MELI - MercadoLibre: A Solid Company With A Long Runway For Growth

2024-01-16 08:00:00 ET

Summary

- MercadoLibre is the leading e-commerce giant in Latin America, with operations in multiple countries.

- The company has a profitable business model and has generated strong revenue growth and cash flow.

- We believe that the growth potential has not been fully priced into the stock. A low e-commerce penetration rate and limited access to credit offerings are the primary drivers.

- MELI's early investments in logistics and local expertise will help maintain its strong competitive position.

- Our estimated fair value is $1,950/share (base case), derived from the DCF model (12% WACC, 4% terminal growth). Key risks include a challenging macro backdrop and competitive threat from Amazon.

Investment Thesis

MercadoLibre ( MELI ) has a long runway for growth, driven by a low e-commerce penetration rate and lagging financial inclusion in Latin America. Additionally, we believe that economies of scale, a profitable 1P (first-party) business, and margin-accretive initiatives such as digital ads will contribute to expanding margins. Furthermore, the strategic early investments in establishing its logistics network and local expertise play a pivotal role in fending off new competitors. The estimated fair value is $1,950/share (18% upside in the base case scenario) derived from DCF valuation.

Company Profile

Founded in 1999, the Argentine company MercadoLibre is the leading e-commerce giant in Latin America. Although it originated in Argentina, the company extended its reach to Brazil, Mexico, and other fifteen Latin American countries. Brazil, Argentina, and Mexico accounted for over 95% of MELI's revenue.

The founder-led company initially operated as an eBay-like marketplace with an auction-based pricing model. But, over time, it transitioned to a fixed-based model. MELI divides its business into two distinct segments:

- MercadoLibre: 1P (first-party) and 3P (third-party) marketplace, logistics service (Mercado Envios), digital advertising (Mercado Ads), classifieds service, and online storefronts solution.

- Mercado Pago: an integrated fintech solution, which includes credit services, saving accounts, insurance, and payments.

{kind=link}

What we like about MELI is that, unlike typical cash-burning e-commerce companies, MELI achieved profitability and generated free cash flow merely six years after its inception. Additionally, the company demonstrated a jaw-dropping 66% 3-year CAGR in net revenues from 2019 to 2022. This is also followed by operating and FCF margin expansion, as well as superior ROE and ROIC compared to its competitors. It is not a capital-intensive business, and its balance sheet remains unburdened by debt, with a 0.6x net debt to adjusted EBITDA ratio.

Further, MELI's stock has surged nearly tenfold the price in seven years, driven by accelerated top-line growth acceleration, in our view. Shares are currently 18% below their all-time high.

MELI Stock Price (YCharts, Vektor Research)

However, we note that markets are concerned about the following points:

- Whether MELI's growth potential has already been fully priced into the stock. Our 10-year reverse DCF model suggests that markets are expecting ~14% revenue growth to justify the current price.

- Whether new competitors, such as PDD Holdings ( PDD )-operated Temu, will erode MELI's competitive positioning in Latin America.

We believe that MELI still has a long runway for growth, and its early investments in logistics, coupled with its local expertise, will help fend off new competitors.

An Integrated E-commerce and Fintech Ecosystem, Long Runway for Growth

With a population exceeding 600 million people, Latin America has witnessed a 50% increase in its middle-income class over the last decade. Furthermore, the onset of the pandemic has led to a shift in consumer behavior, making online shopping the new norm. In 2020, Latin America's e-commerce sales grew 37% (Y/Y).

However, despite the expanding middle-class population and rapid digitalization, a report from Latitud reveals that the e-commerce market size in Latin America is only 19% of the US market and 8% of the Chinese market. Limited internet connectivity and underdeveloped logistics resulted in a low e-commerce penetration rate, according to Lazard.

But this leaves ample room for growth. Research from Payments & Commerce Market Intelligence ("PCMI") indicates that e-commerce transaction volume in Latin America is estimated to grow over 20% annually until 2026, nearly doubling in size within the next three years.

The impressive thing is that, unlike the typical e-commerce companies whose high growth rates eventually decelerate, MELI reported accelerating currency-neutral GMV growth in Brazil (28% Y/Y) and Mexico (34% Y/Y) in 3Q23, the two largest e-commerce markets in Latin America. Further, despite a hyperinflationary environment, Argentina showed recovery in units sold.

GMV year-on-year Growth (%) (Company)

When asked what factors resulted in MELI growing at a similar rate to the rate four years ago, the management highlighted investment in technology, more offerings, and its subscription program as the primary drivers:

We think that we had done prior to 2019 a lot of things. We had invested a lot of money and efforts on mostly technology, so got us at the right time, in the right place. We were able to benefit, I think, more than other players in the region when that happened.

And since then, when we grew in scale, obviously, the power of the ecosystem is very strong, and we continue to add features and functionalities and products to this ecosystem, advertising being one of them. Financing on the credit cards being another one, insurance being another one.

And more recently, all the content plays, whether it's our partnership with Disney and other great content providers that we are distributing through MELI Mas, or whether it's or whether it's Mercado Play our Clips.

First, MELI relaunched its loyalty program, MELI+, offering subscribers free shipping for orders above R$29 ($6), in contrast to the free shipping fee threshold of R$79 ($16) for selected products. While MELI previously had a "six level" subscription program with varied benefits, analysts at Goldman Sachs note that, despite the similarities in benefits, the new program will provide "greater clarity around the value proposition" and "drive broader adoption," as reported by Bloomberg Linea . Typically, subscription programs play a pivotal role in boosting customer spending and increasing retention rate .

MELI+ subscription program (Company)

{kind=link}

Second, MELI's integrated ecosystem plays a crucial role in driving growth . Mercado Pago, one of the leading fintech platforms in Latin America, was designed to support the commerce business. But it extends its services beyond MELI's Marketplace platform. Mercado Pago actually addressed one of the biggest pain points for Latin Americans: a lack of trust in the traditional financial system, limited access to credit offerings, and a large underbanked and unbanked population.

Mercado Pago initially focused on facilitating online payments but later expanded its services to include credit offerings, saving accounts, insurance, and investments. Research conducted by Mastercard ( MA ) and Americas Market Intelligence indicates that, while 58% of the respondents already possess a credit card, only 31% have access to loans or line of credit . In Mexico, credit card penetration is at 39%, with only 18% having access to loans. Notably, a significant portion of respondents reported facing rejection in their applications for these offerings at least once.

This opens up an opportunity to explore. For instance, the partnership between Mercado Pago and Visa ( V ) reportedly has issued 150,000 credit cards in Mexico just three months since its announcement.

This is also in line with what the management highlighted on the 2Q23 earnings call :

For Mercado Pago, Mexico represents an exciting opportunity. It is a growing country, with a large population that currently has lower adoption of financial services than other markets in Latin America, such as Brazil.

Over the last few quarters, we have been rolling out our fintech product stack in Mexico, positioning MercadoPago as one of the leaders in the development of the market for digital payments and other financial services. Our strategy is to serve both payers and merchants, focusing on users that are already within our ecosystem. As we do this, we build on the trust of MercadoLibre's brand, and build on the user relationships and knowledge from the commerce business to better serve our fintech users.

Credit Portfolio ($ million) (Company)

The advantage of an integrated ecosystem is that, instead of navigating typical time-consuming procedures in the traditional financial institutions, prospective customers can undergo a more efficient onboarding process since MELI already possesses the customer data. This translates to improved access to credit offerings, thus enhancing spending power.

Unique Fintech and Marketplace Users (million) (Company)

Mercado Pago is a significant growth driver and demonstrates profitability. From 3Q20 to 3Q23, Total Payment Volume ("TPV") more than tripled, and fintech net revenues grew 61% annually, on average, during the same period.

Mercado Pago's TPV ($ million) (Company)

Indeed, non-performing loans ("NPL") due less than 90 days and more than 90 days in 3Q23 stood at 11% and 20%, respectively. The management stated that the slight uptick in the short-term NPL ratio was due to the initiative to expand to the "mid-risk segment." Yet, profitability remained robust with Net Interest Margin After Losses ("NIMAL") at 37%.

NIMAL (%) (Company)

In conclusion, we believe that MELI still has a significant growth potential driven by the low e-commerce penetration rate in Latin America, the success of its subscription program, and the fintech offerings that effectively address lingering challenges in the region. In our view, MELI's growth potential has not been fully baked into the stock.

Getting More Efficient as the Business Scales Up

Since 3Q20, MELI has expanded its gross margins by over 1,000 bps, operating margins from single digit to high teens, and it has generated 20%+ FCF margins.

MELI's margins (%) (Vektor Research)

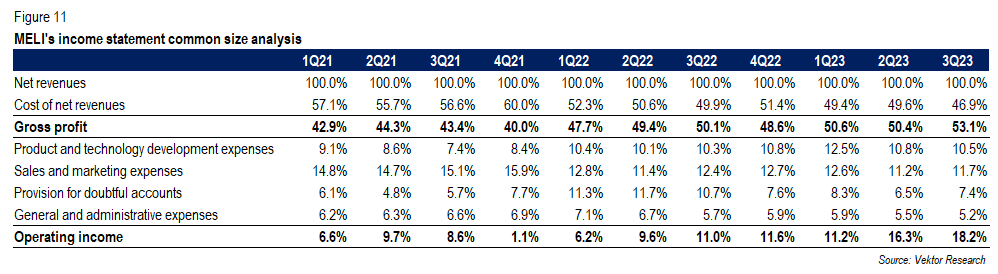

Several reasons help explain the ongoing margin expansion. First, as MELI scales up, shipping costs are spread over a larger volume of goods. Second, despite still being a loss-making business, the company has been improving the profitability of its 1P operations. Lastly, MELI has demonstrated the ability to increase its revenue without solely depending on sales and marketing. A common size analysis indicates a decline in S&M and G&A expenses as a percentage of net revenues, while the company maintains its R&D expenses.

MELI's income statement common size analysis (Vektor Research)

{kind=link}

Looking forward, we believe that MELI can expand its operating margins to 20%+. This is supported by economies of scale, profitable 1P operations, and margin-accretive initiatives, such as the digital ads business.

Leveraging its Own Logistics Network to Stay Ahead of Competitors

The management acknowledged that Latin America has become more competitive, as foreign players seek to establish their presence in this fast-growing region. However, MELI remains the leading e-commerce player in Latin America with over 30% share, per Bloomberg. The early adoption of the 3P model, which generally produces higher margins than its 1P counterpart, proved to bear fruit, while others entered the game later.

For instance, MELI's Brazilian competitor Americanas S.A. launched its marketplace platform in 2013, but it has closed down its stores and downsized its operations following the accounting fraud allegation last year. Magazine Luiza ( MGLUY ), or simply known as Magalu, joined the game later, deploying its marketplace platform by the end of 2016.

We believe that MELI's early investment in establishing its own logistics network has been crucial in maintaining its leadership. Previously, logistics were underdeveloped in Latin America, resulting in slow and costly deliveries. In that case, MELI decided to build its own logistics network in 2016. By the end of 2019, the managed network penetration, representing the percentage of items shipped through MELI's own logistics network, reached 43%. The number was over 94% in 3Q23. Furthermore, the fulfillment by MELI, which is similar to Amazon's ( AMZN ) Fulfillment by Amazon, accounted for 48% of all shipment. This contributes to a shorter delivery time for customers.

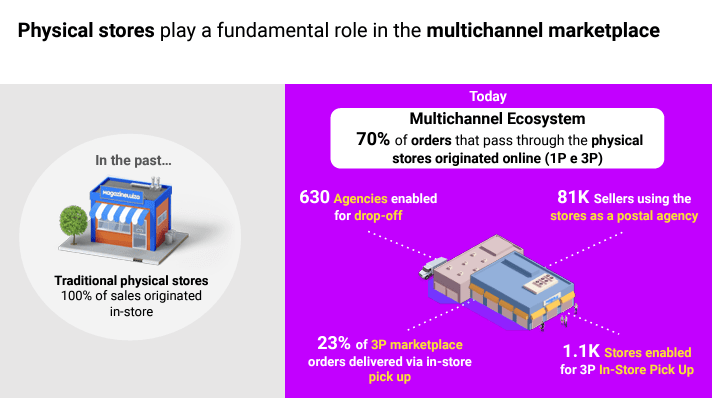

On the other hand, Magalu took a different approach, undertaking "multichannel" approach by leveraging its physical presence. As the CEO said:

It took us a while to launch fulfillment because we wanted to launch it absolutely integrated with our 1P operation and physical store. Way back in the past, when we launched 1P, its logistics was launched integrated with the physical store, which gave us a competitive differential, with many deliveries in 1P, thus we become the 1P leader in Brazil, as we used the physical store network to deliver 1P with lower costs and better deadlines for customers.

Magalu's Multichannel Approach (Magalu)

{kind=link}

Nevertheless, in terms of fulfillment penetration rate, Magalu lags behind MELI. As of 2Q23, only 14% of 3P orders went through the fulfillment centers, and just 51% of its 3P orders were delivered within 48 hours. In comparison, MELI achieved an 80% delivery within 48 hours for all orders.

While this is not exactly an apple-to-apple comparison, this highlights how MELI's early investments in its own logistics network contribute to its strong competitive position. Faster deliveries will typically attract more buyers and sellers. And an increase in product availability equals more growth . Additionally, MELI operates more efficiently than Magalu, producing over an 18% operating margin compared to Magalu's 8% in 3Q23.

While Amazon began its operations in Brazil as early as 2012, it was only selling digital books and Kindle e-readers, and just only recently they started to invest massively in logistics. Yet, Amazon is widely known for its AWS service in Latin America. Even Mercado Pago is a customer of AWS, as noted by Rest of World .

Further, when it comes to foreign players, it is more challenging for them to dominate the market, or even just take a slice of share, since it often goes beyond aggressive marketing and incentives. For example, some unsuccessful attempts such as Uber Technologies ( UBER ) in Southeast Asia and Coupang ( CPNG ) in Japan prove that local expertise is highly important.

When asked about competition, MELI's management acknowledged the highly competitive nature of the e-commerce space. However, they have gained market share in Mexico and Brazil. On 2Q23 earnings call :

So, I think Latin America has become one of the most intense competitive scenarios in the world probably. We have the big American player investing heavily in the region. We have Asian players who have local players to defend their position. So I guess we are all trying to serve the customers in different ways.

Actually, for us, I think our strategy has played well. If you were to look at third-party data, it seems that the case that we have been gaining market share, both in Mexico and in Brazil , even in this tough environment.

In other words, we believe that logistics advantage and local expertise are crucial in gaining share and defending against competitors. Indeed, Temu is gaining traction in the region, but MELI still showed strong growth. Per 3Q23 earnings call:

Over the last 24 years, we've been always competing with players from all over the world. So in a sense, we are used to having new entrants trying to get a pie of Latin America. We've seen Temu get into Mexico, in particular, in May, more or less. We've seen them making progress in app downloads and monthly active users. They seem to be spending a lot of money on marketing on social media, directed consumers, has been trying to download their app.

We are, obviously, monitoring that closely. But our data suggests that there is a bigger overlap between that business and the one with other cross-border platforms. Our business in the meantime continues to perform really well, as shown by the acceleration of items sold to 38% . Unit growth has been strong across the board, including categories where some of those players are focusing on, and all ASP ranges.

In our view, it will be challenging for new players to enter the competitive landscape where a few dominant players are in place, like those in Brazil. Overcoming the expensive and time-consuming shipping challenges is not an easy feat, as building logistics network will take years and require billions of dollars. In contrast, MELI has already established its logistics network, leveraging economies of scale that enable it to operate more efficiently than its competitors.

Valuation

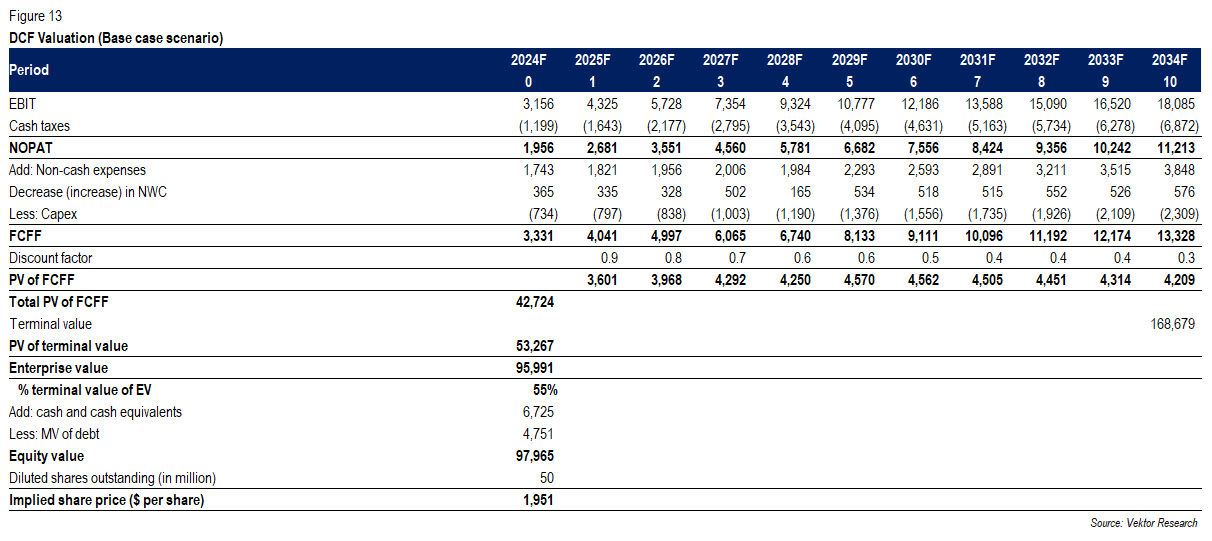

We arrive at MELI's fair value estimate at $1,950 per share (18% upside) based on DCF valuation (12% WACC and 4% terminal growth rate), implying a 38x P/E based on 2025F EPS. This assumes a 15% annual revenue growth over the next 10 years and a 23% operating margin in the terminal year. Our scenario analysis suggests that the fair value is between $1,500 and $2,500.

DCF Valuation (Vektor Research)

{kind=link}

Investment Risks

A Challenging Macroeconomic Backdrop

Elevated interest rates, slowing economic growth, and a wide deficit are the notable risks. In addition, change in regulations is another factor to consider.

Competitive Threat from Amazon

Amazon is investing heavily in Latin America, particularly in Mexico, where it already has a solid market share almost comparable to MELI. It has invested around 52 billion pesos ($3 billion) since 2015, and just recently opened the largest last-mile delivery station in the country. But logistics is also MELI's key focus to maintain its strong competitive position, as they opened a fulfillment center in Brazil in 3Q23, and plan to open a new one in Mexico this year.

Conclusion

We like MELI because it is a cash-generating company with a high growth rate, expanding margins, and a strong competitive position in the market. The e-commerce market still has ample room for growth, and millions of people lack access to credit products. Further, MELI+ and credit offerings will drive growth. And we believe that its logistics advantage and local expertise will fend off new competitors. A challenging macroeconomic backdrop remains a key risk to MELI. And while Amazon is spending massively in Latin America, logistics remain MELI's focus to maintain its competitive advantage.

Valuation-wise, MELI appears to be expensive with a forward P/E of more than 35x based on 2025F EPS. But its revenue is growing ~35%, margins are continuing their upward trajectory, and it is generating ROIC above the cost of capital. In addition, markets are expecting 14% of revenue growth in the next 10 years, which we believe is realistically possible for MELI to beat that expectation. Our estimated fair value is $1,950 per share (18% upside in the base case scenario) based on the DCF valuation method. We rate the stock buy . If you have any thoughts, please do not hesitate to comment below.

For further details see:

MercadoLibre: A Solid Company With A Long Runway For Growth