MELI - MercadoLibre: A Digital Ads Giant In The Making

2023-08-22 08:30:00 ET

Summary

- In Q2 2023, MercadoLibre's digital ad business reached new heights. It is now 1.6% of MercadoLibre's $10B worth of Q2 2023 GMV.

- In Q1, this business grew at 60%+, and, of note, it's a very high margin business that creates substantial value for all ecommerce stakeholders: the marketplace, consumer, and merchant.

- Today, we will also discuss MercadoLibre's FinTech and ecommerce business briefly. I also shared thoughts on identifying quality businesses with decades of growth ahead.

- In short, I like MercadoLibre at ~$1,350/share.

The Cycle Of Life And Death

To begin this review of MercadoLibre's (MELI) most recent quarter and the business broadly, I'd like to share concepts core to my investment philosophy, which underpin my investment in and ownership of MercadoLibre.

If we assume a high-level view of the business world (investing is generally the act of purchasing the best businesses and holding them for the long run), we can scientifically determine where exceptional returns will spawn.

That is, every industry, every market, and every discipline in life cycles through:

- Birth

- Maturation

- Productive Application

- Death

In the case of business, with each birth, new companies emerge that renew the industry in which they operate. Sometimes, they renew the industry to the extent that it becomes unrecognizable.

We can think of this as cells regenerating in a body, leading to a renewed body (industry) over the course of years or decades.

And, with each death, incumbent/old companies die, making room for the new to grow and flourish.

To believe that the business world exists in any other way would be akin to believing that the laws of nature do not exist. Everything, from an individual human or plant cell to our great empires to this very universe itself, will experience the cycle of life and death.

I capitalize on this process of life and death within the world of business by allocating capital in accordance with my "Inverse Bubbles" investing framework (this is term I coined so it's not worth Googling it, which I share to save you time and provide context).

An "Inverse Bubble" is an industry populated by the aforementioned incumbent/aging companies: stagnant cells that will be eliminated by new, more dynamic cells in the body (industry). These businesses are no longer dynamic and evolving, and they often possess technology or thought structures from bygone eras that make them fundamentally disadvantaged.

In the Inverse Bubble framework, a new entrant (new business) emerges, and, over time, with its dynamic, evolving, and technologically advanced product/platform, it eats away at the existing market (defined by total addressable market $), capturing market share via its differentiated, more desirable product.

Coupang Eating Away At Its "Inverse Bubble"

- It's "Inverse" Because Coupang's Value (Market Cap) Is Small Relative To The Industry/TAM In Which It's Growing; Therefore, Coupang Collapses The Bubble Into Itself By Consuming Market Share And, Commensurately, Expands As The Bubble's Collapses Into Coupang's Revenue And Profits.

Coupang Investor Relations

- Conversely, in a regular bubble, Coupang's market cap would dwarf the industry in which it's consuming market share, making the entire situation an unsustainable bubble where the business' value is set to collapse down to the size of the actual market.

A fantastic example of this investing framework/dynamic was Walmart ( WMT ) in the 1970s. Walmart introduced a vertically integrated retail concept that used technology and economies of scale to create the cheapest, most convenient shopping experience available to consumers. It employed technology at giant scale to facilitate this inexpensive, convenient shopping experience.

The incumbents of the retail industry, e.g., mom and pop grocers or department stores like Sears, fundamentally could not compete with Walmart's new and differentiated offering. (In the interest of brevity, I won't go into "The Innovator's Dilemma," which is often the basis for why incumbents struggle to compete with new entrants during this cycle of life and death, but this is worth noting, and I will discuss it in the future with you.).

Over time, Walmart gradually consumed this trillion dollar+ total addressable market (grew within its Inverse Bubble), and, today, it generates hundreds of billions in annual sales, much of which it took from the incumbent/aging businesses that, in accordance with the laws of nature, were to inevitably die. It was all a matter of the cycle of life and death for the retail industry, just as the industrial revolution catalyzed the death of the Catholic Church's grip on government in Europe, ushering in our current 19th-20th century nation-state paradigm.

It was all a matter of the cycle of life and death, just as this cycle of life and death plays out ubiquitously in our universe.

The Digital Ad & AI Revolution Lumbers Forward

With these ideas in mind, I have been focused on the emergence of new life in specifically the ad industry as it pertains to MercadoLibre.

I penned an in-depth exploration of the emergence of AI-driven advertising (digital ads) not just at Meta ( META ) and Alphabet ( GOOG ) ( GOOGL ) but also, at businesses like Roku ( ROKU ) and MercadoLibre. You may read that work via the links below.

- The Greatest Secular Growth Trends I (Digital Ads)

- And I recently highlighted the growth of digital ads for ecommerce platforms in this note specifically.

From those notes, I shared important industry data that has underpinned my investment in my favorite digital ad businesses, such as MercadoLibre.

Total Digital Ad Spend Globally

eMarketer

Notably, this chart is from 2021, and 2023 has proven to be a challenging year for the entire ad market, so growth may come in below 10%, but the long term trend is certainly up.

And, within this TAM, growth on ecommerce ad spend is growing faster than the overall digital ad TAM, which we can see below:

Digital Ad Money Spent On Ecommerce Platforms (Read Description for More Detail)

eMarketer

- Note: It is worth emphasizing that, in the Inverse Bubble paradigm, the new entrants often not only capture large portions of the overall total addressable market (the inverse bubble so to speak), but also, they expand the size of the bubble, creating greater value for all stakeholders (including shareholders) in the process. This is important to remember, and we may be seeing this play out with Tesla ( TSLA ). It is standard practice for bears highlight the size of the TAM populated by aging incumbents, but this can often be misguided. The new technologies, such as Walmart's vertically integrated business model, often serve to expand the TAM of the industry. In the world of technology, this is especially true.

And this growth makes sense based on the numbers reported by ecommerce platforms around the world, such as Amazon ( AMZN ) and MercadoLibre.

{kind=link}

At Long Last

When I published The Greatest Secular Growth Trends I (shared with you just a moment ago), in which I highlighted MercadoLibre as well as Sea ( SE ) and Amazon as interesting digital ad businesses, I don't recall MercadoLibre reporting any metrics related to its ad business.

In fact, I don't believe they really began reporting digital ad metrics until 2022 in earnest.

But, based on Amazon's ad business , I knew the MercadoLibre ad revenue would come, and it would likely become a $10B+ revenue business over time.

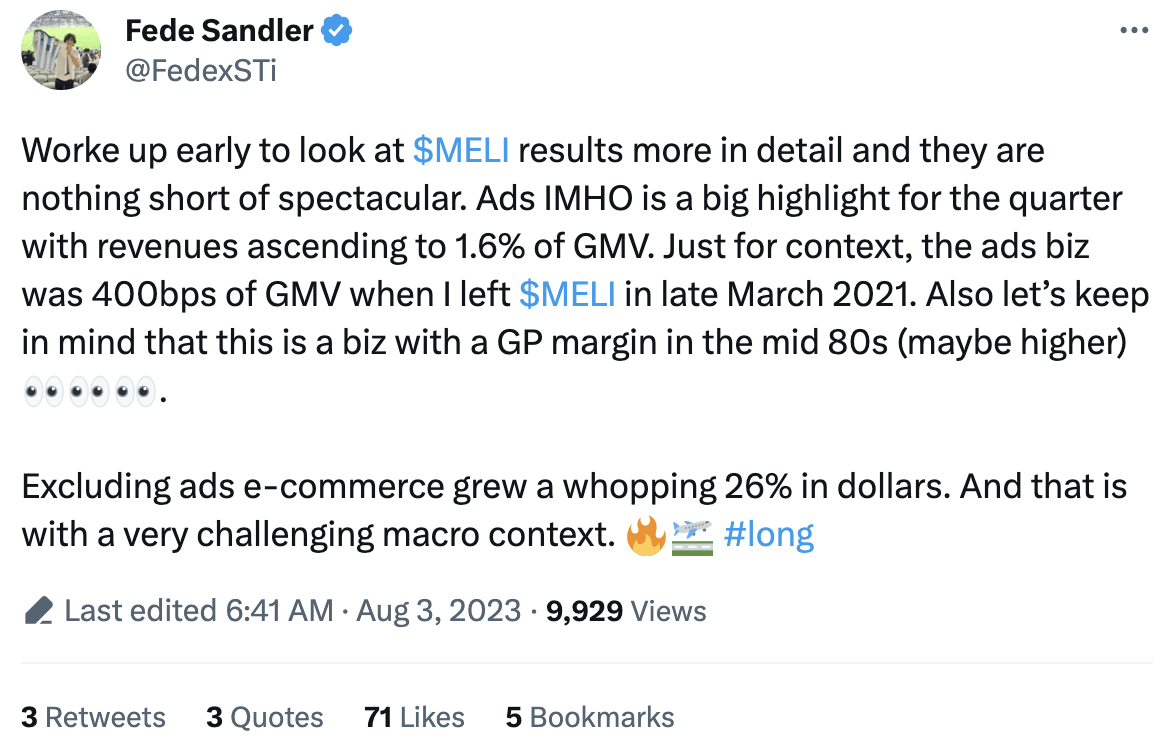

In this vein, I found the following Xeet (?) relevant to this discussion:

{kind=link}

As we read, MercadoLibre has made material progress on its digital ads business.

In 2021, it was only .4% of GMV, and GMV was much smaller than what it is today.

Today, not only has MercadoLibre grown its ad business, but also it's grown its GMV materially.

Today, MercadoLibre's ad business is 1.6% of $10B worth of quarterly GMV, and MercadoLibre's ad business grew at over 60% in Q1 2023.

This suggests that MercadoLibre's ad business currently generates about $640M in annualized, 80% gross margin sales, and this is likely growing at well over 50% , in the midst of an economic environment where ad spending has entered a state of paralysis, relatively speaking.

Once we emerge from this period of advertising spend paralysis, created by the fastest rate hiking cycle in American history, which is exported to Latin American countries as explained by the "Trilemma," this ad growth could very well accelerate.

In short, I believe MercadoLibre's ad business will one day generate tens of billions in high margin sales for the conglomerate, and, as such, we're still in the very, very early innings for MercadoLibre's ad business and for the growth of its overall conglomerate.

Let's now turn to MercadoLibre's other lines of business, which are likewise very early in their growth journeys.

Just Doing The Right Thing Consistently: Payments & Ecommerce Business

In response to MercadoLibre's report, I remarked,

It's fairly easy to produce such great results when our competition is dropping like flies due to blatant fraud and allegations of fraud.

By which I meant that Americanas, one of MercadoLibre's largest competitors in the highly sought after Brazilian commerce market, outright committed fraud and will likely wind down operations over time, or, at the very least, is no longer genuinely competing head to head with MercadoLibre's innovation and growth engine. The fraud was fairly egregious:

Around the same time this was revealed, DLocal ( DLO ), a payments business (specifically acquiring platform) that competes with MercadoLibre's payments business (specifically acquiring platform, which allows merchants to accept payments), was accused of fraud.

In the case of DLocal, the fraud allegations have been just that: allegations.

That said, I can't imagine that being publicly accused of fraud, which sent the share price down 50%; from which it's not recovered, is exactly good for business.

With these ideas in mind, as I have often shared, business is far, far less about competition and far, far more about focusing on the customer and executing in a high integrity manner.

For the most part, and with few exceptions, quality, high integrity execution with a focus on the customer will yield a successful business outcome. On what timeline will that occur? I cannot be sure. Will there be setbacks? Will there be competitive pressure? Sure, but those that provide quality, high integrity products (execution is required) to their customers day in, day out, for years and decades at a time will ultimately "find the kingdom of heaven," i.e., their businesses will succeed and their shareholders will be happy.

And we're seeing this play out with MercadoLibre in some sense. While we've seen competitors begin to pressure MercadoLibre over the years, including Amazon ( AMZN ), it has simply continued to serve Latin America with quality, high integrity execution.

Now, the path forward is being opened unto it: One of its largest Brazilian competitors just folded (Americanas). One of its largest payments competitors is getting rocked by fraud accusations.

The storm clouds are gradually dissipating and the heavens are opening up, in some sense, creating a path for sustained elevated growth in the future.

And this all happened by virtue of quality, high integrity, consistent execution as opposed to some 5D chess, Silicon Valley stratagem.

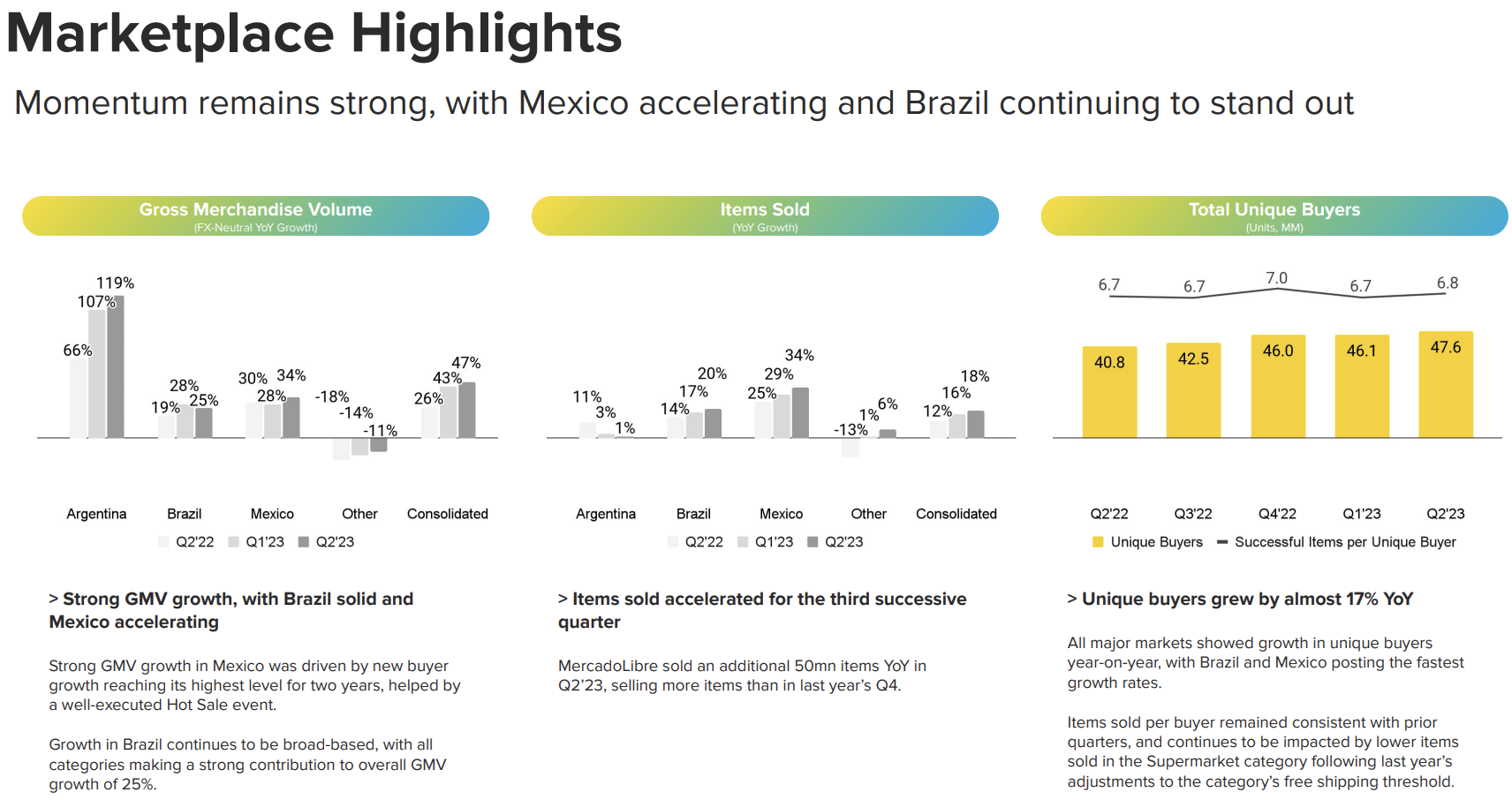

MercadoLibre's Ecommerce Business Highlights

- Note exceptional growth in Brazil and Mexico. Mexico is now the 2nd largest market for MercadoLibre, which is fantastic and alleviates pressures from Argentina's political instability.

- Note solid growth in unique buyers.

{kind=link}

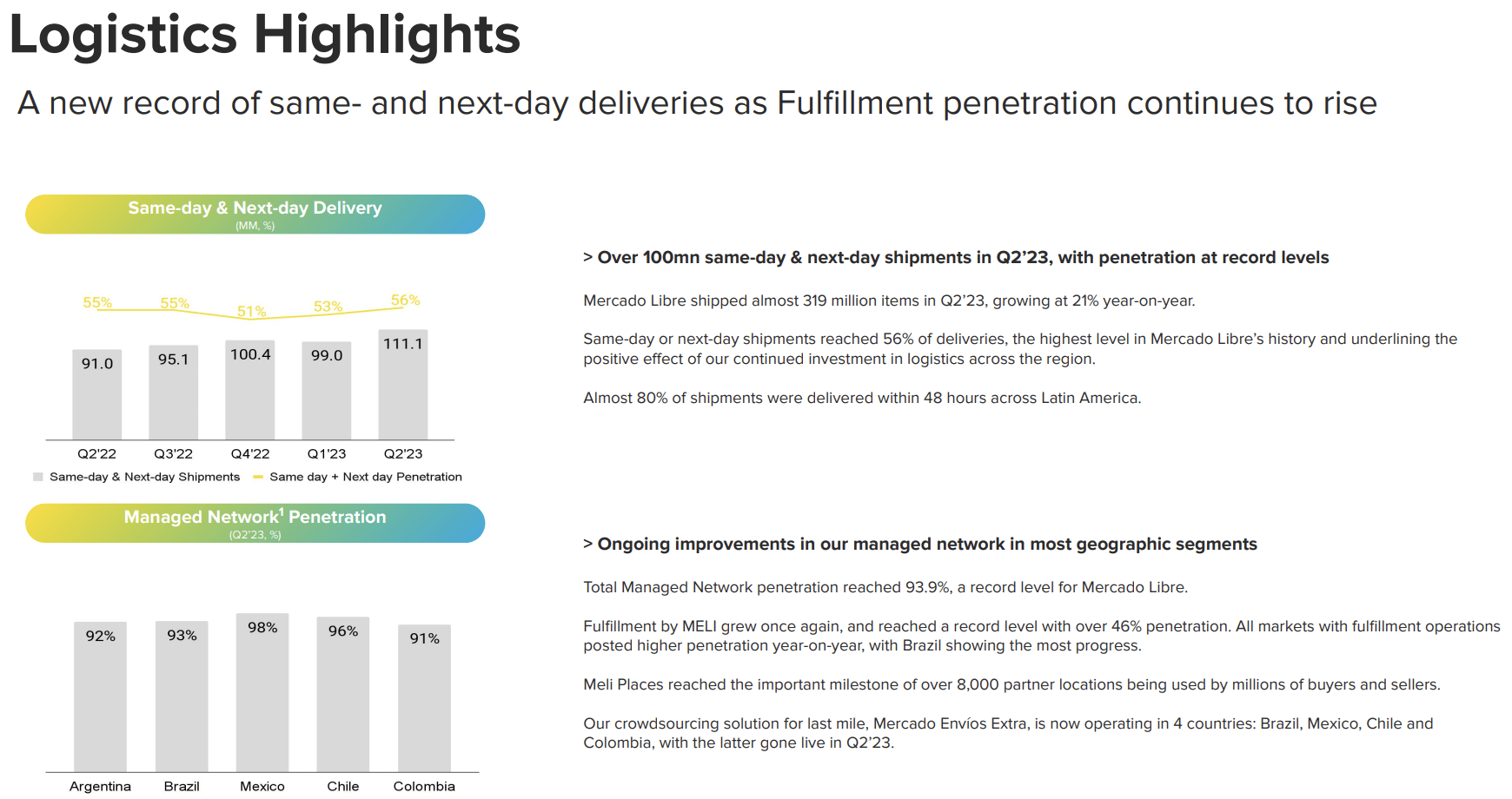

This exceptional growth was predicated on MercadoLibre's robust logistics network, which acts as a moat for the business. Notably, I believe there's very material room to evolve ecommerce logistics networks via AI and automation, which will serve to further heighten MercadoLibre's moat in this respect.

{kind=link}

I believe we still have a long runway for MercadoLibre's ecommerce business. In the U.S. ecommerce sales penetration has reached 21.7%, but in Latin America, ecommerce sales are still only at about 7%.

eMarketer eMarketer

MercadoLibre's ecommerce marketplace business, its ads business, its payments business, and its shipping & logistics business will all grow by virtue of this long runway for growth still ahead.

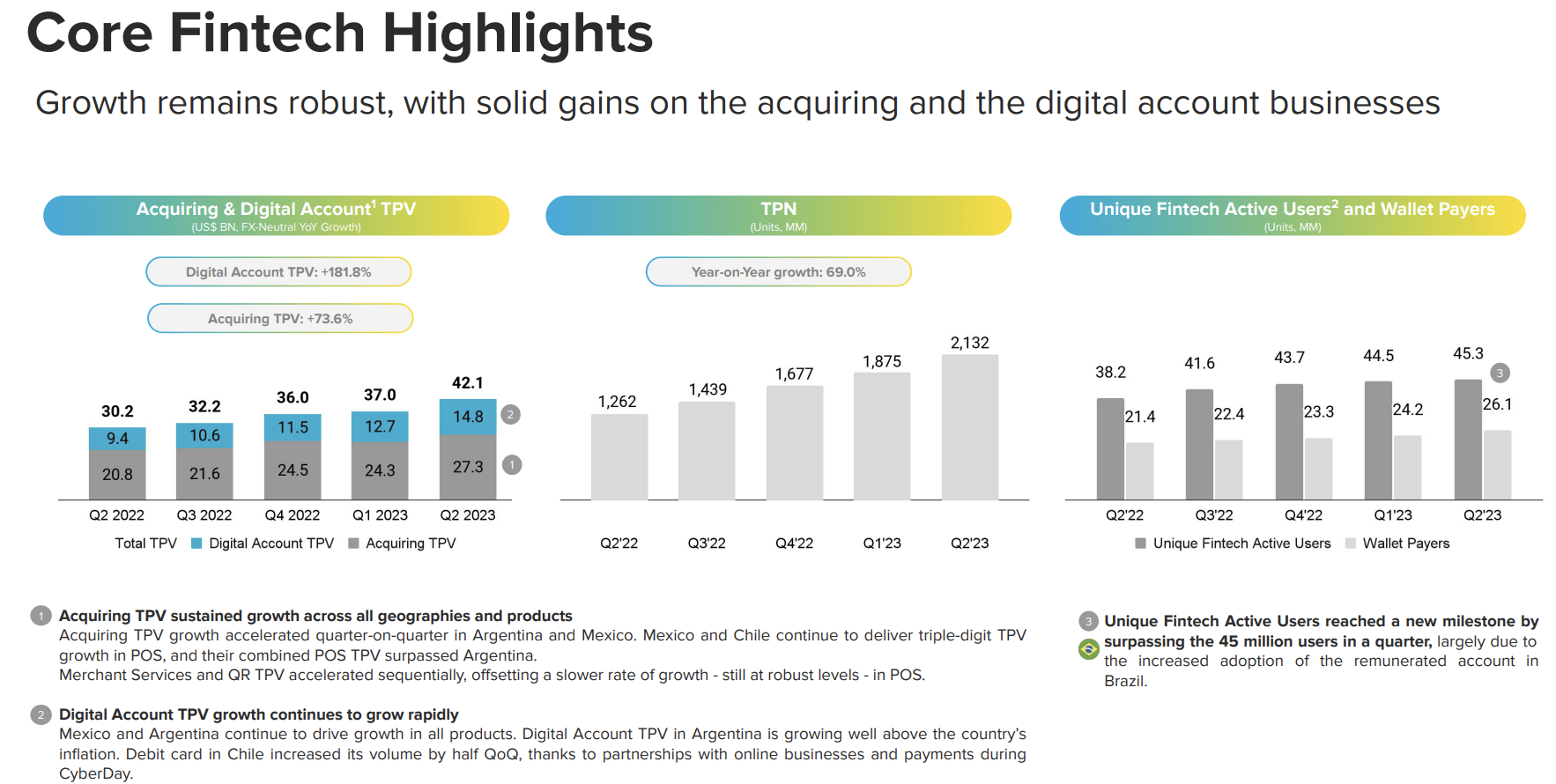

Turning to MercadoLibre's payments business, we saw exceptional growth from its acquiring platform.

Acquiring Platform (Allows Merchants To Manage & Accept Payments) And Consumer Platform (Think Whatever Digital Banking Platform You Use)

{kind=link}

As mentioned, DLocal competes with this business, but also, companies, like Adyen (ADYEY), which I own and like a lot, compete with this business.

I think it's a fantastic business, and I think ecommerce is also a fantastic business, especially when we consider the digital ads upside that we've anticipated and are now experiencing, and we now have an even longer runway for growth in light of the troubles MercadoLibre's competitors have faced.

{kind=link}

Further, with the majority of people in Latin America still unbanked, MercadoLibre's consumer facing financial platform likely has decades of runway for growth still ahead.

And, as Latin Americans gain access to digital banking, MercadoLibre's acquiring platform, which, again, allows merchants to accept and manage payments digitally, will naturally gain further adoption, leading to further exceptional growth for MercadoLibre.

In an underbanked country like Mexico, our strategy has been to serve and develop both sides of the market payers and merchants to drive market development. By bringing more consumers to digital finance, we also drive adoption among merchants in the country.

That is why Mercado Pago offers complete payment solution to these merchants, combined with the fastest payment settlement in the market and competitive receivables discount rates. During 2023, we increased our focus on our smart POS in Mexico, aimed at larger merchants that generate higher TPV. Merchants also have access to online payment tools and are able to offer payments in installments to their buyers.

Richard Cathcart, Investor Relations, Q2 2023 Earnings Call

Concluding Thoughts

I have publicly shared my thesis for MercadoLibre since about mid-2020, and the core pillars of my thesis have not wavered.

- MercadoLibre would become a digital ads juggernaut.

- Ecommerce had decades of growth still ahead in Latin America

- The majority of Latin America's population was unbanked, and, as such, MercadoLibre's FinTech offering had a long runway for growth as well.

Notably, despite incredible core business performance for the last few years, my first and central pillar is only now really getting started. There's still a giant runway ahead for this first pillar, and I believe the same could be said for the latter two pillars as well, as the data that I shared with you today indicates.

Thank you for reading, and have a great day.

For further details see:

MercadoLibre: A Digital Ads Giant In The Making