WW - Medifast: Looking Attractively Valued Even Amidst Declining Fundamentals

2023-04-12 14:29:55 ET

Summary

- Medifast stock was truly exceptional, as it embodied the desirable traits of value, growth, and dividend stocks all in one.

- However, latest quarterly earnings were down around 10% YoY.

- The company is expected to have decreasing top and bottom lines in 2023 and is expected to slowly recover in 2024.

- Despite these points, MED, in my opinion, remains an attractive addition for investors seeking exposure in this segment.

Editor's note: Seeking Alpha is proud to welcome Financeflash Research as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Thesis

Medifast (MED) has a rich history in the weight loss management industry, and the business restructuring in 2016 breathed new life into the company.

By shifting its focus to its product Optavia, Medifast experienced tremendous revenue and income growth, while also honing in on its profitability. Consequently, the share price soared, until a dip in June 2021 caused a nearly 50% drop in value. Despite this setback, I firmly believe that Medifast's stock will regain its footing and surpass market expectations, thanks to its bright market outlook and superior balance sheet compared to its peers. Additionally, I believe the stock is currently undervalued, making it an attractive investment opportunity.

Business

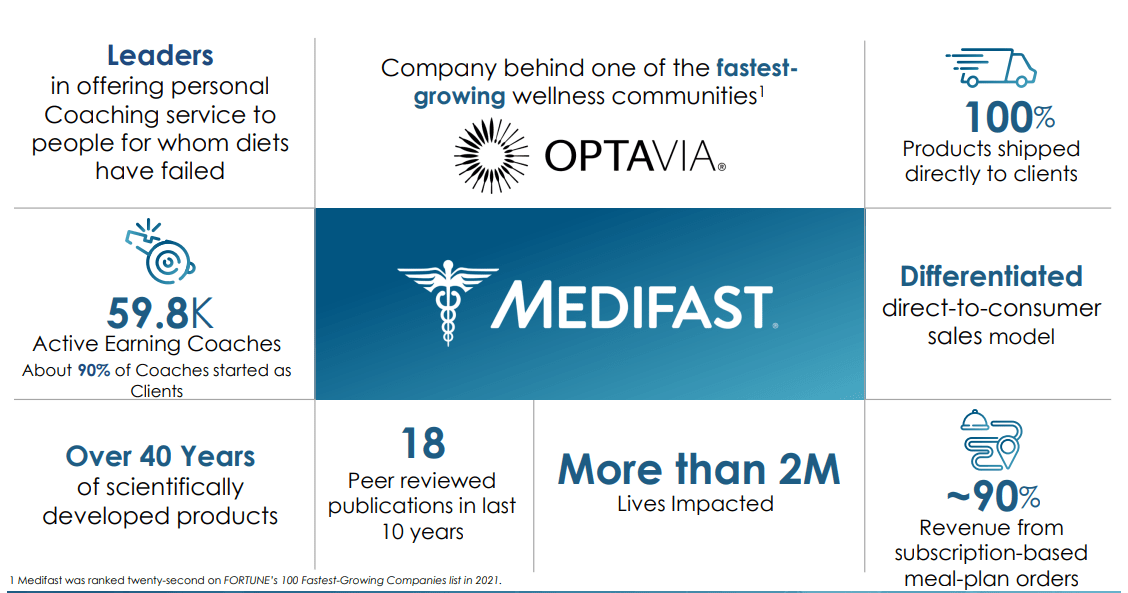

Medifast has a rich history spanning 40 years of providing healthy meal replacements for busy individuals seeking a better diet. The company has established a supportive community of coaches who help customers achieve their goals through the combined use of meal replacements and training plans.

{kind=link}

Optavia , formerly known as 'Take Shape For Life', has emerged as Medifast's primary growth driver in recent years, outpacing its competitors by offering scientifically-proven plans, meal replacements, diet products, and personal coaching support. Optavia aims to help clients create a sustainable healthy lifestyle rather than simply focusing on weight loss, which sets it apart from its peers.

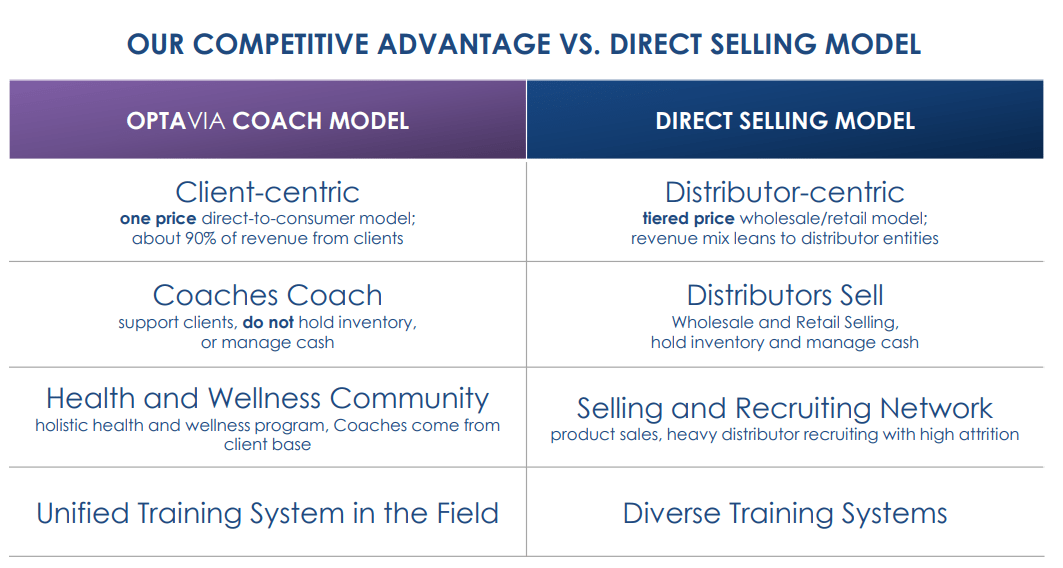

Optavia vs. Direct Selling Model (MED Investor Presentation Q1 2022)

{kind=link}

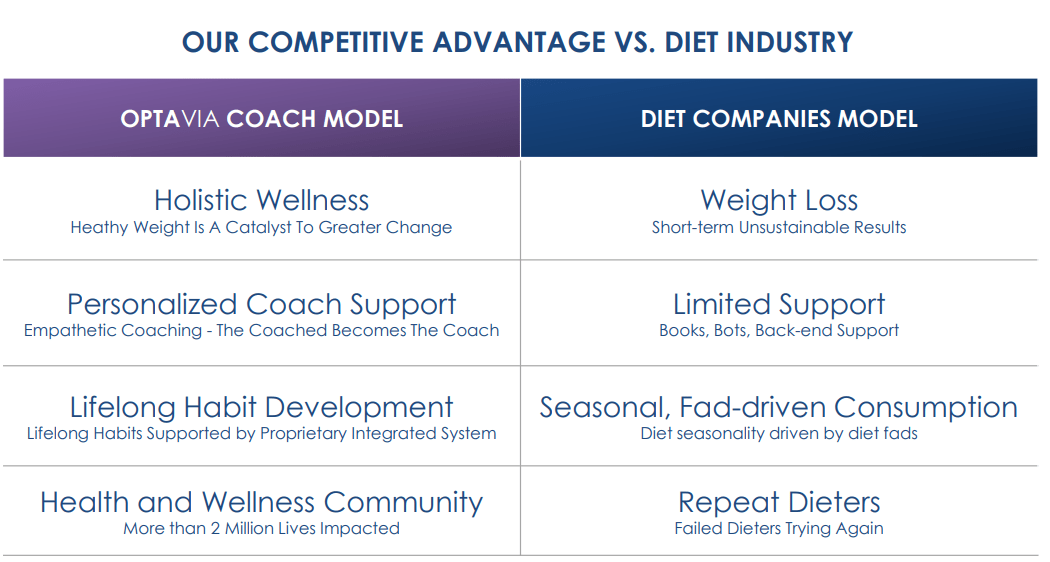

What makes Optavia unique is its independent coaches , who provide clients with education, encouragement, and inspiration to stay motivated and committed to their transformation. This community-based approach not only helps with weight loss but also addresses the clients' overall lifestyle, making the weight-loss sustainable. A truly noteworthy aspect is that 90% of Medifast's current coaches began their journey as clients. I think their deep satisfaction with the service led them to become fully invested in the company and even pursue a career with Medifast. In my view this advantage, coupled with a direct selling channel and recurring revenue from subscription-based products, gives Medifast an edge over its competitors and contributes to its market and peer outperformance. Medifast has already helped more than 2 million clients achieve their health goals, making it a leader in the weight-management industry.

Optavia vs. Diet Industry (MED Investor Presentation Q1 2022)

{kind=link}

Fundamentals And Outlook

Fundamentals

In my view, Medifast was a standout stock that exemplified a combination of exceptional growth and dividend metrics. Its track record for growth is nothing short of phenomenal. Between 2017 and 2021, Medifast saw a remarkable 455% increase in revenue, equating to an annual growth rate of 91%.

In 2022 alone, the company generated an impressive $1.6 billion in revenue, with Q1 2022 alone generating $417.6 million, a YoY growth of 22.6%. In Q4 2022 Medifast however experienced a YoY decline of 10.7% in quarterly revenues and a decrease in their total active OPTAVIA coaches on a sequential basis. The average revenue per active earning coach also fell by 12.4% YoY due to continued customer retention disruptions and softness in customer acquisition. This seems to be a trend that is expected to continue - at least for the next few months - as the forecast for Q1 2023 also wasn't positive, but more on this later. Nevertheless, I believe this is a short-term phenomenon due to the price increase of Optavia and the uncertain economic times leading to customers prioritizing their spending, which in turn negatively impacts Medifast's business due to the fact that less people are able to afford a healthier diet.

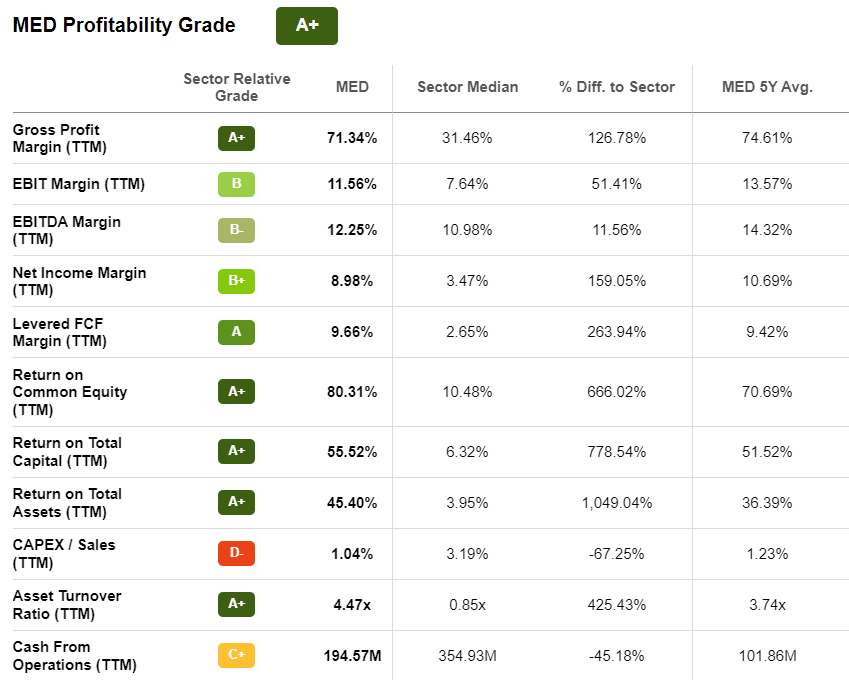

When it comes to profitability, Medifast's gross profit margin of 71% compared to the sector median of 31% , EBITDA margin of 12% vs. 10% sector median, and net income margin of nearly 9% vs. 4% sector median - all of this demonstrate the company's general proficiency at turning sales into profits.

However the margins over the last years have generally decreased.

In my opinion, this can also be attributed to the challenging macroeconomic environment, as we've seen a significant increase in production, raw material , and staffing costs from 2021 to 2023.

Medifast's remarkable return ratios are worth noting, as it boasts an impressive 84% return on equity, compared to a mere 11% among its peer group, and a 39% return on assets, which is significantly higher than the 4% achieved by its competitors. These ratios have shown a positive trend over the years, further demonstrating the company's strong financial performance.

In comparison to the sector median, Medifast's margin and return ratios are also outstanding, earning mostly grades between "A+" and "B" and an overall Profitability Grade of "A+" by the SA Quant rating system.

MED Profitability Rating (Seekingalpha.com)

{kind=link}

Medifast also currently offers an attractive dividend of $6.60. This results in a yield of currently 6.9% , paying out 45% of its net income, with a 5-year dividend growth rate of 33%.

Overall, Medifast's combination of high yield, substantial growth, and good dividend coverage make it an interesting investment opportunity at first glance.

Outlook

In Medifast's Q4 2022 earnings the management gave the following guidance for Q1 2023.

Revenue: $300-320 million, down around 28% from $417 million in Q1 2022

EPS: $1.75-2.40, down around 50% from $3.62 in Q1 2022

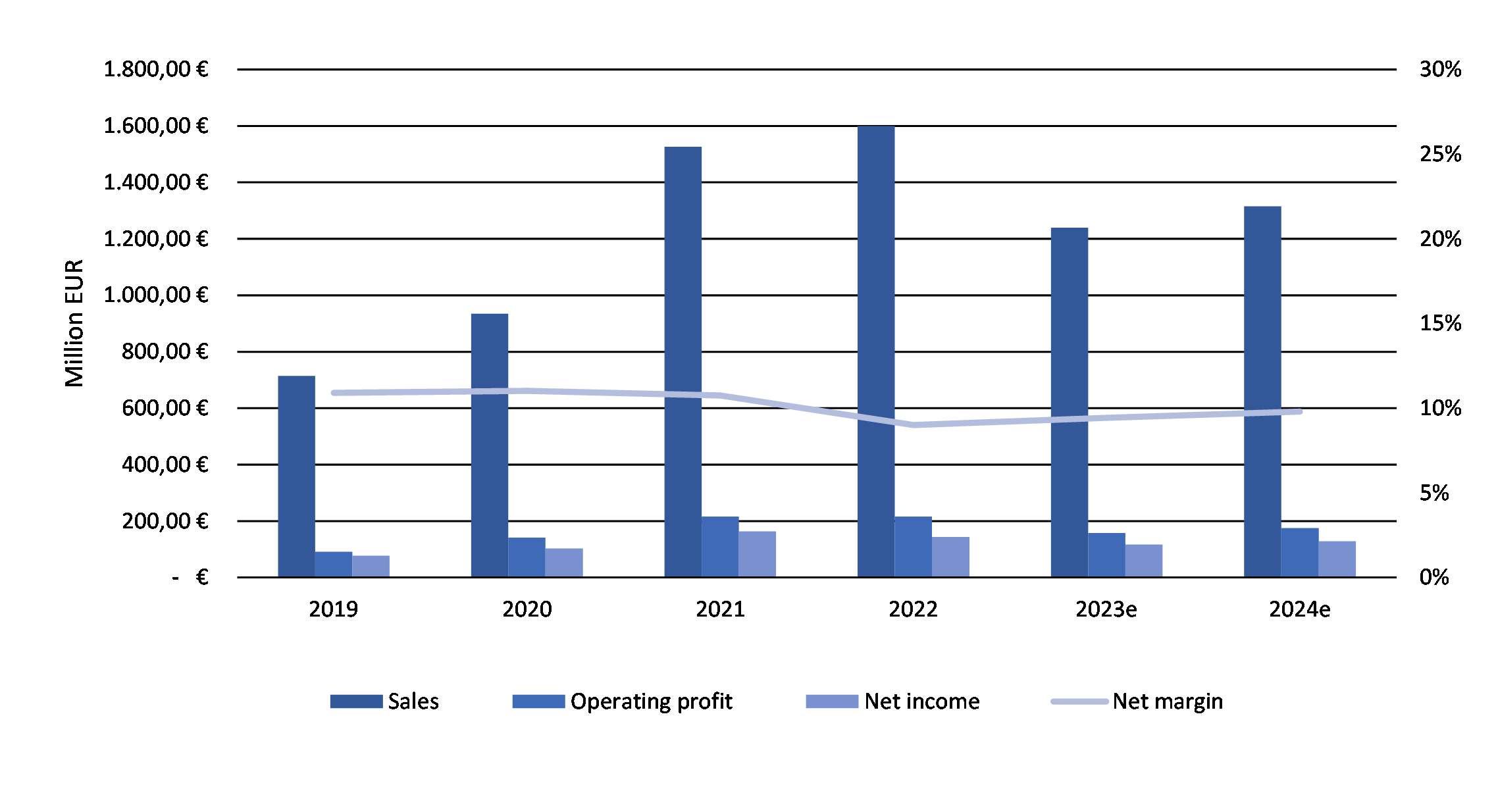

The management didn't specify any guidance for the remaining year 2023, which certainly indicates the uncertainty surrounding Medifast right now. The expected top and bottom lines for 2023 and 2024 in relation to MED's past performance can be seen below.

{kind=link}

Despite the declining business in Q4 2022 and the expected declines in 2023 and 2024, I believe the general market outlook for MED continues to look attractive.

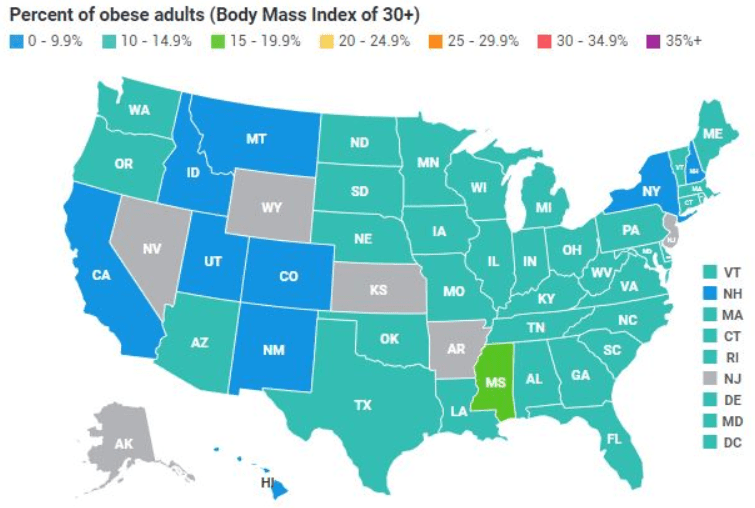

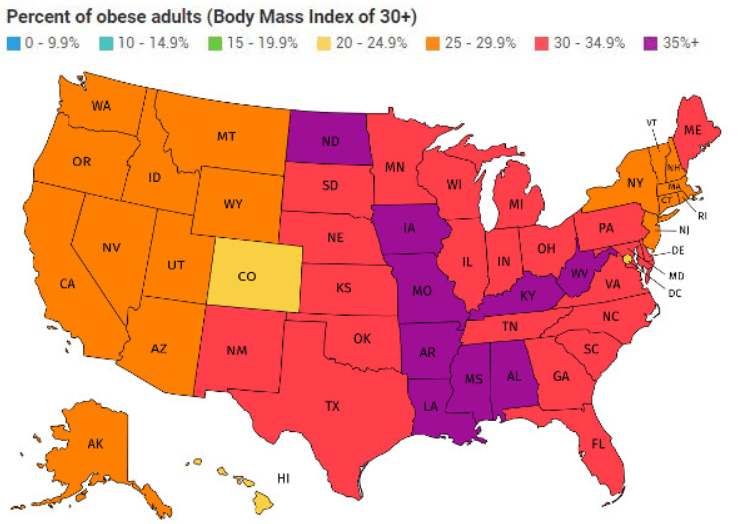

In the United States, Medifast's only market right now, currently roughly two out of three adults are overweight or obese, with 36% being obese right now. This ratio has more than doubled since 1980 and is expected to climb to nearly 50% by 2030, according to a Harvard study. This unfortunate trend is also evident in the following two pictures. The first depicts the obesity rate (BMI over 30) per US state in 1990, while the second portrays the obesity rates of every state in 2018.

Obesity Rates Per State 1990 (obesity.procon.org/us-obesity-levels-by-state/) Obesity Rates Per State 2018 (obesity.procon.org/us-obesity-levels-by-state/)

{kind=link}

{kind=link}

The consequences of obesity are severe and include a higher risk of developing diseases such as type 2 diabetes, high blood pressure, strokes, and certain types of cancer. In addition, obesity leads to an annual healthcare spending of $173 billion , and it is the most common reason for rejection by the military. Shockingly, at least 2.8 million people die each year due to obesity. This unfortunate development has the potential to be a significant catalyst for growth in the field of MED.

Despite its deadly consequences, obesity is often overlooked. However, we have seen a recent trend towards a healthier lifestyle with a greater work-life balance, healthier food options, and more emphasis on sports, especially during the pandemic. Governments, especially in Europe , are putting pressure on food producers to tackle the rising obesity rates. Moreover, the healthcare system is expected to support programs to prevent the obesity rate from rising further.

Medifast has conducted surveys that indicate a growing awareness of healthy habits and weight loss during the pandemic. With its superior financial situation, growth, and profitability, Medifast could be uniquely positioned to capitalize on this trend, since its system is built in a way that gives it a competitive advantage over its peers.

Industry And Competitive Analysis

Speaking of competition, major competitors of Medifast are USANA Health Sciences Inc. ( USNA ), Herbalife Nutrition Ltd. ( HLF ) and WW International Inc. ( WW ).

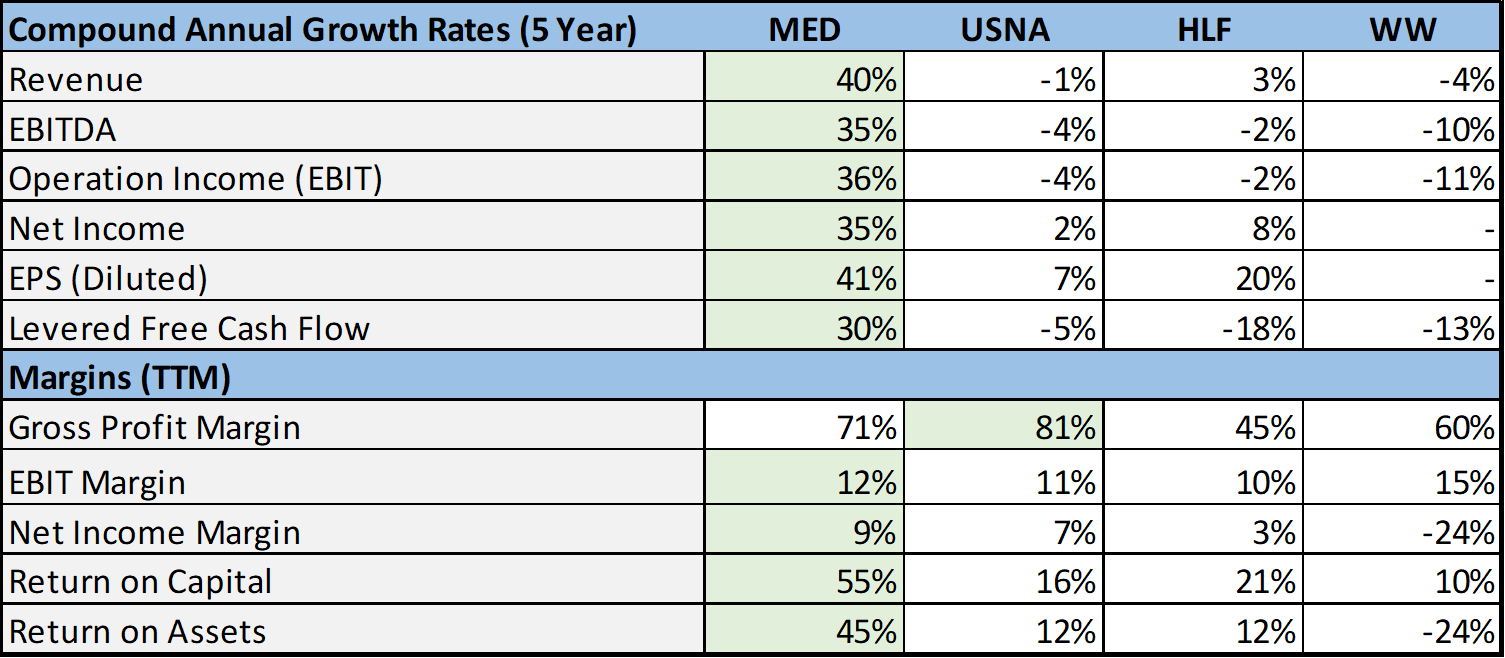

To further set these competitors in context, I created the following matrix with relevant metrics:

{kind=link}

Here, it's evident that Medifast stands tall as the fastest-growing and most profitable company. After the expected decline in MED's top and bottom line in 2023, I expect the company to get back to growing metrics in 2024. Based on the above mentioned outlook, I believe MED will be capable of achieving low double-digit growth over the next years. Additionally MED is the sole contender currently paying dividends. USANA Health Sciences is a close competitor regarding profitability. However, it's clear that Medifast reigns supreme, as it masterfully combines the best of all worlds, making it a true leader not just in its business model but also in its fundamentals.

Valuation

At first glance, Medifast seems to be undervalued, with its price to earnings of 9x or price to sales of 0.7 x - especially when considering the company's average growth rate of >30% in the last five years and the high profitability metrics compared to its peers.

Even after assessing the P/E ratios of Medifast's competitors, Medifast continues to shine as an attractively valued option. It's worth noting that HLF, trading at a P/E ratio of 5x, is lower quality than MED, which justifies HLF's current lower valuation, in my opinion. While USANA Health Sciences comes close to MED in terms of profitability, their inability to sustainably grow their business over the last five years raises questions as to why they're valued with such a discrepancy.

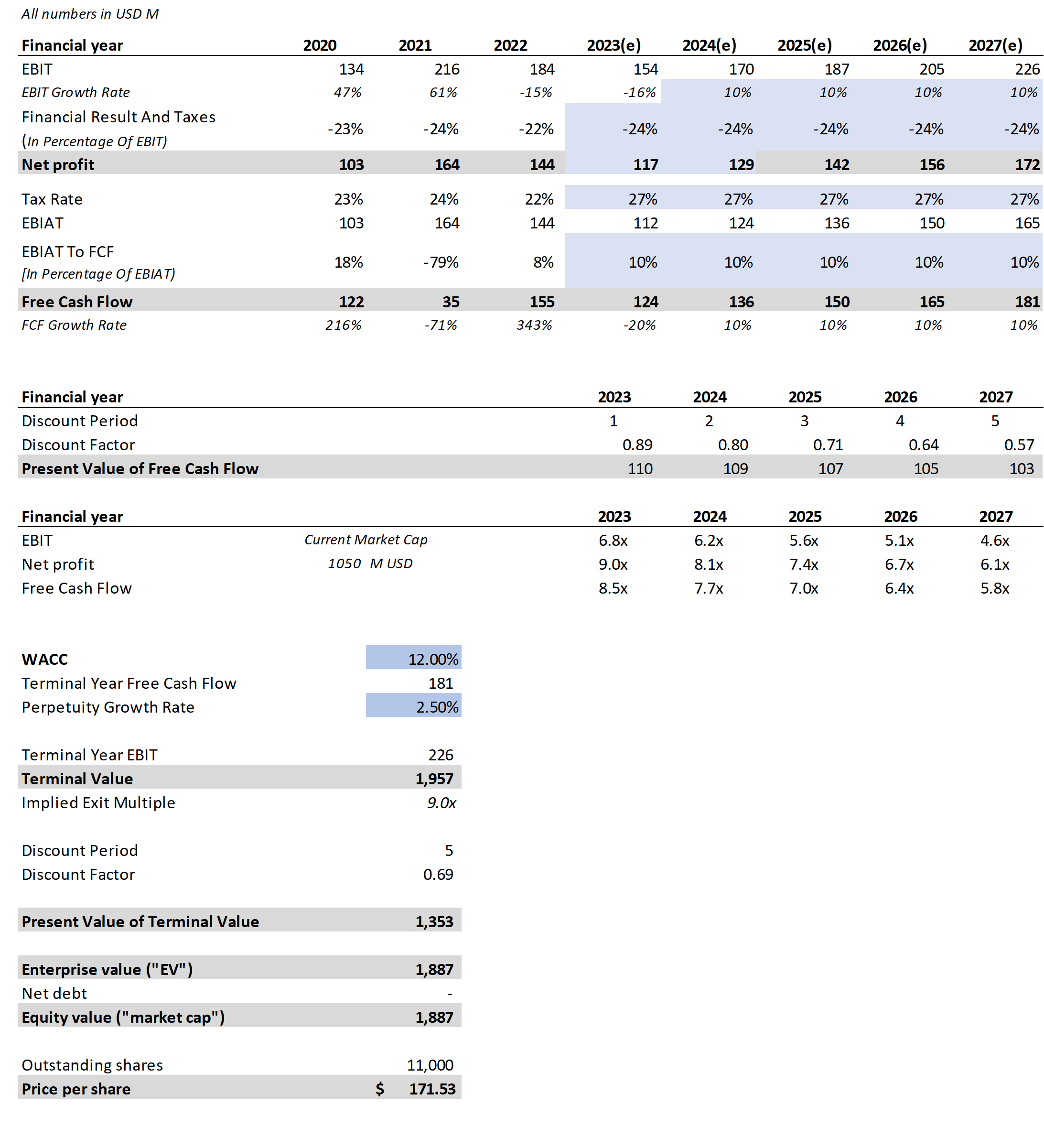

It's important to note that the aforementioned comparisons do not account for the potential challenges that Medifast may face in 2023 and 2024. As such, I have conducted a comprehensive Discounted Cash Flow Analysis ((DCF)). The blue cells in the analysis represent the assumptions made to evaluate MED. Here is a brief overview of how I calculated and predicted the future prospects:

- Net profit: By applying a conservative approach, I have forecasted a net profit of $117 million for 2023. To do so, I considered the lower end of the revenue guidance provided by management for Q1 2023, which amounts to $300 million. Based on this, I arrived at a total revenue estimate of $1.2 billion. Assuming a conservative net margin of 9.75% compared to the average margin of 10,7% over the last five years, my analysis projects a net profit of $117 million. For 2024 I predicted a net profit growth of 10% up to $129 million. This growth rate also seems reasonable compared to MED's five year average EBIT growth of around 30% . Both assumptions are also pretty much in line with the above mentioned expected fundamentals from Marketscreener.

- Financial Result And Taxes: I averaged the values of the last three years and therefore used 24% to calculate the EBIT and Net Profit for the years 2023 to 2027.

- EBIT: The EBIT for 2023 and 2024 was calculated with using the 24% Financial Result and Taxes and the predicted Net Profit mentioned above. From there on I assumed the 10% growth-rate for 2024 will persist until 2027.

- Tax Rate: Here I used 27%, the high end of management's Q1 2023 guidance.

- Free Cash Flow: Using the Tax Rate above, I calculated the EBIAT and afterwards tried to determine a suitable EBIAT to FCF ratio. In that case I think 10% seems reasonable, compared to 18% in 2020 and 8% in 2022.

- WACC: I assumed a, in my opinion conservative, WACC of 12% .

- Perpetuity Growth Rate: The perpetuity growth rate assumed for the analysis is 2.5%.

DCF Analysis Medifast (Data: seekingalpha.com; marketscreener.com )

{kind=link}

This analysis gives us a target share price of $171.53 . With considering this and assuming Medifast will grow like we anticipated here, Medifast's upside potential appears to be around 70%, suggesting it could be an attractive investment right now.

More Things To Like

No Debt

Medifast has a relatively low level of debt, making it a financially stable company. As of its most recent financial statements, the company reported a total debt of $26.1 million, which is significantly lower than its total equity of $588.5 million. MED's net debt is even negative, meaning they currently have more cash on hand than debt. This is a positive indication for investors, as a low debt level provides the company with more financial flexibility, allowing it to invest in future growth opportunities and weather any potential economic downturns. Overall, Medifast's low debt level is a testament to its sound financial management and responsible approach to managing its finances.

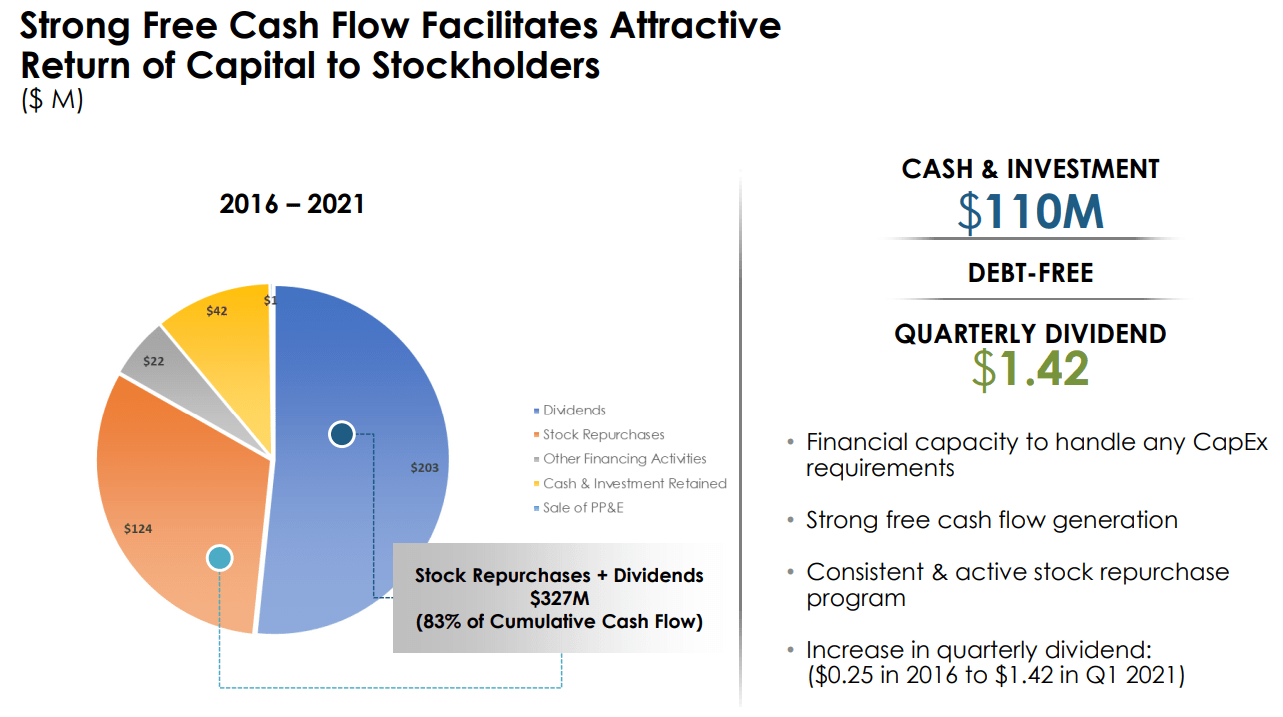

High Buybacks And Dividends

Medifast's management has proven to be highly investor-friendly, as evidenced by their previous use of capital. From 2016 to 2021 , 83% ($327 million) of free cash flow went towards returning value to shareholders.

{kind=link}

The majority of this was in the form of dividends ($203 million), with the rest used to buy back shares ($124 million). Since 2010, the company has bought back 3.1 million shares, equivalent to 21% of total outstanding shares. This demonstrates their commitment to enhancing shareholder value and maximizing returns.

Outstanding Business Model

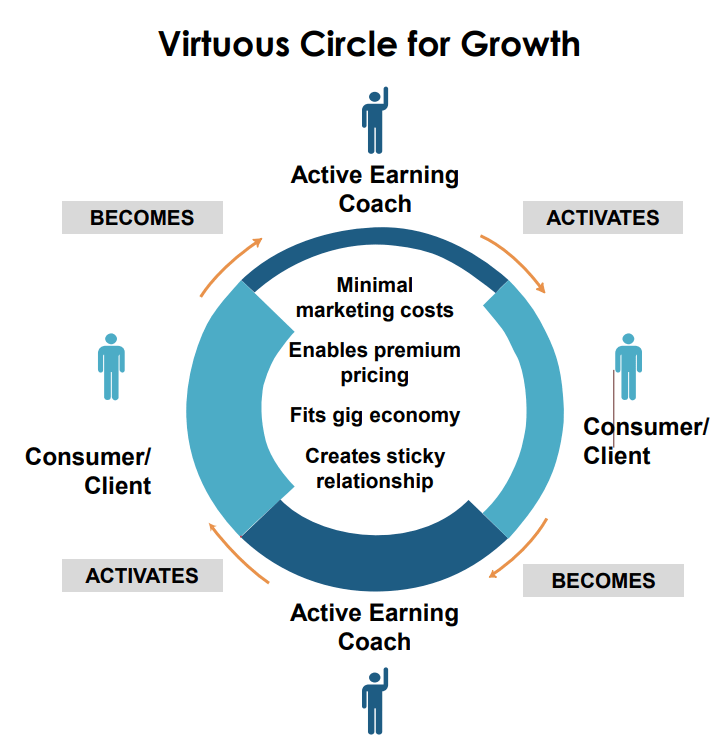

Medifast's business model is highly scalable, thanks to a virtuous cycle created when clients become coaches. This leads to automatic customer acquisitions and significant cost savings. As more clients become coaches, the company can experience exponential growth, with more coaches leading to more clients and vice versa. The company's latest investor presentation provides a good visualization of this cycle.

{kind=link}

Risks To Consider

Business Model

Medifast's business model is known as multi-level marketing ( MLM ), which involves coaches recruiting clients who, in turn, can recruit other coaches. MLM is often associated with negative connotations due to past and present illegal pyramid schemes . However, Medifast has addressed this issue in their latest annual report, stating that OPTAVIA Coaches do not handle or deliver merchandise to clients, and revenue is primarily derived from point-of-sale transactions executed over an e-commerce platform.

Public Opinion

Nowadays, with everything at our fingertips, it's easy to find reviews and test results for Optavia on various websites like US News Health. Currently, Optavia has received a mediocre rating of 3.6 out of 5 stars . Which isn't great but pretty solid if you ask me.

However, I find it strange that the main criticism of this diet is its difficulty to follow, as this is actually one of Optavia's core advantages according to Medifast.

While some reviewers claim that Optavia's diet isn't particularly healthy , most of the negative comments are due to the lack of long-term results. It's understandable that this is a concern for many, given that Optavia is a relatively new diet. However, I personally find it unlikely that Optavia's diet is worse than its competitors.

Nevertheless, it's worth noting that a shift in public opinion towards Optavia and, in turn, towards Medifast could have a negative impact on MED's fundamentals and ultimately, its stock price.

Mismanagement

One potential risk to consider for any company is mismanagement. However, Medifast's management has already successfully restructured the company in 2016 and has since multiplied its revenue and income. Therefore, I don't believe that mismanagement is something that investors need to seriously factor into their investment case, as long as the key personnel remain the same without major changes.

Conclusion

Investing in Medifast can offer an attractive opportunity for growth and profitability, as the company has demonstrated impressive double-digit growth and maintains a debt-free status, while also paying a generous dividend and actively buying back shares. Medifast's unique business model benefits from a network effect and favorable market conditions, as well as strong management, which inspires confidence in its future prospects. Medifast is currently rated as a "Hold" by Street analysts and by the Quant ratings:

seekingalpha.com/symbol/MED

I believe that one reason for this may be the current uncertainty that surrounds the stock. MED's management has refrained from providing any guidance for 2023 and has only "dared" to make predictions for Q1. While this highlights the uncertainty that MED faces, it is also important to consider the growth prospects of the overall market for MED. As consumers in the US become increasingly concerned about overweight issues, controlling weight through diet is becoming more important. This trend is expected to be the main driver of growth for MED in the coming years, and compared to its competitors, MED should be in the best position to benefit from it.

Given the undervaluation of Medifast compared to its peers and historical performance, I would therefore rate it as a ' Buy ' with the potential for higher total returns than the sector median. Even with decreasing top and bottom line in 2023 and 2024, the stock remains an attractive investment for investors seeking exposure in this (sadly) rapidly growing segment and at current prices this seems like a good opportunity to start a position in your long-term dividend growth portfolio.

For further details see:

Medifast: Looking Attractively Valued Even Amidst Declining Fundamentals