WW - Medifast: Strong Earnings But Guidance Disappoints

2023-05-12 07:46:54 ET

Summary

- Medifast's Q1 2023 EPS of $3.67 beats by $1.27 and revenue of $349M beats analysts' expectations by $29.5M.

- For Q2 2023, the company expects a ~25% decline in revenue and a ~50% decline in EPS.

- This, however, seems to already be priced into the current stock price, why MED, in my opinion, remains an attractive option.

Medifast (MED) declared their quarterly earnings on May 01, that's why we are revisiting MED to see if my 'Buy' rating from my last article remains intact.

Thesis

The change to placing their primary emphasis on the Optavia brand after their strategic pivot in 2016 has led to MED's impressive expansion. Recent developments, as seen in the performance of the company's revenue and stock price, suggest that this remarkable expansion may be slowing down.

Despite this setback, I think that Medifast's stock will recover and outperform market expectations because of its promising market outlook and stronger financial sheet than its competitors. The stock is also, in my opinion, now undervalued, which makes it a desirable investment option.

I won't go into detail regarding the business model, instead please see my other article on Medifast for a thorough introduction.

Fundamentals and Outlook

Having $1.5 billion in current trailing twelve months ((TTM)) revenue, Medifast recently released financial results. The company produced quarterly revenue of $349 million and an operating profit of $54 million, according to Medifast's most recent quarterly results report for the first quarter of 2023. Both the company's $3.67 GAAP EPS and $349 million in revenue were above market expectations by $29.5 million and $1.27, respectively.

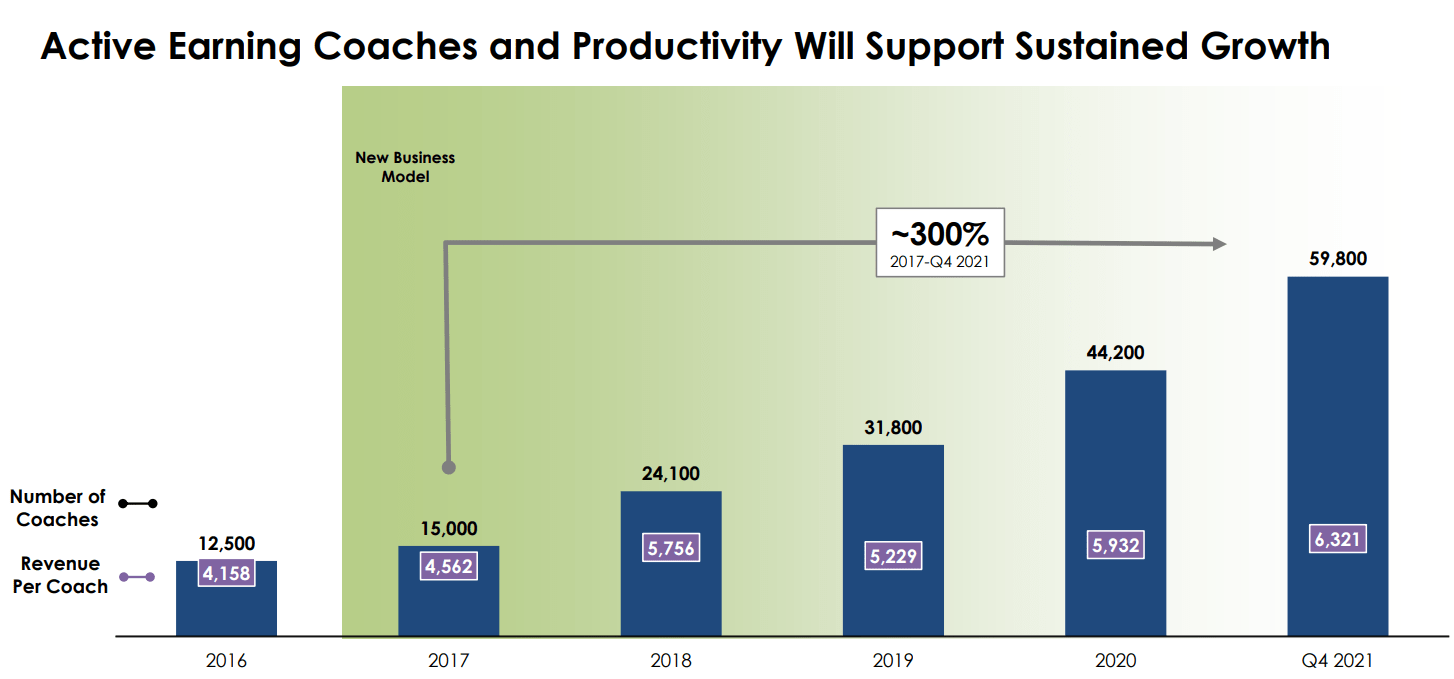

For Q1 2023, there are currently 58,700 active earning coaches with an average income of $5,945 each. While these numbers reflect a decline from the end of 2021, with income per coach down slightly by 6% from $6,300 and the number of active coaches falling by about 2% from 59,800, it is clear that these declines are quite small when seen in the perspective of the previous few years. This implies that despite these minor variations, Medifast's coaching network is still strong and resilient, continuing to contribute to the company's success:

Medifast Investor Presentation Q1 2022

{kind=link}

Looking at the TTM-EBITDA development, one can also notice the slight hiccup brought on by the general revenue decline:

When laying emphasize on the margin development of MED we, however, see another picture, with the EBITDA, Gross and Profit Margin increasing in the latest quarter:

This seems to be a step in the right direction and management seems to prepare for a potential economic downturn. In their latest earnings call , the management mentioned the following:

While we are not yet providing full year guidance for revenue and EPS, I want to remind everyone that we are continuing to use cost savings and efficiencies to fund strategic growth initiatives. The near-term cost savings action from the 15x25 objectives will be offset by approximately 240 basis points of customer acquisition investment in 2023 to get back on track with our growth initiatives.

I also like the fact that potential near-term savings will be reinvested in the customer acquisition.

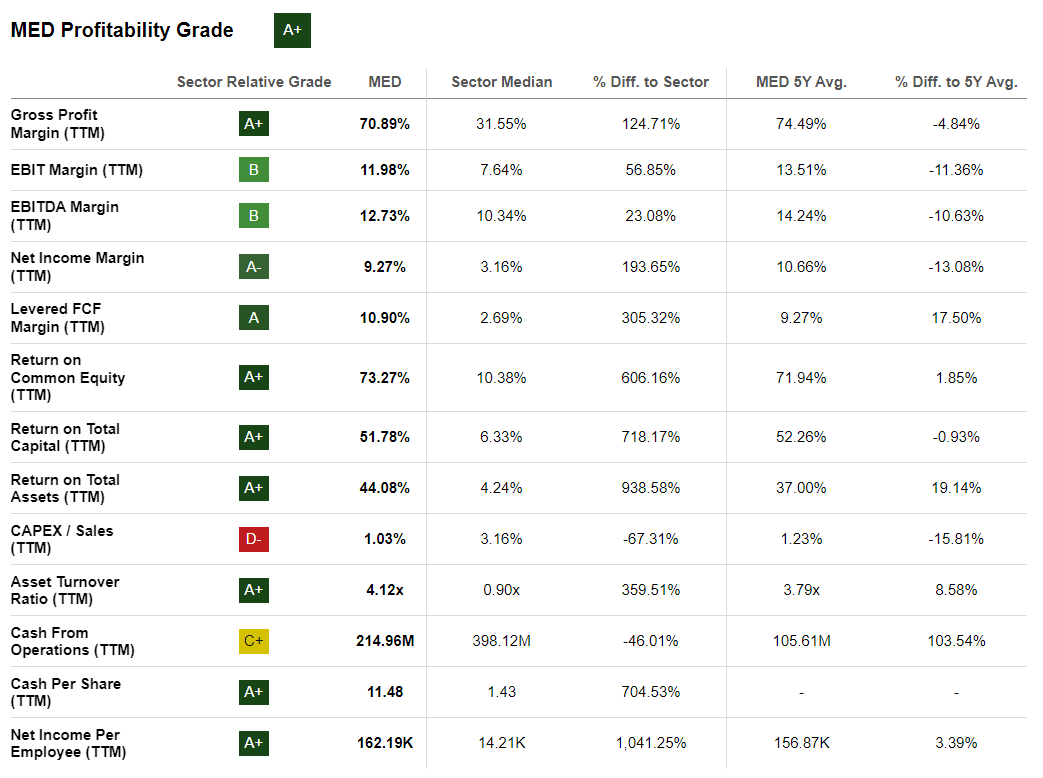

The small upwards tick can also be seen in the return ratios, which are now even more impressive with a Return on Assets of 41% , compared to a sector average of 4% and a Return on Equity of 86% compared to the sector standard of 11%.

In general, Medifast's overall Seeking Alpha Profitability Grade is currently at an "A+" further suggesting that MED is currently operating very efficiently:

{kind=link}

Medifast currently pays a quarterly dividend of $1.65, which was recently increased by 0.6% up from $1.60. While this increase is nothing to brag about, I think it still shows management's commitment to a growing or at least stable dividend, which in turn I as an investor am keen to see. This currently means a dividend yield of around 7.5% with a five year growth rate of 33%.

No Debt

Medifast is a financially sound business because of its low amount of debt. The business's total debt as of its most recent financial filings was $26.1 million, which is a lot less than its $588.5 million total equity. Since MED's net debt is actually negative, they actually have more cash on hand than debt at the moment. In fact, they even "decreased" their net debt to negative $99.4 million from negative $61.6 million in the end of 2022. A low debt level gives the company more financial flexibility, enabling it to invest in potential future growth prospects and weather any prospective economic downturns. This is good news for investors. Overall, Medifast's low level of debt is evidence of its strong financial management and careful handling of company finances.

Outlook

Medifast has presented its projected financial results for the second quarter of 2023. Revenue is expected to be between $250 million and $270 million, which is less than the $313.20 million expert estimate. In addition, Medifast anticipates diluted EPS to be between $1.32 and $1.44, behind the $2.82 estimate.

Like last quarter , the management didn't gave any guidance for the full year of 2023. This was justified as follows :

Turning to our guidance. While we are pleased with first quarter results that are ahead of our guidance, the operating environment remains challenging, and we continue to expect that programming changes, compensation dynamics and future growth initiatives will take time to gain traction and deliver meaningful results. It is too early to assess how our recent initiatives to drive customer acquisition will do over the coming quarters.

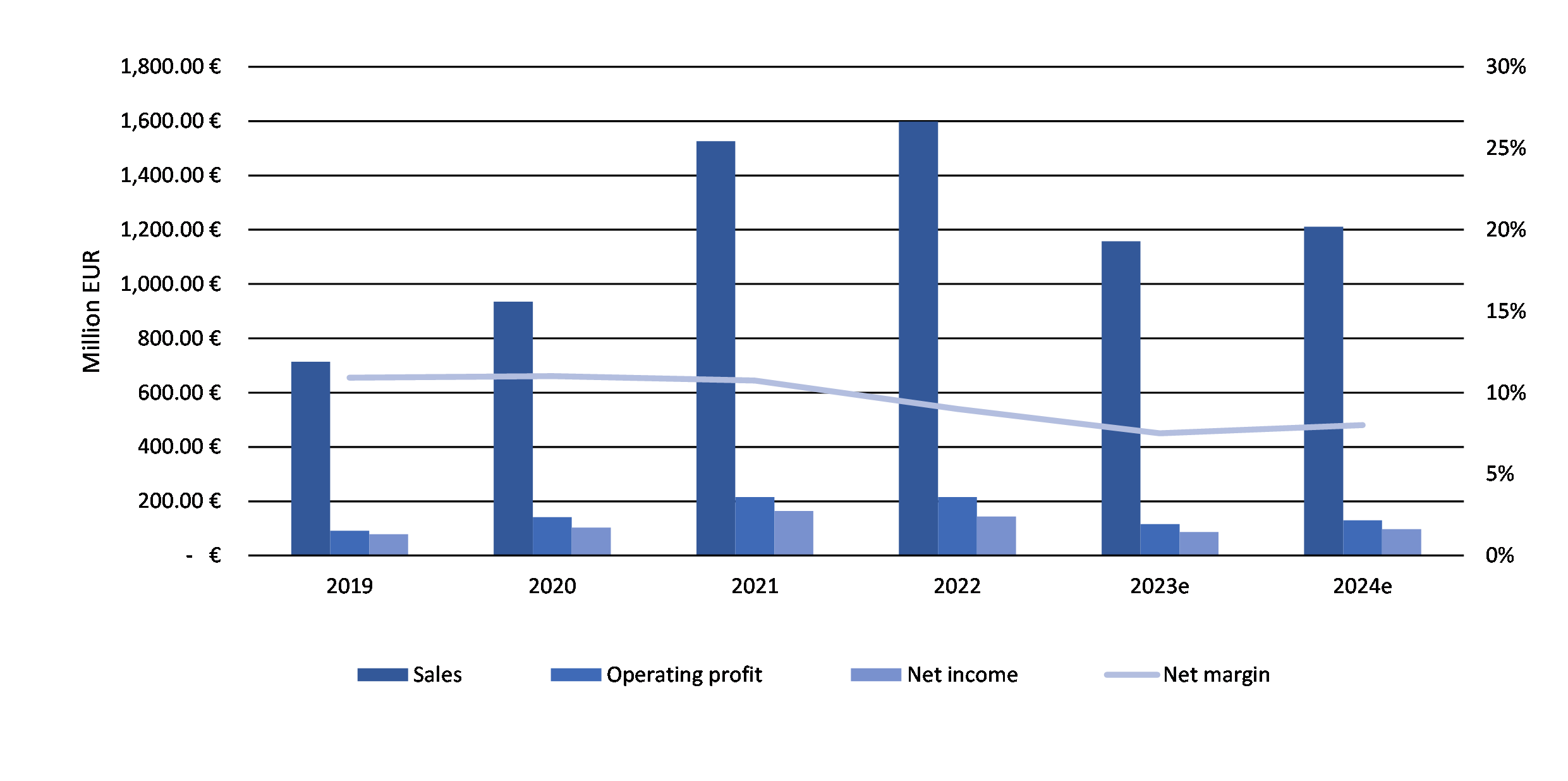

Medifast's development in revenue, operating profit, net income and net margin as well as the expected values for 2023 and 2024 can be seen here:

{kind=link}

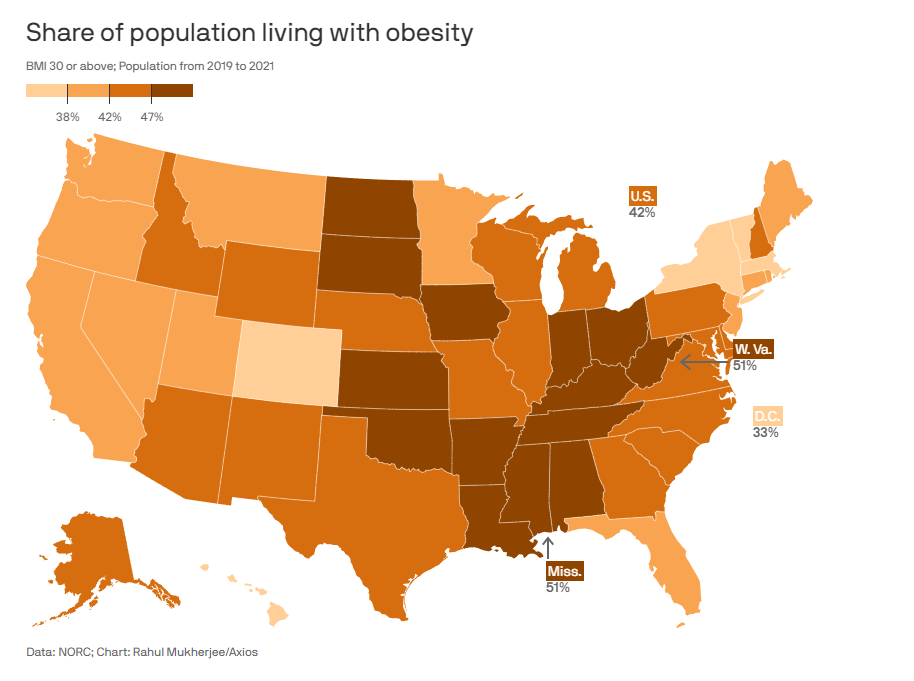

As already stated in my last article, the overall growing obesity in the US is in fact growing Medifast's TAM - once again for more detail please refer to my previous article.

In short, currently around 42% of the US population is obese and should therefore consider changing their food choices and lifestyle. This trend as well as the general awareness for this issue is growing globally, which could in turn fuel sales for companies like Medifast.

Obesity Rate In The US (www.axios.com/2023/03/23/norc-share-americans-obesity)

{kind=link}

Industry And Competitive Analysis

Major competitors for Medifast are USANA Health Sciences, Inc. ( USNA ), Herbalife Ltd. ( HLF ) and WW International, Inc ( WW ). As can be seen the whole segment is currently in a downtrend, with MED, in my opinion, looking the strongest right now.

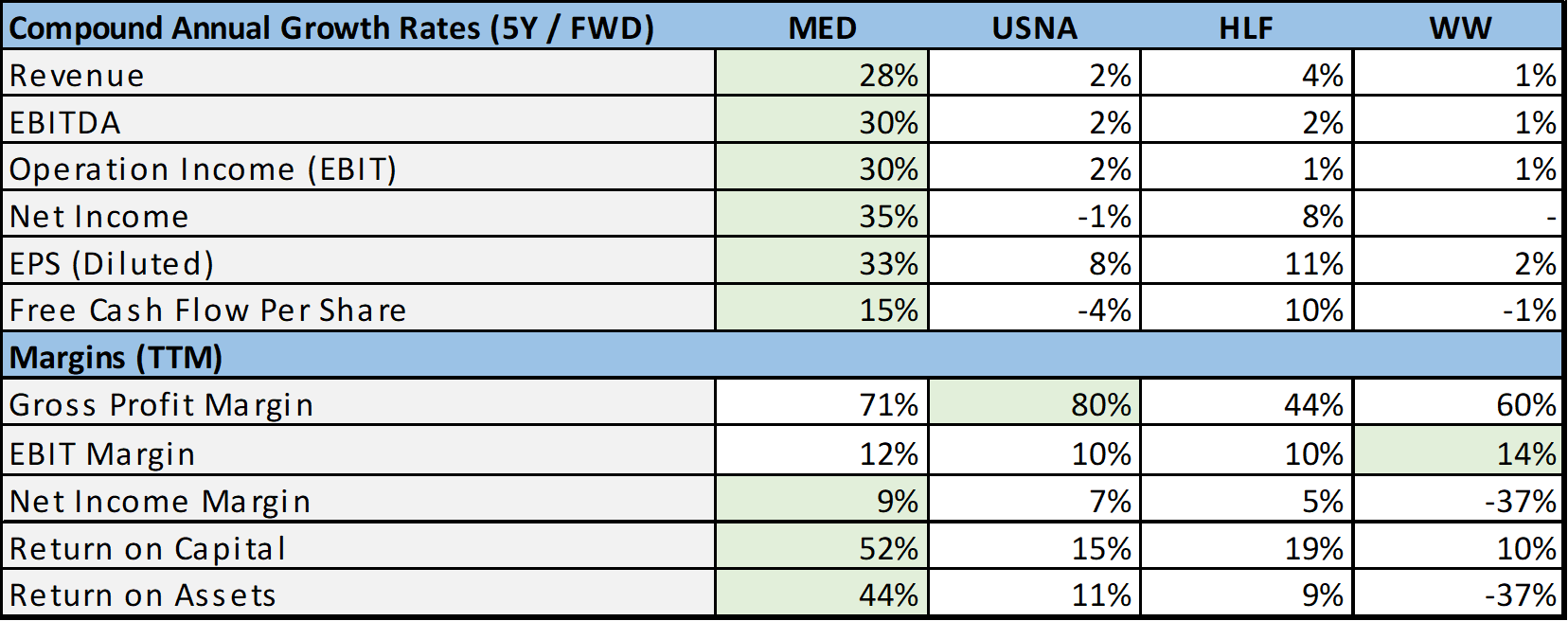

To set the competitors apart, I conducted the following matrix with relevant growth and profitability metrics. The highest value of each line is highlighted.

{kind=link}

I think here it becomes pretty apparent that Medifast currently outshines its competition in both growth and profitability.

Valuation

For a company that has been growing with ~30% over the last years, a forward PE-ratio of 11 and a price-to-sales-ratio of 0.63 seems to be cheap on the first glance. However the days of pure growth are certainly over for Medifast - at least for the next 2 years - why the company's current valuation makes sense to some extent.

However where things get interesting is, when we compare the valuation of above mentioned competitors to Medifast's valuation.

The only company trading at a lower valuation than MED is HLF, which is a lower quality company compared to MED, in my opinion. The fact that USNA is trading at twice the PE indicates that Medifast could be highly undervalued.

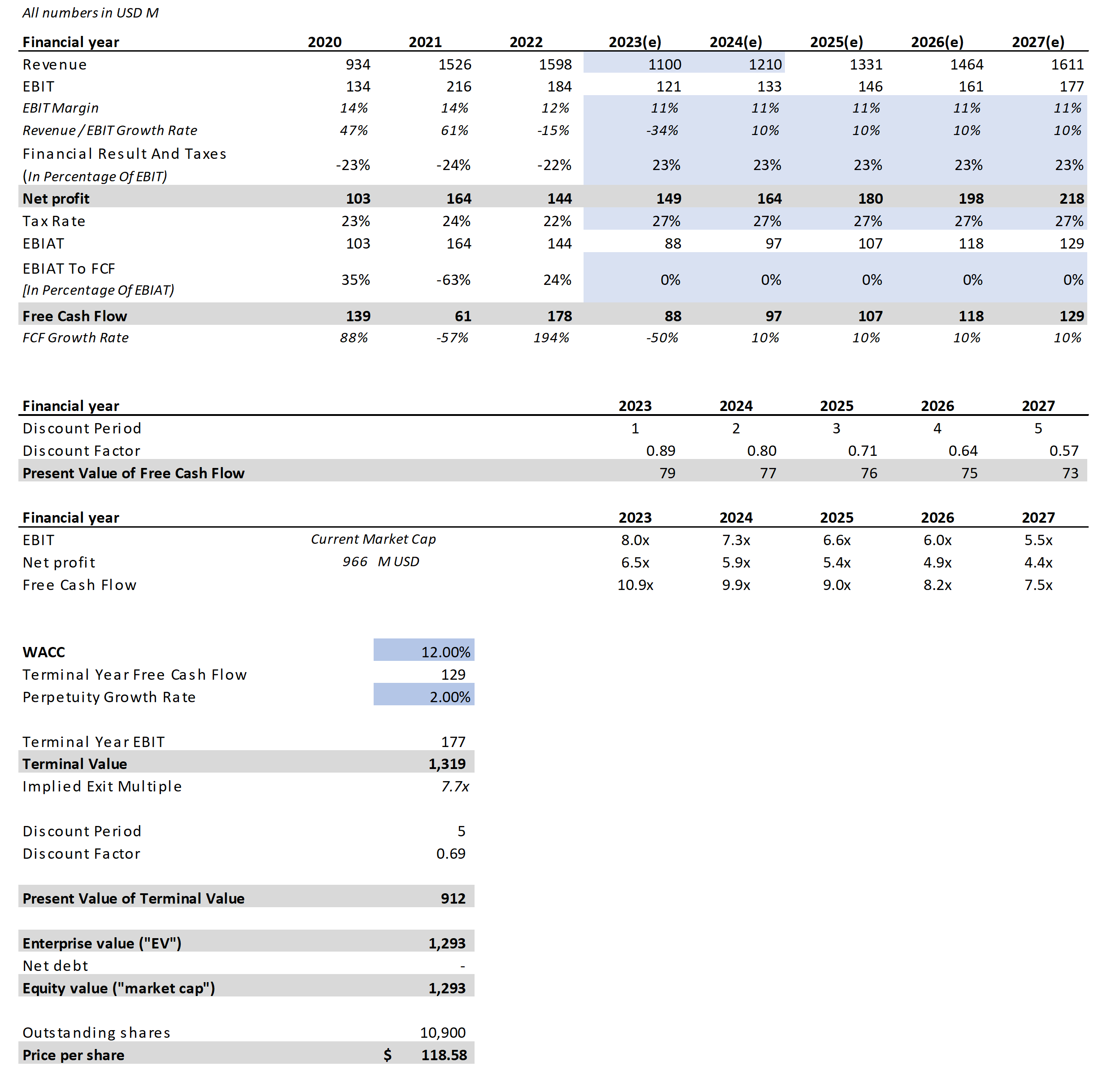

To get a clear picture and to address the expected decline in top and bottom line in 2023 and 2024 as well as the growth after these challenging times, I conducted a Discounted Cash Flow Analysis ((DCF)). The analysis's blue cells stand for the presumptions used to valuate MED. Most of my assumptions are similar to the analysts' expectations stated by Marketscreener. Here is a quick summary of how I determined and forecast the values for the future:

- Revenue: First of all I forecasted the 2023 revenue to be $1.1 billion, this consists of the $350 million from the Q1 of 2023 and 3x the lower end of quarterly guidance - $250 million - for Q2 2023. From there on, I assumed an annual revenue growth rate of 10% till 2027.

- EBIT: To get to appropriate EBIT values, I precited a rather conservative margin of 11%, compared to 14% in 2020 & 2021 and 12% in 2022.

- Financial Result And Taxes: I used 23% to calculate the EBIT and Net Profit for the years 2023 to 2027 after averaging the figures from the previous three years.

- Net profit: To calculate the net profit, I used the above mentioned Financial Result And Taxes metric.

- Tax Rate: Here I used 27%, the high end of management's Q2 2023 guidance.

- Free Cash Flow: Using the Tax Rate above, I calculated the EBIAT and afterwards tried to determine a suitable EBIAT to FCF ratio. I once again averaged out the last three years and therefore used 0% as a EBIAT to FCF metric till 2027.

- WACC: I assumed a, in my opinion conservative, WACC of 12% .

- Perpetuity Growth Rate: The perpetuity growth rate assumed for the analysis is 2%.

seekingalpha.com; medifast.com

{kind=link}

Our target share price, determined by this analysis, is $118.58. With this in mind and assuming Medifast will expand/contract as predicted above, its upside potential appears to be over 35%, indicating that it would be a good purchase at the moment.

Risks To Consider

The first two risks were also stated in my latest article, if you already have these aspects in mind you continue to at the chapter "Recession".

Business Model

The multi-level marketing ((MLM)) business model used by Medifast entails coaches enlisting customers who can then enlist additional customers. Due to past and contemporary illegal pyramid schemes, MLM is frequently connected with negative connotations . In contrast, Medifast has addressed this matter in their most recent annual report, noting that OPTAVIA Coaches do not handle or distribute goods to customers and that the majority of their revenue comes from point-of-sale transactions carried out on an e-commerce platform.

Public Opinion

It's simple to obtain reviews and test results for Optavia on numerous websites, like US News Health, in the digital age of instant information. Optavia currently has a meager rating of 3.6 out of 5 stars . Which, in my opinion, is pretty good but not outstanding.

However, I find it odd that the biggest issue with this diet is how tough it is to adhere to because, according to Medifast, this is one of Optavia's key benefits.

Even if some critics contend that Optavia's diet isn't very healthful , the majority of the unfavorable remarks are attributable to the paucity of long-term outcomes. Given that Optavia is a relatively new diet, it makes sense that this is a worry for many people. I do not believe Optavia's diet is worse than that of its rivals, nevertheless.

However, it's important to keep in mind that a change in public opinion in favor of Optavia and then Medifast could be detrimental to MED's fundamentals and eventually its stock price.

Drugs

Special thanks to "Fcfrag," who raised the topic of drugs that can aid people with health problems and obesity in a comment on my previous post. This inspired me to research this risk factor more thoroughly.

Weight loss is assisted by medications like "semaglutide". To help with the process, they are usually used in combination with a good diet and exercise routine.

While there may be medications available now or in the future that will completely treat obesity, in my opinion, no prescription can substitute a truly healthy lifestyle that includes a balanced diet and regular exercise. However, due to a natural drive toward ease and quick cures, some people may choose an easier path and this poses a serious risk to Medifast.

Conclusion

With the facts mentioned, I think Medifast can offer an good investing opportunity, even amidst the declining fundamentals and the mentioned risks. Due to excellent long-term market conditions, a network effect, good management, and a distinctive business model, Medifast has a bright future ahead. Street analysts and Quant ratings presently have Medifast rated as a "Hold":

seekingalpha.com

I think that the stock's current level of ambiguity may be one factor in this. The management of MED still refrained to give a guidance for the whole year of 2023. This seems to indicate that even the management currently isn't certain about MED's short-term perspectives.

However when consider the undervaluation of ~35% and the growing Total Addressable Market ((TAM)) of Medifast due to the rising obesity rates and the growing awareness for health and weight issues. Through its outstanding balance sheet, profitability and business model compared to its competitors remains, to be the best investment in this segment.

Given these circumstances, I, therefore, reiterate my ' Buy ' rating for Medifast, with a price target of ~ $115.

For further details see:

Medifast: Strong Earnings But Guidance Disappoints