual guidance, and costs will once again be well above the industry average (~$1,800/oz vs. FY2023 industry average estimate of ~$1,380/oz). Meanwhile, although Los Azules is certainly making progress, the project still has a long way to go before a development decision, making it hard to assign over $300 million to MUX's share of the project today. Finally, the company has two short life assets in San Jose (49%) and Gold Bar, giving McEwen Mining a much lower weighted-average mine life than its peers, and while MUX's revenue is growing, it's still struggling to generate any free cash flow. In summary, while a rising tide (gold price) could certainly lift all boats, I think there are far better ways to get exposure to gold.

For further details see:

McEwen Mining: Tracking To Low End Of 2023 Guidance