MELI - MercadoLibre: An Undervalued Overachiever

2024-01-09 07:17:37 ET

Summary

- MercadoLibre is a leading company in the Latin American e-commerce and fintech marketplaces.

- These markets are projected to grow significantly up until at least 2027.

- MELI has proven it knows how to execute its business plan and has set itself up to continue to do so.

- The main risks are that MercadoLibre may suffer if competition from larger competitors becomes stronger, or if they are forced to operate in a weakened economy for an extended period - particularly if that weakness is due to political or regulatory forces.

- I’ve calculated the fair value of MercadoLibre’s share price to be approximately $1,980.70 and believe this company is currently undervalued.

Introduction

If someone asked me to explain why I thought MercadoLibre ( MELI ) was a great company in just one sentence, I'd say "it's the Amazon of Latin America." Then when they ask how the Amazon River was able to generate net income and cash flow, I'd tell them I've already used up my one sentence and wish them good luck.

But using two sentences (or more), I'd go into depth about the diversity of MercadoLibre's business model, how sticky it is to existing customers (which in turn attracts new customers) and of course its growth rates and profitability. The No. 1 e-commerce player in Latin America has done nothing but execute at a high level over the past decade and in my opinion, will only continue to do so going forward. Also, the cherry on top is that it's a great way to diversify a portfolio outside of the USA. I've taken a deep dive into this business model and estimated the intrinsic value of the stock to be $1,980.70. Let's get into it.

What is MercadoLibre's opportunity?

For starters, MercadoLibre isn't a carbon copy of Amazon - but it's an easy starting point to conceptualize what they do and how they make money. There are six parts to their business model, with five of them having comparable similarities to what Amazon provides: MercadoLibre MarketPlace vs Amazon's e-commerce platform, Mercado Pago vs Amazon Pay, Mercado Envios logistics vs Amazon Prime/Logistics, Mercado Ads vs Amazon ads and Mercado Shops vs Amazon Stores. The only outlier is Mercado Libre Classifieds service, which doesn't have an Amazon counterpart that's similar enough to compare.

Starting with the MercadoLibre MarketPlace opportunity, it's estimated that MercadoLibre currently controls around 21.6% of the Latin American e-commerce market. The three major players in the Latin American e-commerce market are Brazil, Mexico, and (arguably) Argentina - and these three countries make up 95.4% of MercadoLibre's revenue. Now, the true beauty of the Latin American market is that it's still in its development stage and facing rapid growth prospects ahead. Brazil is anticipated to grow from $36.6 billion e-commerce sales in 2022 to $77.2 billion by 2027, representing a 111% growth. Mexico is also expecting rapid growth with a projection from $34.2 billion e-commerce sales from 2022 to $68.2 billion by 2027, which is a 99% increase. Argentina is the smallest e-commerce market size of the three, as it's currently estimated at around $7 billion in 2022. However, the growth rate is no less rapid, as this is projected to grow 111% by 2027 to reach 109% by 2027.

As per the below screenshot from MercadoLibre's Q3 investor presentation , they're showing that they're consolidating extremely well in these three markets. Both Gross Merchandise Volume (GMV) and the amount of items sold are increasing rapidly on a q/q basis. The amount of unique buyers has also increased 18% y/y, showing that they are attracting new customers at a fast pace.

MercadoLibre's Q3 Investor Presentation

This is fantastic to see as e-commerce is a very competitive industry, so it's clear that MercadoLibre is making all the right moves to grow its customer base in such an environment. Customer retention, however, is another matter entirely, which is where MercadoLibre truly shines with its sticky business model.

The first element of this is Mercado Pago, which is MercadoLibre's digital payments platform, but deeply integrated within the MercadoLibre ecosystem. Sticking with the comparison theme, it's quite similar to PayPal (PYPL) (which I previously wrote an article on here ), but specific to MercadoLibre and the Latin American market. Obviously, this is a downside as it means that it will have difficulties being adopted outside of Latin America - but its weakness is also its strength. People who want to buy items on MercadoLibre MarketPlace will decide to use Mercado Pago. On the other hand, people who want to use Mercado Pago will buy things on MercadoLibre MarketPlace. Both of these act in turn to attract and retain customers, and therefore boost revenue and profit. However don't just take my word for it, see the below screenshot from MercadoLibre's Q3 investor presentation. Total Payment Volume (TPV) in my opinion is the most important metric used to measure the success of a digital payment platform and has been rapidly increasing each quarter. In Q3 of 2022, this was measured at $32.2 billion and has now grown to $47.3 billion in Q3 of 2023 - an increase of 46.9% y/y. This should continue to increase as the Latin American market continues to develop. Another interesting point is the amount of unique users that are on the fintech platform rose to 48.4 million in Q3. Considering that Latin America currently has around 300 million online purchasers, Mercado Pago accounts for around 16% of the market, which is not bad at all.

MercadoLibre's Q3 Investor Presentation

The second part of their sticky business platform is Mercado Envios logistics. Once a customer buys a product via Mercado Libre MarketPlace and pays with it via Mercado Pago, they will then have it delivered to them through MercadoLibre's logistics network. This network is also extremely competitive within the Latin American Market. As of Q3, Mercado Libre accounts for 48% of all shipments across its jurisdiction. Also, its total managed network penetration reached a record level of 94.2%, which is great to see them keeping everything in-house and maintaining a level of control.

There is also a great opportunity with MercadoLibre ads and Mercado Shops. While I don't expect either of these two to take over the world anytime soon, they definitely will have a spot within the Latin American Market. Considering the current population of Latin America is 650 million (nearly double the population of the USA), there should be a decent slice of revenue they can grab. However, it is hard to measure how much this will be considering Amazon, Meta and Google practically dominate the advertising industry worldwide. Mercado Shops on the other hand I expect to perform well, as it integrates well within their business model. Customers will buy items through Mercado Pago from stores set up on Mercado Shops and have them delivered via Mercado Envois logistics.

Overall, MercadoLibre has a powerful ecosystem that can attract and retain customers and in turn will be difficult to disrupt. This is because once a consumer has been exposed to the system, it will be very difficult for another company to convince them the grass is greener elsewhere, which shows up in the impressive double-digit growth rates.

What about MercadoLibre's management team?

MercadoLibre's management team has proven they are capable of executing their business model. There was a recent shakeup with Martín de los Santos taking over as the new CFO from Pedro Arnt in August 2023. There is both good and bad news with this change. The good news is that Martín has been with MercadoLibre since 2007 as a board member, which shows loyalty. The bad news is that MercadoLibre has been executing extremely well, so seeing a potential change in how they perform isn't exactly ideal. I believe Martín will do well, however, we'll need to double-check his performance in both the upcoming quarter and Q1 of 2024.

Otherwise, Marcos Galperin (the CEO) has done a wonderful job building this company up from scratch and running it today, so hopefully he will stay around for as long as he can.

What about MercadoLibre's financial position?

MercadoLibre's financials are in a very good position. For the full year 2022, they printed over $2.49 billion in FCF and $9.54 in EPS. These numbers have already been beaten in the first 3 quarters of 2023, as they've so far reported $2.88 billion in FCF and a whopping $16.29 in EPS. While no guidance has been provided for Q4, I would expect this to be a record quarter for MercadoLibre due to their proven growth strategy and all the main consuming holidays being located in this quarter (including Black Friday and Cyber Monday).

Regarding their balance sheet, MercadoLibre currently has $5.49 billion in cash and cash equivalents and $2.14 billion in long-term debt. This means if they wanted to, they could pay off all their debt relatively quickly and still have cash to burn. Please see my below summary of MercadoLibre's key metrics:

Author's Calculations

At first glance, this stock looks extremely overvalued, but looks can be deceiving. MercadoLibre typically trades with a trailing P/E in the 40 to 90 range. Given the current TTM P/E of 80 we're definitely towards the upper end of the range, however keep in mind the growth rate this company is experiencing - which is demonstrated by the exceptionally low PEG ratio of 0.43

MercadoLibre also typically trades with a trailing EV/EBITDA of 30 to 90 - so currently TTM EV/EBITDA of 31.12 we appear to be trading cheap - not in absolute terms at least, but in relative terms. The industry median trailing P/E and EV/EBITDA ratios are approximately 14.5 and 11.1 respectively, which MercadoLibre is obviously trading above. Overall, these are clearly mixed results.

Regarding the balance sheet ratios, nearly all of these are good with some being quite excellent that are incredibly rare to see. A TTM RoE of 36% is definitely top tier and there is a strong FCF yield. The current and quick ratios above 1.0 also indicate there is a low financial risk to the company. The P/B ratio is extremely high at 28.96, however, the only hard assets they really have are their warehousing/storage units - and their PP&E marks up approximately 7% of their total assets for reference. Overall, MercadoLibre has placed itself in a position of strength.

What's MercadoLibre's intrinsic value?

As per my last article, I've also decided to undertake 3 different approaches to determine the fair value per share of MercadoLibre's stock. I've also put together the below financial projections based on where I believe MercadoLibre is headed:

Historical financials and projections

Author's Calculations

As mentioned earlier, no official guidance has been provided. I do believe however that MercadoLibre will continue to grow revenue rapidly based not only on their proven past performance but also due to the rapidly growing Latin American markets, the penetration they have developed within these markets, and of course, the quality services they provide to their customers. However, to be on the safe side, I've rapidly decreased their y/y growth percentages to reach 11% by 2028.

I would also expect margin expansion to continue at a constant rate, as MercadoLibre expands and cost-cutting measures come into play - boosted by the typical benefits of having an integrated ecosystem working in conjunction with an economy of scale.

Net income analysis

Author's Calculations

I've decided that a current fair P/E for MercadoLibre is around 60. While this is definitely quite high, I believe that their strong financial position and growth rates demand this premium. In comparison, Amazon is currently trading with a forward P/E of around 55, which is close to the 60 I chose. Remember, with the growth rates they should be putting up, this time next year their current 67 P/E will drop to around 45.

Assuming they hit my projected net income of $1.66 billion in 2024, the fair price of MercadoLibre currently should be around $1,974.77 - giving us a 25.78% upside from the current price.

In addition, this 60 P/E implies that the share price will reach $4,764.10 if my projections are correct - which implies a 203.45% return.

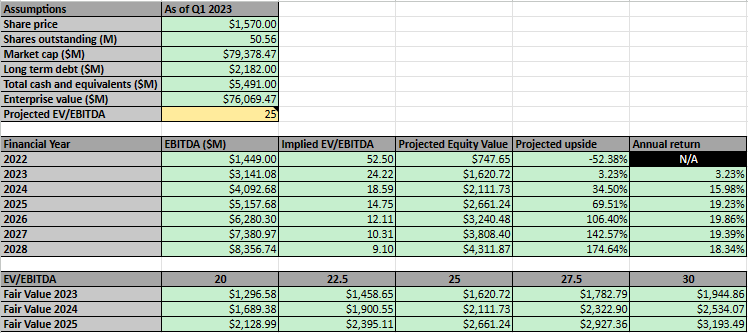

EV/EBITDA analysis

{kind=link}

I've decided that MercadoLibre should have a base case EV/EBITDA of 25. Again, this is relatively high, but for the same reasons as above, I think that this premium is deserved. In addition, this is actually lower than their current projected forward EV/EBITDA of around 28.5, which means this isn't out of the running.

Using this, the fair value for MercadoLibre should be around $2,111.73 per share based on the EBITDA they should be printing for 2024. I've also provided calculations for EV/EBITDA ratios higher/lower than 25 if you'd like this adjusted.

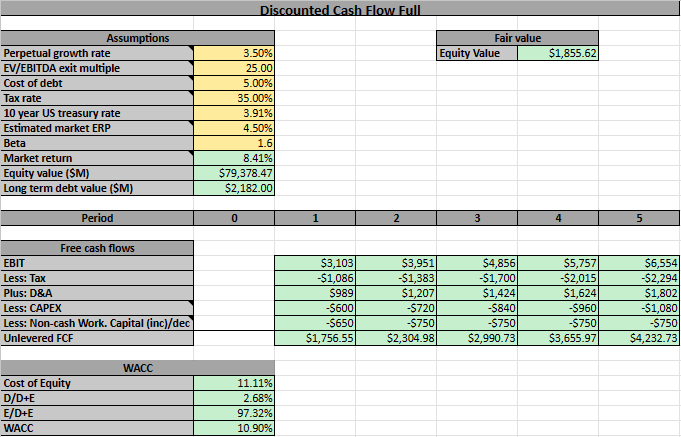

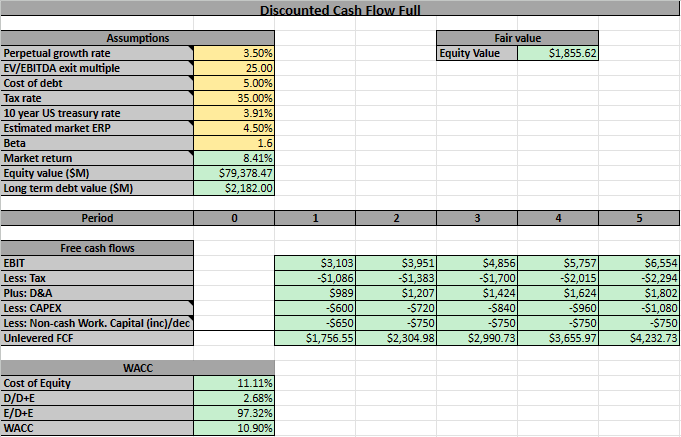

DCF analysis

Please see the below DCF analysis, where I calculated the terminal value using the average of the EV/EBITDA exit multiple method and WACC method:

Author's Calculations Author's Calculations

{kind=link}

{kind=link}

I believe an appropriate perpetual growth rate for MercadoLibre is 3.5%. This is not only due to the rapidly growing industries this company operates in but also that they're specific to the Latin American market that is anticipated to go through a rapid development cycle. I think 3.5% is more than fair.

Their cost of debt was estimated using their latest 10-Q and I used an effective tax rate of 35% based on what they've historically paid. For the risk-free rate, I've decided on using the 10-year US treasury rate, which was 3.91% at the time of writing.

MercadoLibre's current beta is 1.6 and I used a market return of 8.41%, which I calculated based on the current estimated market ERP (around 4.5%)

I've run the calculations and found a fair share price of approximately $1,855.62. Just like in my previous article, I've provided the below sensitivity analysis, if you think I've been too aggressive/conservative.

Author's Calculations

Average share price

Taking the averages from these 3 methods, I've found an intrinsic value for MercadoLibre's share price of $1,980.70, which is a 26.16% upside from the current share price.

Author's Calculations

What are the risks to MercadoLibre?

Like any company, there are of course risks to MercadoLibre's business model which will affect my projections

Firstly, as I hinted at earlier, competition is incredibly tough in both the e-commerce and fintech space. MercadoLibre is going to be competing in their market against the likes of Alibaba, Sea Limited and of course, Amazon. MercadoLibre is currently holding its own and has grown market share since 2020, however if they drop the ball or companies like Alibaba and Amazon decide to shovel their millions of dollars into attacking the Latin American market - it could spell big trouble for MercadoLibre.

Secondly, there is economic risk in general. Of course, MercadoLibre has shown they can still perform well even in a tough economic environment, as the South American economy has been doing poorly since 2020, so I believe this risk is low overall. However, inflation has also been a hot topic recently and Argentina has been hit heavily - reporting inflation rates of over 100%. While this is obviously bad for Argentina's economy, MercadoLibre does get a positive side from this. Mercado Pago became a way to fight against inflation by trading the Argentine Peso for safer assets and protecting their customers' net worth. In turn, this increased the adoption rate of Mercado Pago.

Thirdly, political/regulatory risks. Counties outside of the West aren't typically known for running free and fair democracies - and South America is no exception. If some of the countries MercadoLibre operates in start to become more aggressive on the political stage, or they start to unfairly push through regulations - then there may be downstream (or perhaps even purposeful) effects on MercadoLibre's performance.

Conclusion

Based on the analysis I've conducted, I believe MercadoLibre is currently undervalued and therefore a buy. The company has a strong history of proven outperformance as well as a promising future with realistic growth and profit ventures ahead.

I think the only real risks to MercadoLibre are competition and the general economic environment they operate in. Competition wise, they'll need to ensure they keep tabs on what the likes of the big boys are doing, such as Alibaba and Amazon. One day, at least one of them will likely decide to open the floodgates and strike hard at the Latin American market - a day that MercadoLibre needs to be anticipating and prepared for. Regarding the economic risk, they have proven they can execute in poor economic environments after showing their performance post-2020. However, a weaker economy in general is never ideal for e-commerce or fintech companies. This is especially true if events occur in Latin America that cause an overall slowdown in how they develop their economy/infrastructure, such as a change in leadership that pushes political instability or regulatory frameworks.

All in all, the thing that I like most about MercadoLibre is that it's a fantastic hold for the long term. We have countless examples of how investors benefit from buying fantastic companies while they're still in their growth phase and are now reaping the rewards 10 years later. When I think about the position MercadoLibre will be in if they continue executing for the next 10 years, then this will just become another example of people wishing they had bought in.

For further details see:

MercadoLibre: An Undervalued Overachiever