MELI - MercadoLibre: How To Play Argentina's Bold Economic Experiment

2023-12-26 01:57:23 ET

Summary

- Argentina is going through a radical transformation. We will go through the key points on how to understand it and how to play it.

- We will go through the accounting implications of hyperinflationary reporting to the multiple FX in Argentina.

- Discover why I am picking this E-commerce and Fintech Giant as the top contender on a risk-adjusted basis for Argentina.

Nobel laureate Simon Kuznets argued that the world has four types of economies: developed, underdeveloped, Japan, and Argentina. This has never been more accurate than today, when understanding the Argentinian economy will lead us to analyze unique periods, relatively obscure economies, and philosophical premises like the nature of money and the psychological biases of loss aversion.

Nevertheless, understanding this context is vital to discovering how to play the Argentinian economy and substantial market distortions that will shift in 2024 and beyond.

The article will go through the complexities of the Argentinian situation and the rationale for picking MercadoLibre (MELI) as the best risk-adjusted way to profit from this trend.

The Election, Dollarization and Futurology

After three rounds of elections, Argentina elected Javier Milei, a self-described Libertarian anarcho-capitalist, as the new president. His plan has many controversial proposals for the social reorganization of Argentina, but we will focus on his economic plan, proposals, and problems.

The problems are many and complex. At the time of the elections, Argentina had reported inflation above 140% , with 40% of its population in the poverty line, negative reserves, and substantial debts with the IMF.

All these issues are made even more complex because of the many regulations that Argentina has imposed to try to control these issues. We will focus on some of the most important.

- Price ceilings on goods . Inflation is measured using this basket of goods as a reference, suggesting a higher real inflation than the one reported.

Argentina - 200 USD in ARS (My Photos)

{kind=link}

- Strict Control of foreign exchange rate . This has led to many different exchange rates depending on what they are used for, between the "official rate," which at the time of the election traded around $350 Ars/USD, to the street exchange rate Dollar-Blue, which was around $1,000 Ars/USD. There are many other exchange rates like the Qatar-Dollar used for World Cup items, ColdPlay-Dollar used for concerts, MEP for credit cards, and Cripto-Dollar tied to stablecoins in Argentina. In the first two weeks from the start of its presidency, the official rate depreciated more than 150% to around $900 Ars/USD, and almost all exchange rates are converging in the 900-100 range, which is a significant prowess.

- Tariffs, Taxes, and Transfers. The country has many taxes or particular exchange rates for exports, imports, and money coming in and out of the country. It also has budgetary burdensome programs to transfer money to the population. These significantly modify the supply and demand curve of goods and make forecasting demand and supply shocks.

Milei's proposals to address these issues are to:

- Reduce government spending and bring the budget back to Control.

- Eliminate or cut regulations on imports and exports.

- Then, allow the free flow of currency, eliminating the many exchange rates, which would likely depreciate the currency, increasing exports and decreasing imports.

- Dolarize the economy. To Switch the Argentinian peso for the US dollar.

The first three points depend solely on the Argentinian government. So, their implementation is likely to occur in some form. The effectiveness and reach of the measures depend on the president's ability to use his office and convince the legislative power to pass meaningful reforms.

While its party is new and does not hold the majority in the legislative branch, the surprisingly strong election results will likely buy him enough political cash to maneuver meaningful changes in the short term.

However, by his own admission and economic principles, 2024 would result in a challenging and volatile economic environment, with higher inflation resulting from eliminating price ceilings, reduced government spending, and the uncertainty of opening the free flow of currency.

The problems in achieving this turnaround stem from the complexity of executing a radical transformation without reducing the already deteriorating country's economy and balancing the perception that the economy is worsening in the short term, as it will likely occur in 2024, with the improving prospects of the country in the long term.

The Dollarization

While the first three proposals are the easiest ones to implement, the issue with the Argentinian economy is that the country varies widely in its policies and willingness to meet its financial obligations.

Argentina has a history of cyclical crises, starting with high inflation environments followed by radical reform and drastic monetary and fiscal measures that create a temporary period of prosperity that eventually decelerates and is kept alive by optimistic overspending and inflation, where the cycle repeats itself, and where we stand right now.

So, while the first three points alone could be seen only as a temporary improvement, in one country's periodic crisis, the dollarization of the economy could be the critical element that cements these changes in the long term.

Dollarization is not a magical solution to Argentina's problems, nor does it mean eliminating monetary policy. However, it substantially restricts the monetary policy and creates boundaries on the budgetary deficit.

Proponents of dollarization argue that loosening monetary and fiscal policy flexibility is not desirable. However, it is compensated with increased confidence in the international markets, reduced inflation, and a return to a non-hyperinflationary economy.

"Give me a one-handed Economist. All my economists say 'on hand...', then 'but on the other..." ? Harry Truman

On the other hand, many economists argue that dollarization will result in similar issues that have occurred in Zimbabwe, where dollarization of the economy did not happen in total, and the dual currency system has only led to more complex problems to solve and fewer tools to sustain a healthy fiscal policy.

However, there seem to be more consequences of not dollarizing the economy unsuccessfully rather than reasons why Argentina should not dollarize its economy. So the real issue is whether Argentina has what it takes to dollarize the economy successfully and at what cost it will be able to do it.

One of the biggest obstacles is whether Argentina has enough dollars to make the transition physically and in real terms. The physical issue of having dollars has been overblown, as the renowned CFA Charter Holders podcast " Money Talks " explained, comparing this issue to the one that occurred during the post-war in Bosnia. Bosnia had no physical currency and decided to implement the German Mark as its currency, which led the governments to arrange transportation of bills using convoys from Frankfurt to supply banks with enough currency to circulate in the economy.

The issue of having real dollars is more complex. If the country cannot sustain a stable exchange rate due to mistrust in the economy's future, a "bank run" could occur where dollars fly outside the country.

This is similar to the money availability paradox. In a large city, if there were only one ATM, people feel scarcity and take out large sums each time, which would require extraordinary amounts of cash to sustain the ATM demand, and in turn, large amounts of money would circulate in the economy. In contrast, if there were one ATM in each street, people would feel abundance and would not use it as much, and the amount of cash required would reduce the more available it is.

Argentina has to have enough dollars to sustain the feeling of abundance in the economy and for companies and entities to trust in the country's long-term prospects instead of the short-term opportunity to release previously trapped funds.

Here, there are factors that I believe will tilt the scale towards a successful and prompt dollarization of the economy.

1.- The "Corralito" effect, since 2001, has created mistrust in the banking system of the Argentinian economy, especially when it comes to dollars. The Argentinian population habitually saves dollars in cash under the proverbial mattress. So, while official accounts estimate a hefty $30bn dollar gap that the country would require to dollarize the economy, that gap could be much lower, as one of Milei's advisors argues , and was the case in Ecuador's dollarization. Where the reserves of dollars that the population had tilted the balance and hastened the transition.

2.- From the IMF to many other institutions and companies have bet on the long-term recovery of the Argentinian economy, maintaining franchises and IP in the country, hoping for a return to the golden age of Argentinian prosperity, and now would be the time to put the bet to the test, and many will double down.

If you owe the bank $100 that's your problem. If you owe the bank $100 million, that's the bank's problem. - J. Paul Getty

This shared stake in the recovery makes it more likely that the government can obtain a $30-40 billion loan.

3.- The high sophistication of the Argentinian economy and reliance on electronic methods. Argentina's cyclical crisis and extreme events like the Corralito, the temporary peg of the Argentinian peso to the US Dollar in the early 90s, and other extreme devaluations have made the population highly sophisticated in the use of nontraditional banking tools and the adoption of electronic methods of payment. While it is hard to measure quantitatively the rapidness of adoption and the average level of sophistication from an empirical and biased viewpoint, it is impressive to see this on the market.

Full disclosure and representativeness bias alert: I am writing this from Argentina, where I have spent the last few weeks. So, the lack of numerical and objective metrics to measure these factors is supplemented with my opinion and impression of the country's situation.

It is impressive to see electronic payments being accepted in small establishments, predominantly led by Mercado Pago from MercadoLibre, Crypto, referenced daily and regularly used for some transactions.

This sophistication will play a favorable part in the likely adoption of dollarization and the ease of adopting this complex process in the population. Whereas in other countries, explaining FX fluctuations and changes in the interest rate payments and impacts on pension plans implied by the dollarization would be a significant hurdle for such a plan to be implemented, the average Argentinian has a higher and perhaps more empirical than theoretical, understanding of these changes. The level of discussion shown in mainstream media is impressive and above what I have seen in most countries.

How Does This Translate to a Stock Idea?

From the list of stocks correlated to the Argentinian economy, Banks like (BMA) might benefit from the dollarization and stabilization of the economy. However, the aforementioned distrust of the Argentinian population in the banking system, the high sophistication of the population in the use of alternative banking methods, and the highly volatile economy make banks a risky proposition with unclear and uncertain ranges and forecasts.

The state-run oil company (YPF) seems attractive at first glance as Milei plans to sell it, which might be done at a premium. However, this is likely priced in the almost 100% jump the company experienced the day of the election results and the uncertainty on when this will happen and at what price.

My pick to play the Argentinian economy is MercadoLibre because of its dominance in the Argentinian e-commerce and Fintech scene and its penetration and adoption of the Argentinian Market of its electronic payment and banking services, Mercado Pago. It is poised to benefit enormously from increased economic growth and a more stable economy while maintaining a solid business outside Argentina, Primarily in Brazil and Mexico, which will provide the company with higher flexibility and stability than other companies that rely exclusively on the Argentinian Economy.

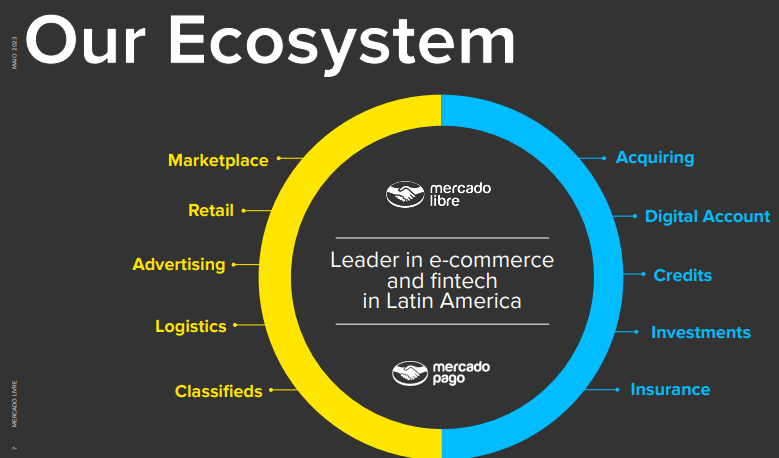

A Closer Look at MercadoLibre

MercadoLibre has two branches. E-commerce (MercadoLibre) and Fintech (Mercado Pago). Their revenue in 2022 was around 55% for the E-commerce and 45% for the Fintech segments.

MercadoLibre Segments (MercadoLibre Investor Relations)

{kind=link}

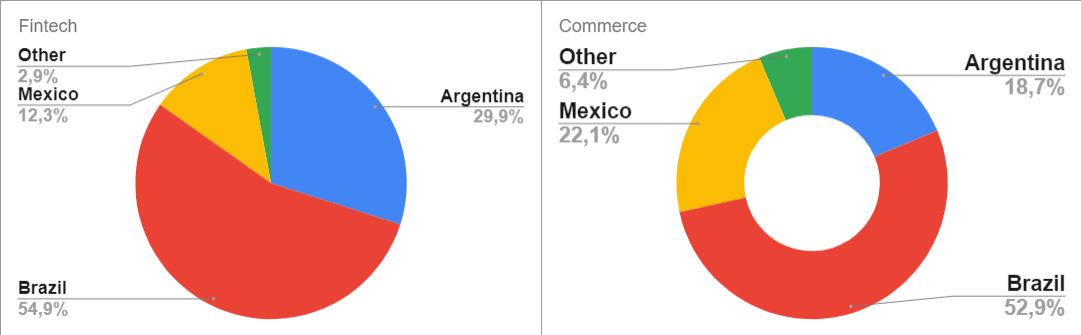

Argentina represents about a quarter of this revenue, at 23% in 2022. While the company does not disclose gross margin info by segment, it is noteworthy that Argentina represents a higher percentage of revenue in Fintech (almost a third of revenue) than in E-commerce (nearly a fourth of revenue).

Revenue by Segment & Country (My charts with 2022 10K)

{kind=link}

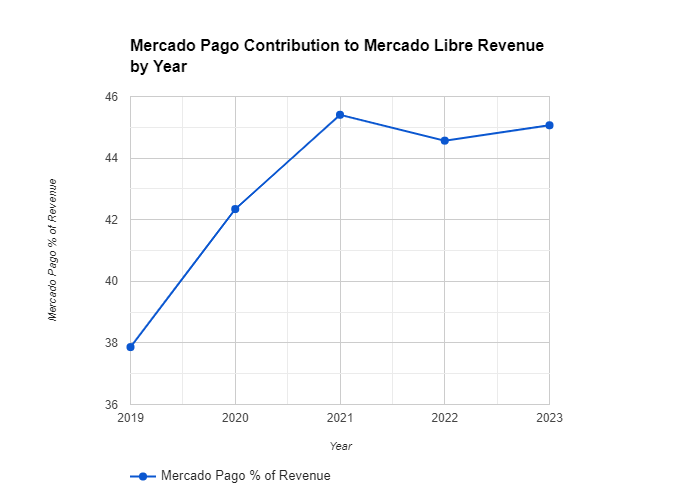

Looking at these charts through the last few years, Mercado Pago has grown more than the e-commerce segment.

Mercado Pago as a % of Revenue (My charts with MercadoLibre Investor relations)

{kind=link}

Mercado Pago's services are plentiful and work well with the e-commerce segment. They have become a staple of Argentinian life, and even the latest round of "presidential decrees of urgent need." (Decreto De Urgencia y Necesidad) will allow the employees to receive their salary directly in Fintech accounts like Mercado Pago. This decree was part of the campaign promises as many users already do this manually to take advantage of the asset management and Monthly interest that Mercado Pago provides.

Mercado Pago also manages Cryptocurrency transactions in other countries , and it is likely that if regulations change in Argentina, it will include its services in the country.

Mercado Pago Services (MercadoLibre IR)

{kind=link}

From an accounting and valuation point of view, the exciting part is that Argentina is reported on a hyperinflationary basis, which adjusts numbers based on the year of reporting inflation, making them arguably more optimistic, somewhat balanced by the highly deteriorating FX rate characteristic of hyperinflationary economies.

All else equal, if Argentina manages to come out of its hyperinflationary status, we might see a reduction of revenue as a percentage of the total in an accounting base; however, on an actual cash basis, the company would effectively receive more money from Argentina than what it is receiving right now. These accounting distortions could be reflected in the 2024-2026 period, as cumulative inflation of the last three years has to be below 100% for an economy not to be considered hyperinflationary.

In the meantime, with free FX conversion and more controlled inflation in 2024-2025, the company might have an optimistic accounting of Argentinian financials and improvement on an actual cash basis paired with a more stable FX rate.

Valuation

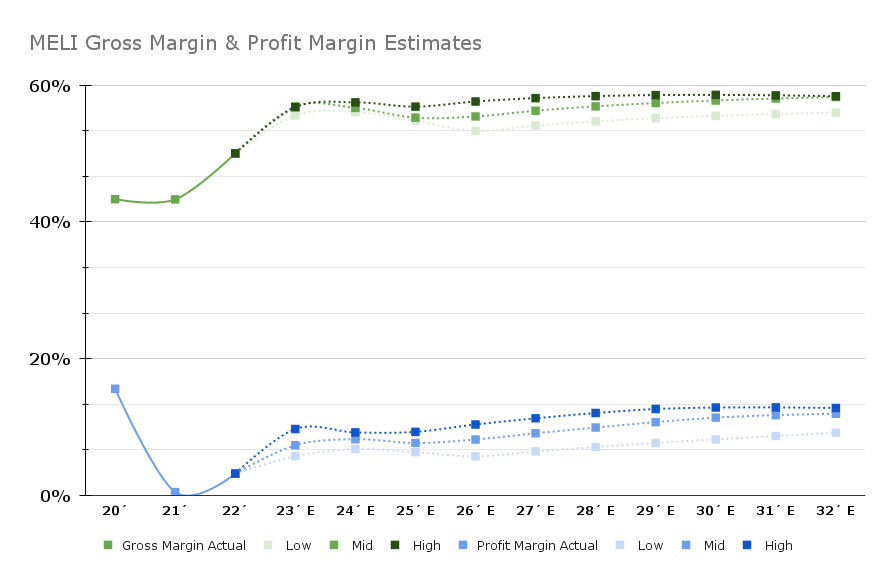

The valuation of MercadoLibre is considering pre-election Macroeconomics and forecasts but considering short-term impacts on the 2024 results.

MercadoLibre Gross and Profit Margin Estimates (My Charts)

{kind=link}

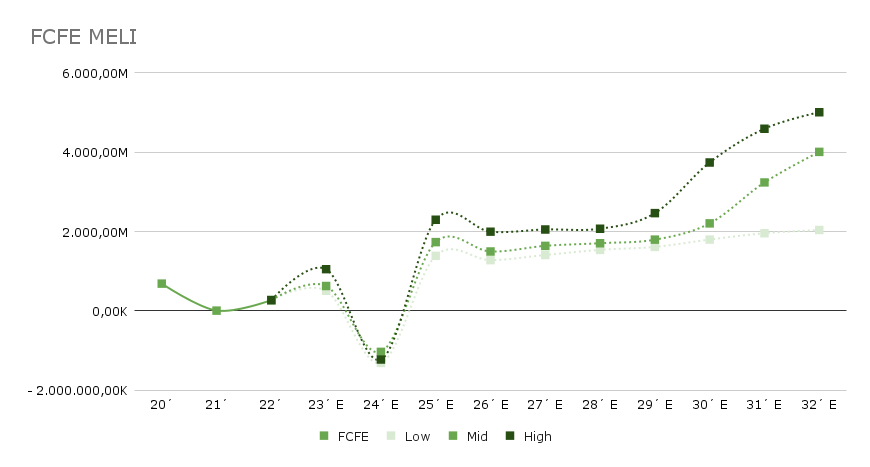

While the drop is not as noticeable in revenue and gross margin estimates, it is more noticeable in the FCFE forecast. This is partially because of accounting standards (IAS29) on hyperinflationary economies that reflect numbers adjusted for the year's inflation.

FCFE estimates MELI (My charts)

{kind=link}

The low side of the valuation shows a lower performance than the mid scenario; however, this is only slightly reflected in the valuation because of perpetuity growth considerations. None of the scenarios reflect the improving conditions of Argentina or the effect that the country's becoming a non-inflationary economy would have on earnings and cash balance.

MELI Fair Value Estimates (My Charts)

With these projections, the fair value of MercadoLibre is close to the current trading price, with a 17% drawdown from the current price but a hefty discount versus the high scenario of about 70%. The stock might be overvalued based on pre-election forecasts; however, the asymmetry between upside and downside is attractive, especially considering the unquantified catalysts of Argentina's new economic conditions.

On the Balance Sheet side, the company has over 5 billion in cash and short-term investments and only 2 billion in Long-term debt. So, the company is in a comfortable position to increase its leverage.

Conclusions

MercadoLibre has cemented a strong moat and deep presence in the Argentinian economy and e-commerce scene. It has proven it can compete with Amazon (AMZN). It has a diverse profile that may allow it to expand in Argentina without putting into question its financial viability or representing substantial risk. The stock is not without risks, and 2024 will be a rollercoaster for the Argentinian economy. Still, the upside more than compensates for the slight overpricing and the variability it will experience in the following years.

As it has been the custom, I will provide perspective on the two Dummy Portfolios: the Tortoise and the Cat.

The Tortoise portfolio would include MercadoLibre as a holding. Playing on the long-term trend of Argentina and the strong moat MercadoLibre has shown in Latin American markets. It focuses on two of the most important trends of the XXI century: The integration of physical and digital realms and the technological convergence across sectors. It is slightly lacking on the green from which this portfolio seeks exposure but does not entail a disqualifying aspect of the stock. The low downside risk coupled with long-term solid prospects, regardless of catalysts in the short term, make it a good fit for the risk profile of the portfolio.

For the Cat portfolio, it is a vital inclusion. With a substantial upside and high uncertainty in the macroeconomic scene, which make it less likely for the securities to trade at a statistically fair value, MercadoLibre is a good candidate for a 2024 play. As the portfolio has shorter-term considerations, a revisit of the position would be required at the end of 2024 to review whether the catalysts have played out.

As for my portfolio, I have been holding MercadoLibre for a few years and will likely increase my position. The company has reached a strong presence in the Latin American market, and in some regards, it has a much stronger presence in these economies than Amazon in the US. Its strong moat, highly innovative services, and adaptability to complex markets make it an impressive company and a strong contender for the king of e-commerce south of the Panama Canal.

Its high-risk tolerance and exploration of new services in banking and crypto are also essential elements for this company, which is often compared to Amazon, to outperform its competitors in the long term.

Editor's Note : This article was submitted as part of Seeking Alpha's Top 2024 Long/Short Pick investment competition , which runs through December 31. With cash prizes, this competition -- open to all contributors -- is one you don't want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!

For further details see:

MercadoLibre: How To Play Argentina's Bold Economic Experiment