MELI - MercadoLibre: Downgrading Stock On Argentina Risks

2023-04-29 06:35:42 ET

Summary

- MercadoLibre continues to generate strong top and bottom line growth even as e-commerce peers lap tough comps.

- The company has benefited from an increase in 3P sales.

- The stock does not look expensive considering the strong balance sheet and profitability.

- I am concerned about the interest and inflation rate situation in Argentina and the stock has not priced in such risks.

MercadoLibre ( MELI ) has bounced strongly off the lows as the Latin America e-commerce juggernaut continues to deliver strong profitable growth. In spite of a tough macro environment and tough comparables, MELI has somehow continued to grow GMV and increase profit margins. MELI appears to be benefiting from increased adoption of e-commerce in Latin America and has made substantial progress in improving the profitability of its credit portfolio. Yet, with the stock trading sharply higher since my last report, investors may begin to place greater attention on the absurdly high interest rates in its home country of Argentina. While I remain optimistic for the long-term outlook for the company, I must move to the sidelines as the risk-reward proposition is no longer favorable.

MELI Stock Price

After a strong bounce from the lows, MELI represents one of the few e-commerce stocks which are trading sharply higher than pre-pandemic levels.

I last covered MELI stock in January where I rated it a buy on account of the robust growth rates and solid profit margins. The stock has since returned around 40% and I must now withdraw my buy rating.

MELI Stock Key Metrics

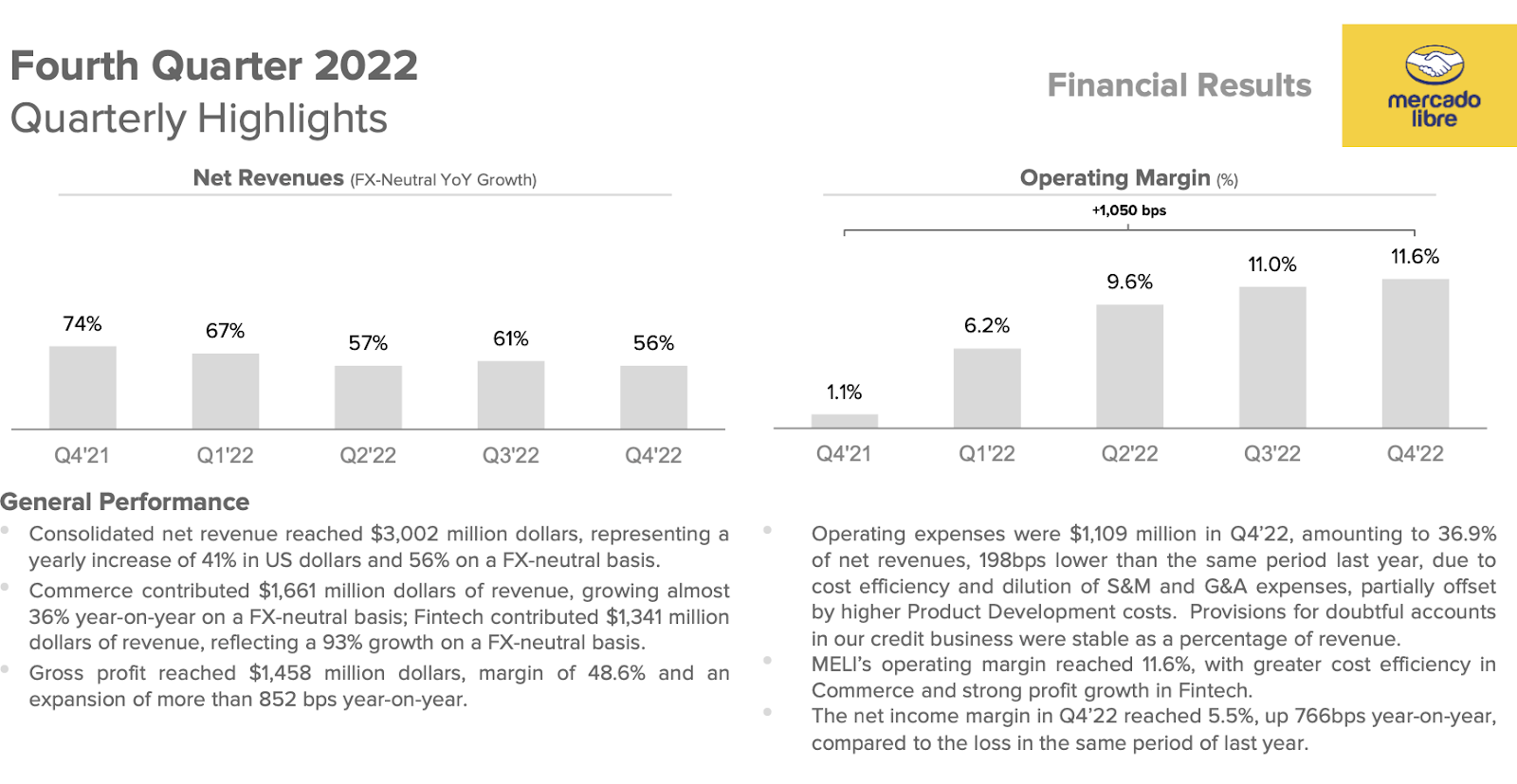

There have already been many quarters in which e-commerce operators started to show steep deceleration in growth rates as they lapped tough comparables. Even so, MELI has somehow been able to sustain rapid growth, with its most recent quarter showing 35% GMV growth.

{kind=link}

Revenues grew by 56% YOY on a currency neutral basis in large part due to 93% YOY growth in the fintech business (again on a currency neutral basis).

{kind=link}

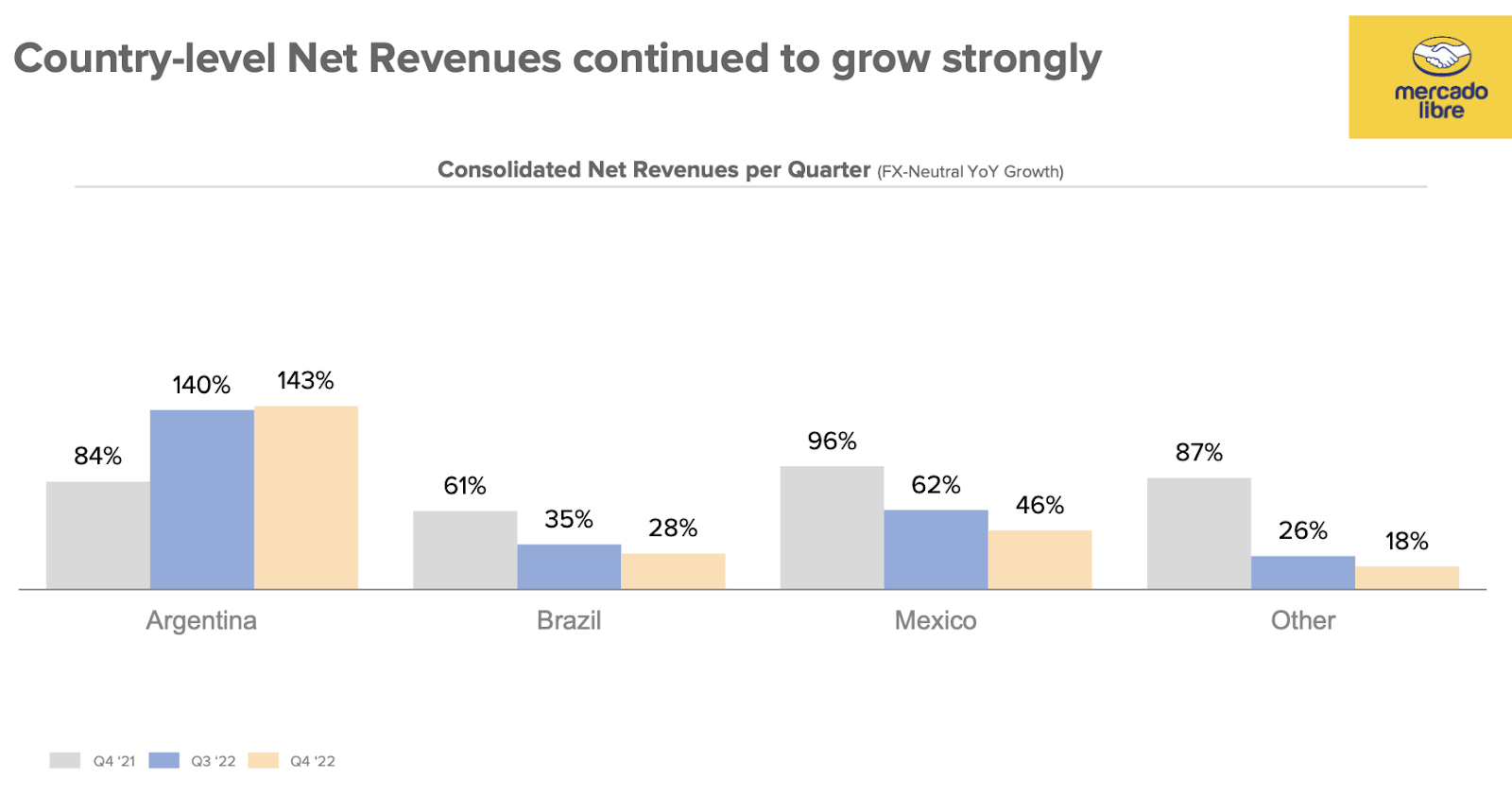

MELI’s strong growth relative to US peers can be explained by the fact that e-commerce penetration in Latin America remains around half of that in the US . Thus, while MELI is undoubtedly lapping tough pandemic comps, it is still benefiting from increasing adoption of e-commerce. MELI’s strong growth came from its core markets, with Argentina leading the way with a stunning 143% YOY growth rate in the quarter.

{kind=link}

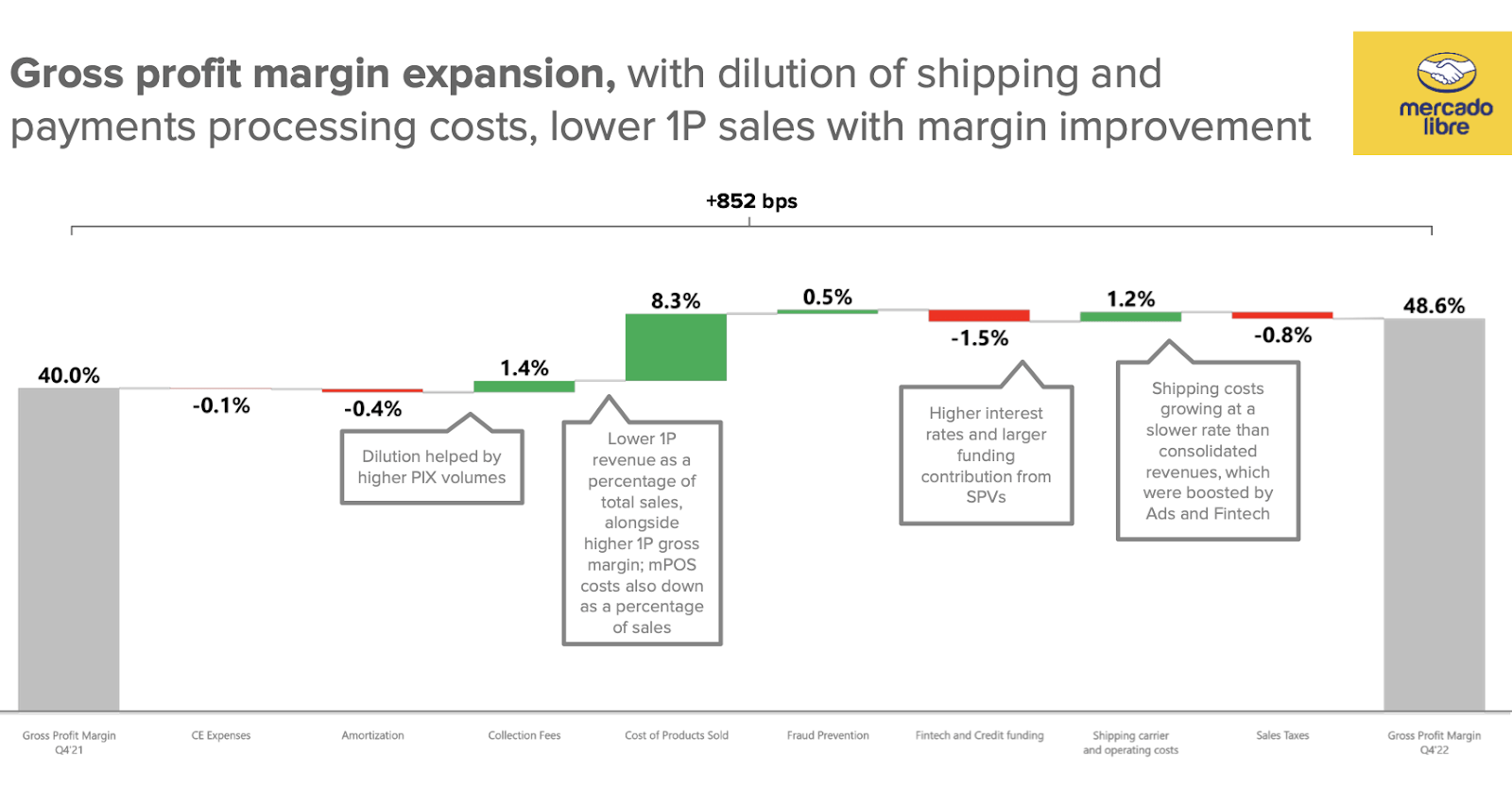

MELI was able to increase its gross margin by 852 bps to 48.6%, driven in large part due to lower 1P sales.

{kind=link}

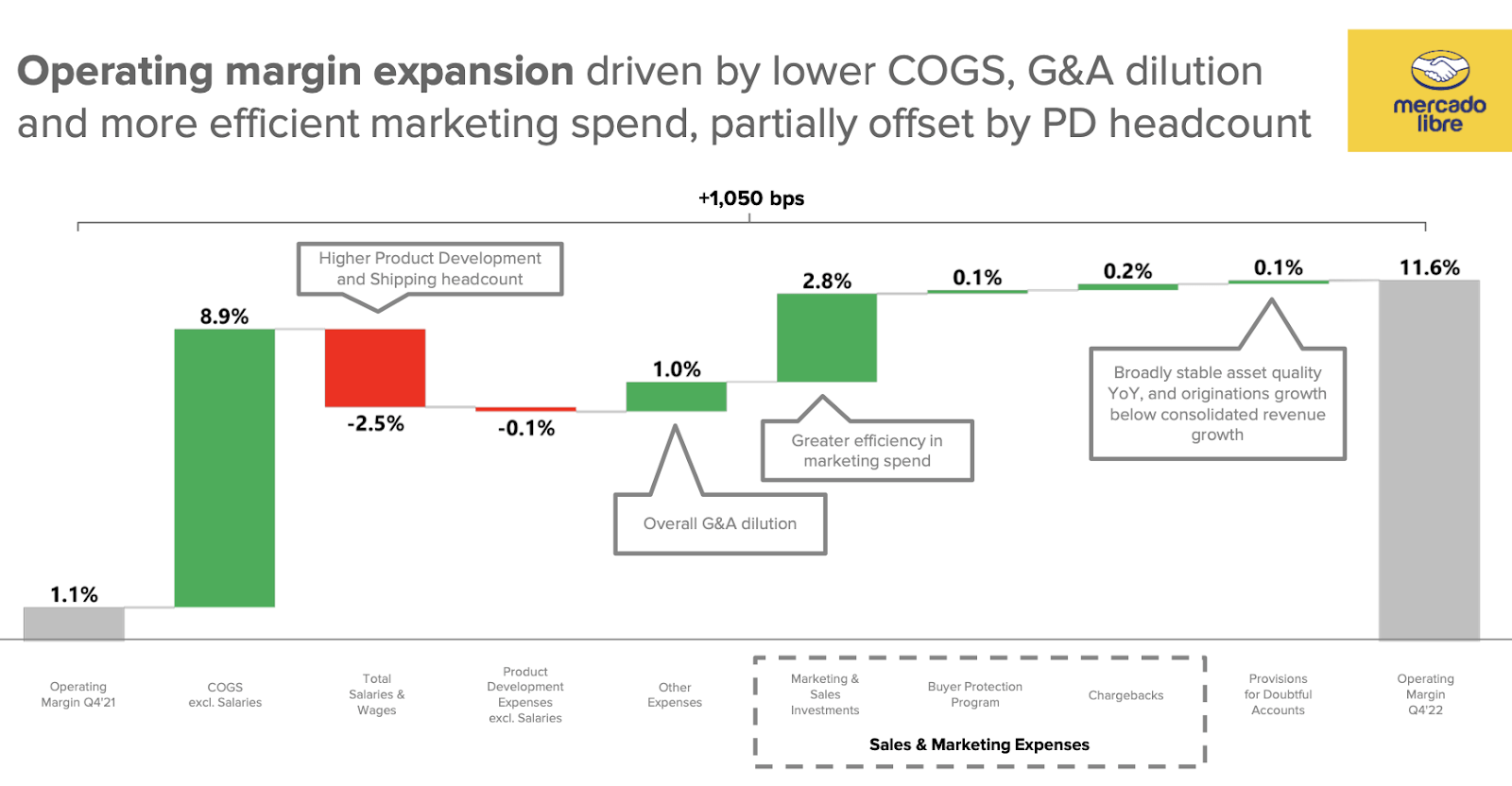

That in turn helped operating margins expand by 1,050 bps as the company also realized benefits from improved efficiency. Many tech companies are trying to appease shareholders by offsetting muted top-line growth with margin expansion. MELI is delivering margin expansion on top of strong revenue growth - because they can.

{kind=link}

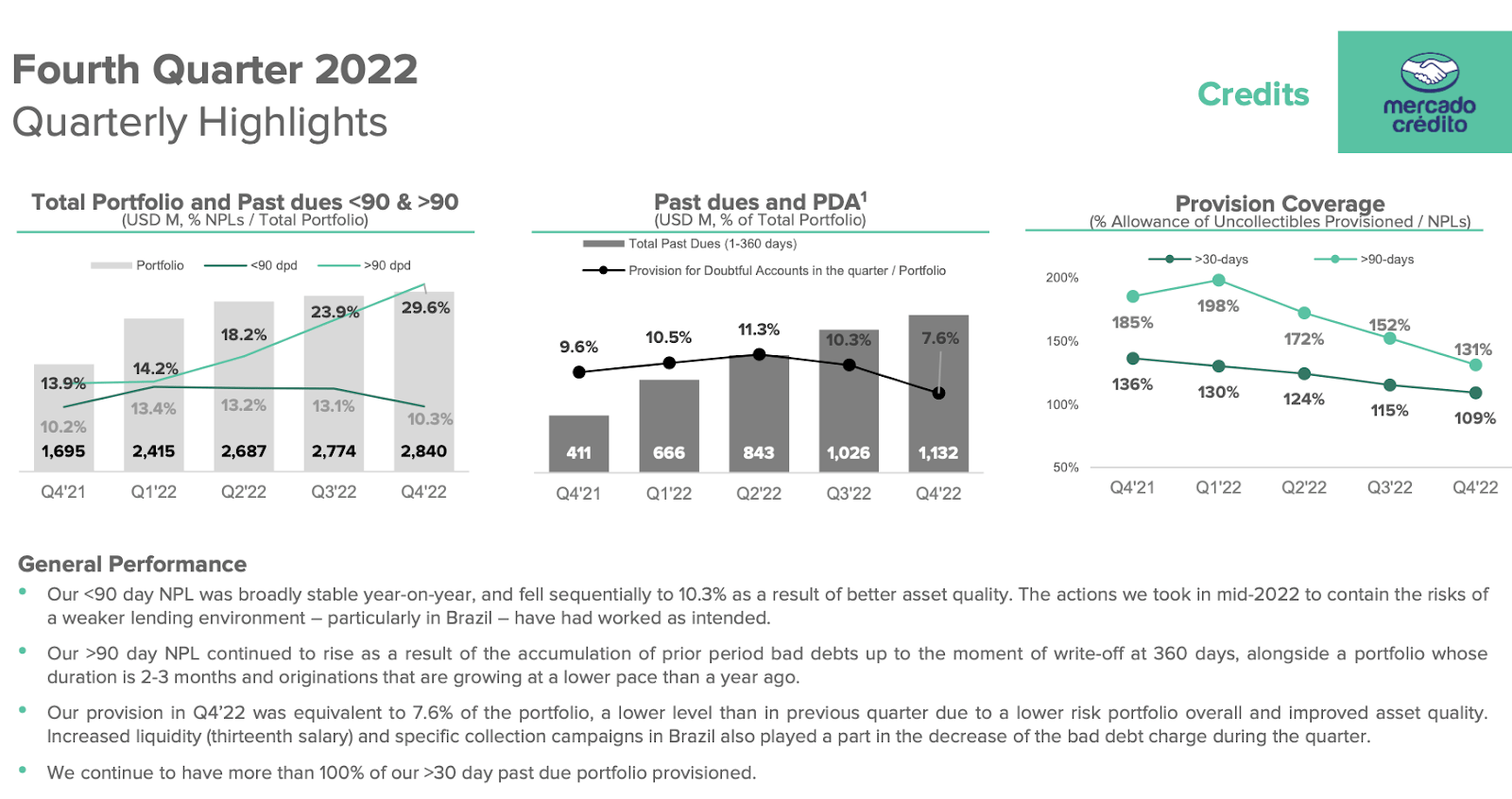

I have previously highlighted the potentially poor credit quality of MELI’s credit portfolio. MELI saw a sharp improvement in credit quality which led to its provision coverage declining precipitously.

{kind=link}

On the conference call , management reminded analysts that they had identified worsening market conditions two quarters prior. They had taken proactive steps to reduce exposure to higher-risk segments. That in turn led to lower NPLs, meaning that as they originated lower risk loans, provisions for those new loans were lower as well. Management noted that if market conditions improved, then they might consider increasing the aggressiveness of their lending platform to increase growth rates, but that time has not come yet.

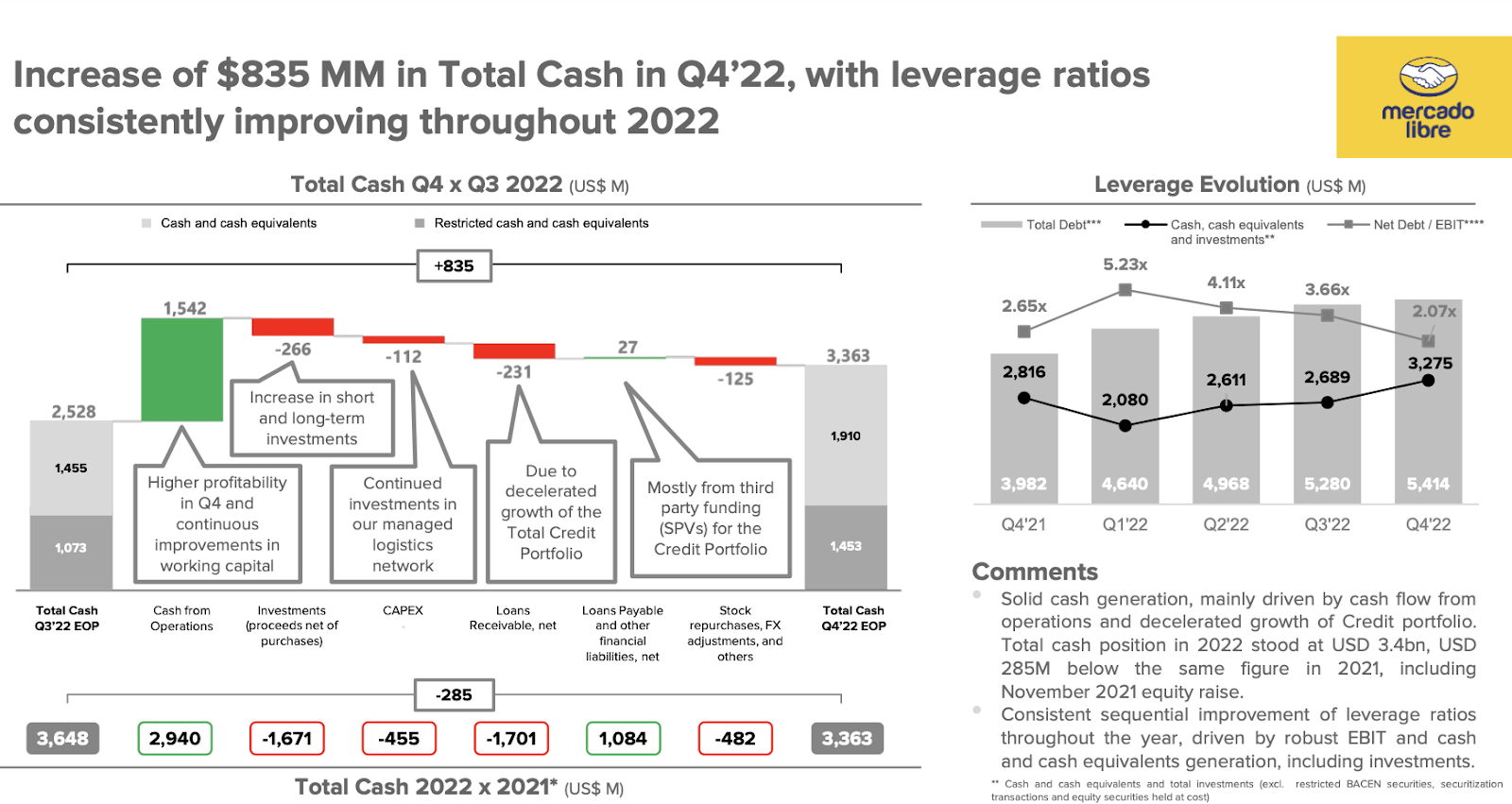

MELI ended the quarter with a strong balance sheet position. The company noted its leverage ratio as being 2.07x debt to EBIT but I note that this has not given credit to an additional $2.3 billion in short term investments.

{kind=link}

As many tech peers are taking advantage of the environment to undergo layoffs, management noted that there is “no downsizing necessary” because they had been disciplined in hiring over the past few years. Management did note that they the rate of hiring might slow down, but it is clear that the company is coming from a position of strength as they have shown an ability to drive both top and bottom-line growth in the current environment.

Is MELI Stock A Buy, Sell, or Hold?

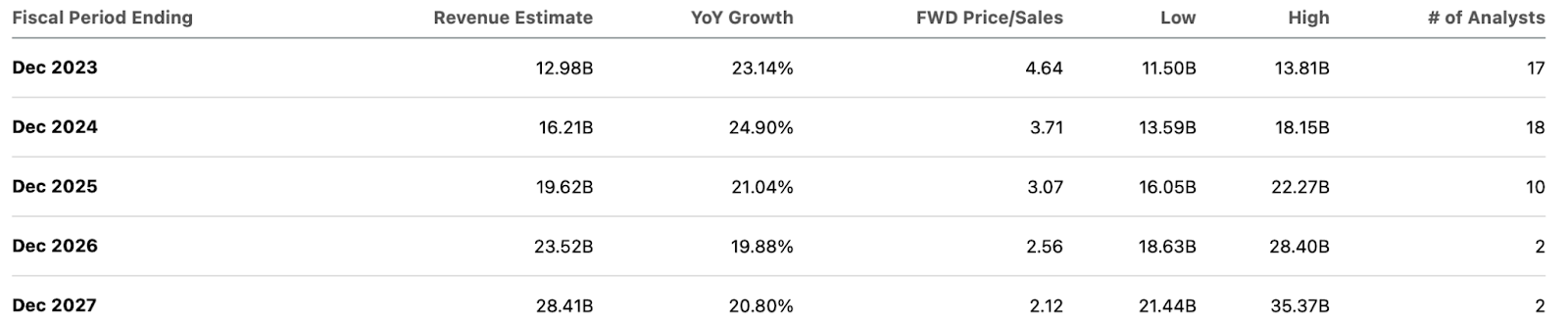

After the recent rally, MELI finds itself trading at around 4.6x sales. That is a fairly reasonable multiple considering the projected 20% growth rate moving forward.

{kind=link}

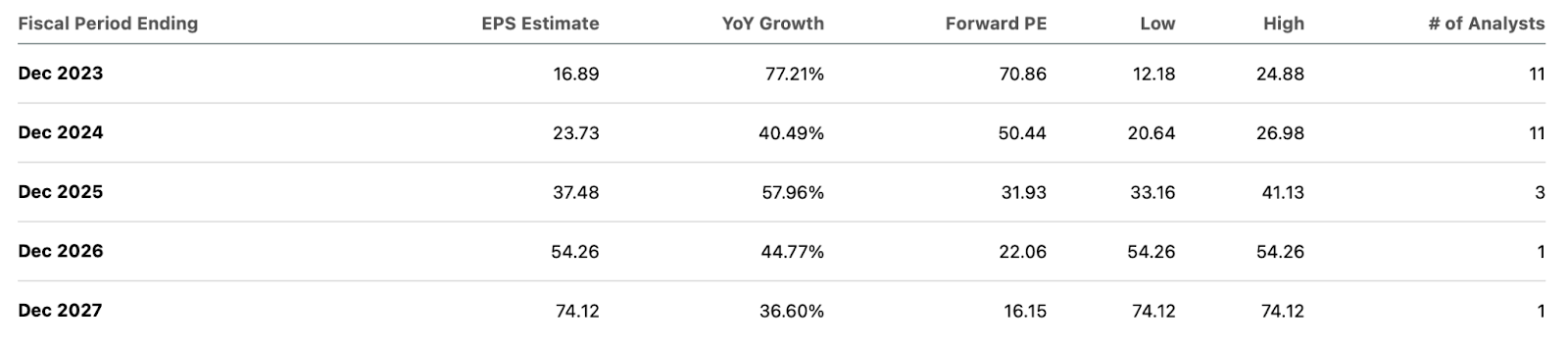

MELI is trading at 71x earnings with earnings expected to grow significantly faster than revenues over the coming years.

{kind=link}

Based on my assumptions of 20% long term net margins, 20% growth, and a 1.5x price to earnings growth ratio (‘PEG ratio’), I could see MELI trading at 6x sales, implying a stock price of $1532 per share. That still represents sizable upside and there remains a sizable growth opportunity ahead. Yet I am downgrading the stock from buy to hold. While I acknowledge the possibility of geographic bias, at these higher stock prices MELI may be more susceptible to risks stemming from high interest rates. In particular, its home country of Argentina has recently increased interest rates 300 bps to 78% as inflation hit 100%. Those are not typos. Meanwhile, Mexico and Brazil already have interest rates in the double-digits. While MELI appears poised to benefit from the long term growth of e-commerce in Latin America, I cannot ignore the nagging feeling that financial distress is just around the corner. Considering the deep discount that Chinese e-commerce operator Alibaba ( BABA ) trades at, I am of the view that MELI stock has not appropriately discounted these international risks. While MELI may see some near term boosts due to the bankruptcy of Brazilian competitor Americanas , I suspect that the high interest rates will still weigh on sentiment and the stock may face great downward pressure until the interest rate situation is resolved. I rate the stock a hold as I await a greater margin of safety.

For further details see:

MercadoLibre: Downgrading Stock On Argentina Risks