VZ - Medical Properties Trust: A Cautionary Tale On Reaching For Yield

2024-01-08 11:44:20 ET

Summary

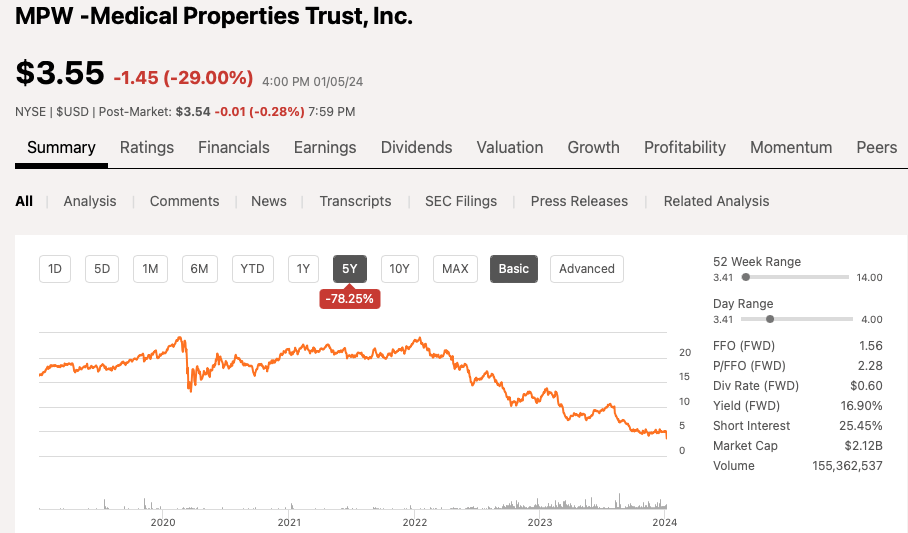

- Medical Properties Trust shares fell 29% on Jan. 5, resulting in a total return of -45.6% over the past 53 weeks.

- There were 82 free site articles written on MPW in 2022, with the majority being "buy" or "strong buy" recommendations.

- The cottage industry of high yield dividend stock investing has attracted retirees looking for higher returns, but it may have underrepresented the risks involved.

On Friday, January 5, 2024, shares of Medical Properties Trust ( MPW ) fell another 29%, closing at $3.55. Over the past five years, including $5.18 in cumulative dividends, if you owned MPW shares from January 1, 2019 - January 5, 2024, your total return is -45.6%. On a three year basis, January 1, 2021 - January 5, 2024, your total return is -61.1% and your five year return is -69.7% (January 1, 2021 - January 5, 2024).

{kind=link}

Lo and behold, in 2022, there were 82 free site articles written on MPW. There were 70 "strong buy" or "buy" articles, 10 "hold" articles and two "sell" articles.

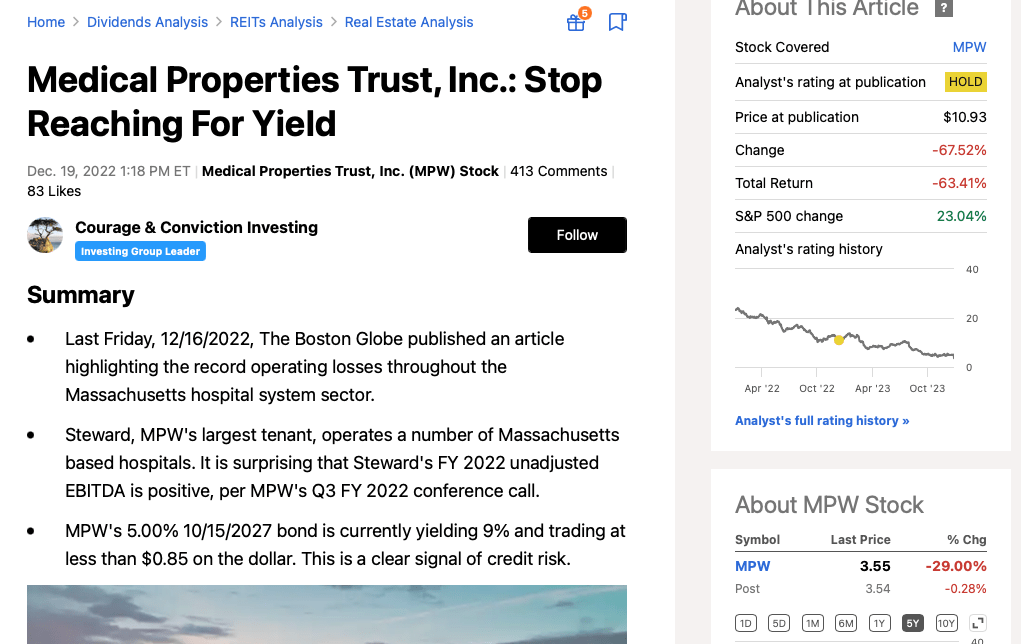

I was one of the authors who wrote on MPW, only one article in fact, when on December 19, 2022, I published Medical Properties Trust, Inc.: Stop Reaching For Yield . If you actually take the time to read my article, it reads bearishly and as a highly cautionary piece. That said, I'm not a short seller, and I rarely write "sell" rated articles. Moreover, let's face it, more often than not, it's harder to make thoughtful points and get your intended message across when it comes to these battleground stocks. The reason is there is too much emotion in the room, so to speak, often way too many strong opinions, and invariably too much groupthink. Unfortunately, the bear case or cautionary warnings seem to get lost or drowned out by the loud chorus of bulls, emphatically touting their reasons why these stocks are "money good," simply mis-understood, and a compelling situation that retirees can't pass up. The leading arguments are almost always pointing readers to the irresistibly attractiveness of dividend yields, with less emphasis on the risks and why the opportunities exist.

{kind=link}

Further, when it comes to articles on MPW, during the first half of 2023, there were 62 "buy" rated articles, 12 "hold" rated articles and five "sell" rated MPW articles. Finally, well after the horse left the barn and the stock clearly broke down, after when it became obvious the smoke was looking a lot more like fire, and during the second half of 2023, there were 24 "buy" rated MPW articles, 25 "hold" rated articles and 10 "sell" rated articles.

I'm still trying to work out is why on god's green earth there have more than two hundred articles been written on MPW (in 2022 and 2023)? Is MPW curing cancer or does MPW have the next AI chips? Of course not! So, again, what's the big appeal?

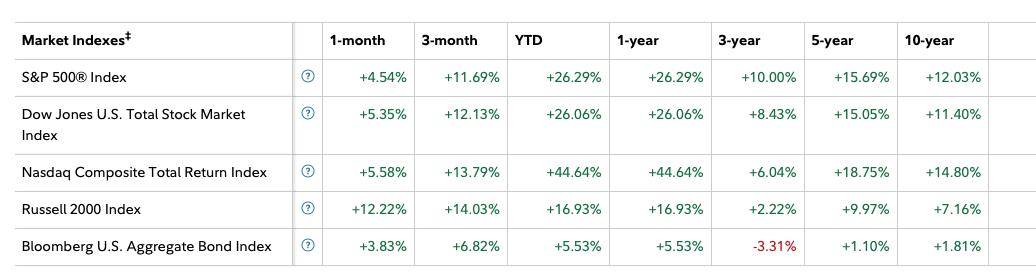

Nothing for nothing, last year the S&P 500 ( SPY ) returned 26.3%. On a three-year basis, buy and hold capital, invested in the S&P 500, compounded at 10% per year. And on a five-year basis, simply owning the S&P 500 has resulted in capital compounding at 15.7% per year. Moreover, the Nasdaq Composite ( QQQ ) did even better when comparing its one-year, three-year, and five-year returns.

{kind=link}

Over the next month or so, I'm guessing there could be upwards of a dozen new MPW articles. Some might say buy the dips whereas many might explain why MPW's stock got destroyed, and why, at least most likely, these are mostly likely permanent principal impairments on retiree's invested capital, as MPW's balance sheet is way too leveraged and the bearish case is playing out has played out nearly exactly as the sophisticated short sellers said it would, way back at $12 to $15 per share.

Why Is There A Cottage Industry Reaching/Chasing Yield?

Setting MPW completely aside, the much more important question that retirees need to reevaluate is why are these high-yield dividend stock investing strategies so popular? Secondly, retirees need to carefully and objectively evaluate whether they are getting any real alpha in these strategies. Honestly, over a one-year, three-year, or five-year period can anyone empirically point to these strategies beating the S&P 500?

Perhaps, driven by demographics or the Federal Reserve keeping interest rates way too low, for way too long, dating back from 2009 - 2022 or simply great marketing, there has been a cottage industry that has sprung up around 2020 surrounding this concept of building the perfect portfolio of high-yield equities. The messaging, at least on the surface, has been very persuasive, and filled with one sided pitches (what can go right), and arguably has under represented the risks or pitfalls to these strategies (what can go wrong).

The pitch goes something like this: You're in the your late 50s or early 60s or perhaps slightly older and you have $500K or maybe upward of $700K of investable capital, but definitely not $1 million (or more). Maybe you took early retirement, maybe you got laid off during the COVID job purge, or maybe you're so ready to retire. Or perhaps, you're already retired and occasionally have trouble sleeping at night, worrying about your finances. Chances are you own your house and cars for cash and most likely your children have left the nest, have jobs, as you did your best to nurture and encourage your children, making sure that they got their educations or pursued a trade/vocation, etc.

Although not having to make a mortgage payment or car payment means your cost of living is relatively low and perhaps you're counting down days until when you turn 65 and qualify for Medicare. Yes, $500K to $700K is a good chunk of money, yet from 2019 - 2021, high-quality investment grade bond yields were relatively unattractive, then only offering say 3% to 4% yields. Maybe taking Social Security early (or perhaps waiting until 67) and earning an incremental 4% on $500K is enough to live modestly, yet comfortably. That said, maybe you live in a high cost state where taxes are really high or perhaps you're helping other family members, etc. Alternatively, maybe you've always wanted to travel and want to enjoy your golden years, while you are still young and healthy. Who knows, everyone's story, personal financial situation, health, and family situation varies.

Now, along comes this new movement, this cottage industry of high-yield dividend stock investing. Glossy marketing messaging abound, highlighting this is proverbial hidden corner or unexploited section of the stock market. It's described as this magical Willy Wonka-esque Chocolate Factory offering a bountiful basket of juicy 7% to 10% yielding dividend stocks, perfectly ripe (meaning great and well curated securities selection / well underwritten) that can be plucked from the trees or sipped from these confectionary chocolate streams. If you build a portfolio of say 35 to 40 different stocks, the messaging goes, at purportedly, you have ample downside protection from an unexpected blow up on perhaps only one or two of these companies. This diversification is expressly designed to give people comfort that their principal is "money good," well guarded, and well protected.

Next, the messaging is don't worry about any (temporary) drawdown of the overall portfolio's principal. Instead, just sit back, relax, and let the dividend checks roll into your account. No longer do you need your finger on the pulse of markets, no longer do you have to worry about a stock market drawdown, a recession, interest rate risk, etc. After all, you bought the cow for the milk (the dividends).

This all sounds great and it's understandable why retirees might easily have become intoxicated, swept away with by these juicy yields on the front end, during the initial honeymoon period. On portfolio of $500K, earning a blended and average 8%, or $40k per year, seems a heck of a lot better than earning a blended 4%, or only 20K per year, via a portfolio of "money good" and high-quality investment grade bonds or perhaps high quality collection of Blue Chips such as Procter & Gamble ( PG ), Kimberly Clark ( KMB ), PepsiCo, Inc. ( PEP ), The Hershey Company ( HSY ), The Coca-Cola Company ( KO ), or perhaps even taking a little risk and sprinkling in a Verizon Communications Inc. ( VZ ) or AT&T Inc. ( T ).

The real question, though, and what retirees need to objectively and smartly suss out is are these strategies right for them? Is their principal actually "money good?" Is the underwriting and portfolio selection process consistently thorough?

In the absence of having a high yield stock index, as a benchmark or barometer, for people to evaluate these strategies, there is a lot of guess work and unknowns.

Let's face it, outside of maybe the highly popular Vanguard Real Estate Index Fund ( VNQ ), with just north of $62 billion of assets, how can a retiree objective compare and understand if this high yield dividend stock strategy has been well vetted and successful?

This is a person's nest egg and financial future, there are no do overs. I'm not sure why people are taking these strategies, at face value, on faith. Save faith for the weekends and for religion. There's no place for blind faith when it comes to something as important as your retirement health and nest egg.

And by the way, the VNQ hasn't exactly done so well. At least not compared to the S&P 500. And if someone has an objective high-yield stock index, I'm all ears. In the absence of that, let's compare VNQ with the S&P 500.

VNQ's total compound annual returns:

- 1-year (2023): +11.4%

- 3-year (2021- 2023): 4.8%

- 5-year (2019 - 2023): 7%

S&P 500's total compound annual returns:

- 1-year (2023): +26.3%

- 3-year (2021- 2023): 10%

- 5-year (2019 - 2023): 15.7%

In case you're wondering, $500K compounded at 15.7%, over five years, is more than $1 million.

Moneychimp.com

$500K compounded, at 7%, over 5 years, is only $701K.

Moneychimp.com

Now, trust me, I get it that people will say the S&P 500's valuation is stretched, led by the Magnificent Seven (Meta Platforms, Inc. ( META ), Amazon.com, Inc. ( AMZN ), Apple Inc. ( AAPL ), Alphabet Inc. ( GOOGL ), Microsoft Corporation ( MSFT ), Nvidia Corporation ( NVDA ), and Tesla, Inc. ( TSLA )). Because these stock have done so well, people will say the S&P 500 is ahead of itself and those type of return won't be available over the next five years. There may be some truth to that. However, generally speaking, I've never met any great market timers, people that can consistently run between raindrops, and successfully for long periods of time.

Next, they might say - look - dividend stocks, even 7% to 10% yielding stocks have only gotten dinged as their relative attractiveness was greatly diminished by the opportunity to build 5% to 6% investment grade bond portfolios, as the Fed has raised its Fed Funds rate to 5.5%. Therefore, if the Fed ends up on a rate cutting campaign then these stocks are poised to rebound.

Maybe or maybe not!

The devil's in the details and every business and setup is different. What I've observed is there's often a good reason why these securities have these big dividend yields. At least anecdotally, many are highly leveraged. Are there diamonds in the rough? Yes - of course. Out of say 40 names, perhaps a small handful, bought after a big drawdown can generate strong returns.

Lastly, people might start pointing me to "Buying Hand Over Fist" or other similarly worded pieces expressly designed to make a splash and grab attention of people who are often too busy with life or distracted by other endeavors. In the world full of noise, bold proclamations are one way to get attention.

That said, if you're actually following these high-yield dividend stock strategies then this means you're nearly always fully invested as you want to maximize your current dividends and collect those dividend checks. Outside of not reinvesting the dividends, dividends that I thought that were earmarked for spending / enjoying life and having fun on, then where are all of these people getting this extra capital to be "Buying Hand Over Fist?"

Buying hand over fist implies betting big. Perhaps, taking a 3% sized bet to 10%. Only how can you do that if you're nearly fully invested? Either you follow and believe in these strategies or you don't, but again, there's no "Buying Hand Over Fist" money (or dry powder) to take advantage of these drawdowns that invariably seems to occur far more frequently than advertised.

The Alternative

As I learned a long time ago, back when I was a worker bee, a wee young grasshopper, working in the trenches of corporate America, I had a boss said "I love your analytical thinking, but please tell me how to build the house and not burn it down." Pointing out the flaws and weaknesses and why things should be different are great intellectually exercises, but mapping out a better way forward is what we need. Leaders that can actually build the house as opposed burn it down are far more valuable.

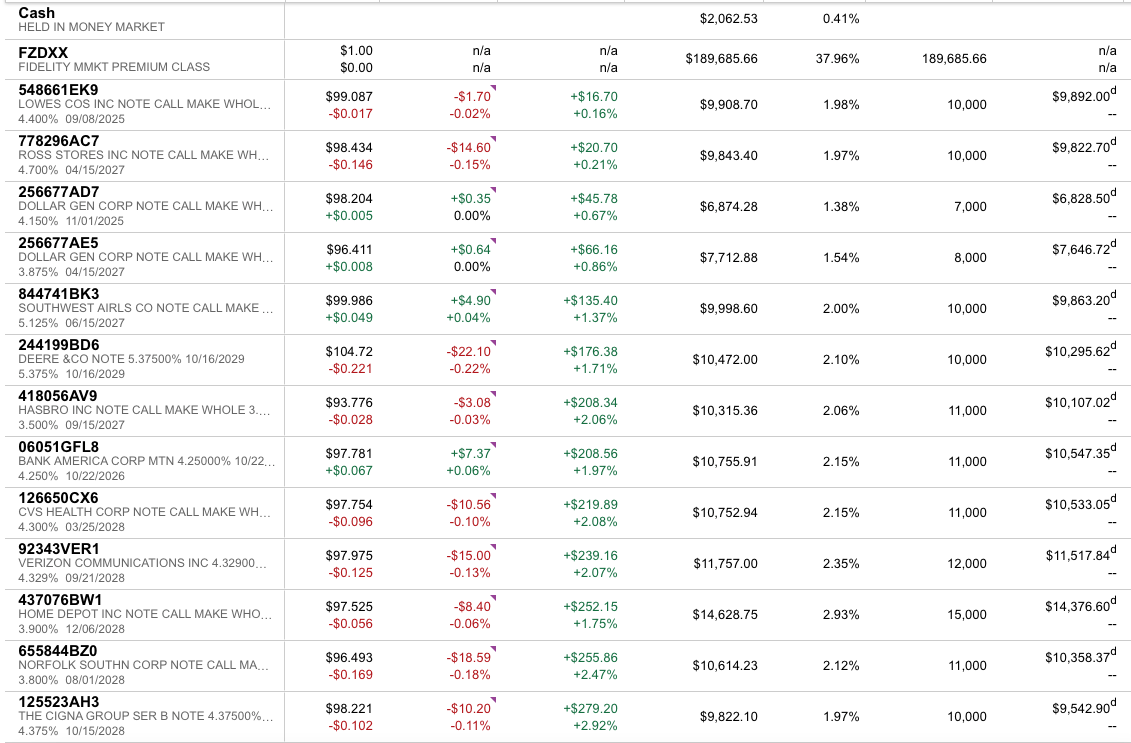

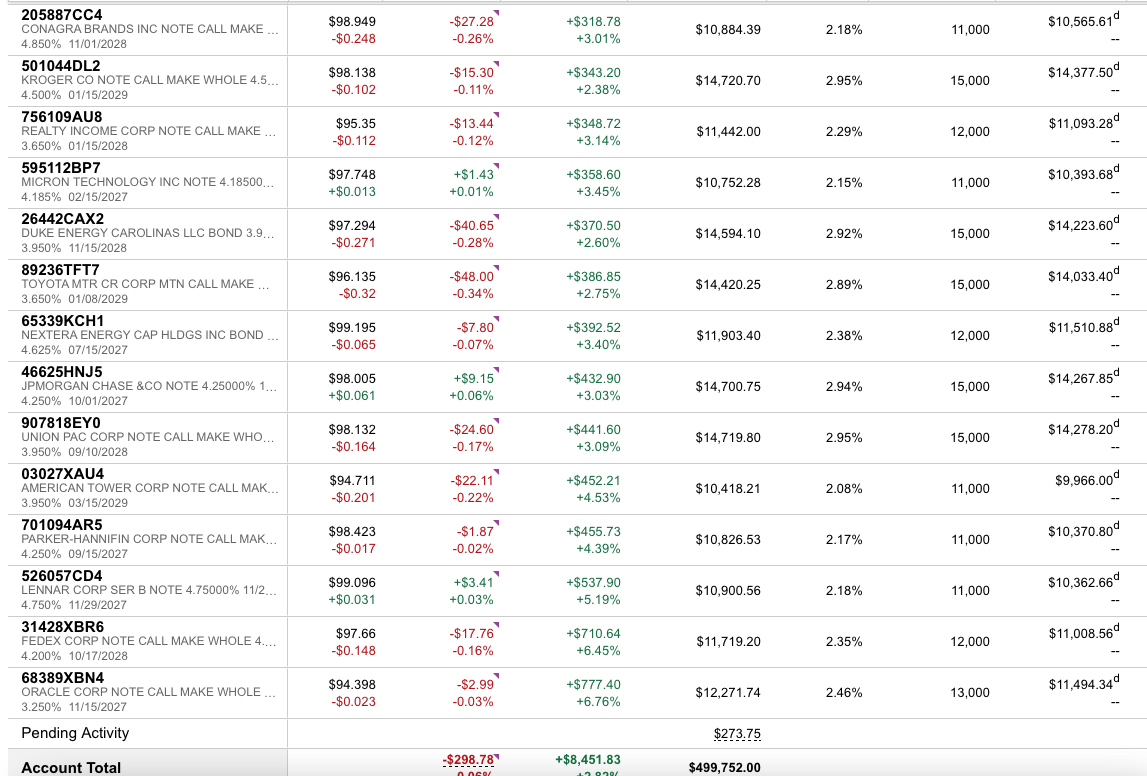

To that end, back on October 28, 2022, I penned this piece: My Gift To Retirees: Sharing My Recently Constructed $300K Investment Grade SWAN Portfolio .

Although I didn't get the peak of the interest rate cycle right, far from it, so far so good. Lo and behold, this portfolio owns all of the original bonds. The idea to buy and hold to maturity. And as you can see, every single bond has an unrealized long-term capital gain. No big drawdowns, no big surprises. The portfolio is spits off its semi-annual coupon payments and the principal is "money good." Just as I said it would be.

Moreover, similar investment grade bond opportunities exists, albeit at slightly less attractive all in yields to maturity.

{kind=link}

{kind=link}

{kind=link}

Putting It All Together

MPW's blow up should be a cautionary tale and a big wake up call for retirees. This event is a mini Enron type of shock, something that should lead to a product recall, just like if planes get grounded or consumer packaged goods get recalled. It's a good warning sign that reaching for yield is actually much harder than it seems and some of the purportedly highly attractive and "money good" equities really aren't at all suitable for retirees.

In life, there are "no shortcut" or easy ways to outsmart the market. There's much more to this game then gathering a list of stock that yield 8% to 10%-plus and then buying a basket of them because you need current income. Retirees really need a total return mindset. You've worked your entire life to build the principal and protecting it is equally important. And unless empirically proven otherwise, at least over the past five years, the S&P 500 has most likely blown the doors off the high-yield stock strategies. If anyone has any empirical evidence or an objective way to prove otherwise, I'm all ears.

Simply put, unless your timing is perfect, I would argue that in most cases, it's probably best for retirees to avoid these battleground and controversial / highly short high-yield stocks.

For further details see:

Medical Properties Trust: A Cautionary Tale On Reaching For Yield